The Shield and the Sword: 5 Surprising Legal Protections Every Taxpayer Should Know

The Shield and the Sword: 5 Surprising Legal Protections Every Taxpayer Should Know

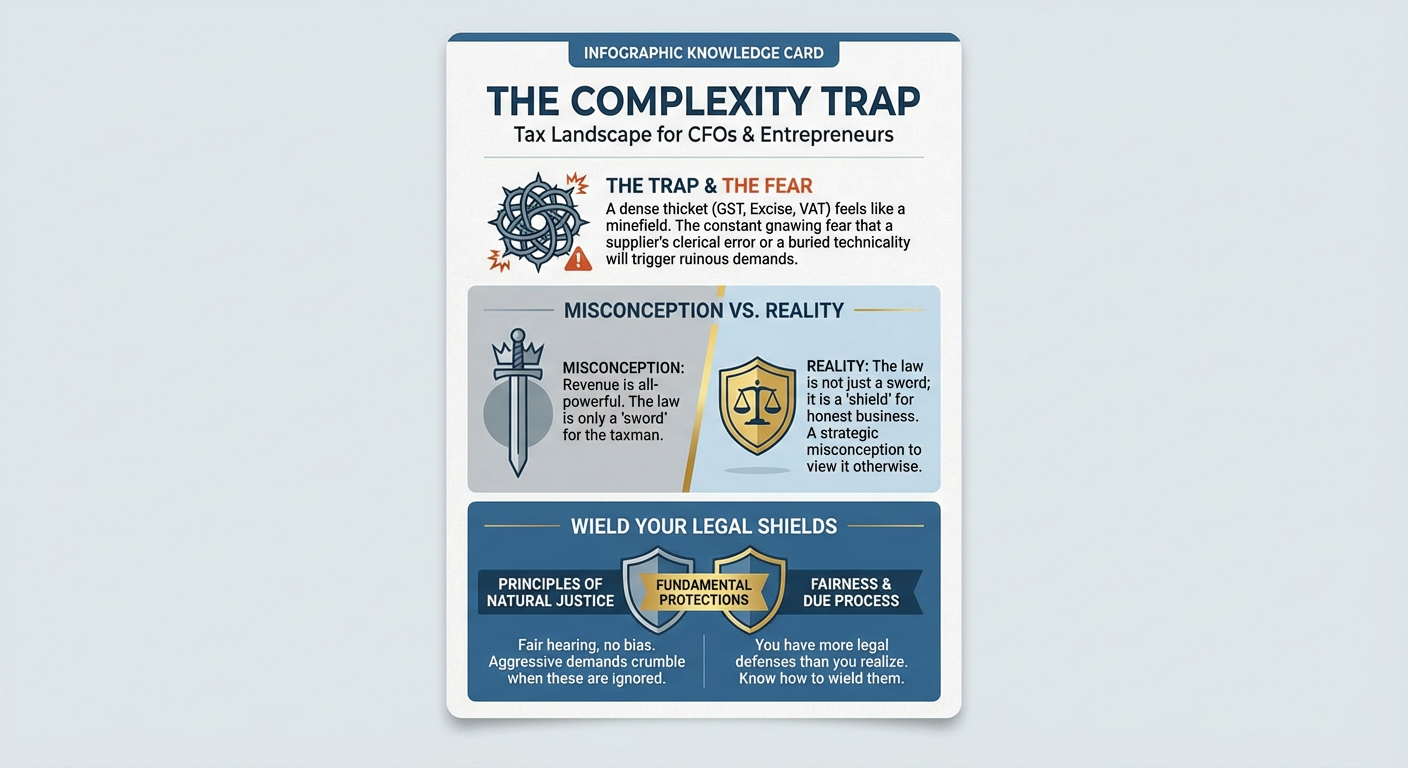

For the modern CFO or entrepreneur, the tax landscape—a dense thicket of GST, excise, and VAT—often feels less like a regulatory framework and more like a minefield. The "complexity trap" is real: the constant, gnawing fear that a supplier’s clerical error or a technicality buried in a three-year-old return will trigger a ruinous demand. Most taxpayers view the revenue as an all-powerful force, but this is a strategic misconception. The law is not just a sword for the taxman; it is a shield for honest business. As a litigator, I have seen the most aggressive demands crumble because the revenue ignored the fundamental principles of natural justice and fairness. You have more legal "shields" than you realise, provided you know how to wield them.

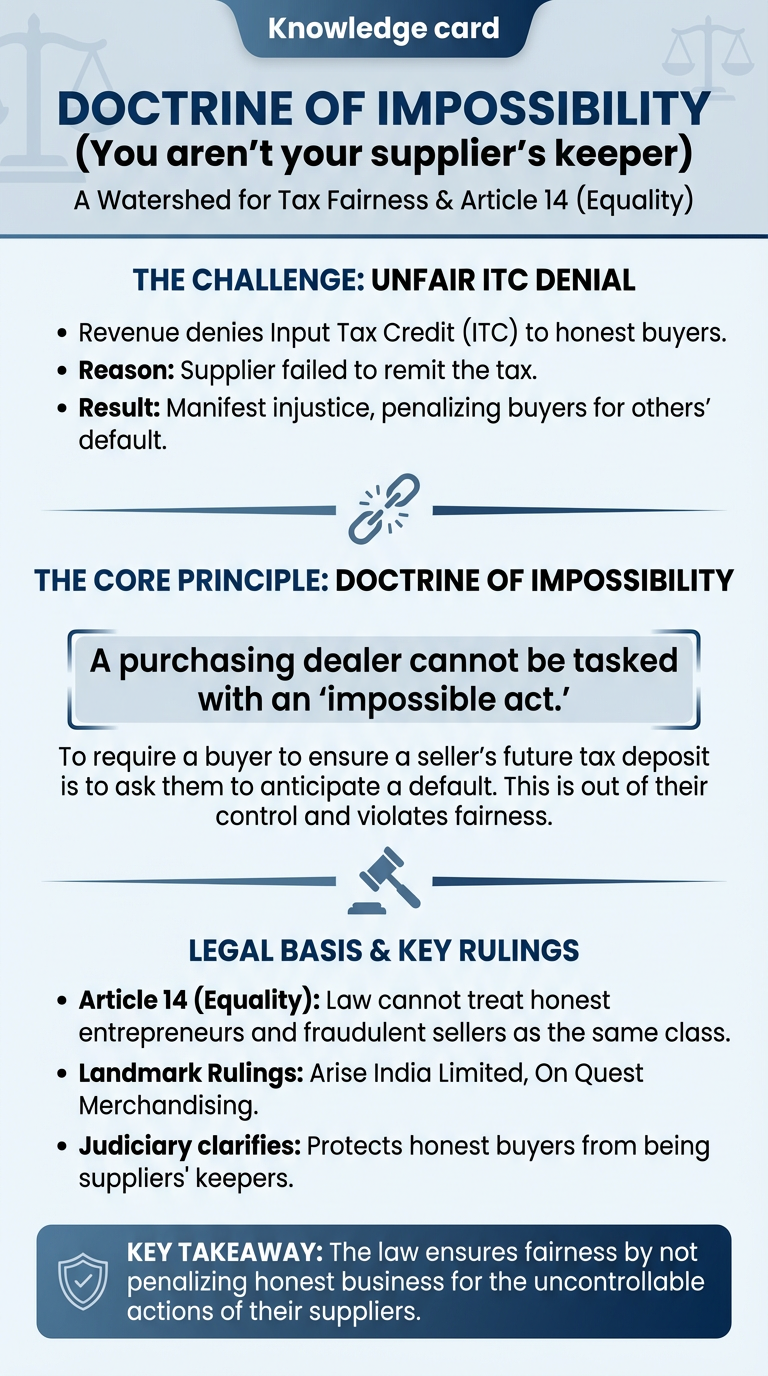

Takeaway 1: The "Doctrine of Impossibility" (you aren't your supplier’s keeper)

In the world of tax litigation, the rulings in Arise India Limited and On Quest Merchandising represent a watershed moment for Article 14 (Equality). The revenue often tries to penalise honest buyers by denying Input Tax Credit (ITC) under GST simply because their supplier failed to remit the tax. This is a manifest injustice.

The judiciary has stepped in to clarify that the law cannot treat an honest entrepreneur and a fraudulent seller as the same class. Under what we call the Doctrine of Impossibility, a purchasing dealer cannot be tasked with an "impossible act".

"To require a purchasing dealer to ensure that the selling dealer has deposited VAT with the government requires them to do the impossible act of anticipating a supplier's future default. This is out of the control of the purchasing dealer and violates the principles of fairness."

Strategic Analysis: You cannot be expected to audit your supplier’s bank account or predict their future non-compliance. Provided your transaction is bona fide (genuine), your right to credit is protected. Treating an innocent buyer as a guarantor for the state’s revenue collection is unconstitutional.

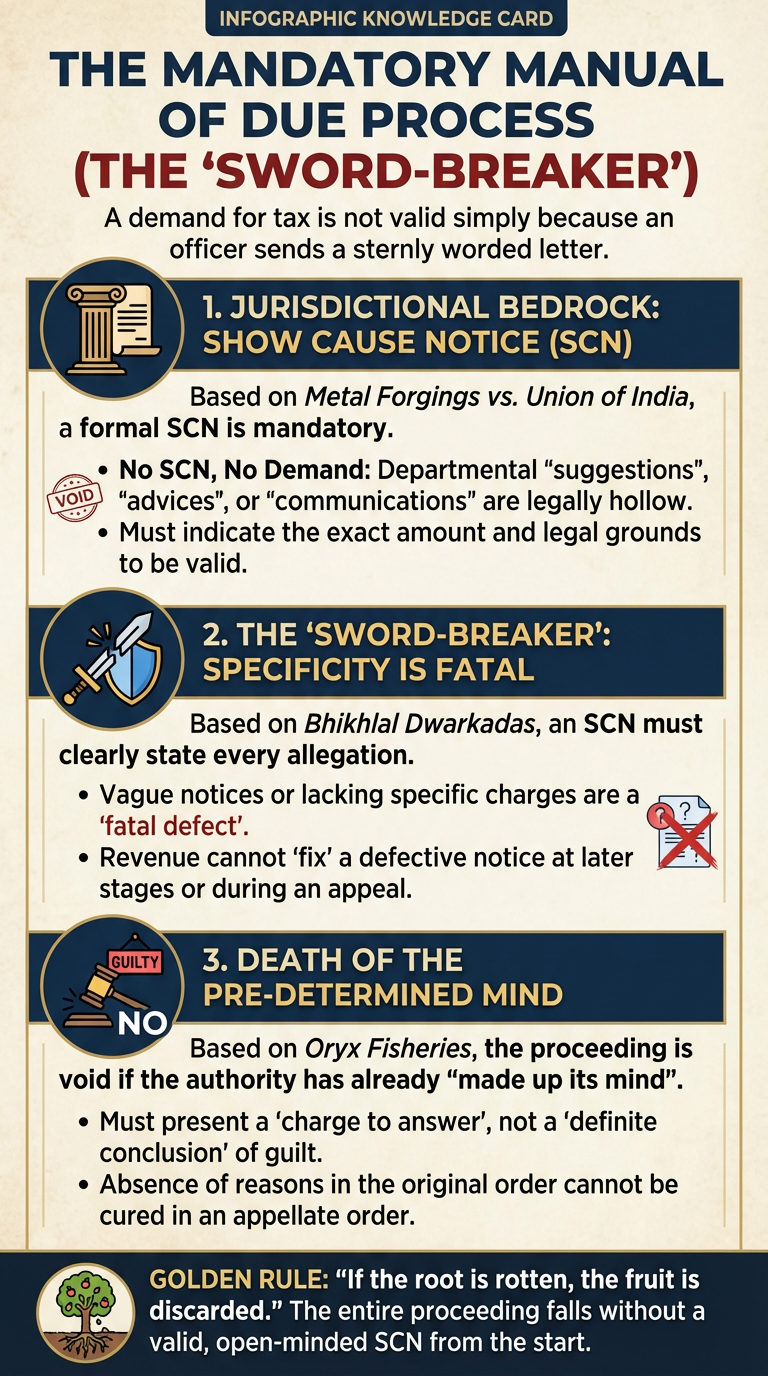

Takeaway 2: The mandatory manual of due process (The "Sword-Breaker")

A demand for tax is not valid simply because an officer sends a sternly worded letter. Based on Metal Forgings vs. Union of India, a formal GST show cause notice and departmental communication is the jurisdictional bedrock of any tax demand.

-

No SCN, No Demand: Departmental "suggestions", "advice", or "communications" are legally hollow. Unless the revenue issues a specific SCN indicating the exact amount and the legal grounds, similar to procedures followed for GST demand notices under Rule 142 (DRC-01), there is no valid demand.

-

The "Sword-Breaker" (Bhikhlal Dwarkadas): An SCN must clearly state every allegation. If the notice is vague or lacks specific charges, that defect is fatal. Crucially, the Revenue cannot "fix" a defective notice at later stages or during an appeal.

-

Death of the Pre-Determined Mind (Oryx Fisheries): If an SCN shows the authority has already "made up its mind"—confronting you with a "definite conclusion" of guilt rather than a charge to answer—the entire proceeding is void. Furthermore, the absence of reasons in the original order cannot be compensated for by disclosing reasons in an appellate order. If the root is rotten, the fruit is discarded.

Strategic Analysis: This protects you from administrative bullying. A notice that pre-judges your guilt is not a notice; it is a verdict in disguise, and the courts will quash it, which is why businesses increasingly focus on a structured GST litigation, audit, and appeal strategy.

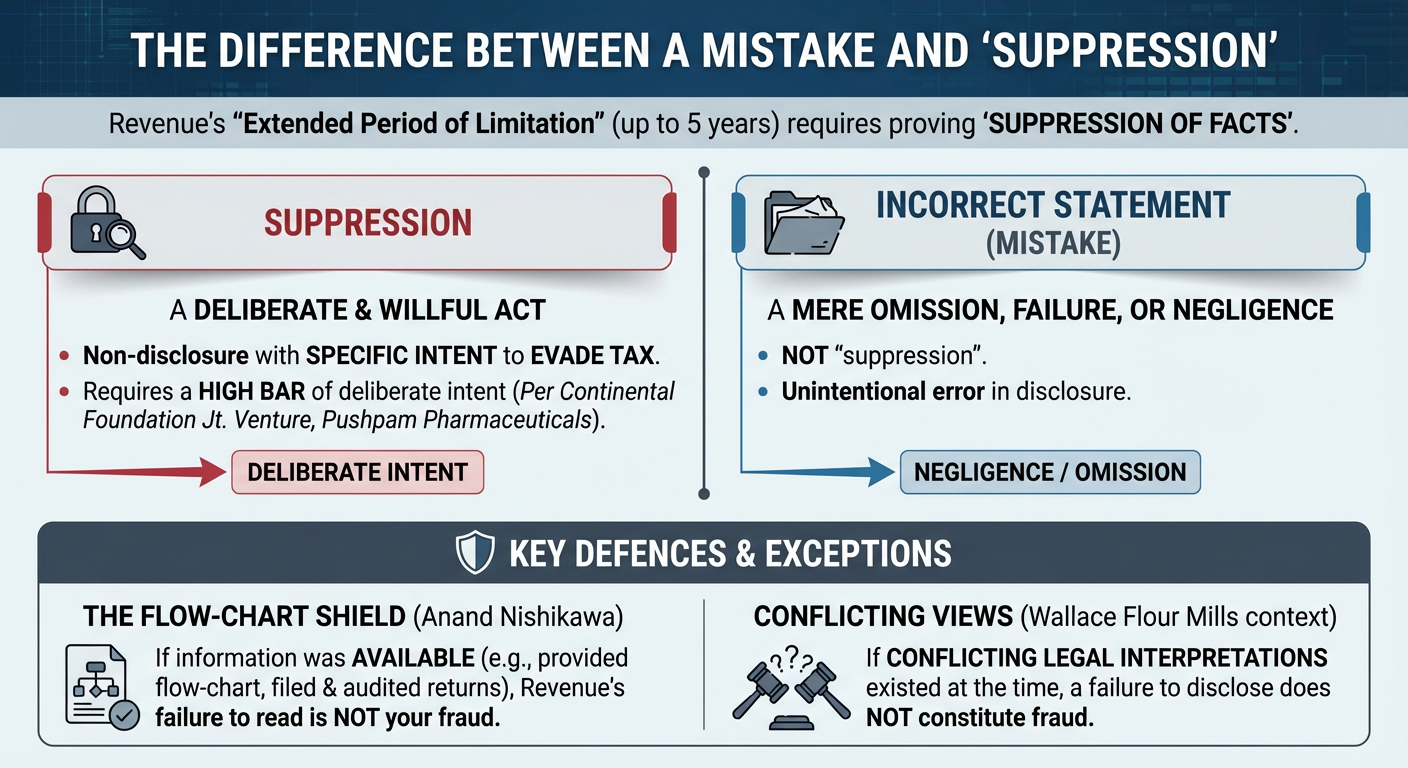

Takeaway 3: The difference between a mistake and "suppression"

The Revenue loves the "extended period of limitation" (up to five years), available under provisions like Section 73 vs Section 74 under GST, but they can only use it if they prove "suppression of facts". Per Continental Foundation Jt. Venture and Pushpam Pharmaceuticals, "suppression" requires a high bar of deliberate intent.

Defining the Divide:

-

Suppression: A deliberate and wilful act of non-disclosure with the specific intent to evade tax.

-

Incorrect Statement: A mere omission, failure, or negligence in disclosure is not "suppression".

-

The Flow-Chart Shield (Anand Nishikawa): If you provided the department with a flow chart of your manufacturing process, or if your returns were filed and audited, they cannot later claim you "suppressed" facts. If the information were available for them to see, their failure to read it would not be your fraud.

-

Conflicting Views: If there were conflicting legal interpretations at the time (e.g., the Wallace Flour Mills context), a failure to disclose does not constitute fraud.

Actionable Insight: For a CFO, transparency is a tactical defence. Documenting your disclosures (like flowcharts or detailed process notes) effectively "breaks" the revenue's ability to use the five-year extended limitation period.

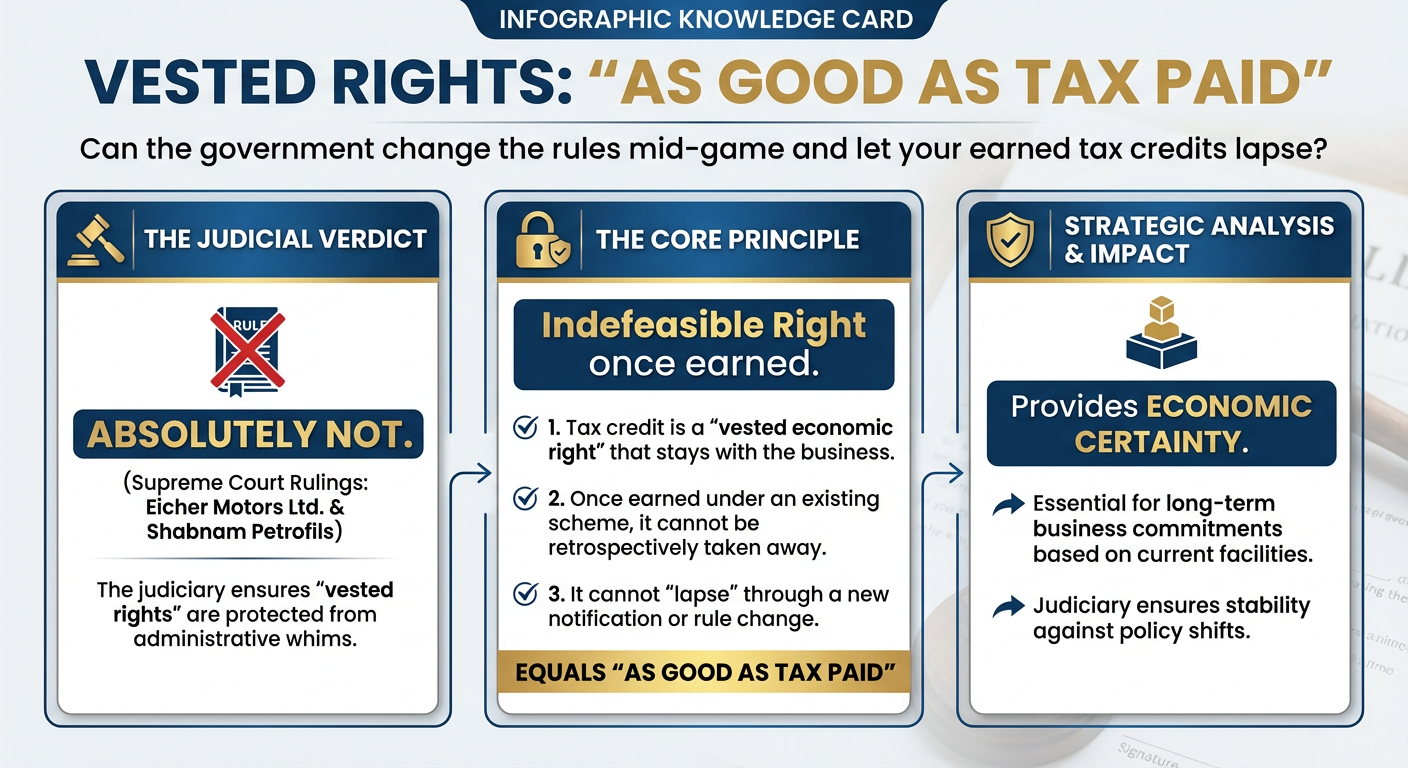

Takeaway 4: Vested rights are "As Good as Tax Paid"

Can the government change the rules mid-game and let your earned credits lapse? The Supreme Court in Eicher Motors Ltd and Shabnam Petrofils says absolutely not. Once a taxpayer earns a credit under an existing scheme, it becomes an indefeasible right.

The Principle: A tax credit is "as good as tax paid". It is a vested economic right that stays with the business. The government cannot retrospectively take it away or let it "lapse" through a new notification or rule change.

Strategic Analysis: This provides "economic certainty". If you made long-term business commitments based on current tax facilities, the judiciary ensures that those "vested rights" are protected from administrative whims.

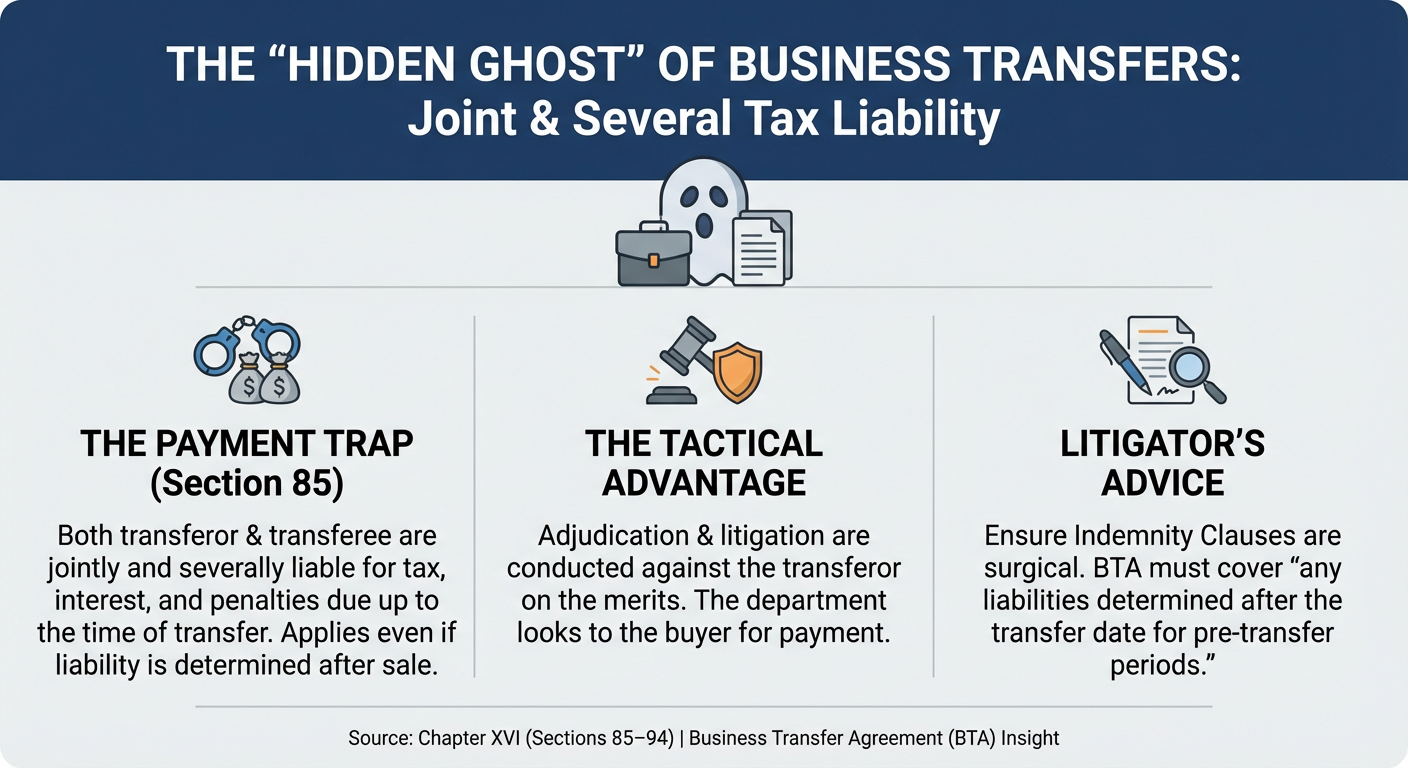

Takeaway 5: The "Hidden Ghost" of business transfers

Chapter XVI (Sections 85–94) contains a "joint and several" liability trap for anyone acquiring a business. If you buy, lease, or are gifted a business, you also acquire its tax history.

-

The Payment Trap: Under Section 85, both the transferor and transferee are jointly and severally liable for tax, interest, and GST penalties and liabilities due up to the time of transfer. This applies even if the liability is determined after the sale.

-

The Tactical Advantage: While the transferee is liable for the payment of the bill, the process of adjudication and litigation must still be conducted against the transferor. The department must fight the seller on the merits, even if they ultimately look to the buyer for the cheque.

-

Litigator’s Advice: Your indemnity clauses must be surgical. Ensure your Business Transfer Agreement (BTA) covers "any liabilities determined after the transfer date for pre-transfer periods".

Note on Scope: Beyond Section 85, Chapter XVI extends liability to agents, principals, and directors of private companies, making it essential to audit the "tax health" of any entity you engage with.

What these taxpayer protections mean for businesses today

Understanding taxpayer protections is no longer just a legal exercise. From ITC disputes and show cause notices to limitation periods, vested rights, and business transfer liabilities, the law provides several safeguards for honest taxpayers. The key is knowing when and how to use them.

Businesses that maintain proper documentation, follow due process, and stay informed about their legal rights are often in a much stronger position during audits, assessments, and litigation. In an increasingly complex tax environment, compliance alone is not enough. Awareness of your rights is equally important.

Need expert guidance on GST compliance, tax notices, audits, or litigation support? Connect with Masters India and book your free consultation with our experts today.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified