The Powers of GST Officers: A Comprehensive Analysis of the Legal Framework for Assessment, Enforcement, and Recovery

1.0 Introduction: The Role and Significance of GST Officers in Tax Administration

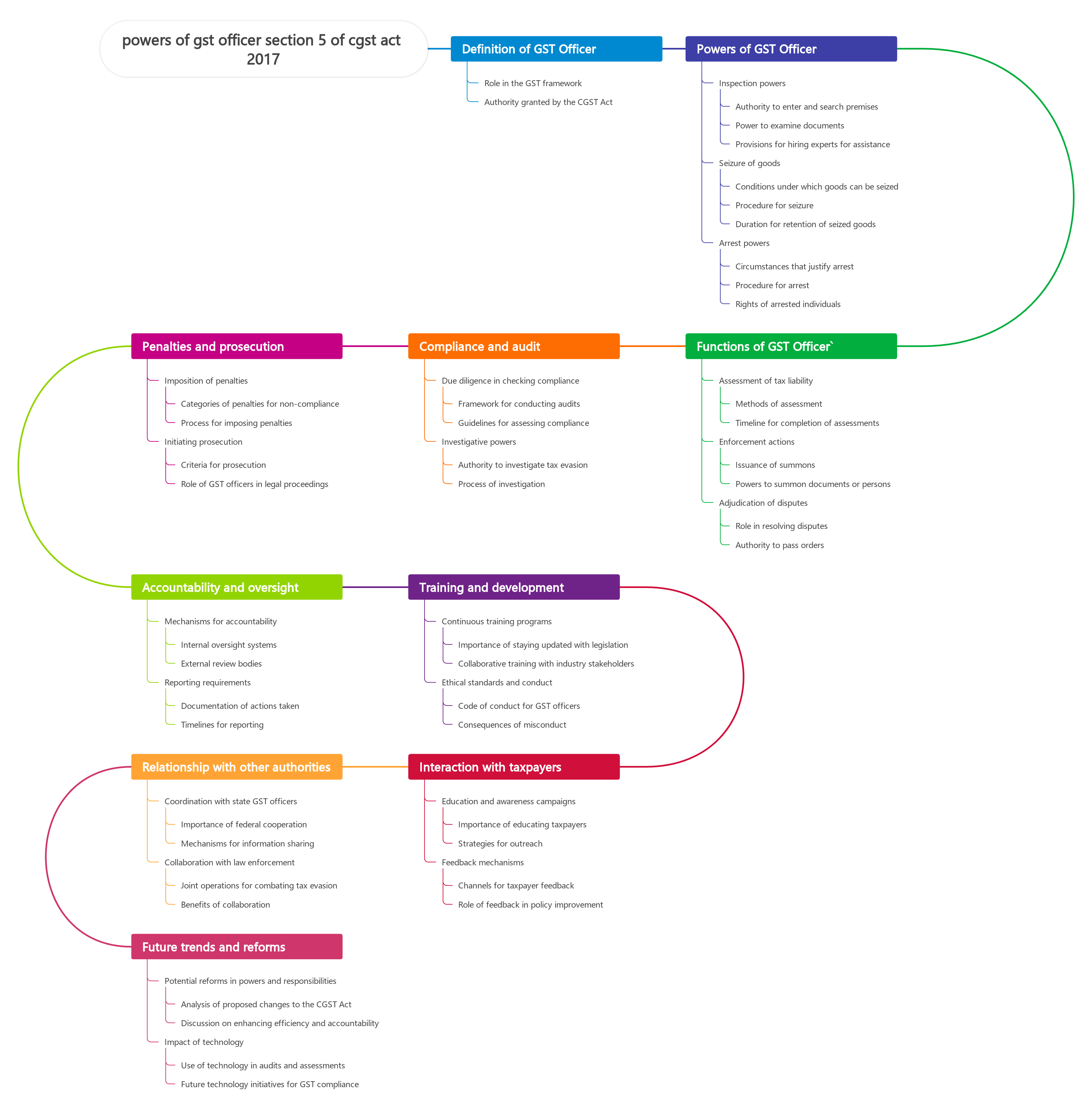

The Goods and Services Tax (GST) regime, a cornerstone of India's tax reform, relies on a robust framework of compliance and enforcement administered by a hierarchy of designated officers. The effective functioning of this self-assessment-based system hinges on these officers' ability to verify taxpayer declarations, investigate discrepancies, and enforce the law where necessary. Businesses increasingly rely on GST return filing and compliance management solutions to maintain filing accuracy, reduce reporting mismatches, and minimise the likelihood of scrutiny or enforcement proceedings. Understanding the scope, extent, and limitations of GST officers’ powers is essential for both taxpayers and compliance professionals. This balance is critical for protecting government revenue against evasion while simultaneously ensuring that taxpayers are treated fairly and are not subjected to arbitrary or excessive actions. This article provides a detailed analysis of the powers vested in GST officers under the Central Goods and Services Tax (CGST) Act, 2017, examining their authority across the full administrative continuum from initial assessment to final recovery.

2.0 The Legal Foundation of Authority

The powers exercised by GST officers are not arbitrary but are derived from a clear statutory framework established within the CGST and Integrated Goods and Services Tax (IGST) Acts. This legal scaffolding defines not only the extent of their authority but also the procedural safeguards and jurisdictional boundaries within which they must operate. This section deconstructs the legal basis of their authority, covering their appointment, the principle of delegated powers, and the crucial jurisdictional rules that govern their actions, preventing administrative overreach and ensuring procedural consistency. A clear understanding of this foundation is essential before examining the specific powers they wield.

2.1 Appointment and Classes of Officers

Under Sections 3 and 4 of the CGST Act, 2017, the Government is empowered to appoint various classes of officers for the administration of the Act. These officers form the administrative backbone of the GST system, with a clear hierarchy of authority. The classes of officers include:

-

Principal Chief Commissioner of Central Tax / Principal Director General of Central Tax

-

Chief Commissioner of Central Tax / Director General of Central Tax

-

Principal Commissioner of Central Tax / Principal Additional Director General of Central Tax

-

Commissioner of Central Tax / Additional Director General of Central Tax

-

Additional Commissioner of Central Tax / Additional Director of Central Tax

-

Joint Commissioner of Central Tax / Joint Director of Central Tax

-

Deputy Commissioner of Central Tax / Deputy Director of Central Tax

-

Assistant Commissioner of Central Tax / Assistant Director of Central Tax

-

Any other class of officers as the Government may deem fit

2.2 General Powers and Delegation

Section 5 of the CGST Act establishes the principles of authority and delegation among officers. It specifies that a central tax officer may exercise the powers conferred on any subordinate officer. Furthermore, the Commissioner has the authority to delegate their powers to any subordinate officer, subject to any conditions or limitations they may specify.

However, a critical word of caution is necessary. The general rule that a superior officer is empowered to exercise the authority of a subordinate does not hold good in all instances. The specific notification granting a particular power must be carefully examined to determine whether the power is conferred on an officer of a certain rank or on officers below a specific rank. This distinction is a frequent subject of litigation, as challenges to the jurisdiction of the notice-issuing officer are a primary ground for contesting proceedings ab initio.

2.3 Jurisdictional Framework and Cross-Empowerment

As a cornerstone of cooperative federalism within the GST structure, Section 6 of the CGST Act provides for the cross-empowerment of State GST officers. This provision, explicitly designed to prevent inter-agency friction and taxpayer harassment, authorises officers appointed under the State GST (SGST) or Union Territory GST (UTGST) Acts to be the 'proper officers' for the purposes of the CGST Act, subject to specified conditions.

A key provision that protects taxpayers from overlapping investigations is Section 6(2)(b), which states:

(b) where a proper officer under the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act has initiated any proceedings on a subject matter, no proceedings shall be initiated by the proper officer under this Act on the same subject matter.

This provision is of critical importance as it establishes a "first-in-time" rule. Once an authority, whether Central or State, has initiated proceedings on a specific issue, the other authority is barred from initiating proceedings on the same subject matter. This protects taxpayers from the burden of facing simultaneous actions from two different administrative bodies for the same tax-related issue. With the legal foundation of their authority established, we can now turn to the specific powers they wield in assessments and investigations.

3.0 Investigative and Assessment Powers

Beyond establishing the hierarchy and jurisdiction of officers, the GST framework equips them with a range of powers to verify taxpayer compliance and assess tax liability when necessary. These powers are essential tools for maintaining the integrity of the self-assessment regime, where the primary responsibility for calculating and paying tax lies with the taxpayer. The powers range from the routine scrutiny of returns to more intensive audits and, in cases of non-compliance, ex-parte assessments to protect government revenue. This section details these critical investigative and assessment functions.

3.1 Scrutiny of Returns (Section 61)

The scrutiny of returns is the first line of verification available to a proper officer. It is a non-coercive process aimed at ensuring the correctness of the information furnished by a registered person. The procedure is as follows:

-

The proper officer scrutinises the return and related particulars to verify their correctness.

-

If any discrepancies are noticed, the officer issues a notice in FORM GST ASMT-10, informing the registered person of the discrepancies and seeking an explanation, and failure to respond to GST notices in time may lead to further proceedings.

-

The taxpayer is required to provide an explanation within thirty days of the notice.

-

If the explanation is found to be acceptable, the officer informs the taxpayer, and the proceedings are concluded. If the explanation is not satisfactory, or if the taxpayer fails to take corrective measures after accepting the discrepancies, the proper officer may initiate further action, such as conducting an audit (Section 65), a special audit (Section 66), or determining tax liability under demand and recovery provisions (Sections 73 or 74 under GST).

3.2 Audit Powers (Sections 65 & 66)

When a more detailed examination of a taxpayer's records is required, GST officers can initiate an audit, so businesses should keep a GST audit checklist ready for proper documentation and compliance. The CGST Act provides for two distinct types of audits.

| Feature | Audit by Tax Authorities (Sec. 65) | Special Audit (Sec. 66) |

| Triggering Authority | The Commissioner or any authorised officer. | Any officer not below the rank of Assistant Commissioner. |

| Reason for Audit | General or specific order to conduct an audit of any registered person. | Opinion that the value has not been correctly declared or the credit availed is not within normal limits. |

| Conducted By | The authorized officer. | A nominated chartered accountant or cost accountant. |

| Time for Completion | Must be completed within 3 months from the date of commencement, extendable by the Commissioner for a further 6 months. | Must be conducted within 90 days, extendable by the Assistant Commissioner for a further 90 days. |

| Outcome | The proper officer informs the registered person of findings in FORM GST ADT-02 and may initiate action under Sec. 73 or 74 if tax is unpaid/short paid. | The findings are submitted in a report to the Assistant Commissioner, who then informs the registered person and may initiate action under Sec. 73 or 74. |

3.3 Assessment of Non-Compliant Taxpayers

The statutory architecture of GST grants officers specific assessment powers as a bulwark against non-compliance, enabling them to assess tax liability in situations where taxpayers fail to comply with statutory requirements.

-

Assessment of Non-Filers (Section 62): If a registered person fails to furnish a required return (under Section 39 or 45), even after receiving a notice, the proper officer has the power to assess the tax liability to the best of his judgment. The officer will take into account all relevant material available and issue an assessment order. However, if the registered person furnishes a valid return within 30 days of the service of this assessment order, the order is deemed to be withdrawn.

-

Assessment of Unregistered Persons (Section 63): When a person who is liable to be registered under the Act fails to obtain registration, a proper officer can proceed to assess their tax liability for the relevant tax periods to the best of their judgment. An opportunity of being heard must be given to the person before passing such an order. The assessment order must be issued within five years from the due date for furnishing the annual return for the financial year to which the unpaid tax relates. Non-compliance can also arise from issues related to GST registration requirements.

-

Summary Assessment (Section 64): This power is reserved for special cases to protect the interest of revenue. If a proper officer has evidence that a taxable person has incurred a liability to pay tax and believes that any delay in assessment may adversely affect revenue, they can, with the prior permission of the Additional Commissioner or Joint Commissioner, proceed to assess the tax liability on a summary basis, including cases involving the Reverse Charge Mechanism (RCM) that require careful compliance. This assessment order can be withdrawn if the taxable person files an application for withdrawal within thirty days or if the Additional/Joint Commissioner considers the order to be erroneous.

These assessment powers serve as a critical backstop to the self-assessment regime, enabling authorities to establish liability even in the face of non-cooperation and providing the legal foundation for the more coercive enforcement measures that follow.

4.0 Coercive and Enforcement Powers

When investigative measures like scrutiny and audit prove insufficient to ensure compliance, the GST law provides for more coercive actions. These powers represent the sharp end of tax administration, designed to uncover willful tax evasion, compel the production of evidence, and protect government revenue from imminent risk. This section details the formidable powers of inspection, search, seizure, summons, and arrest, which are vested in GST officers to enforce the provisions of the Act in cases of suspected fraud or significant non-compliance.

4.1 Power of Inspection, Search, and Seizure (Section 67)

The powers of inspection, search, and seizure are among the most potent tools available to GST officers, but their exercise is governed by strict conditions and procedures.

-

Authorisation: This power can only be authorised by a proper officer of the rank of Joint Commissioner or above. This senior-level authorisation acts as a crucial safeguard against misuse.

-

Pre-requisite: The authorising officer must have "reasons to believe" that the taxpayer is engaged in activities to evade tax. This includes suppression of transactions, suppression of stock, claiming excess Input Tax Credit (ITC), or contravening any other provisions of the Act.

-

Procedure: The authorization for inspection or search is issued in FORM GST INS-01.

-

Scope of Power: Once authorized, an officer can inspect any place of business, search premises for evidence, seize goods that are liable for confiscation, and seize any books, documents, or other relevant items that may be useful for proceedings under the Act.

4.2 Power to Inspect Goods in Movement (Section 68)

To prevent the clandestine movement of goods and evasion of tax, Section 68 empowers a proper officer to intercept any conveyance carrying goods. The officer can require the person in charge of the conveyance to produce prescribed documents, such as a tax invoice and a valid e-way bill, for verification. If the officer finds that the provisions of the Act have been contravened, they have the power to detain the goods and the conveyance.

For example, businesses operating through online marketplaces must ensure compliance with e-way bills on e-commerce requirements, as improper documentation is a common reason for detention during transit verification.

4.3 Power to Summon and Access Premises (Sections 70 & 71)

To aid in any inquiry, GST officers are granted powers to compel the production of evidence and access business premises.

-

Power to Summon (Sec. 70): A proper officer has the authority to summon any person whose attendance is considered necessary to give evidence or produce a document or any other thing in an inquiry. Significantly, any such inquiry conducted by the officer is deemed to be a "judicial proceeding," meaning that providing false information can attract legal consequences under the Indian Penal Code.

-

Access to Business Premises (Sec. 71): To facilitate verification of compliance, any officer under the CGST Act, when authorised by a proper officer of the rank of Joint Commissioner or above, is empowered to access any place of business of a registered person. This power allows the authorised officer to inspect books of account, documents, computers, computer programs, and other relevant items necessary to audit, scrutinise, or verify the taxpayer’s records.

4.4 The Power to Arrest (Section 69)

Representing the apex of coercive authority, the power of arrest under Section 69 is reserved for enumerated, egregious offences.

This power is vested in the Commissioner, who may authorise any officer of the central tax to arrest a person. The authorisation can only be given if the Commissioner has "reasons to believe" that the person has committed one of the specific, serious offences listed under Section 132 of the Act, such as supplying goods or services without an invoice to evade tax, issuing invoices without actual supply (fake invoicing), or wrongfully availing Input Tax Credit (ITC), which is a common trigger for investigations. As a critical procedural safeguard, any person arrested must be produced before a Magistrate within twenty-four hours. The inclusion of stringent 'reasons to believe' and post-arrest judicial review safeguards reflects the legislature's intent to reserve this draconian power for cases of significant, demonstrable fraud, balancing enforcement needs with individual liberties.

Once liability has been established, either through assessment or as a result of these enforcement actions, the framework shifts from investigation and coercion to the final, procedural phase of tax administration: the demand for and recovery of established dues.

5.0 Powers of Demand and Recovery

The determination of tax liability through assessment, audit, or investigation leads to the next logical phase in tax administration: the power to demand and recover unpaid government dues. The CGST Act provides a structured and time-bound mechanism for officers to raise formal demands for tax, interest, and penalties, most of which begin with a GST demand notice (DRC-01). Should a taxpayer fail to comply with these demands, the Act equips officers with various modes of recovery to protect the revenue's interests. This section explores these statutory mechanisms, from the initial determination of tax to the ultimate recovery of arrears.

5.1 Determination of Tax Liability (Sections 73 & 74)

The process for determining tax liability is bifurcated based on the taxpayer's intent. The Act makes a clear distinction between cases of genuine error or omission and cases involving fraud, willful misstatement, or suppression of facts.

| Aspect | Non-Fraud Cases (Sec. 73) | Fraud Cases (Sec. 74) |

| Basis for Demand | Tax not paid, short paid, erroneously refunded, or ITC wrongly availed for reasons other than fraud, willful misstatement, or suppression of facts. | Tax not paid, short paid, erroneously refunded, or ITC wrongly availed by reason of fraud, willful misstatement, or suppression of facts. |

| Time Limit for Order | Within three years from the due date for the annual return. | Within five years from the due date for the annual return. |

| Penalty | 10% of tax or Rs. 10,000, whichever is higher. No penalty if tax and interest are paid within 30 days of the show cause notice. | 100% of tax. Can be reduced to 15%, 25%, or 50% if paid at various stages before the order. |

5.2 Mechanisms for Recovery of Dues (Section 79)

If a taxpayer fails to pay any amount payable to the Government, the proper officer can initiate recovery proceedings under Section 79. The Act provides several modes of recovery, including:

-

Deduction from Government Dues: The officer can deduct the outstanding amount from any money that the government owes to the defaulting person.

-

Detention and Sale of Goods: The officer can detain and sell any goods belonging to the person that are under the control of the tax department.

-

Garnishee Proceedings: A notice in writing can be issued to a third party who owes money to the defaulter (such as a bank holding their funds or a debtor). This notice requires the third party to pay the amount directly to the Government instead of the defaulter.

-

Distraint of Property: The officer can distrain any movable or immovable property belonging to the person. If the dues are not paid within 30 days, the property can be sold to recover the amount.

5.3 Provisional Attachment to Protect Revenue (Section 83)

Section 83 grants a significant power to the Commissioner to protect revenue during the pendency of certain proceedings. If, during proceedings under Chapters related to Assessment (XII), Inspection, Search, and Seizure (XIV), or Demands and Recovery (XV), the Commissioner is of the opinion that it is necessary to protect the interest of government revenue, they can issue an order for the provisional attachment of any property belonging to the taxable person. This includes the attachment of bank accounts, which can effectively freeze the taxpayer's financial operations until the proceedings are concluded. This pre-emptive power, while crucial for protecting revenue against potential asset disposal by errant taxpayers, is among the most contentious, as it can severely disrupt the normal course of business before a final liability is even determined.

6.0 Conclusion: Balancing Authority with Accountability

The legal framework of the GST regime grants a wide and multi-faceted array of powers to its officers, ranging from routine scrutiny and audit to coercive actions such as inspection, search, seizure, and arrest. These powers are indispensable for administering the tax law, ensuring compliance, and safeguarding public revenue against evasion. However, this extensive authority is not without its checks and balances. The CGST Act embeds several statutory safeguards to ensure that these powers are exercised judiciously and fairly.

Key among these safeguards are the prerequisite for "reasons to believe" before initiating stringent actions like search or arrest, the jurisdictional limitations under Section 6 that prevent overlapping proceedings, and the adherence to principles of natural justice, such as providing an "opportunity of being heard" before an adverse order is passed. Furthermore, general disciplines related to the imposition of penalties, as outlined in Section 126, guide officers to act in a manner that is commensurate with the severity of the breach. The effective and equitable functioning of the GST regime ultimately depends on the judicious exercise of these powers, striking a crucial balance between the imperative to protect public revenue and the fundamental need to uphold the rights of the taxpayer.

Powers of GST officers under CGST Act | How to check din number in GST portal | GST suvidha kendra franchise provider companies list | How to check DIN number in GST portal

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified