No GST on Salaries Paid to Foreign Nationals: Karnataka & Delhi High Court Clarify the Law (2024–2026)

Where a Genuine Employer-Employee Relationship Exists

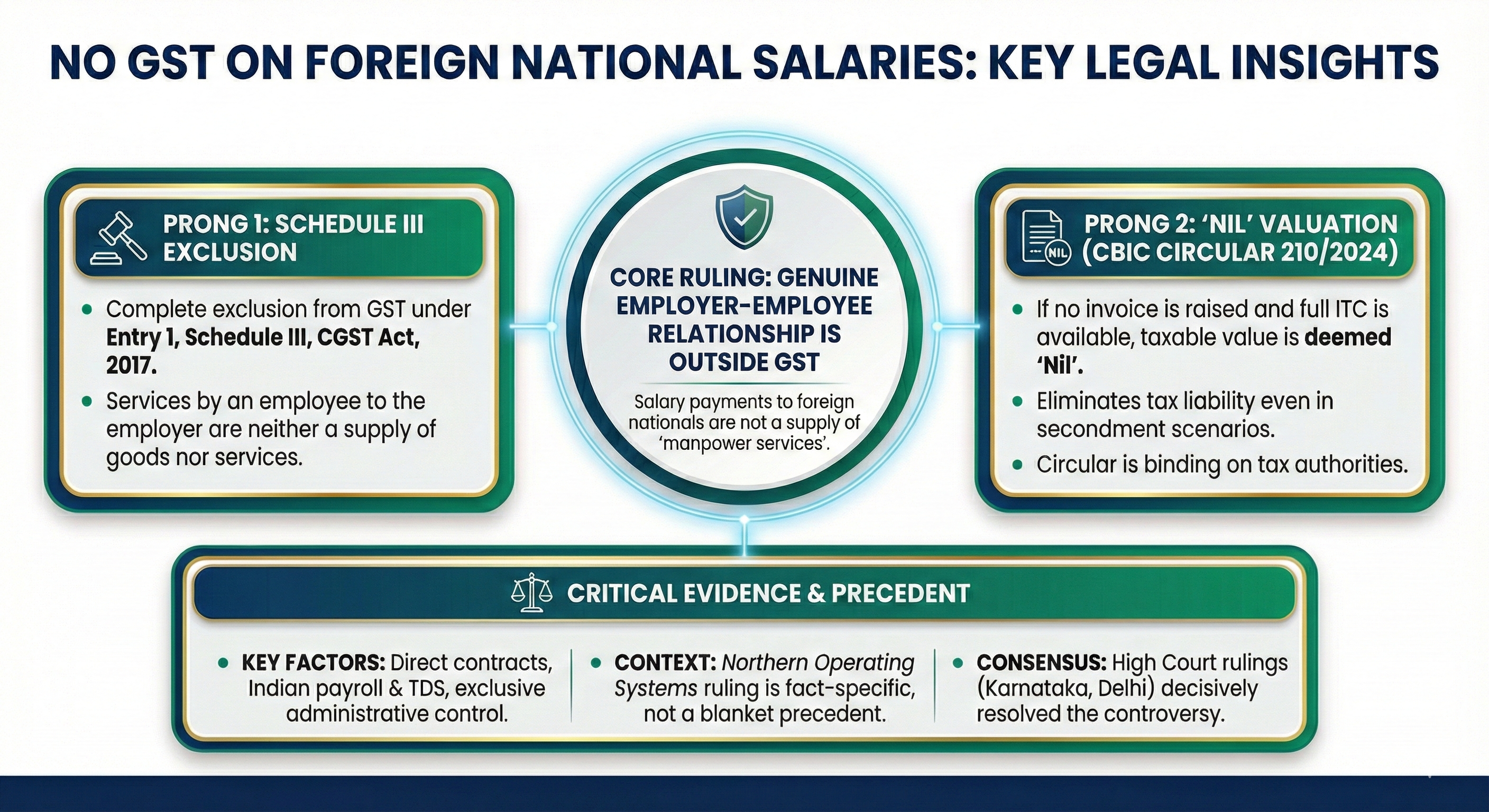

Executive Summary

The question of whether IGST is payable on salaries paid to foreign nationals or expatriate employees deputed to Indian entities has been a significant source of GST litigation across India. Tax authorities have been issuing show cause notices demanding Integrated Goods and Services Tax (IGST) under the Reverse Charge Mechanism (RCM), treating salary payments as consideration for the import of 'Manpower Recruitment and Supply Services' from non-resident taxable persons.

A series of landmark judgements by the Karnataka High Court and the Delhi High Court cumulatively covering the period 2017 to 2026 have decisively resolved this controversy. These decisions, underpinned by CBIC Circular No. 210/4/2024-GST dated 26 June 2024, have firmly established that where a genuine employer-employee relationship exists between the Indian entity and the foreign national, the entire transaction falls outside the ambit of GST by virtue of Entry 1 of Schedule III of the CGST Act, 2017. Even in secondment scenarios, in the absence of invoices, the taxable value is deemed 'Nil', extinguishing any tax liability.

Cases at a Glance

Huawei Technologies India Pvt. Ltd. v. State of Karnataka | (2026) 39 Centax 336 (Kar.) | WP No. 2848/2024 | Decided: 5 December 2025

Direct employer-employee relationship between the Indian company and foreign nationals takes the transaction outside GST entirely under Schedule III Entry 1. Foreign nationals residing and working in India are not 'non-resident taxable persons' under Section 2(77) of the CGST Act. IGST demand of ₹85,51,00,620 quashed.

Alstom Transport India Ltd. v. Commissioner of Commercial Taxes | (2025) 34 Centax 119 (Kar.) | WP No. 1779/2025 | Decided: 15 July 2025

Secondment of employees by a foreign parent company to its Indian subsidiary does not amount to a taxable supply of manpower services. In the absence of invoices raised by the Indian entity, the taxable value is deemed 'Nil' per CBIC Circular No. 210/4/2024-GST. IGST demand of ₹57,94,94,146 quashed.

Metal One Corporation India Pvt. Ltd. v. Union of India | (2024) 24 Centax 13 (Del.) | WP(C) 14945/2023 & connected | Decided: 22 October 2024

CBIC Circular No. 210/4/2024-GST is binding on the Department. Where no invoices are raised for seconded employees, the value of services is deemed 'Nil', resulting in zero tax liability. Multiple SCNs across pan-India entities quashed.

Background: The GST Controversy on Expatriate Salaries

The genesis of this controversy lies in the Supreme Court's ruling in CCE & ST v. Northern Operating Systems Pvt. Ltd. [2022 (61) GSTL 129 (SC)], wherein the Apex Court held that secondment of employees by a foreign entity to an Indian entity where the foreign entity retained economic control and levied a mark-up on salary reimbursements amounted to a taxable supply of manpower services. This judgment triggered a wave of GST investigations by the Directorate General of GST Intelligence (DGGI) and state tax authorities, resulting in show cause notices being issued to hundreds of Indian companies with expatriate workforces.

However, the Northern Operating Systems ruling was explicitly fact-specific. The Supreme Court cautioned that it should not be applied as a blanket precedent to all secondment arrangements. Despite this, tax authorities proceeded to issue notices in cases where the factual matrix was entirely different particularly where Indian entities had executed direct employment contracts, placed expatriates on their own payrolls, deducted TDS, and exercised full administrative control.

The Legal Framework: Entry 1 of Schedule III

What the Law Says

Entry 1 of Schedule III of the CGST Act, 2017 provides that:

Services by an employee to the employer in the course of or in relation to his employment shall be treated neither as a supply of goods nor a supply of services.

This provision, read with Section 7(2)(a) of the CGST Act, operates as a complete exclusion from the charging provisions of GST. The critical question in all three cases was whether the foreign national or expatriate was an employee of the Indian entity, or a service provider rendering manpower supply services through the foreign affiliate.

Non-Resident Taxable Person Section 2(77) CGST Act

The Department's case rested on characterising foreign nationals as 'Non-Resident Taxable Persons' (NRTPs) under Section 2(77) of the CGST Act, triggering import of service provisions under Section 2(11) of the IGST Act. The courts have unambiguously rejected this classification where:

-

The foreign national is not making 'occasional' supplies the hallmark of an NRTP. A full-time employee engaged under a contract of employment does not make 'occasional' supplies.

-

The foreign national has a fixed place of residence in India and is not a transient operator, a condition sine qua non for NRTP classification.

-

The foreign national's income is taxed under the Income Tax Act, 1961 as salary income, not as business income.

-

The location of the supplier (the employee) is in India negating the 'import of service' trigger under Section 2(11) of the IGST Act.

Detailed Analysis of the Cases

1. Huawei Technologies India Pvt. Ltd. v. State of Karnataka (2026)

Huawei's Indian subsidiary, part of the Huawei Group headquartered in China, employed foreign nationals directly under employment contracts for fixed periods to support its Software Development and ITES operations. The State of Karnataka issued an SCN demanding IGST of ₹85.51 crore (plus interest of ₹42.29 crore and penalty of ₹8.55 crore) for the period April 2018 to March 2023, alleging that Huawei India had imported 'Manpower Recruitment and Supply Services' from these foreign employees acting as non-resident taxable persons.

Justice S.R. Krishna Kumar meticulously examined the employment arrangements and identified the following features that conclusively established a direct employer-employee relationship:

-

Valid employment contracts stipulating fixed tenure, reporting authority, working hours, and cost-to-company.

-

Foreign nationals were on Huawei India's payroll; their salaries, annual performance bonuses, HRA, and provident fund contributions were paid directly into Indian bank accounts.

-

TDS was deducted by Huawei India under the Income Tax Act, 1961 and the foreign nationals filed Indian income tax returns as India-based employees.

-

Foreign nationals were treated at par with Indian employees in terms of salary and social security benefits there was no differential treatment.

The court further held that the foreign nationals, residing in India for the majority of the disputed period and provided furnished accommodation at the Huawei Campus, qualified as 'residents' for income tax purposes and did not satisfy the definitional requirements of NRTPs under Section 2(77) CGST Act. Since the location of the supplier was in India, the conditions under Section 2(11) of the IGST Act for an 'import of service' were simply not met.

As a further and independent ground, the court relied on CBIC Circular No. 210/4/2024-GST to hold that since no invoice was raised by Huawei India, the value of any putative supply was deemed 'Nil', and accordingly no tax was liable to be paid. The SCN was quashed in its entirety.

2. Alstom Transport India Ltd. v. Commissioner of Commercial Taxes (2025)

Alstom Transport India, engaged in designing and commissioning railway and metro infrastructure, had employees seconded from its overseas group companies for a fixed tenure during July 2017 to March 2023. The Indian company executed individual employment agreements with these expatriates, placed them on its payroll, paid their salaries directly after deducting TDS, and extended all statutory employment benefits under Indian labour laws. The Department demanded IGST of ₹59.57 crore under RCM for alleged import of manpower supply services.

This case is notable because it arose against the backdrop of Alstom having, out of abundant caution, already discharged IGST on a reverse charge basis on debit-note reimbursements from November 2020 onwards. Despite this, the authorities confirmed the demand for the full disputed period. Justice Sachin Shankar Magadum held that the secondees were under the exclusive administrative and functional control of Alstom India, were integrated into its organizational framework, and that the arrangement constituted a genuine employer-employee relationship excluded from GST under Schedule III.

Importantly, the court extensively analysed the evolution of law from the Service Tax era through the GST regime, traced the impact of the Northern Operating Systems ruling and its fact-specific nature, and concluded that the CBIC's 53rd GST Council-backed Circular of 26 June 2024 had effectively neutralised any residual tax liability by deeming the value 'Nil' in the absence of invoices. The impugned orders confirming the demand were quashed.

3. Metal One Corporation India Pvt. Ltd. v. Union of India (2024)

The Delhi High Court's decision in the Metal One batch of petitions was the first major High Court ruling to comprehensively apply the CBIC Circular No. 210/4/2024-GST to quash secondment-related SCNs. The petitioners including Metal One Corporation India (Delhi, Maharashtra, Tamil Nadu) and Sony India Private Limited were issued SCNs proposing IGST demands for the period July 2017 to March 2023, triggered by the placement of foreign expatriates from parent overseas companies.

The Division Bench of Justices Yashwant Varma and Ravinder Dudeja took a pragmatic approach. Rather than re-examining the employer-employee question in detail, it focused on the overriding effect of the CBIC Circular. The court extracted Para 3.7 of Circular No. 210/4/2024-GST and held that since the Circular is binding on the Department, and since no invoices were raised by any of the petitioner entities, the value of the services must be deemed 'Nil', resulting in zero tax liability.

Para 3.7: ...in cases where full input tax credit is available to the recipient, if the invoice is not issued by the related domestic entity with respect to any service provided by the foreign affiliate to it, the value of such services may be deemed to be declared as Nil, and may be deemed as open market value in terms of second proviso to Rule 28(1) of CGST Rules.

The court's observation on the Circular is particularly significant: while it acknowledged the Circular may possibly be asserted to be founded on a tenuous thread (i.e., the ability to avoid tax simply by not issuing invoices), it unequivocally held that it was not for the court to question the CBIC's policy wisdom the Circular binds the respondents and that is sufficient. All SCNs were quashed. The court separately held that Sony India's interest and penalty imposition could not survive once the CBIC's clarification absolved all assessees pan-India.

The Pivotal Role of CBIC Circular No. 210/4/2024-GST

All three decisions converge on the watershed importance of CBIC Circular No. 210/4/2024-GST dated 26 June 2024, issued pursuant to the recommendations of the 53rd GST Council meeting. This Circular operationalises the second proviso to Rule 28(1) of the CGST Rules, 2017 to create a definitive resolution for related-party cross-border service transactions.

The Circular establishes the following valuation framework for such transactions:

-

Where a foreign affiliate provides services to a related domestic entity and the recipient is eligible for full ITC, the value declared in the invoice shall be deemed the open market value.

-

Where no invoice is raised by the domestic entity for services received from the foreign affiliate, the value of such services shall be deemed 'Nil' and this 'Nil' value is treated as the open market value.

-

This deeming fiction is available specifically when full input tax credit is available to the recipient, a condition satisfied in virtually all B2B intra-group arrangements.

This Circular, being a binding clarification on the field formations of the Central and State tax authorities, overrides contrary departmental positions. As the Delhi High Court held, once the value is 'Nil', there is simply no taxable base and the show cause notices become "essentially rendered impotent and would serve no practical purpose."

Key Takeaways for Businesses and CFOs

A. The Two-Pronged Defence

Companies with foreign national employees or seconded expatriates now have a two-pronged, reinforcing defence against GST demands:

-

Prong 1 Schedule III Exclusion: Where direct employment contracts exist, the transaction is not a 'supply' at all under Entry 1 of Schedule III, and therefore entirely outside the GST net.

-

Prong 2 Nil Valuation under Circular 210/2024: Even if the arrangement is treated as a supply (as in secondment cases), the absence of an invoice deems the taxable value 'Nil', eliminating all tax liability.

B. Indicators That Establish Employer-Employee Relationship

Based on the court's analysis, the following factors are critical in establishing that foreign nationals are employees and not independent service providers:

-

Execution of employment agreements directly between the Indian entity and the foreign national, covering tenure, compensation, benefits, and termination.

-

Placement of the foreign national on the Indian entity's payroll, with salary paid directly in India in Indian Rupees into an Indian bank account.

-

Deduction of TDS under the Income Tax Act and filing of Indian income tax returns by the foreign national as a resident employee.

-

Administrative, functional, and disciplinary control over the foreign national vesting exclusively with the Indian entity.

-

Extension of Indian labour law benefits (PF, statutory bonus, leave, etc.) to the foreign national at par with Indian employees.

-

Furnishing of accommodation and other benefits by the Indian entity establishing the foreign national's fixed place of residence in India.

C. Distinguishing Northern Operating Systems

The Northern Operating Systems ruling is distinguishable wherever: (i) the Indian entity not the foreign company bears the economic cost without a mark-up; (ii) employment agreements are executed directly with the Indian entity; (iii) the foreign national is under the complete administrative control of the Indian entity; and (iv) the secondment is not purely task-specific but reflects genuine integration into the Indian workforce. Where these conditions are met, the NOS ruling has no application.

D. The Invoice Discipline

An important practical takeaway from the Delhi HC ruling is the significance of not raising invoices for intra-group services where the receipt of services is disputed or not acknowledged. Under the CBIC Circular, the absence of an invoice triggers the Nil valuation deeming fiction. However, companies must exercise caution this is a double-edged sword, and the CBIC may revisit this position in future amendments. Companies should maintain contemporaneous documentation of the employment relationship rather than relying solely on the invoice-absence defence.

Conclusion

The trilogy of rulings from the Karnataka and Delhi High Courts has brought much-needed clarity to a vexed area of GST law. The position that emerges is clear and unambiguous: salary paid to foreign nationals who are genuinely employed by an Indian entity does not attract GST. The law recognises the fundamental distinction between an employment relationship and a service procurement transaction, and Entry 1 of Schedule III gives this distinction full legislative force.

For businesses and tax professionals, the immediate priority should be to audit all pending show cause notices and demand orders in this area against the template set by these decisions. Where direct employment contracts, Indian payroll placement, TDS deduction, and full administrative control exist, the Department's case is legally unsustainable. Companies that have paid IGST under protest in anticipation of litigation should also explore refund options in light of these developments.

The broader lesson from this episode is the importance of maintaining robust employment documentation for foreign nationals contracts, payroll records, Form 16s, accommodation details, and proof of Indian tax residence all of which serve as a complete answer to departmental allegations. Companies that invested in sound employment structuring have emerged vindicated by the courts; those that did not must now navigate a more complex factual terrain.

Annexure: Statutory Reference Table

CGST Act, 2017

-

Section 7 read with Schedule III, Entry 1 Exclusion of employer-employee services from the definition of 'supply'

-

Section 7(2)(a) Transactions not treated as supply

-

Section 2(77) Definition of 'Non-Resident Taxable Person'

-

Section 15 Value of taxable supply

-

Section 73 Recovery of tax not paid or short paid

-

Section 128A Conditional waiver of interest and penalty (FY 2017-18 to 2019-20)

IGST Act, 2017

-

Section 2(11) Definition of 'Import of Services'

-

Section 5(3) Reverse Charge Mechanism

CGST Rules, 2017

-

Rule 28(1) Valuation of supplies between related/distinct persons; Second Proviso Nil valuation where full ITC is available

CBIC Circulars & Instructions

-

Circular No. 210/4/2024-GST dated 26 June 2024 Valuation of related party cross-border services; Para 3.7 Nil value deeming for no-invoice situations

-

CBIC Instruction No. 5/2023-GST dated 13 December 2023 Assessment of secondment cases individually; restriction on Section 74 invocation

Notification

-

Notification No. 10/2017-Integrated Tax (Rate) dated 28 June 2017 RCM on manpower supply by non-taxable territory persons.

This article is for professional reference and educational purposes only. It does not constitute legal advice.

Section 74 of GST | Section 130 of CGST Act | Section 47 of CGST Act | Rule 42 and 43 of CGST Rules | GST Portal Login

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified