Powers & Limitations of GST Officers under CGST Sections 5 & 6 (2025 Guide)

Introduction

The Goods and Services Tax (GST) regime in India, governed by the Central Goods and Services Tax Act, 2017 (CGST Act), provides a comprehensive framework for the administration and enforcement of GST laws. Sections 5 and 6 of the CGST Act outline the powers of GST officers, which are crucial for the effective implementation and enforcement of GST laws. This note provides a detailed analysis of these sections, highlighting the powers conferred upon GST officers and the cross-utilisation of powers between Central and State GST officers.

Applicable Sections and Rules

Section 5: Powers of Officers

-

Section 5(1): This subsection empowers an officer of central tax to exercise the powers and discharge the duties conferred or imposed on him under the CGST Act, subject to conditions and limitations imposed by the Board. This ensures that officers operate within a structured framework, maintaining checks and balances.

-

Section 5(2): It allows a senior officer to exercise the powers of a subordinate officer. This provision ensures flexibility and continuity in operations, allowing senior officers to step in when necessary.

-

Section 5(3): The Commissioner has the authority to delegate his powers to any subordinate officer, subject to specified conditions and limitations. This delegation is crucial for efficient administration, ensuring that responsibilities can be distributed effectively.

-

Section 5(4): This subsection explicitly states that an Appellate Authority cannot exercise the powers of any other officer of central tax, ensuring a clear separation of administrative and appellate functions.

Section 6: Cross-Utilisation of Powers

-

Section 6(1): Officers appointed under the State Goods and Services Tax Act (SGST) or the Union Territory Goods and Services Tax Act (UTGST) are authorised to act as proper officers for the purposes of the CGST Act. This cross-utilisation is subject to conditions specified by the Government, ensuring a unified approach to GST administration.

-

Section 6(2): It provides that if an officer issues an order under the CGST Act, they must also issue a corresponding order under the SGST/UTGST Act, and vice versa. This ensures consistency in orders and prevents duplication of proceedings.

Notifications, Circulars, Guidelines, Instructions

-

Circular No. 1/1/2017 and 223/17/2024: These circulars clarify the tasks to be performed by different levels of officers, ensuring clarity in the distribution of responsibilities.

-

Notification No. 09/2017-CT: Effective from 01.07.2017, this notification authorises officers under the SGST/UTGST Act to act as proper officers under the CGST Act, facilitating cross-functional operations.

Practical Implications

-

For Taxpayers: Understanding the powers of GST officers is crucial for compliance. Taxpayers must be aware of the authority of officers to conduct audits, inspections, and other enforcement actions.

-

For GST Officers: These sections provide a clear framework for the exercise of powers, ensuring that officers can perform their duties effectively while adhering to legal constraints.

Examples for Clarity

-

Example 1: A Superintendent of Central Tax can perform duties assigned to him under the CGST Act, such as conducting audits or inspections, within the limitations set by the Board.

-

Example 2: If a State GST officer issues an order under the SGST Act, they must also issue a corresponding order under the CGST Act, ensuring consistency in enforcement actions.

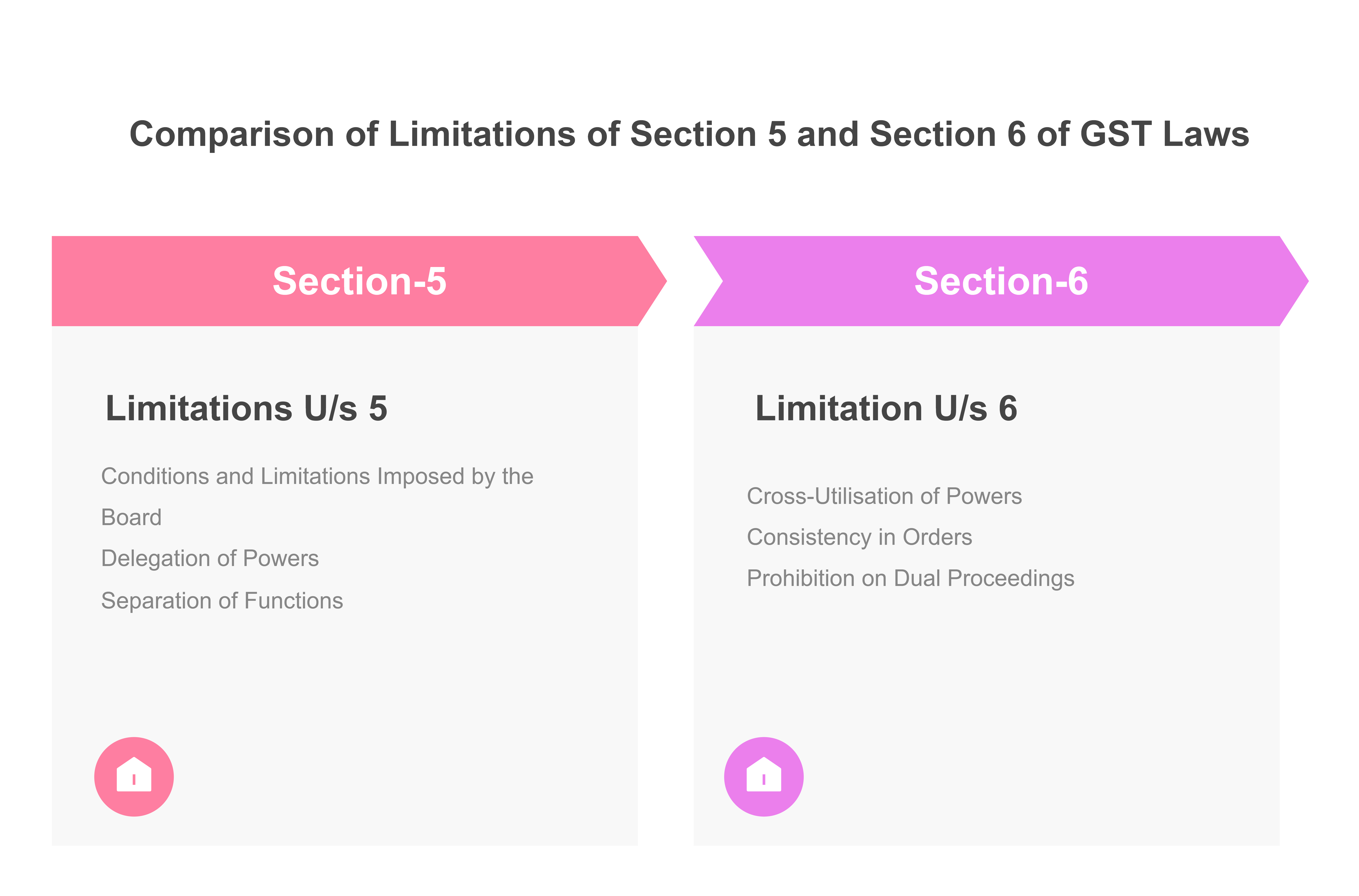

Limitations of Power Under Section 5

1. Conditions and Limitations Imposed by the Board

-

Section 5(1): The powers of GST officers are subject to conditions and limitations imposed by the Central Board of Indirect Taxes and Customs (CBIC). This ensures that officers operate within a structured framework, maintaining checks and balances.

2. Delegation of Powers

-

Section 5(3): The Commissioner can delegate his powers to subordinate officers, but this delegation is subject to specified conditions and limitations. This means that not all powers can be freely delegated, and the scope of delegation is controlled to prevent misuse.

3. Separation of Functions

-

Section 5(4): An Appellate Authority cannot exercise the powers of any other officer of central tax, ensuring a clear separation of administrative and appellate functions. This prevents any conflict of interest and ensures impartiality in decision-making.

Limitations of Power Under Section 6

1. Cross-Utilisation of Powers

-

Section 6(1): While officers appointed under the State Goods and Services Tax Act (SGST) or the Union Territory Goods and Services Tax Act (UTGST) are authorised to act as proper officers for the purposes of the CGST Act, this cross-utilisation is subject to conditions specified by the Government. This prevents conflicting views by tax authorities on the same issue and ensures a unified approach to GST administration.

2. Consistency in Orders

-

Section 6(2): If an officer issues an order under the CGST Act, they must also issue a corresponding order under the SGST/UTGST Act, and vice versa. This ensures consistency in orders and prevents duplication of proceedings. However, it also means that officers must be diligent in ensuring that orders are consistent across different jurisdictions.

3. Prohibition on Dual Proceedings

-

Section 6(3): If a proper officer under the CGST Act has initiated any proceedings on a subject matter, no proceedings shall be initiated by the proper officer under the SGST Act on the same subject matter, and vice versa. This prevents dual proceedings and ensures that taxpayers are not subjected to multiple assessments for the same issue.

Practical Implications

For Taxpayers

-

Awareness of Limitations: Taxpayers should be aware of the limitations on the powers of GST officers to ensure that they are not subjected to overreach or misuse of authority.

-

Compliance: Understanding these limitations can help taxpayers ensure compliance and protect their rights during audits and inspections.

For GST Officers

-

Adherence to Conditions: Officers must adhere to the conditions and limitations imposed by the Board to ensure fair and effective enforcement of GST laws.

-

Avoiding Overreach: Officers should exercise their powers judiciously and avoid overreach, which can lead to legal challenges and undermine the integrity of the GST system.

Recent Judicial Pronouncements:

-

Where two departmental proceedings overlap in assessing or recovering same tax liability/deficiency/obligation from a particular contravention, bar under Section 6(2)(b) applies, but where they relate to distinct infractions, it does not, even if liability or deficiency is similar; further, summons, search or seizure don’t qualify as "Initiation of proceedings" in s.6(2)(b) and it refers only to formal commencement of adjudicatory proceedings by way SCN. Supreme Court in Armour Security India Ltd. vs Commissioner, CGST, Delhi East Commissionerate (2025) 33 CENTAX 222

-

As State GST authorities had no jurisdiction to initiate parallel proceedings on same cause already taken up by Central GST, and their proceedings were subsequently closed, show cause notice issued by Central GST official was not barred. Chhattisgarh High Court in South Eastern Coalfields Ltd. vs Principal Commissioner, GST (2025) 33 CENTAX 150

-

Where the Central Tax authority had initiated proceedings prior in point of time, the State Tax authority could not proceed by carrying out a raid and sealing the premises of the assessee for the same cause; only the Central Tax authority had jurisdiction and authority to deal with the assessee. Himachal Pradesh High Court in Shivalik International vs Joint Commissioner of State Tax and Excise-cum-Proper Officer (2025) 31 CENTAX 374

Conclusion and Recommendations

-

Key Points:

-

Section 5 outlines the powers and duties of GST officers, allowing for delegation and flexibility in operations.

-

Section 6 facilitates cross-utilisation of powers between Central and State GST officers, promoting a unified approach to GST administration.

-

-

Recommendations:

-

Taxpayers should ensure compliance with GST laws and cooperate with GST officers during audits and inspections.

-

GST officers should adhere to the conditions and limitations imposed by the Board to ensure fair and effective enforcement of GST laws.

-

In summary, Sections 5 and 6 of the CGST Act provide a robust framework for the administration and enforcement of GST laws, ensuring that officers have the necessary powers to perform their duties while maintaining checks and balances. The limitations on the powers of GST officers under Sections 5 and 6 of the CGST Act are designed to ensure a balanced approach to GST administration. By adhering to these limitations, GST officers can perform their duties effectively while maintaining the trust and confidence of taxpayers. Taxpayers, on the other hand, can ensure compliance and protect their rights by understanding these limitations and cooperating with GST officers during audits and inspections.

Power of GST Officer | GST Inspector Power | How to do GST Audit | GST Audit Procedure | DRC 01A

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified