GST Payment Under Protest: What ASP Traders Judgment Means

Payment is not, Acceptance..!!

The Constitutional Immunity of Taxpayers Against Coerced Payments

Article 265 of the Constitution of India strictly mandates that "No tax shall be levied or collected except by authority of law". This constitutional safeguard acts as a dual prohibition against arbitrary state action: the law must explicitly authorise both the imposition (levy) of a tax and the procedure for its actual recovery (collection). In this framework, the principle that "Payment ≠ Acceptance" acts as a crucial defense for taxpayers against unjust tax collections.

Recent Supreme Court jurisprudence, specifically the landmark ruling in M/s ASP Traders v. State of Uttar Pradesh (2025), reinforced that the mere payment of a tax or penalty does not legitimise an illegal demand or imply that the taxpayer agrees with the liability. The Court highlighted several core dimensions of this principle under the umbrella of Article 265:

-

Compulsion Does Not Equal Consent: Taxpayers frequently make payments under commercial pressure—for example, paying a penalty to secure the immediate release of detained goods and prevent business losses. The Court clarified that paying to avoid losses is an act of compulsion, not an agreement.

-

No Waiver or Acquiescence in Tax: A taxpayer cannot waive their constitutional rights, nor does their silence or delayed protest validate an illegal tax demand. The Court established that there can be no "acquiescence" in tax matters; the State must strictly justify its actions within the four corners of the law, regardless of whether the taxpayer has already paid the amount.

-

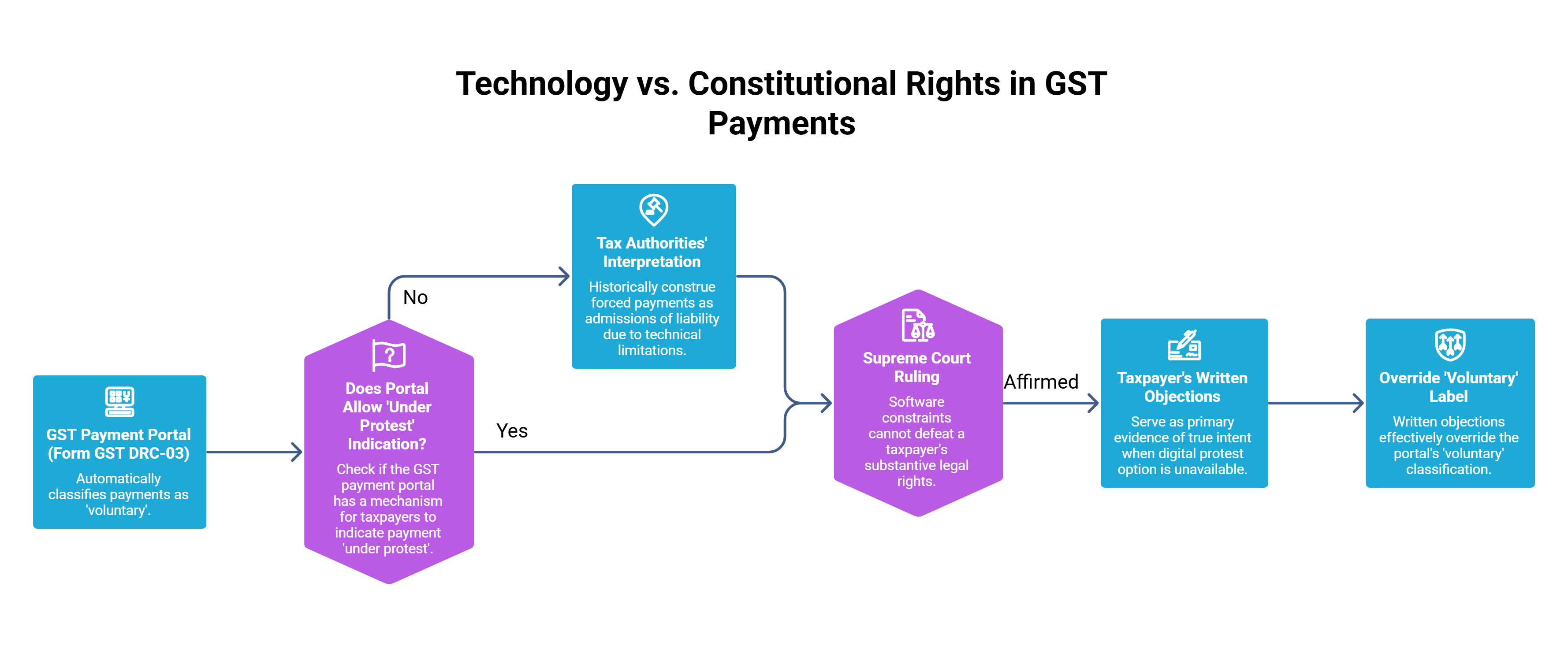

Technology Cannot Defeat Constitutional Rights: A practical challenge arises because the GST payment portal (Form GST DRC-03) automatically classifies disputed GST payments as "voluntary" and lacks a mechanism for the taxpayer to indicate they are paying "under protest". Tax authorities have historically used this technical limitation to construe forced payments as admissions of liability. The Supreme Court struck this down, stating that software constraints cannot defeat a taxpayer's substantive legal rights. When a digital protest option is unavailable, a taxpayer's written objections serve as the primary evidence of their true intent, effectively overriding the portal's "voluntary" label.

-

Mandatory Adjudication is Non-Negotiable: Payment by the taxpayer does not allow the tax authorities to skip proper legal procedures. The Court ruled that "deeming fictions" (where statutes claim proceedings are "deemed to be concluded" upon payment) cannot be used to bypass a formal, reasoned adjudication. Even if a payment is made and the portal marks the case as concluded, authorities are still duty-bound to issue a speaking order that addresses the taxpayer's written contentions. If money is collected without a final reasoned order, it creates a "legal vacuum" making the collection unconstitutional and a direct violation of Article 265. Furthermore, without an official order, a taxpayer cannot exercise their statutory right to appeal, making the collection legally invalid.

In summary, the authority of law requires an unbroken legal chain consisting of valid legislation, correct procedure, a reasoned adjudicating order, and the protection of appellate rights, which is central to any effective GST litigation, audit, and appeal strategy.

If the government relies merely on the fact that a payment was made under pressure or processed as "voluntary" by a computer system, the tax collection collapses under the scrutiny of Article 265.

.png)

ASP Traders vs State of Uttar Pradesh – Supreme Court

(2025) 32 Centax 446 (S.C.)/2025 (100) G.S.T.L. 257 (S.C.)

Civil Appeal No. 9764 of 2025 | 24-July-2025

Where for release of detained goods and conveyances, tax and penalty are paid, whether voluntarily or otherwise, a formal order in Form GST MOV-09 is to be passed after granting an opportunity of being heard, similar to adjudication procedures followed in cases involving GST demand notices under Rule 142 (DRC-01), and a summary of said order in Form GST DRT 07 is to be uploaded.

Penalty - Detention of goods and conveyance in transit - Notice and order - Period 2022 - Due to business exigencies, assessee secured release of intercepted goods and conveyance by paying tax and penalty, reflecting practical issues commonly seen in disputes involving GST penalties and detention proceedings. Penalty relating to detention of goods and conveyance in transit frequently arises from documentation lapses associated with e-way bill requirements under GST and related movement compliance obligations.

No formal order under section 129(3) was passed - Appellant requested such an order but respondent authorities stated that in view of section 129(5), no further order needed to be passed - High Court accepted stand of respondent authorities - HELD : Every show cause notice must culminate in a final, reasoned order - Section 129(5) of CGST Act, 2017 provides that proceedings shall be deemed to be concluded upon payment of tax and penalty - This deeming fiction cannot be interpreted to imply that owner of goods has agreed to waive or abandon right to challenge levy.

Proper officer is duty-bound to pass a formal order in Form GST MOV-09 and upload a summary thereof in Form GST DRC-07 as mandated under Rule 142(5) and C.B.I. & C. Circular No. 41/15/2018-GST, since such orders form the basis for statutory remedies available under GST appeals and revisions under Sections 107–121, so as to enable taxpayer to avail appeal remedy as per law. Once objections are filed, adjudication is not optional, it becomes imperative to pass a speaking order to justify demand of tax and penalty.

Language of section 129(3) is categorical in stating that officer "shall issue a notice and thereafter, pass an order" - Use of words "and thereafter" reinforces mandatory nature of passing a reasoned order, regardless of payment, particularly where protest or dispute is raised - No written material was placed on record to substantiate that objections were orally withdrawn - Written reply would prevail over an oral submission contrary to such written reply.

GST payment portal permits payments only through Form GST DRC-03, which is automatically classified as a voluntary payment, and does not provide any mechanism for an assessee to indicate that payment is being made under protest - Payment made by appellant could not be treated as voluntary, and absence of a mechanism to record protest should not operate to detriment of appellant, especially when objections were already on record and payment was clearly necessitated by business exigencies - Proper officer could not be absolved of statutory obligation to pass a reasoned order in Form GST MOV-09 and upload corresponding summary in Form GST DRC-07 [Section 129 of Central Goods and Services Tax Act, 2017/ Uttar Pradesh Goods and Services Tax Act, 2017].

GST Law GST Payments GST Exemption

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified