The Notice Pay Recovery Conundrum: Demystifying the GST Trap on Corporate Exits

For years, corporate India has grappled with a persistent thorn in its administrative side: the taxability of notice pay recovery. Picture this: an employee resigns abruptly, failing to serve their contractually mandated notice period. To mitigate administrative gaps and operational disruptions, the finance team recovers an amount equivalent to the unserved period from the employee's final settlement.

Suddenly, a Show Cause Notice lands on the Chief Financial Officer's desk, with the Department demanding 18% Goods and Services Tax (GST) on this recovery, categorising it as a consideration for "tolerating an act" of premature termination.

This aggressive interpretation has created widespread operational friction, leaving CFOs, tax consultants, and corporate lawyers locked in endless, unnecessary litigation over what is fundamentally an employment safeguard rather than a commercial service, often leading to GST demand notices and adjudication proceedings.

1. The Statutory Framework: Employment Contracts vs. Taxable Supply

To dismantle the Department’s case, one must look directly at the statutory definitions governing transactions under the Central Goods and Services Tax (GST) Act, 2017.

Exclusion Under Schedule III

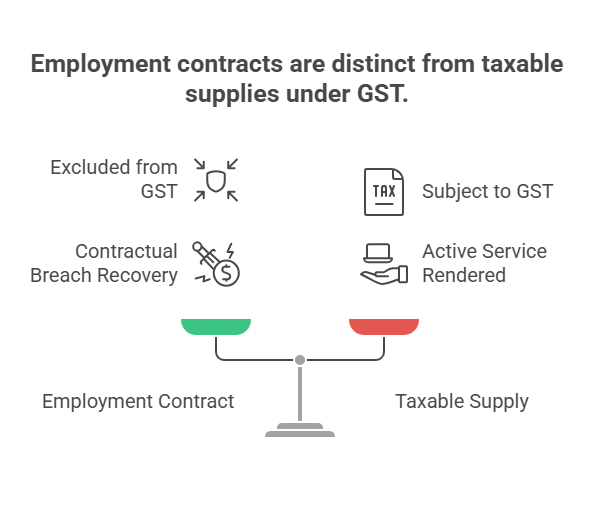

Employment in India is strictly governed by the terms and conditions stipulated in the employment agreement executed between the employer and the employee. Under Schedule III of the CGST Act, "services by an employee to the employer in the course of or in relation to his employment" are explicitly treated as neither a supply of goods nor a supply of services.

Contractual Flow, Not Independent Supply

The relationship between an employer and an employee—including conditions related to joining, working, and the cessation of employment—is entirely bound by the contract of employment. The recovery of notice pay is an incidental, protective condition built into this continuous relationship.

-

It cannot be isolated or treated as a taxable commercial transaction independent of employment.

-

The recovery does not constitute a "supply of goods" or a "supply of services" under Section 7 of the CGST Act.

-

The money changes hands because of a contractual breach, rather than any active service rendered by the employer to the employee.

2. The Legal Character: Compensation vs. Consideration

A fundamental error made by adjudicating authorities is confusing a contractual "penalty" or "compensation" with a "consideration" for a service.

Absence of Consideration Under Section 2(31)

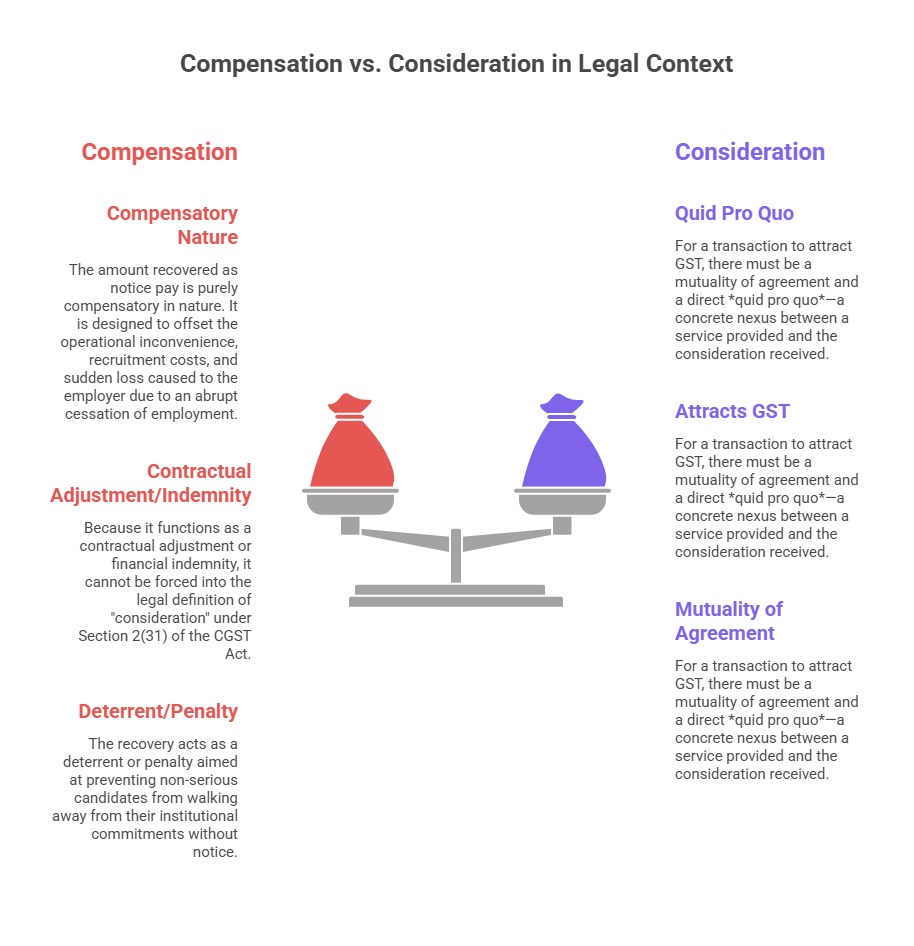

The amount recovered as notice pay is purely compensatory in nature. It is designed to offset the operational inconvenience, recruitment costs, and sudden loss caused to the employer due to an abrupt cessation of employment.

-

Deterrent Intent: The recovery acts as a deterrent or penalty aimed at preventing non-serious candidates from walking away from their institutional commitments without notice.

-

No Quid Pro Quo: For a transaction to attract GST, there must be a mutuality of agreement and a direct quid pro quo—a concrete nexus between a service provided and the consideration received.

"The amount recovered by the employer does not constitute consideration for tolerating the act of early termination. Rather, it represents a form of penalty or deterrent aimed at preventing non-serious employees from undertaking employment obligations without due commitment."

Because it functions as a contractual adjustment or financial indemnity, it cannot be forced into the legal definition of "consideration" under Section 2(31) of the CGST Act.

3. Dissecting the "Tolerating an Act" Fallacy

Tax authorities frequently lean on Entry 5(e) of Schedule II of the CGST Act, which levies tax on the "agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act". This interpretation is legally flawed and completely unsustainable.

The Requirement of Prior Consent

To "agree to tolerate an act," there must be a prior mutual agreement where one party permits the other to commit a breach in exchange for money, consistent with the broader legislative intent behind taxing such transactions. In an employment setup, the employer never enters into an agreement to tolerate early quitting. On the contrary, the employer wants the employee to stay and fulfill their duties.

The imposition of a notice pay clause is an enforcement mechanism to discourage such conduct, meaning the essential ingredient of mutual consent for "toleration" is entirely absent.

Judicial Precedents Shifting the Balance

High Courts across the country have consistently corrected the Department's position on this point:

Case Citation

Key Judicial Pronouncement

Ge T & D India Limited v. Deputy Commissioner of C. Ex., Chennai [2020] 115 taxmann.com 213 (Mad.)

The Madras High Court ruled that notice pay in lieu of sudden termination does not give rise to the rendition of service by either the employer or the employee. Therefore, no taxable supply exists.

Manappuram Finance Ltd. v. Assistant Commissioner of Central Tax and Excise, Thrissur [2022] 145 taxmann.com 422 (Ker.)

The Kerala High Court held that notice pay recovered by an employer is a contractual penalty, not a consideration for tolerating the act of premature quitting. The employer is not liable to pay GST.

4. The CBIC Clarification and the Right to Refund

Recognizing the widespread litigation, the Central Board of Indirect Taxes and Customs (CBIC) stepped in to provide administrative clarity, which has now turned into a powerful weapon for corporate taxpayers.

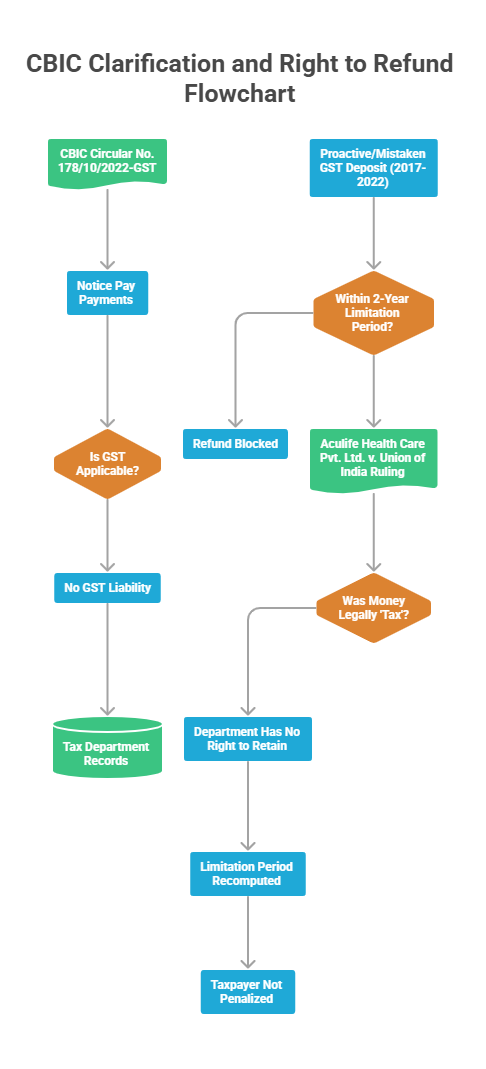

CBIC Circular No. 178/10/2022-GST

The Board explicitly clarified that an employee does not receive any corresponding benefit, quid pro quo, or service from the employer against notice pay payments. Consequently, the amount recovered does not qualify as consideration for any supply and is not liable to GST. These circulars are legally binding on the tax department under Section 168 of the CGST Act.

Extending the Limitation Period for Refunds: The Aculife Ruling

For businesses that proactively or mistakenly deposited GST on notice pay recoveries during the initial years of the GST regime (2017–2022), recovering those funds often hit a wall due to the two-year limitation period under Section 54, particularly where the tax was effectively paid under protest in GST.

However, the Hon'ble Gujarat High Court in Aculife Health Care Pvt. Ltd. v. Union of India [2025] 171 taxmann.com 272 (Guj.) delivered a landmark verdict on the principles of natural justice and procedural fairness.

-

The Ruling: The Court observed that because the money deposited by the assessee was never legally a "tax," the department had no right to retain it.

-

Limitation Shift: Crucially, the Court held that the two-year limitation period for claiming a refund must be computed from August 3, 2022 (the date of the clarifying CBIC Circular), rather than the original date of tax deposition.

This ensures that taxpayers are not penalized for the time it took the government to clarify its own ambiguous laws.

5. Arbitrary Levies: The Illegality of Interest and Penalty

In many ongoing disputes, adjudicating authorities blindly confirm the recovery of interest under Section 50 and penalties under Section 73(9) or Section 74 of the CGST Act. This practice is fundamentally opposed to established legal principles.

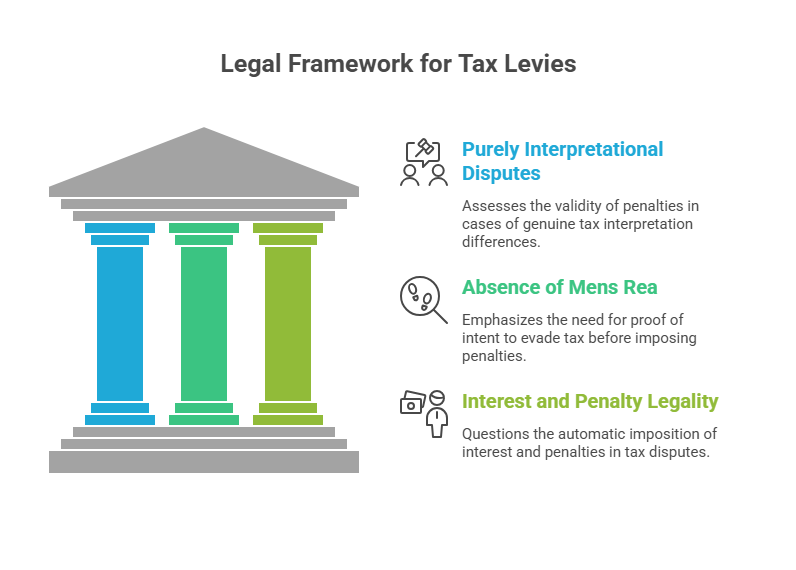

Purely Interpretational Disputes

A penalty cannot be imposed automatically. Notice pay recovery is a classic case of a bona fide interpretational dispute that has split judicial opinions historically. Where an assessee acts with complete transparency, disclosing all recoveries in its books of accounts, there is absolutely no evidence of fraud, willful misstatement, or intent to evade tax, a factor that also assumes importance during GST audits.

Absence of Mens Rea

To invoke harsher provisions like Section 74, the Department must conclusively establish mens rea (guilty mind) or deliberate concealment.

-

Because interest under Section 50 is compensatory and applies only when a legitimate tax remains unpaid, no interest can be levied when the underlying transaction itself falls outside the tax net.

-

Any order imposing penalties on such debatable issues, subsequent to a clarifying Board circular, is wholly arbitrary and liable to be set aside in entirety through the appellate remedies available under GST law.

Forward-Looking Summary

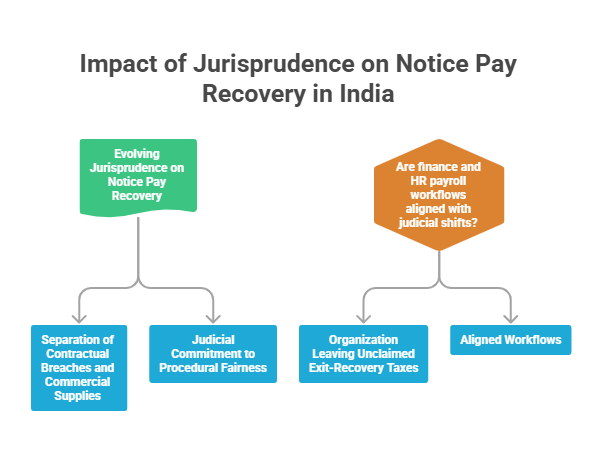

The evolving jurisprudence on notice pay recovery marks a significant victory for corporate governance and fair taxation in India. By firmly separating contractual breaches from commercial supplies, the judiciary and the CBIC have protected the sanctity of employment contracts from aggressive tax assessments. Furthermore, rulings like Aculife Health Care show a refreshing judicial commitment to procedural fairness, ensuring that internal administrative delays within the tax department do not strip corporate citizens of their right to a refund.

As we move toward an increasingly mature and automated tax ecosystem, corporate leadership must ask themselves: Are your finance and HR payroll workflows fully aligned with these judicial shifts, or is your organization leaving unclaimed, mistakenly paid exit-recovery taxes on the table?

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified