Tax Paid Under Protest in GST

Tax Paid Under Protest in GST

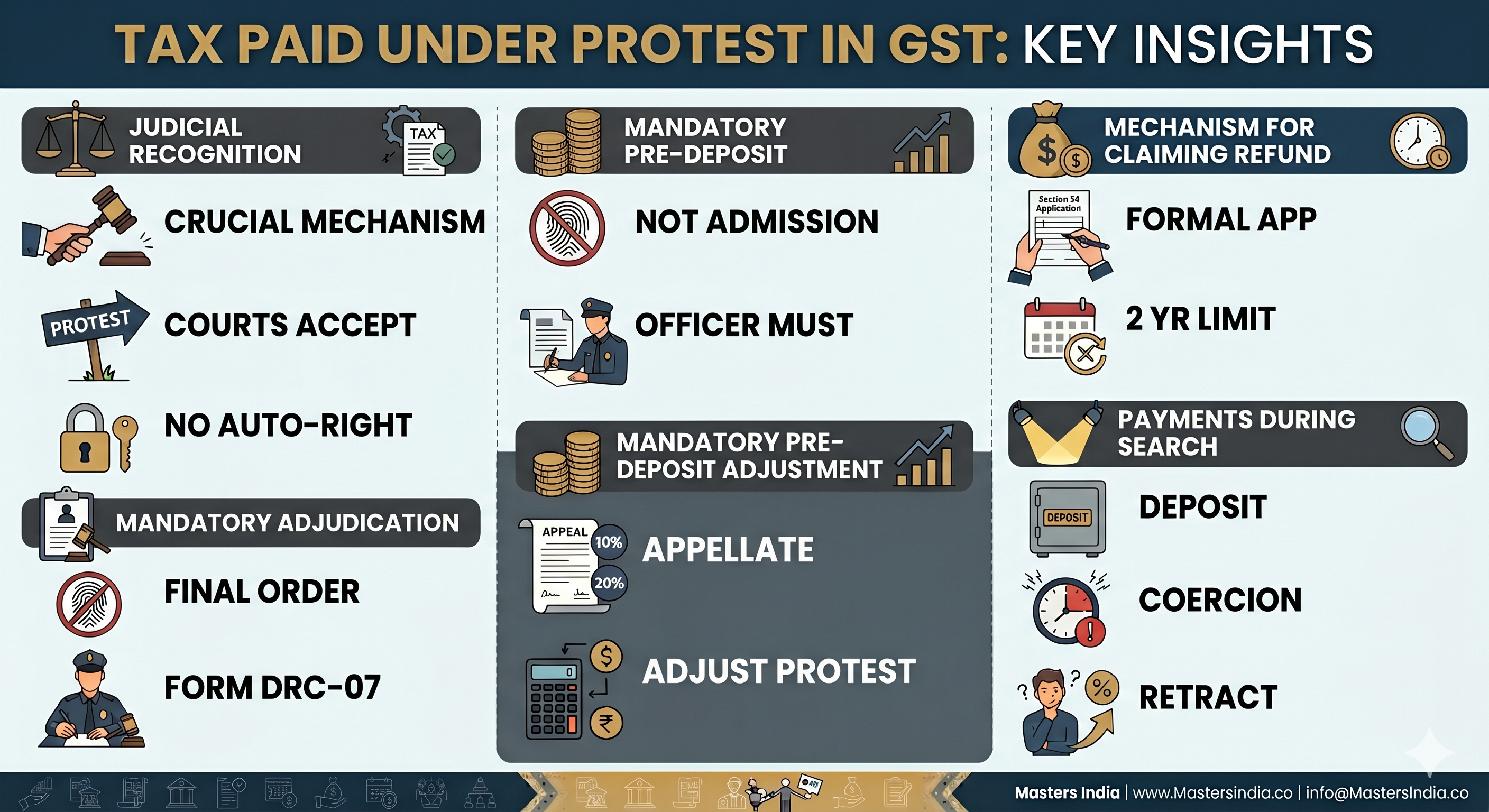

While the Goods and Services Tax (GST) law does not contain an explicit statutory provision that permits a "deposit under protest", it remains a crucial practical and legal mechanism for taxpayers. Taxpayers typically pay tax under protest to halt the "ticking clock" of interest on disputed demands, to avoid coercive recovery actions during investigations, including situations involving GST payments made during departmental investigations, or to secure the immediate release of detained goods.

Here is a detailed note on the treatment, implications, and judicial views regarding tax paid under protest in GST:

1. Judicial Recognition of "Under Protest" Payments

Courts have taken explicit judicial notice of payments made under protest. In the case of Team HR Services Pvt Ltd, the Delhi High Court observed that deposits made under protest to ease the rigours that tax authorities are otherwise entitled to impose are not unknown. The Court, citing the landmark Mafatlal Industries Ltd. case, noted that when an amount is deposited under protest, the taxpayer need not state the specific grounds of protest at that time. However, no automatic right to the funds accrues to the depositee until they are legally held to be entitled to it by a competent authority.

2. Mandatory Adjudication Despite Payment

Authorities cannot treat an "under protest" payment as an admission of guilt or a voluntary conclusion of proceedings. In ASP Traders vs. State of Uttar Pradesh, the Supreme Court ruled that even if a taxpayer makes a payment (voluntarily or under protest due to business exigencies) to obtain the release of detained goods, the proper officer is not absolved of their statutory obligation to pass a reasoned final order. The officer must issue the order (in Form GST MOV-09) and upload the summary (in Form GST DRC-07) to safeguard the taxpayer's constitutional and appellate rights to challenge the levy.

3. Adjustment Towards Mandatory Pre-Deposit for Appeals

Under GST, filing an appeal before the Appellate Authority or Tribunal under the framework governing GST appeals and revisions under Sections 107–121 requires a mandatory pre-deposit (typically 10% or 20% of the disputed tax). In VVF (India) Ltd., the Supreme Court held that there is no reason why an amount previously paid by the taxpayer "under protest" should not be taken into consideration and adjusted towards this mandatory pre-deposit requirement.

4. Mechanism for Claiming Refund

To recover taxes paid under protest, the taxpayer must strictly follow the statutory GST refund procedures prescribed under the law:

-

Filing an Application is Mandatory: A taxpayer cannot automatically reclaim the protested amount; they must file a formal refund application under Section 54 of the CGST Act.

-

Limitation Period: In the pre-GST era (Central Excise/Service Tax), payments made under protest were often exempt from the standard limitation period for claiming refunds. However, under the GST regime, Section 54(1) provides a strict two-year limitation period from the "relevant date". Since GST law does not explicitly carve out an exception for "under protest" payments, the two-year limitation generally applies to these refunds as well.

-

Unjust Enrichment: Even if a tax was paid under protest or was an illegal levy, the refund is subject to the doctrine of unjust enrichment, meaning the taxpayer must prove that the incidence of the tax was not passed on to their customers.

5. Payments Made During Search and Investigation

During search and seizure operations, taxpayers are often pressured to deposit amounts via Form GST DRC-03.

-

Courts have held that amounts deposited during an investigation should be treated as a "deposit" rather than a payment of "duty" or "tax".

-

If an amount is paid during a search under coercion (e.g., at odd hours or without actual self-ascertainment of liability), it cannot be termed "voluntary" and is essentially a deposit under protest, a distinction that becomes particularly important in proceedings involving Section 73 and Section 74 of GST. In cases where the payment is involuntary, the taxpayer is entitled to retract their statement and seek a refund of the deposited amount along with interest, though the department retains the right to issue a proper Show Cause Notice under Section 73 or 74.

6. Shyama Power India Ltd. vs State of Himachal Pradesh – Himachal Pradesh High Court

CWP No. 6990 of 2025 | 19-Jun-2025 | (2025) 32 CENTAX 101 (H.P.)

Amount deposited 'under protest' could not be treated as an admission of liability, enabling the department to impose interest and penalty.

Demand – Tax or Input Tax Credit (ITC) involving allegations of fraud – Determination of tax, interest, and penalty – Deposit made 'under protest' versus admission of liability - Tax period 2017-18 – A certain portion of input tax credit was purportedly wrongly availed. Due to persistent pressure from the department, the allegedly incorrect ITC was reversed 'under protest.' An order was issued under Section 74 of the Himachal Pradesh Goods and Services Tax (HPGST) Act, 2017, imposing interest and penalty. HELD: The amount deposited 'under protest' could not be regarded as an acknowledgement of liability. ITC should not have been reversed solely based on suspicion without conducting an independent investigation. Payment made 'under protest' cannot be considered a voluntary payment; thus, it does not authorise the department to treat it as an admission of liability and subsequently impose penalties and interest. The order imposing interest and penalties is to be annulled, in accordance with Section 74 of the Central Goods and Services Tax Act, 2017, and the Himachal Pradesh Goods and Services Tax Act, 2017.

7. Conclusion

Tax paid under protest in the GST framework serves as a critical legal and practical tool for taxpayers to manage disputes without conceding liability. Judicial precedent affirms that such payments do not constitute an admission of guilt and must be treated as deposits pending proper adjudication, reinforcing the importance of a sound GST litigation, audit, and appeal strategy in disputed tax matters. Authorities remain obligated to issue reasoned orders despite protest payments, ensuring taxpayers’ rights to appeal and challenge various GST notices and departmental actions remain intact. The GST law accommodates adjustment of protest payments against mandatory pre-deposits for appeals, while refund claims must strictly follow statutory procedures within prescribed limitation periods and are subject to the doctrine of unjust enrichment. Payments made under coercion during investigations are recognised as deposits under protest, allowing taxpayers to seek refunds with interest. Overall, the mechanism balances the enforcement powers of tax authorities with safeguards protecting taxpayers from premature or forced acceptance of disputed tax liabilities.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified