GST Red Flags That Trigger Tax Scrutiny in India: A 2025 Compliance Guide

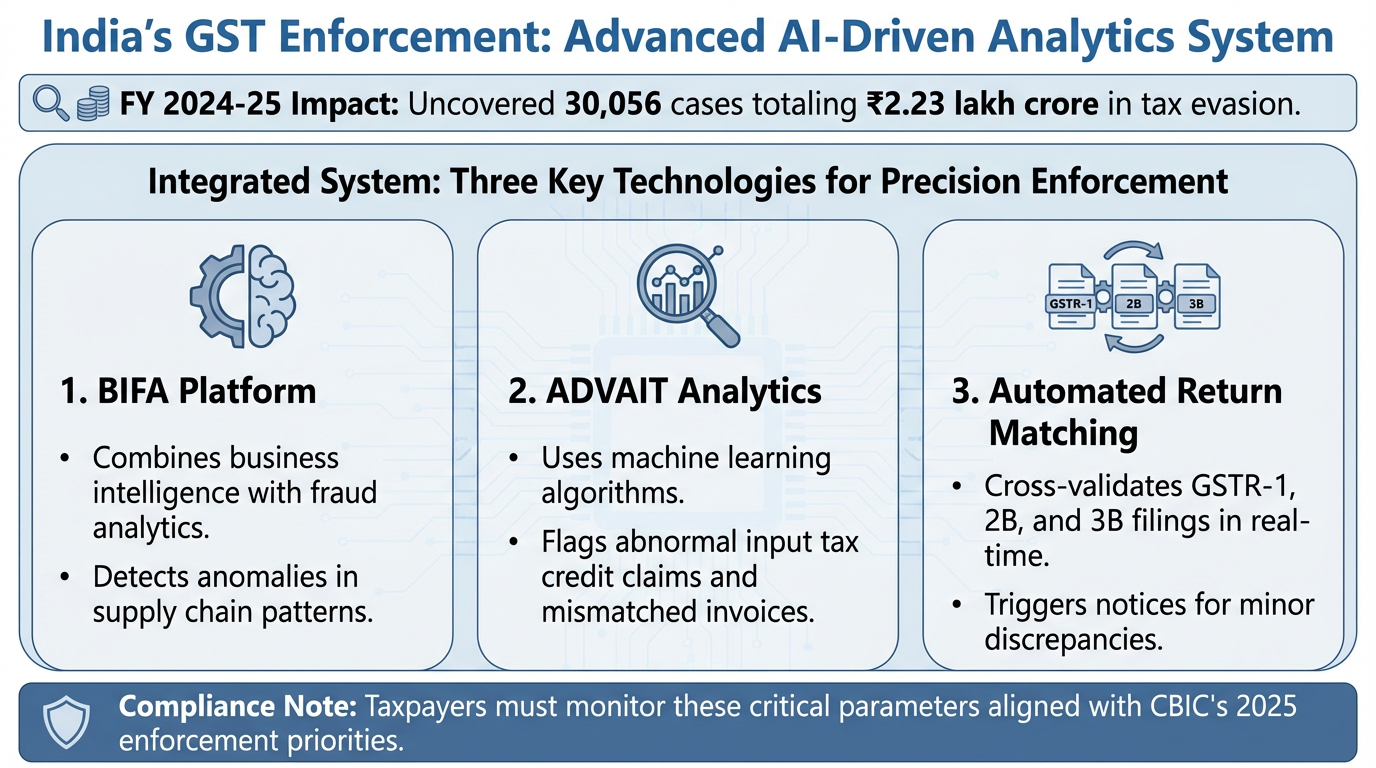

India's GST authorities now deploy sophisticated AI-powered analytics to detect tax evasion, resulting in the identification of 30,056 cases involving ₹2.23 lakh crore in evasion during FY 2024-25 alone. The combination of BIFA (Business Intelligence and Fraud Analytics), ADVAIT analytics, and automated return matching has created an environment where even minor discrepancies can trigger notices. This guide details a select few critical red flags that taxpayers and every CFO must monitor in 2025, incorporating the latest CBIC circulars, system parameters, and enforcement patterns.

Return Filing Mismatches Remain the Top Scrutiny Trigger

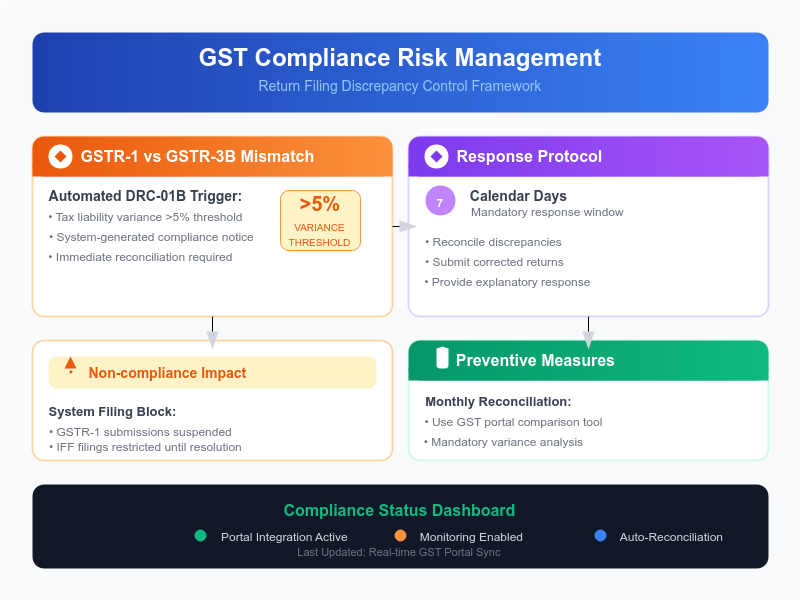

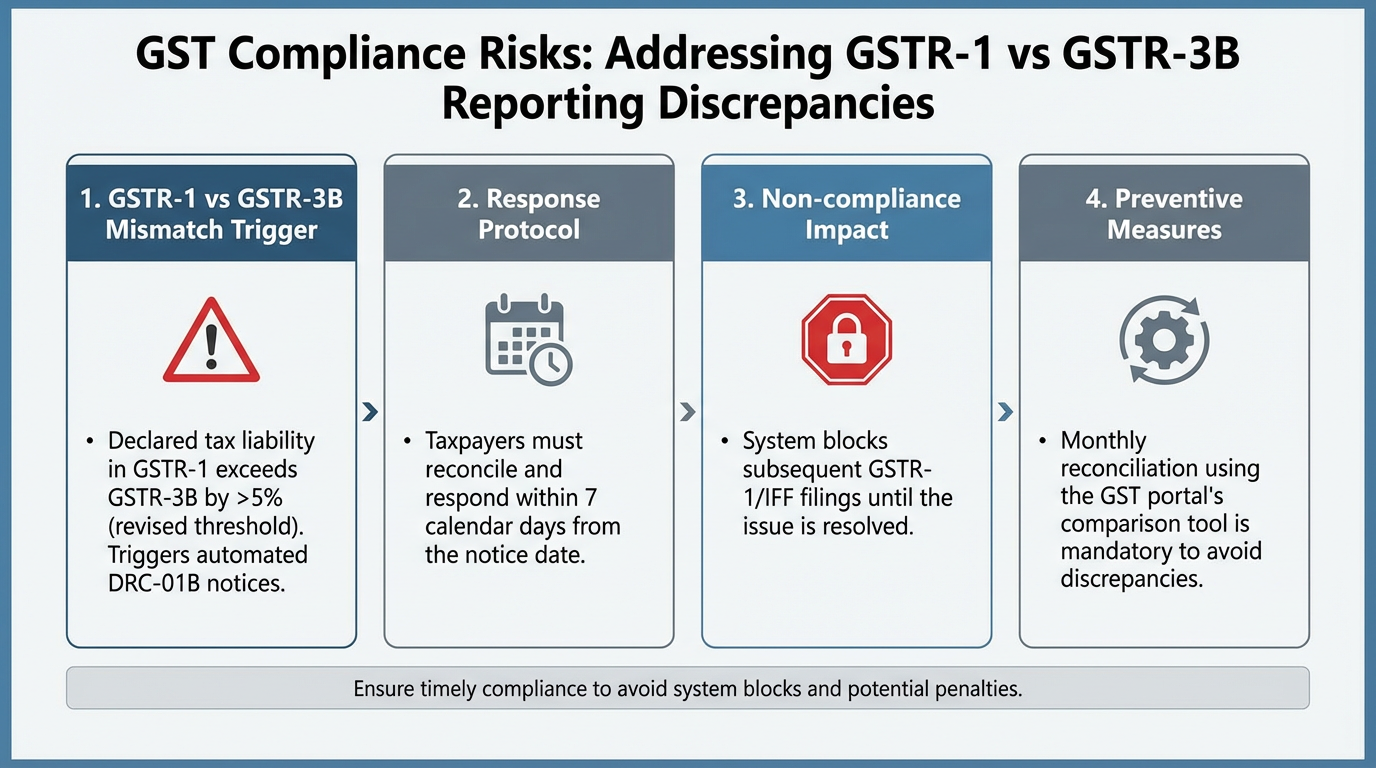

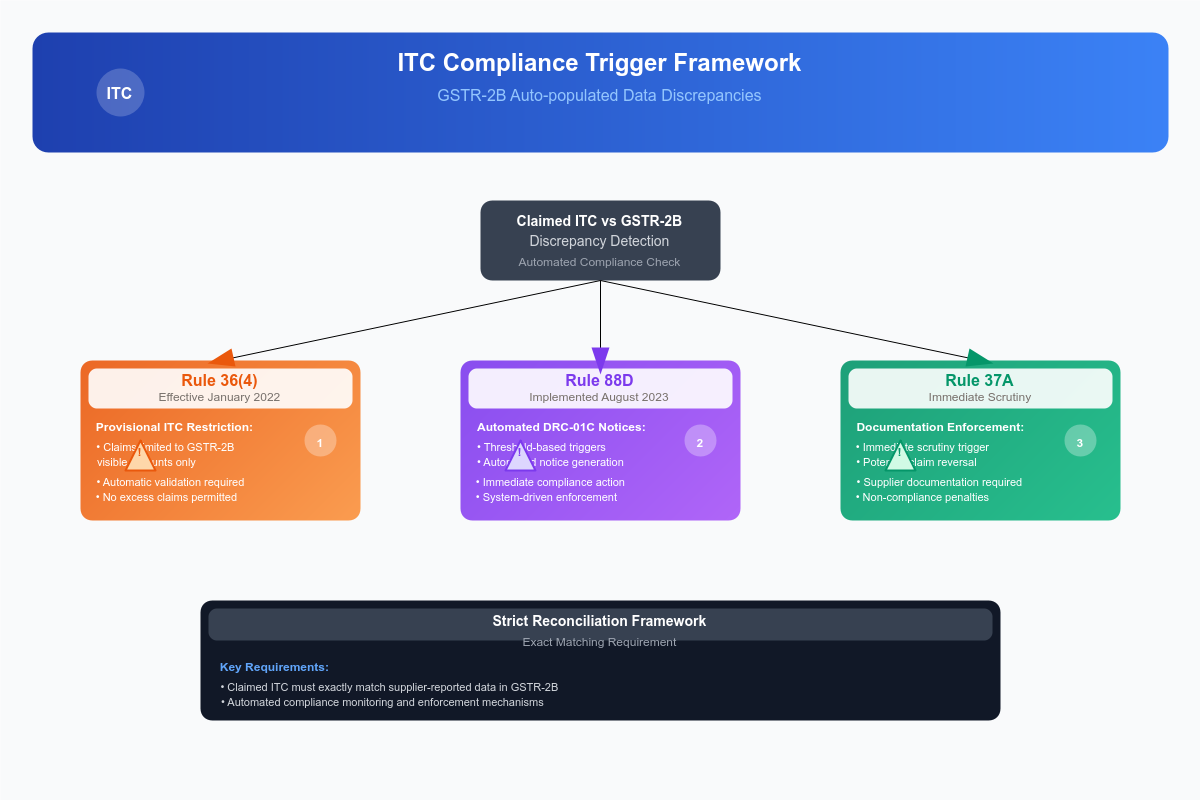

The most common red flag triggering GST notices remains discrepancies between GSTR-1 and GSTR-3B. When tax liability declared in GSTR-1 exceeds GSTR-3B by more than 5% (threshold reduced from 10%), the system automatically generates a DRC-01B notice under Rule 88C. Taxpayers must respond within 7 days, failing which GSTR-1/IFF filing for subsequent periods gets blocked.

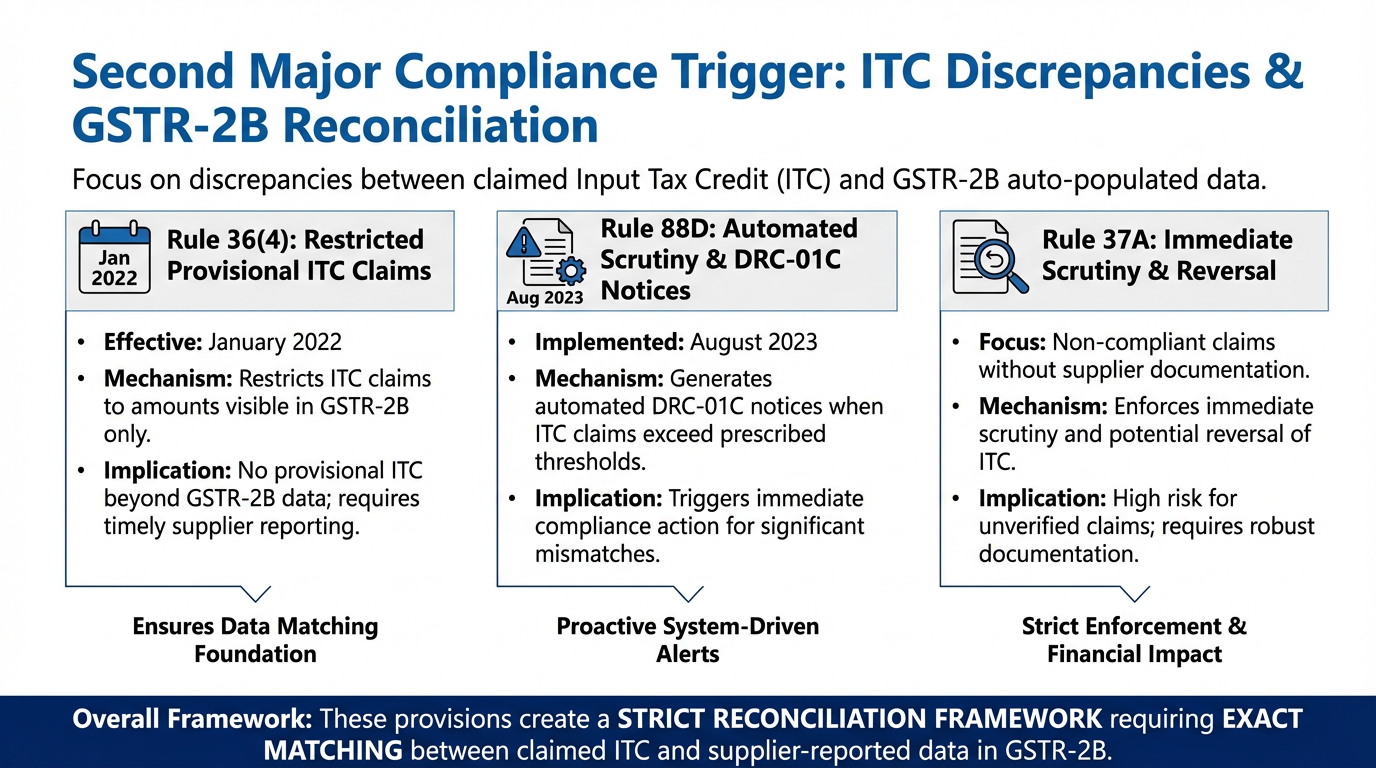

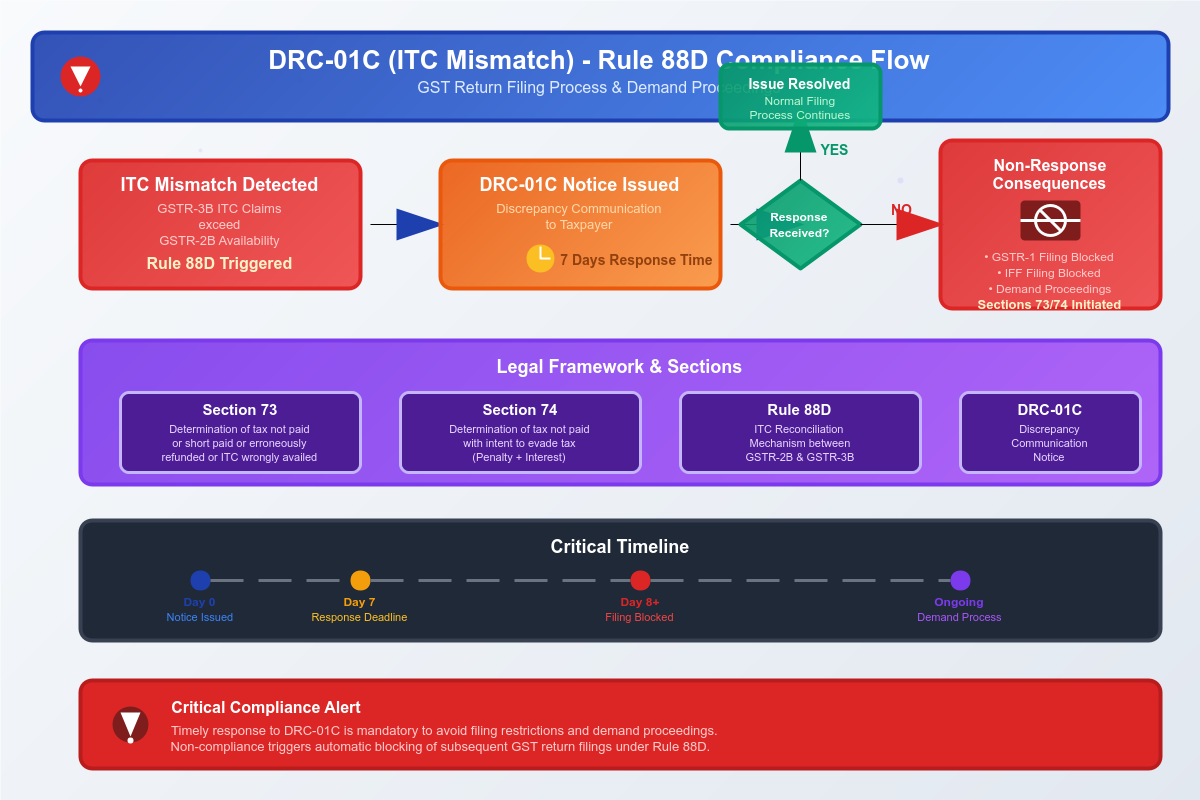

The second major trigger involves ITC claimed exceeding GSTR-2B availability. Rule 88D, notified in August 2023, enables automated DRC-01C intimations when claimed ITC surpasses auto-populated figures beyond the prescribed threshold. Since January 2022, Rule 36(4) permits zero provisional ITC—only amounts appearing in GSTR-2B can be claimed. Recipients who claim ITC without supplier compliance face immediate scrutiny and potential ITC reversal under Rule 37A.

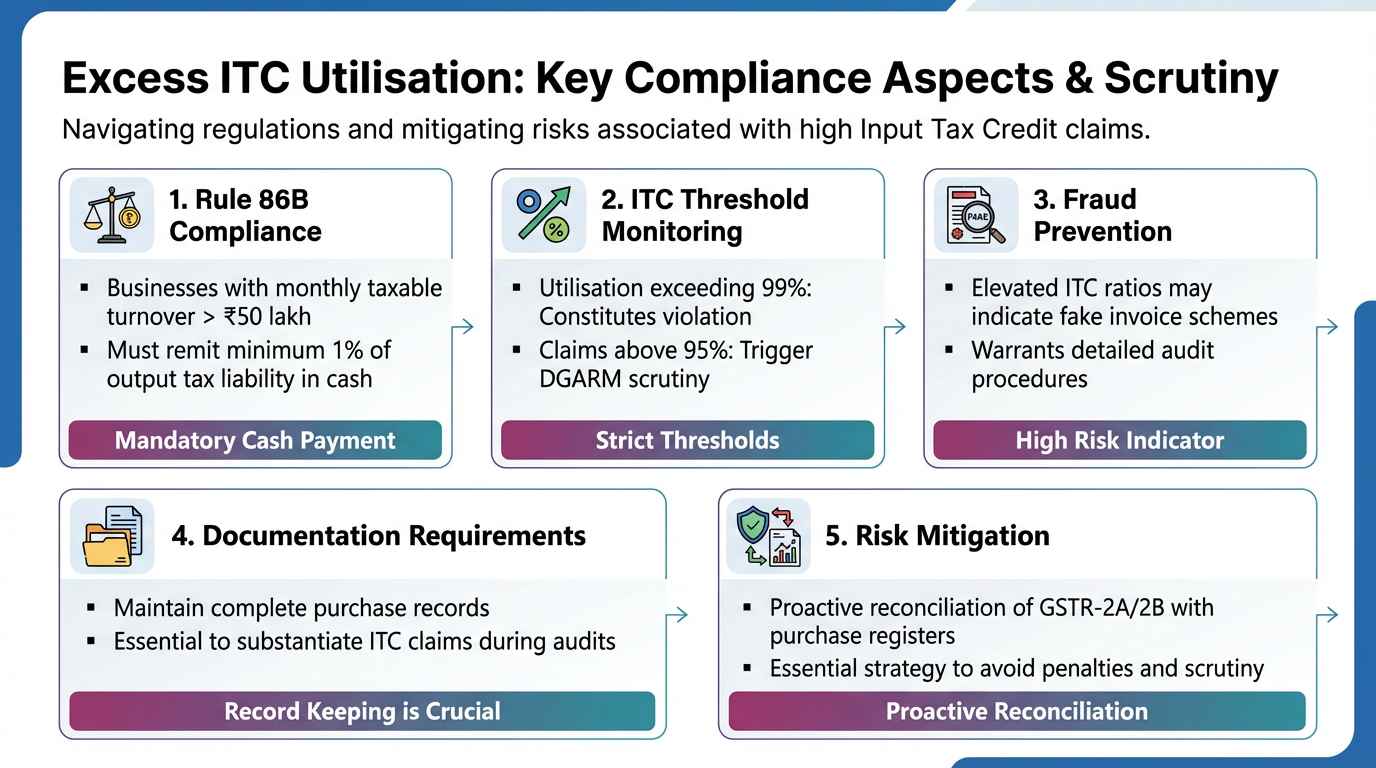

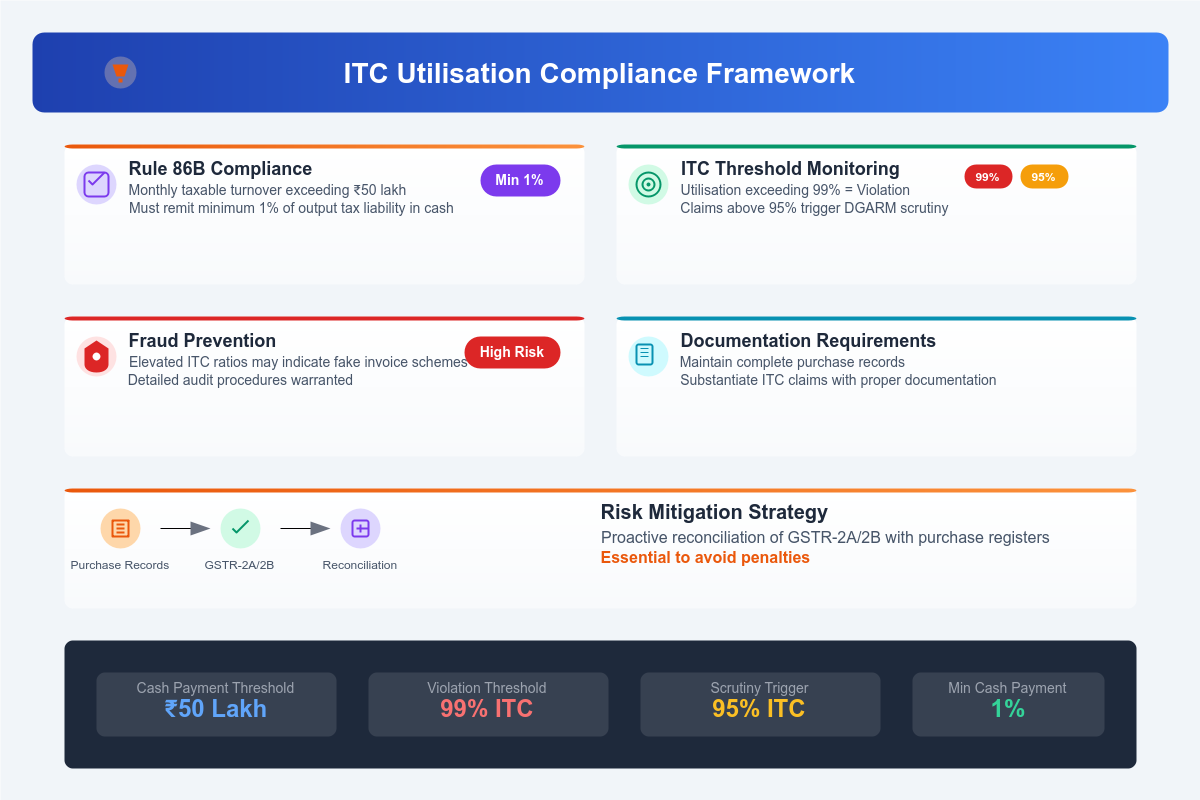

Excess ITC relative to turnover draws particular attention. Rule 86B mandates that businesses with a monthly taxable turnover exceeding ₹50 lakh must pay at least 1% of output tax liability in cash. ITC utilisation above 99% violates this provision. Furthermore, DGARM flags taxpayers with ITC utilisation above 95% as potential beneficiaries of fake invoices, triggering a detailed investigation.

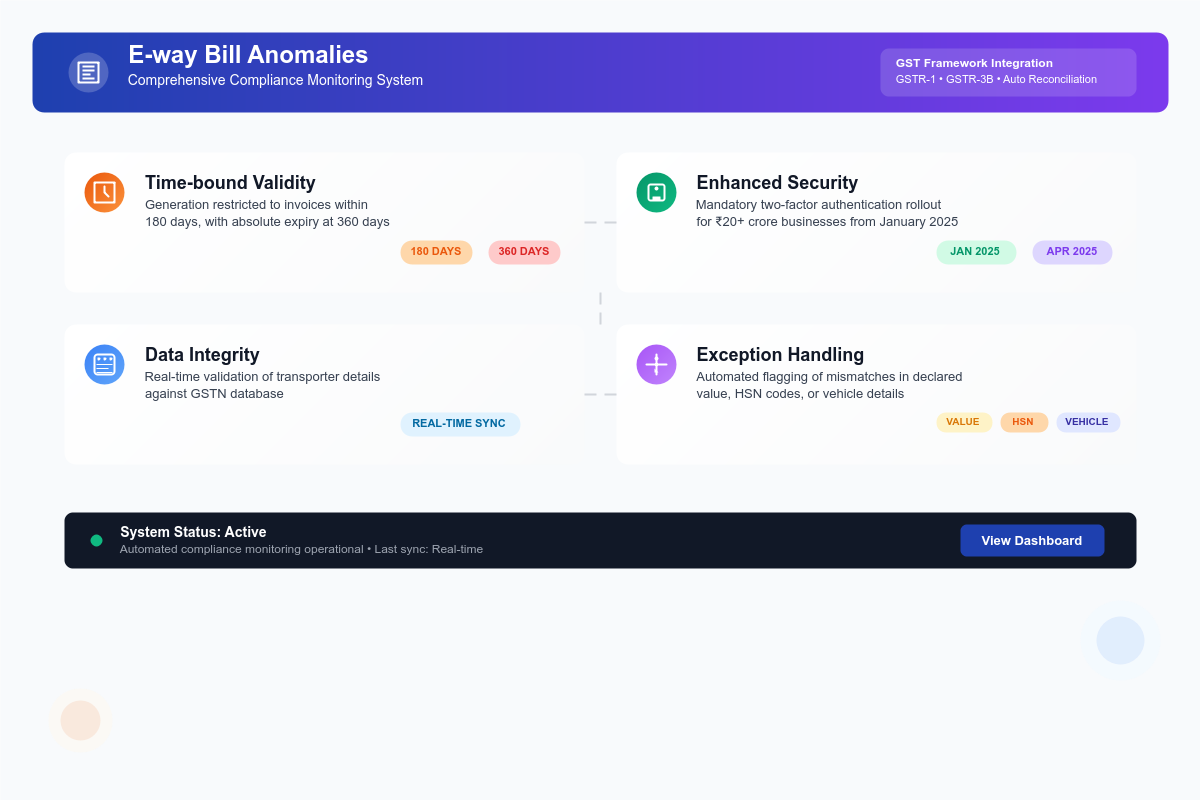

E-Way Bill Discrepancies Signal Potential Fraud

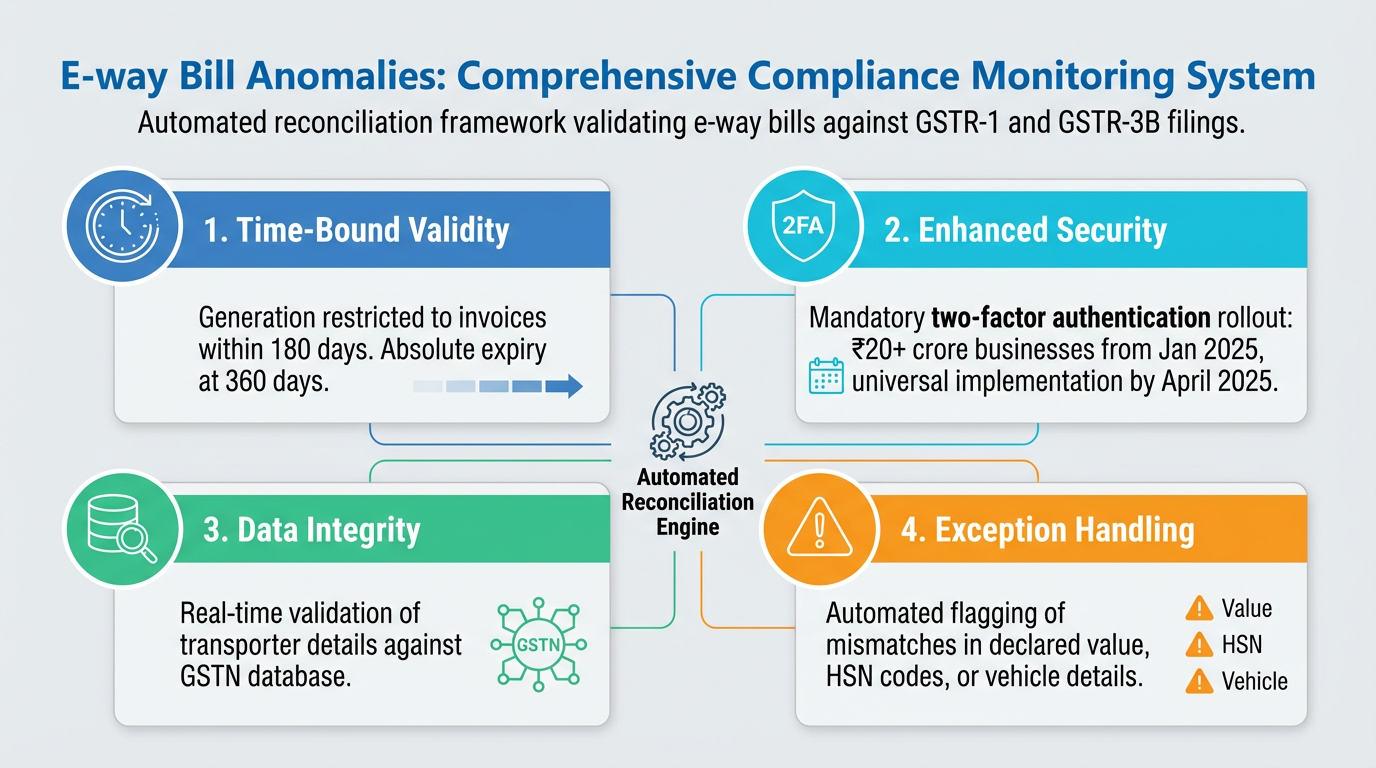

E-way bill anomalies constitute a sophisticated detection mechanism. The GST system cross-references e-way bill data with GSTR-1 and GSTR-3B declarations. From January 2025, e-way bills cannot be generated for invoices older than 180 days, with extensions capped at 360 days maximum. Two-factor authentication became mandatory for businesses with a turnover of over ₹20 crore from January 2025, extending to all taxpayers by April 2025.

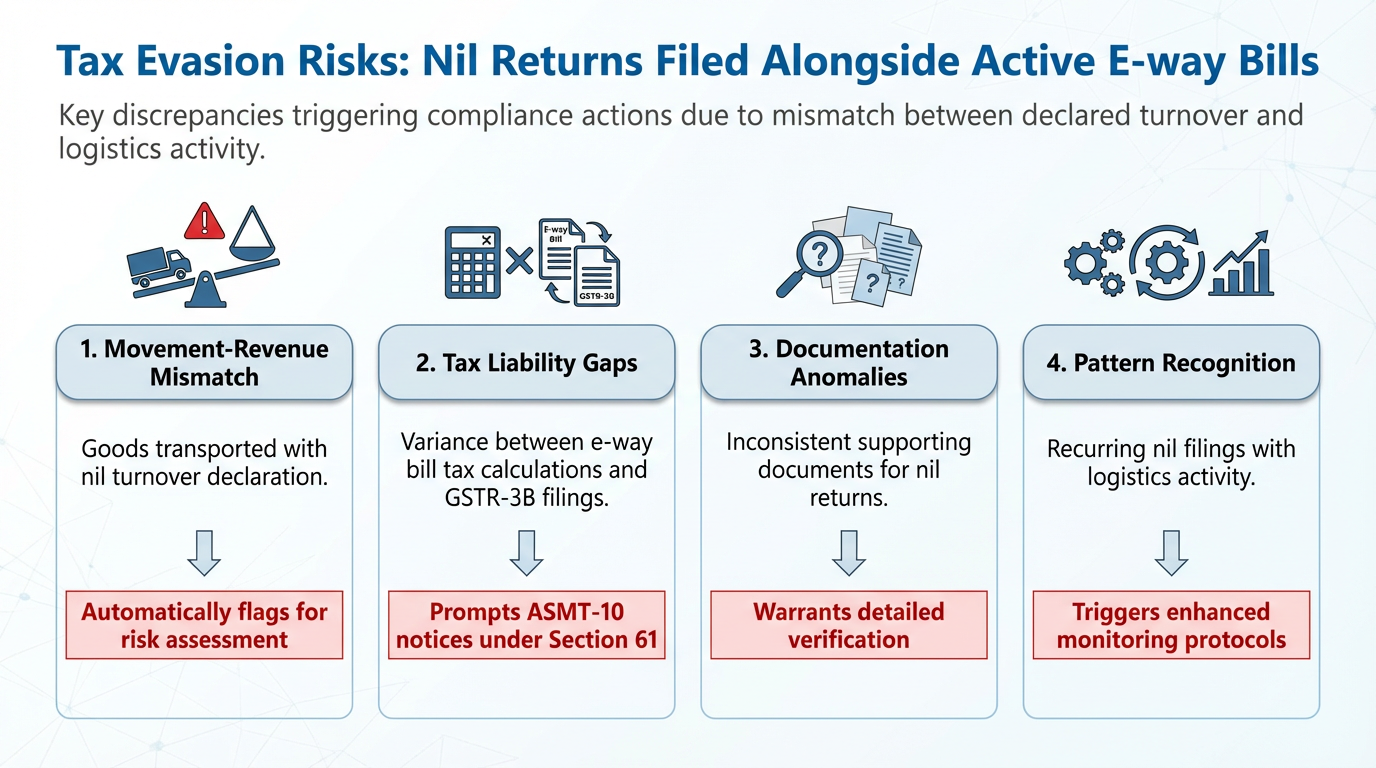

Nil returns filed by businesses with active e-way bills represent an immediate red flag. The mismatch between declared nil turnover and documented goods movement triggers automatic risk profiling. Similarly, significant differences between tax liability in e-way bills versus GSTR-3B result in ASMT-10 scrutiny notices under Section 61.

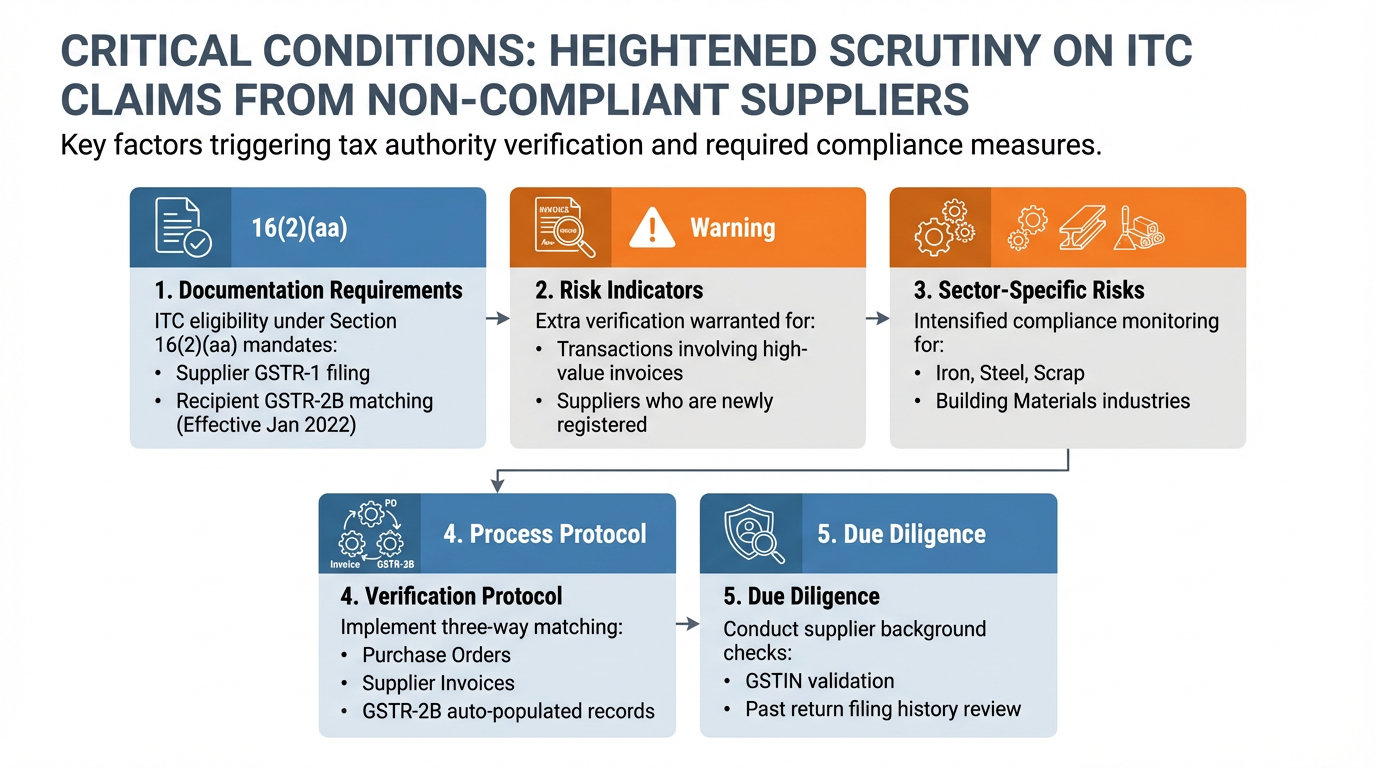

Supplier-Related Risks Have Intensified Verification Requirements

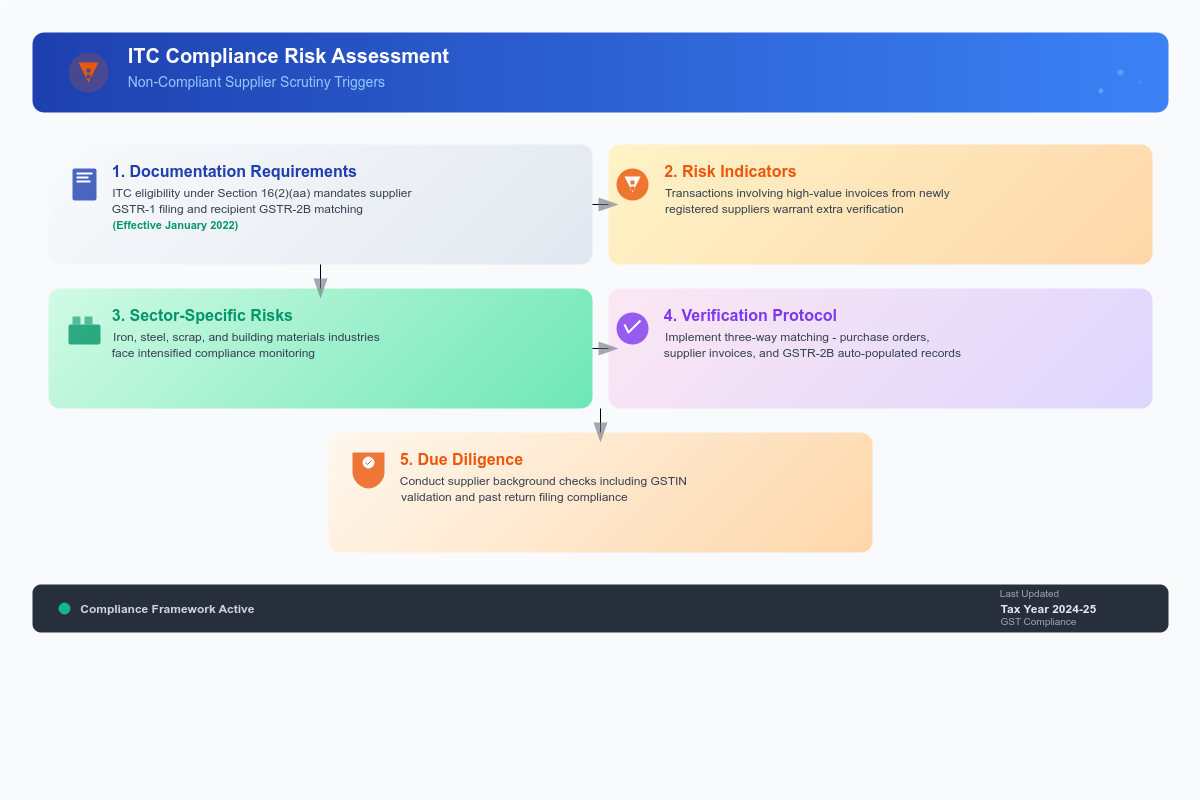

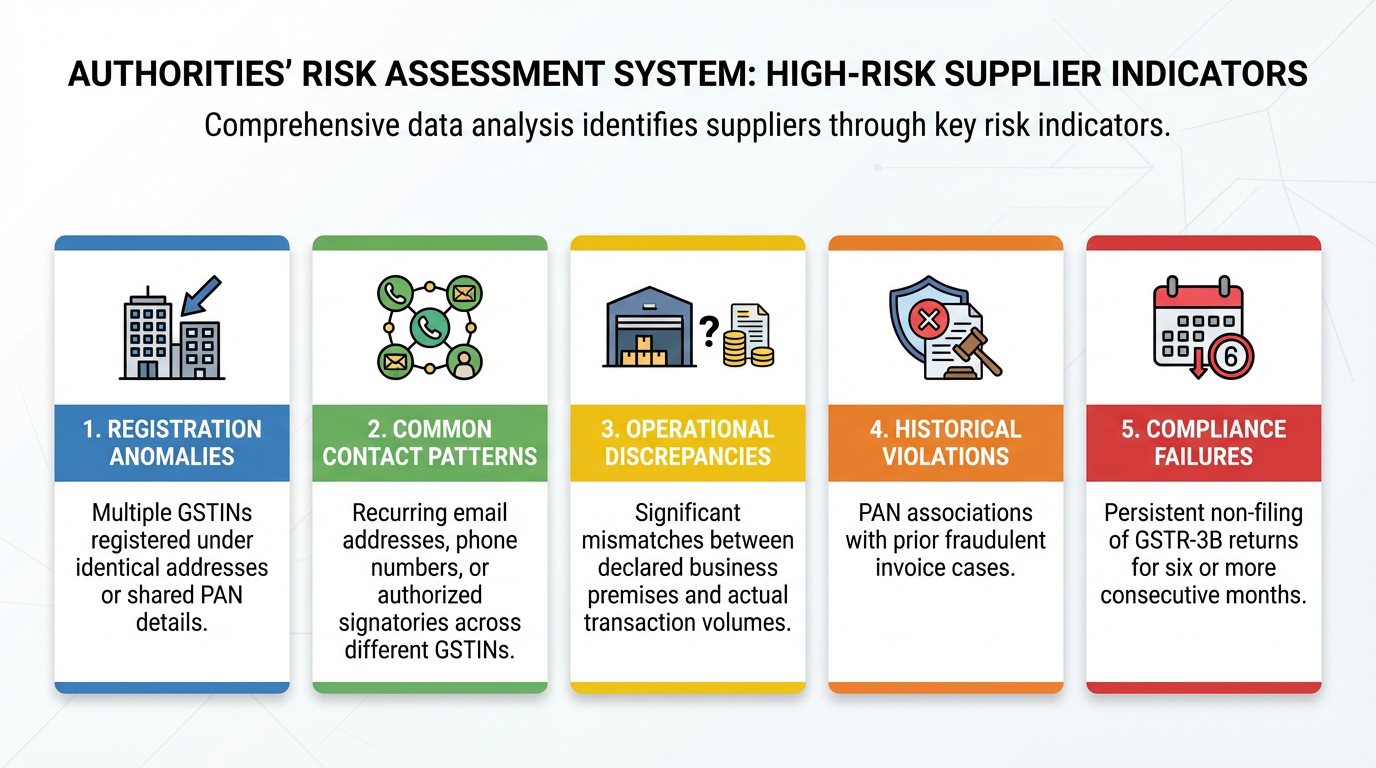

Claiming ITC from suppliers who haven't filed GSTR-1 or GSTR-3B triggers immediate scrutiny. Section 16(2)(aa), effective since January 2022, conditions ITC availability on the supplier's GSTR-1 filing and appearance in the recipient's GSTR-2B. High-value invoices from newly registered suppliers constitute a major red flag, particularly in high-risk sectors like iron, steel, scrap, and building materials.

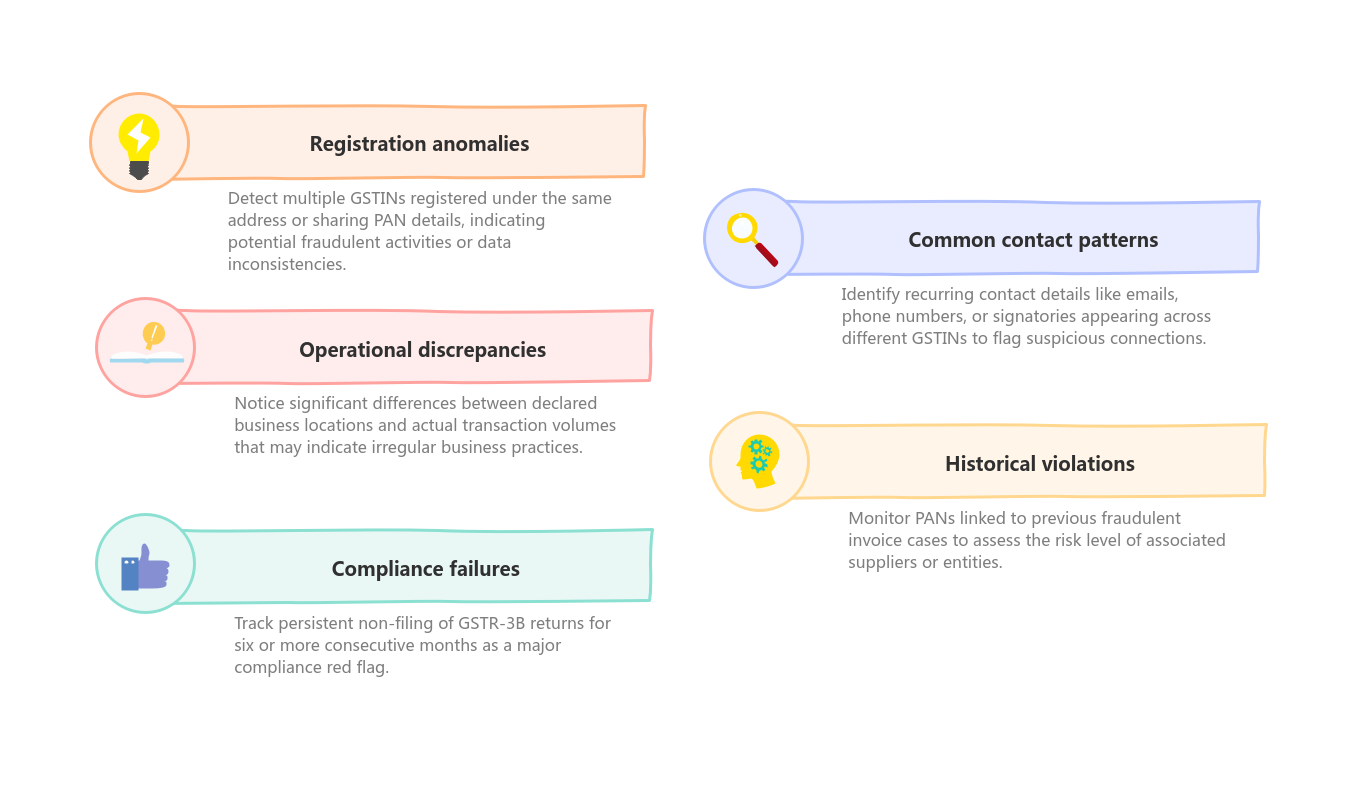

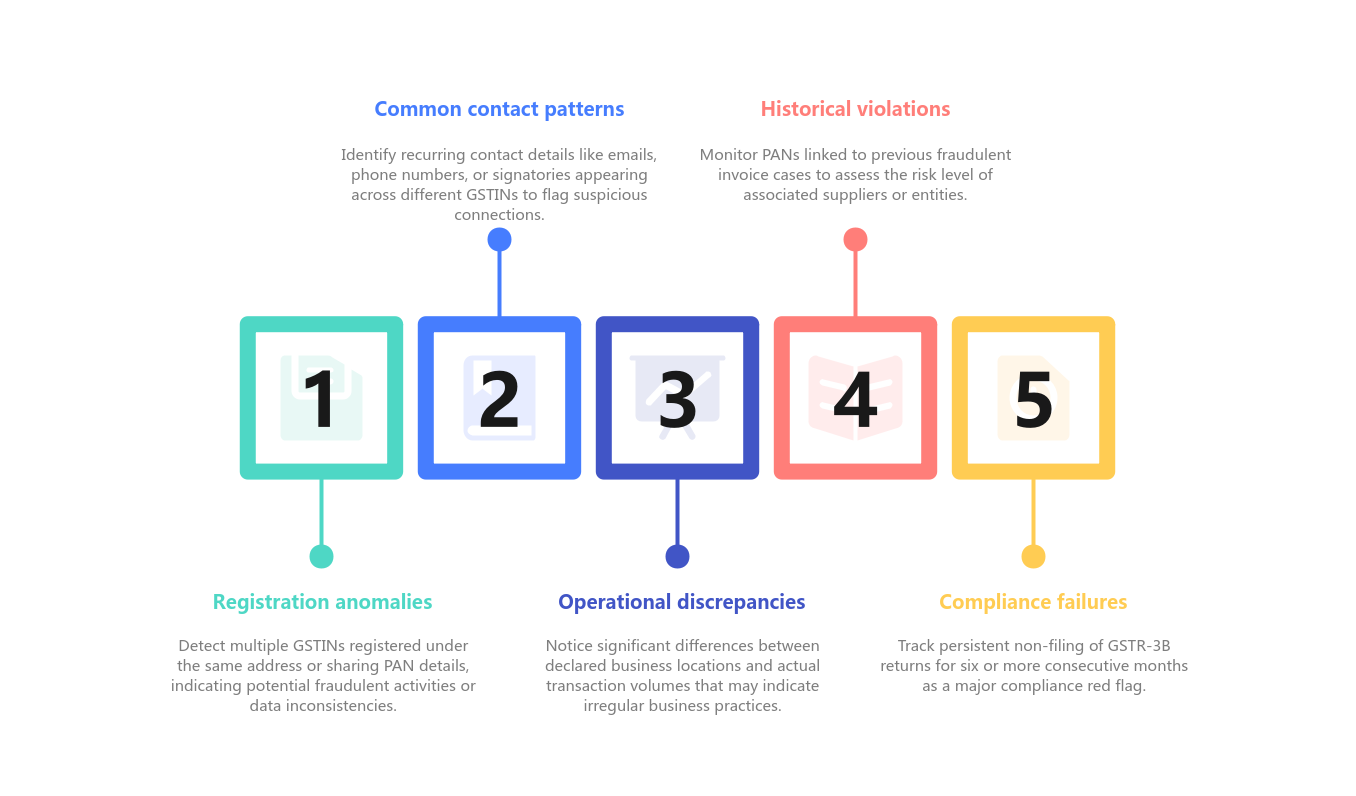

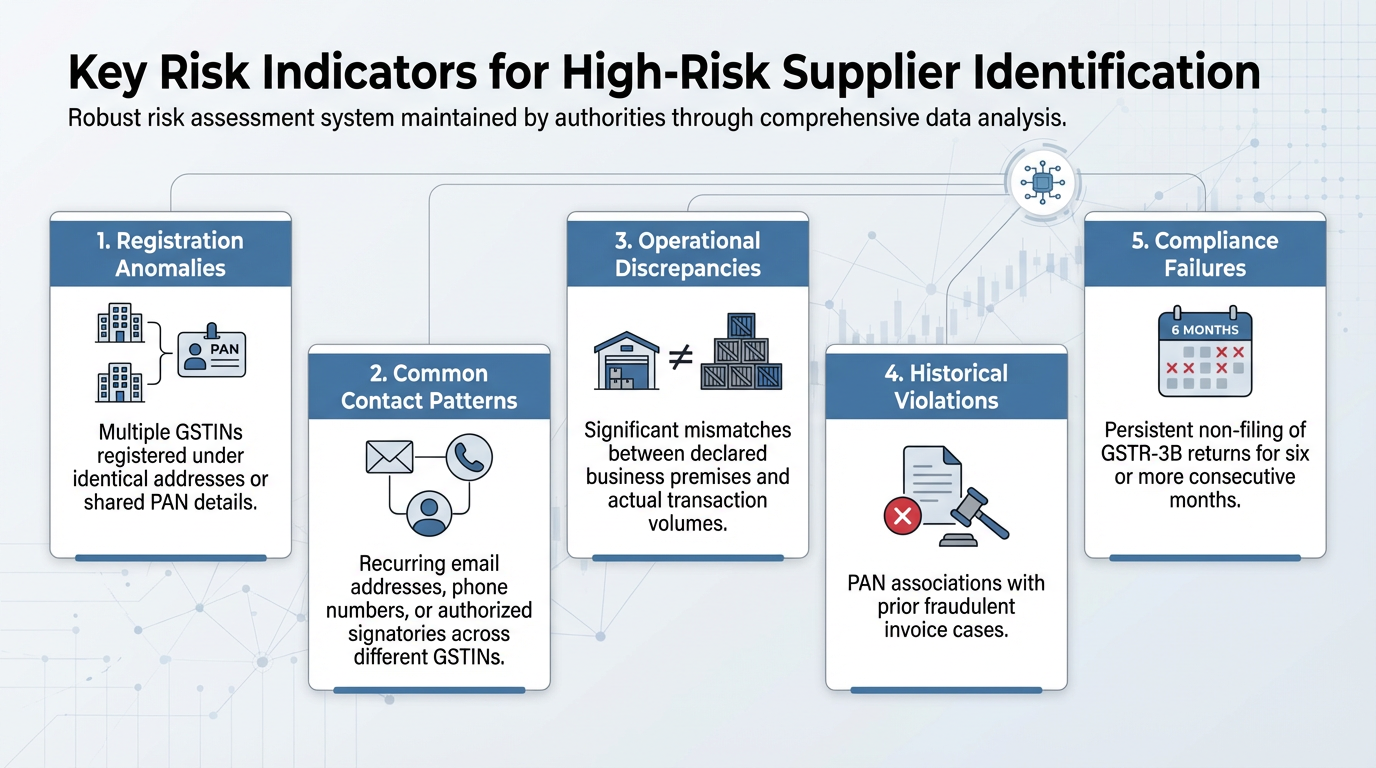

The authorities maintain a comprehensive risk database identifying "risky suppliers" based on multiple parameters:

- Multiple GSTIN registrations at the same address or under the same PAN

- Common email addresses, mobile numbers, or authorised signatories across GSTINs

- Mismatch between declared premises and transaction volumes

- PAN appearing in previous fake invoice cases

- Non-filing of GSTR-3B for 6+ consecutive months

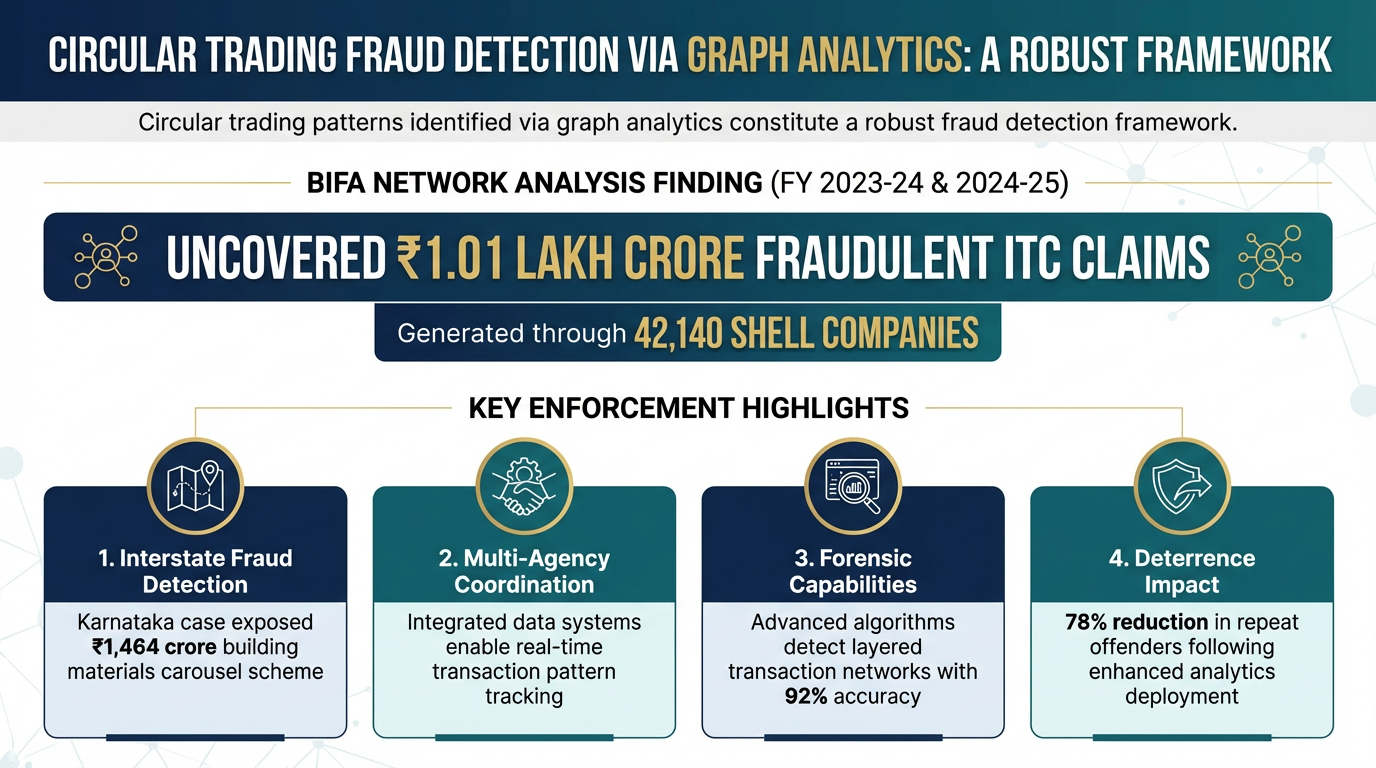

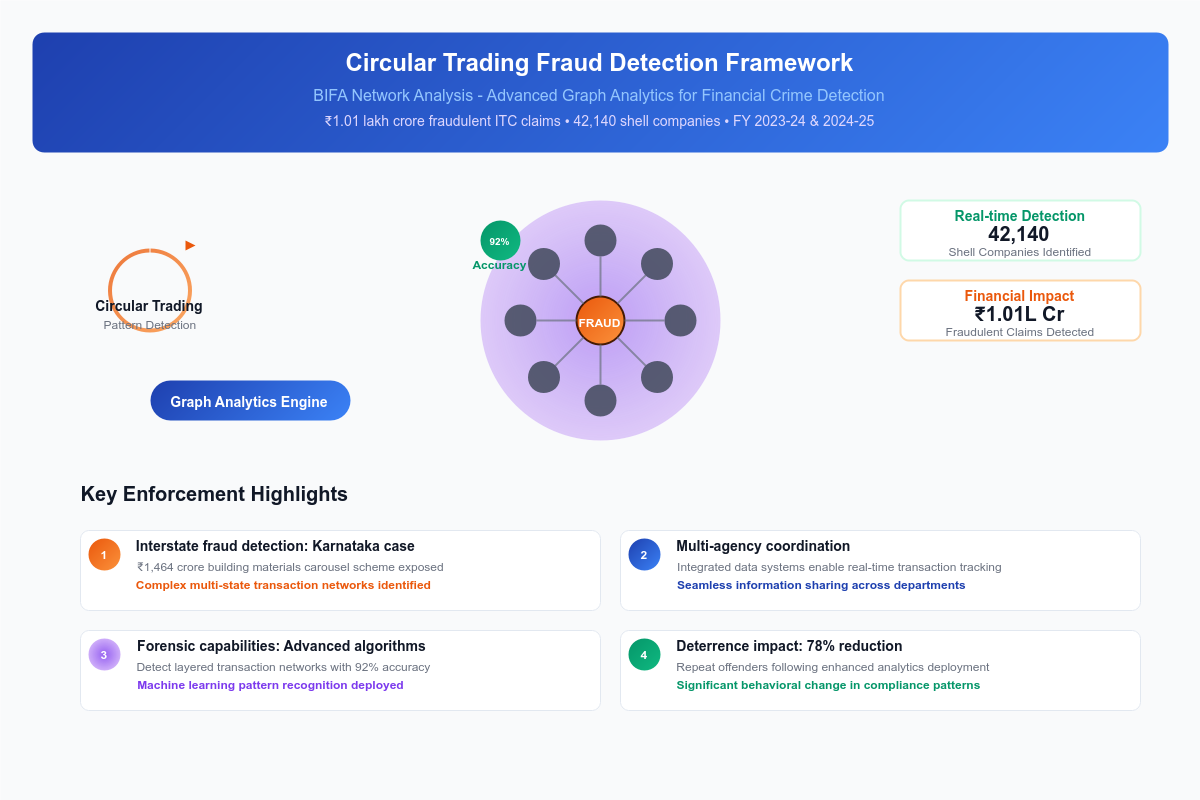

Circular trading patterns detected through graph analytics form a critical detection mechanism. BIFA's network analysis capabilities identified ₹1.01 lakh crore in bogus ITC generated through 42,140 fake firms during FY 2023-24 and 2024-25. The Karnataka case involving ₹1,464 crore interstate carousel fraud through circular trading in building materials exemplifies enforcement intensity.

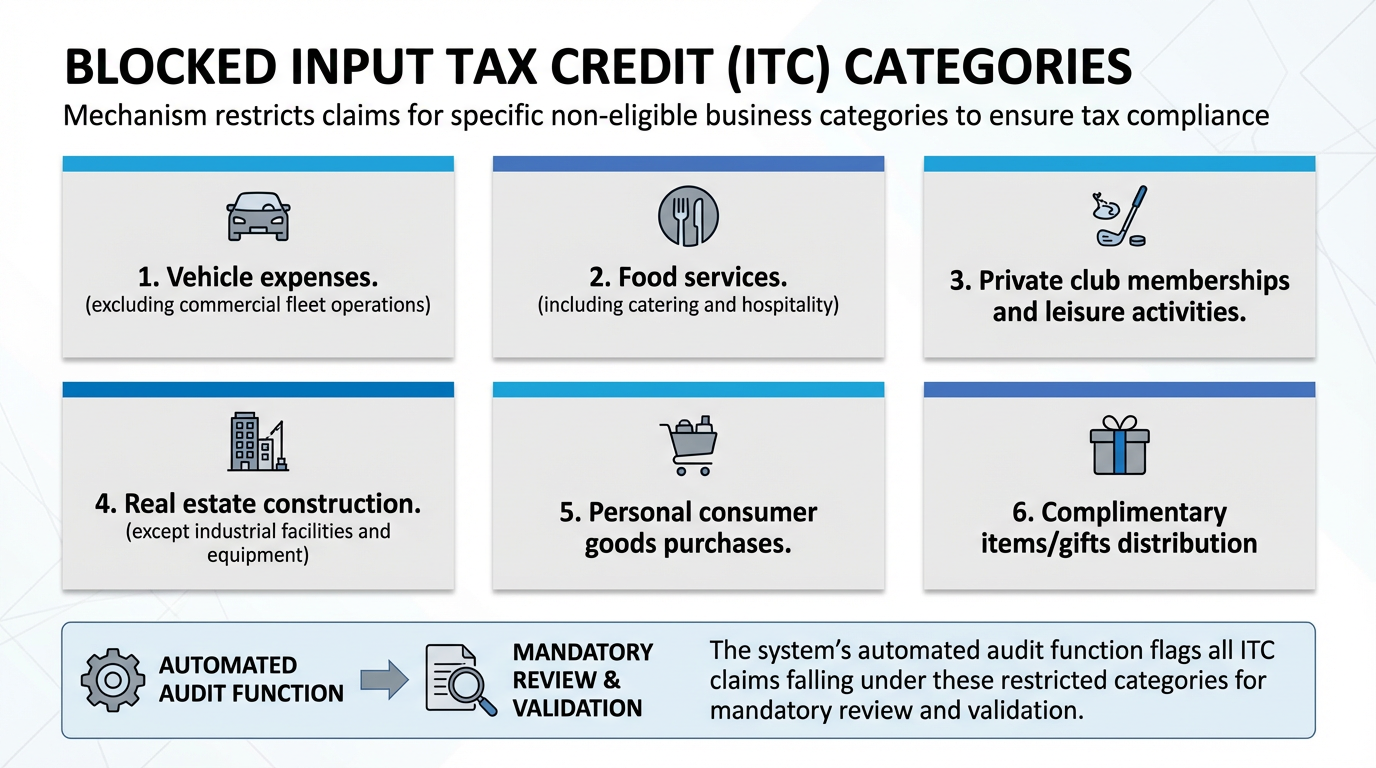

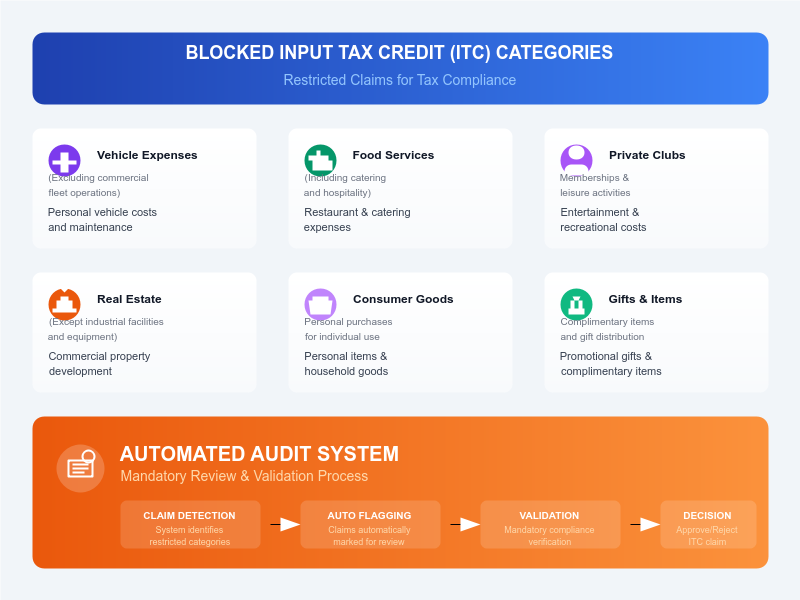

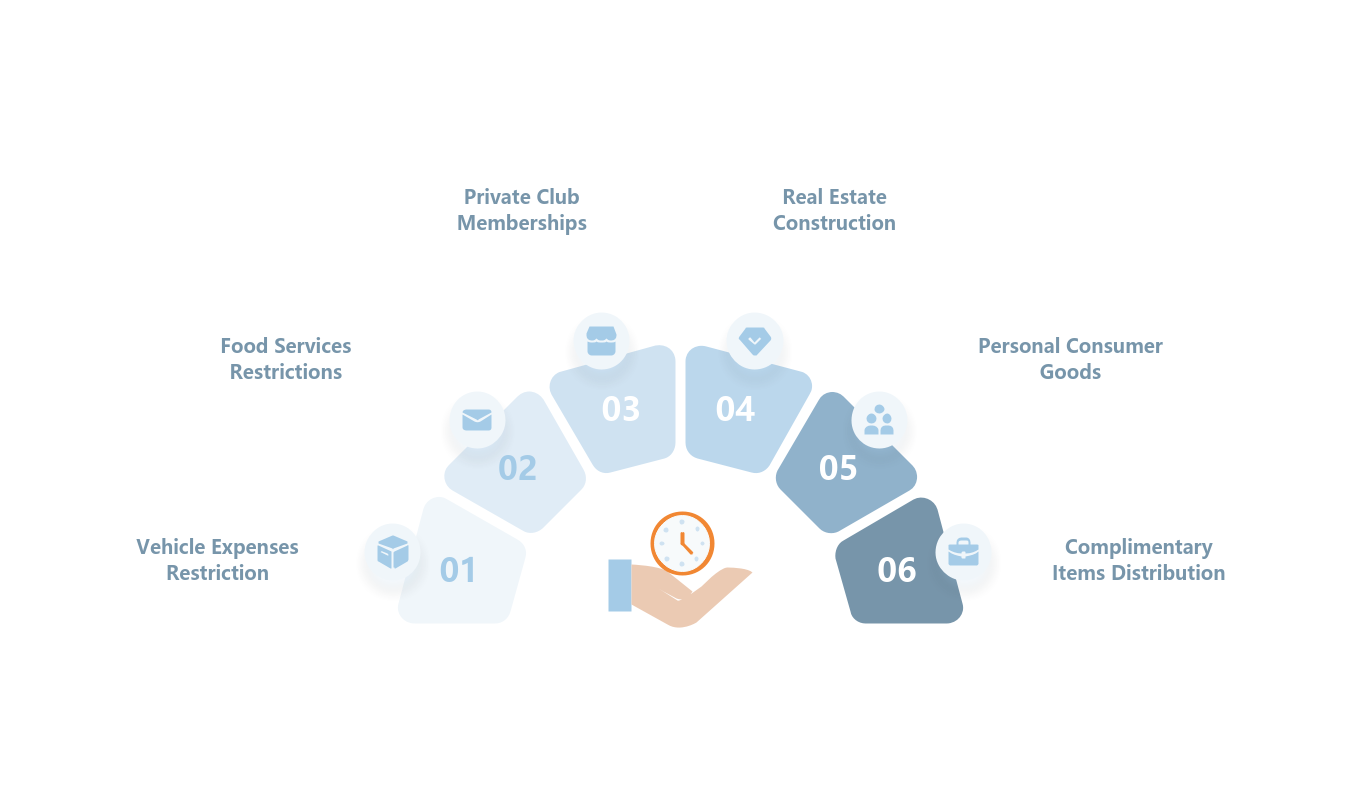

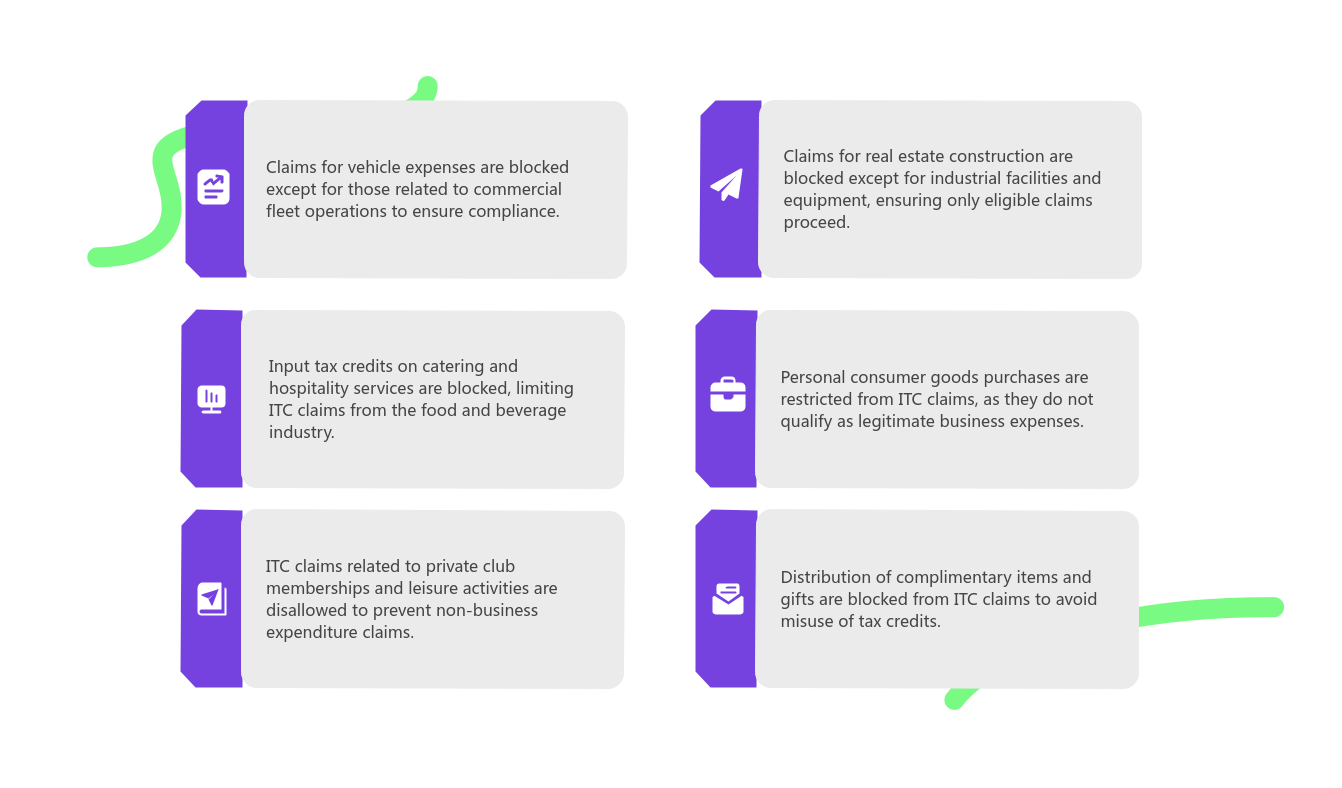

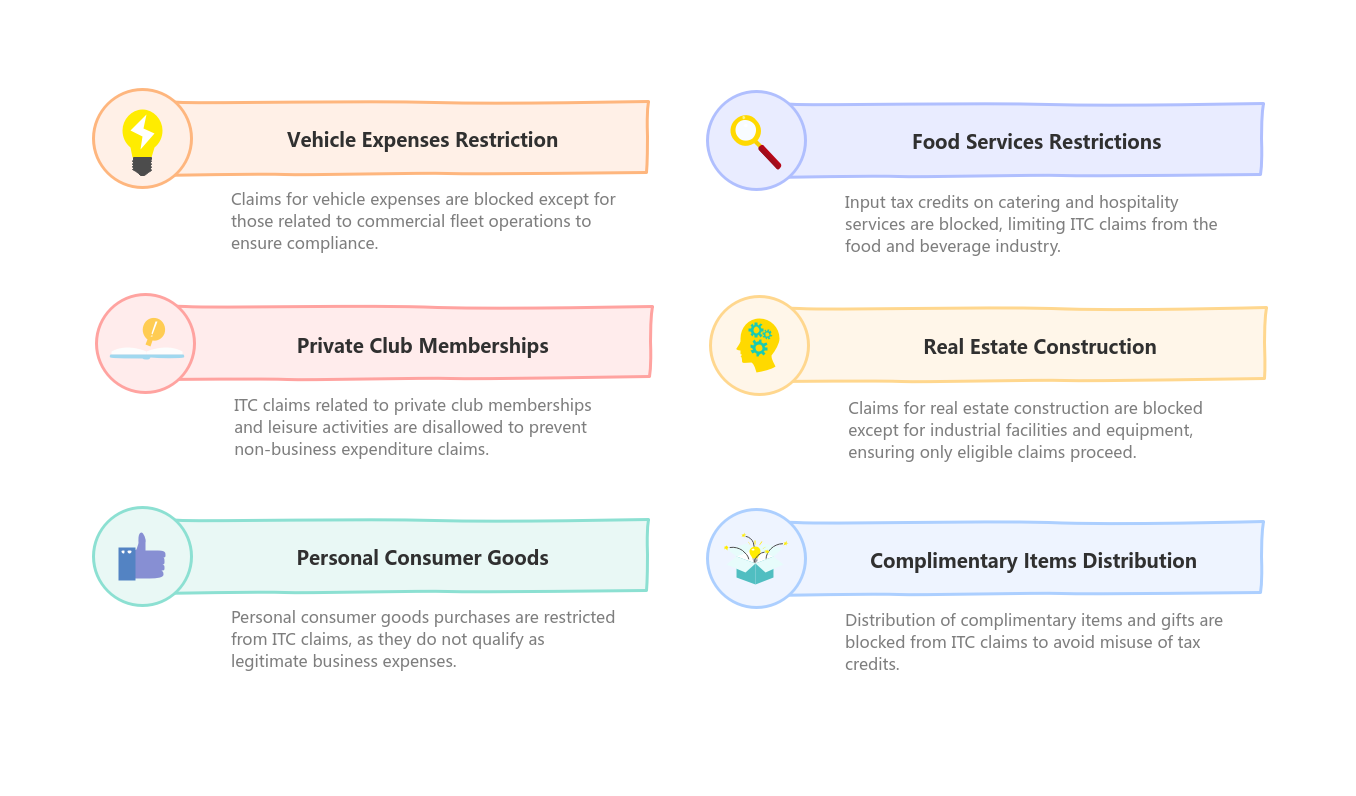

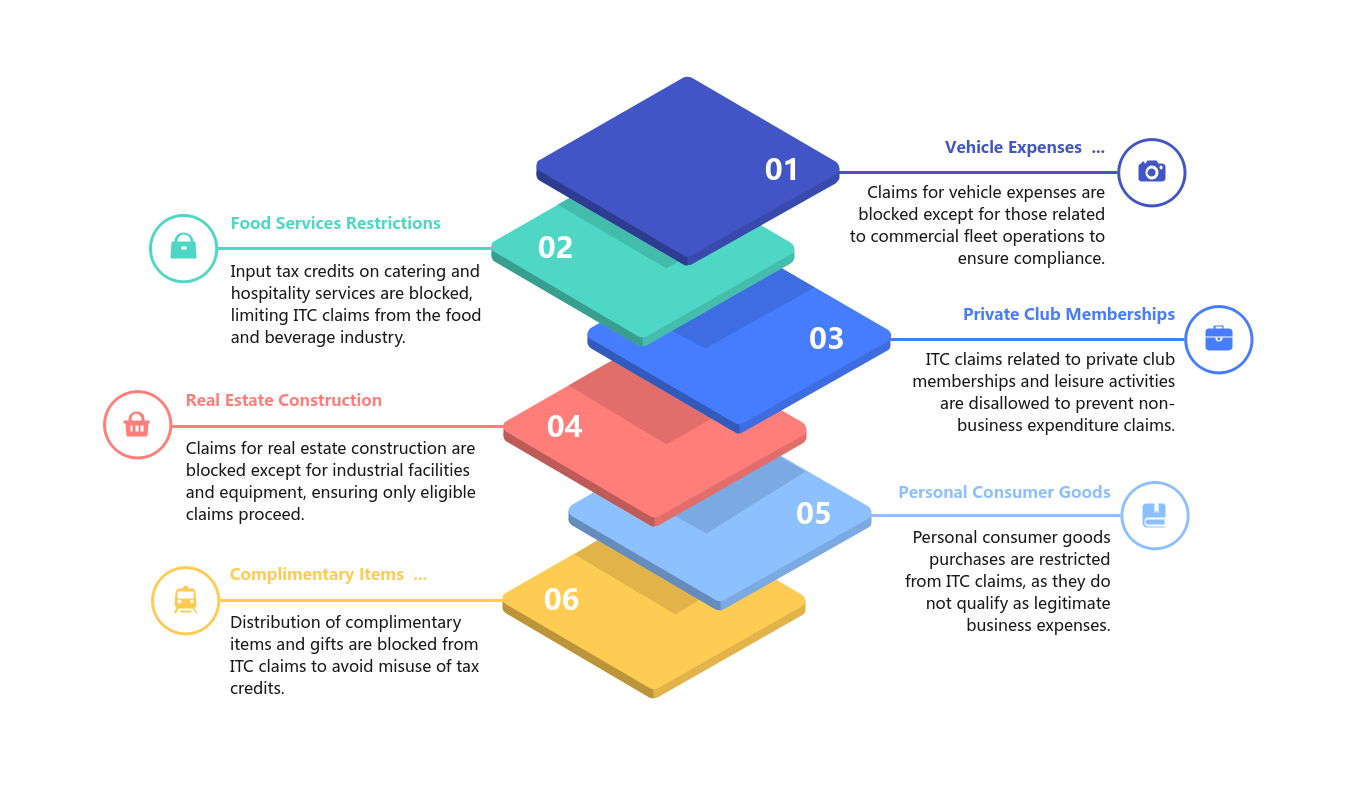

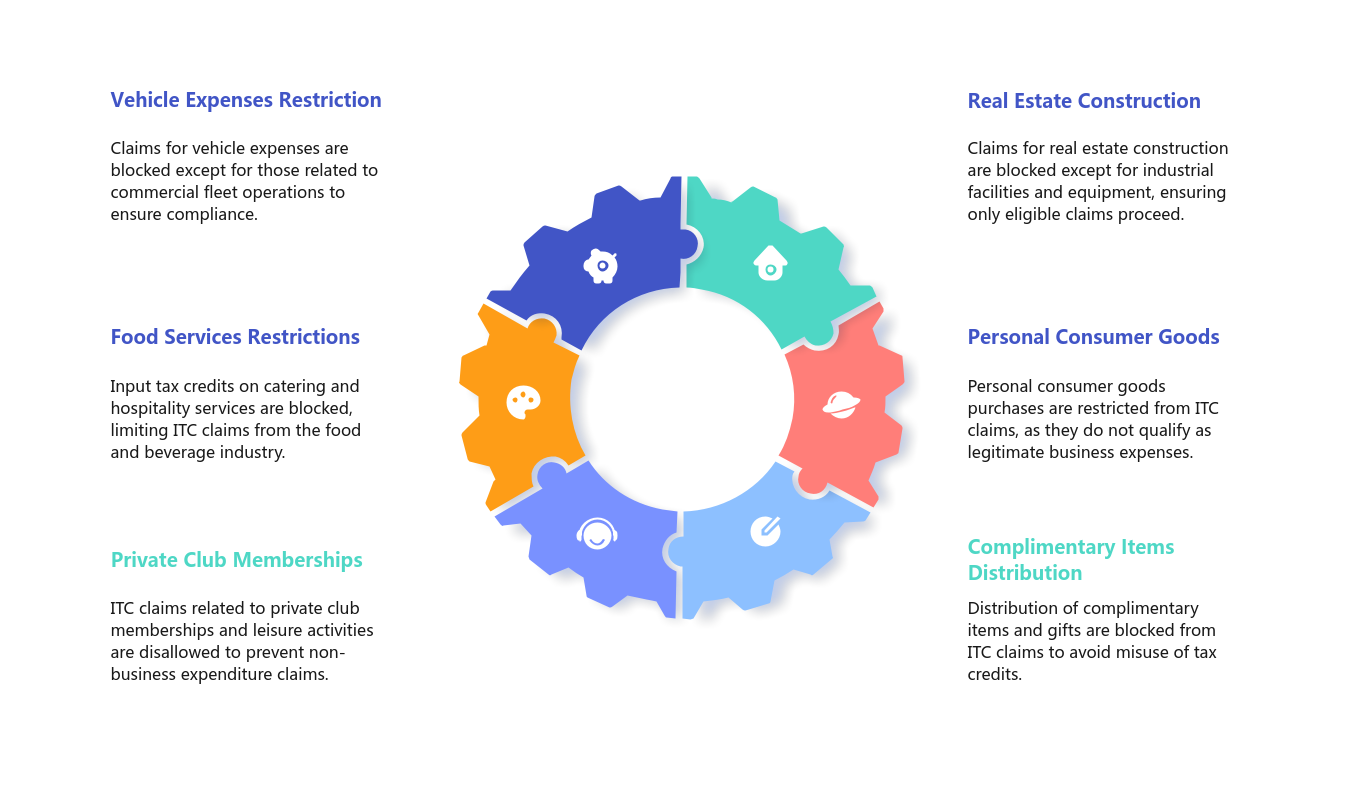

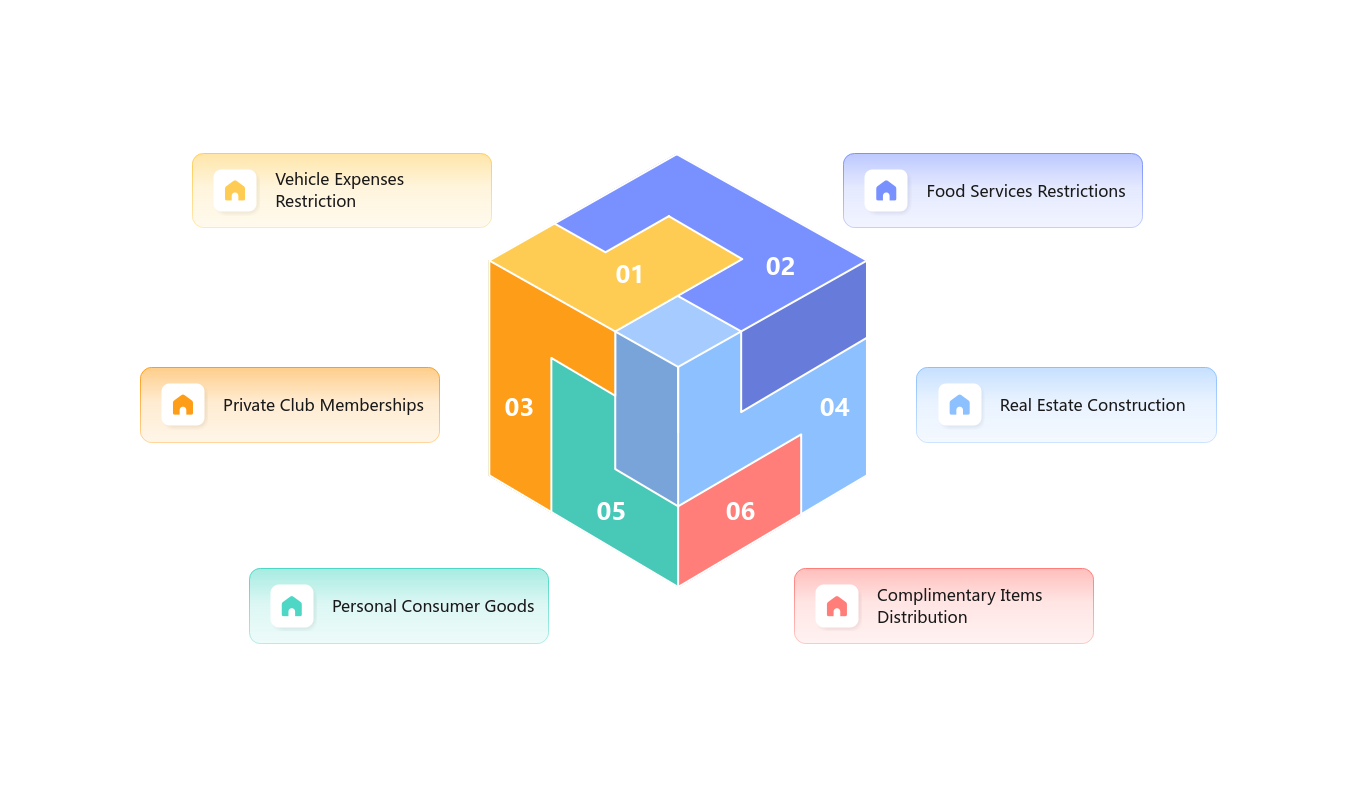

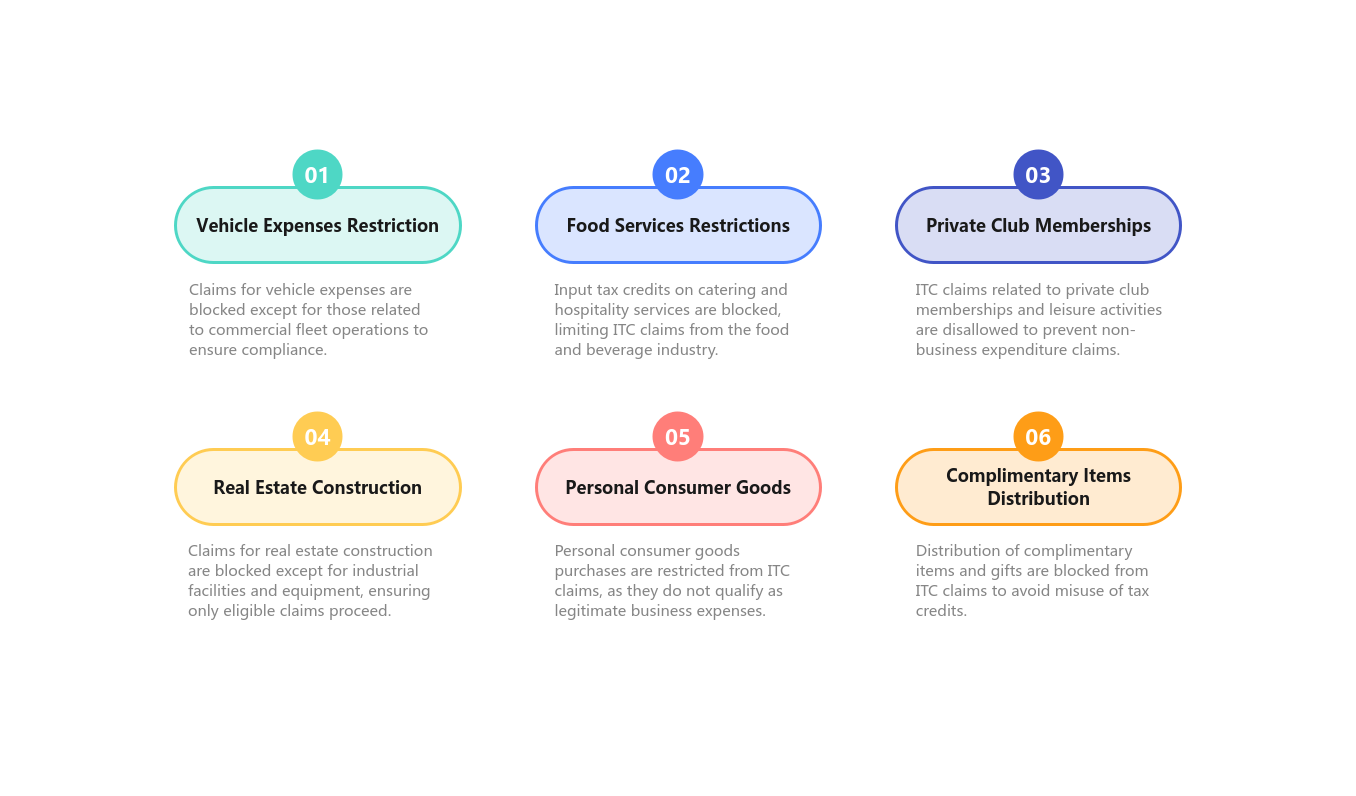

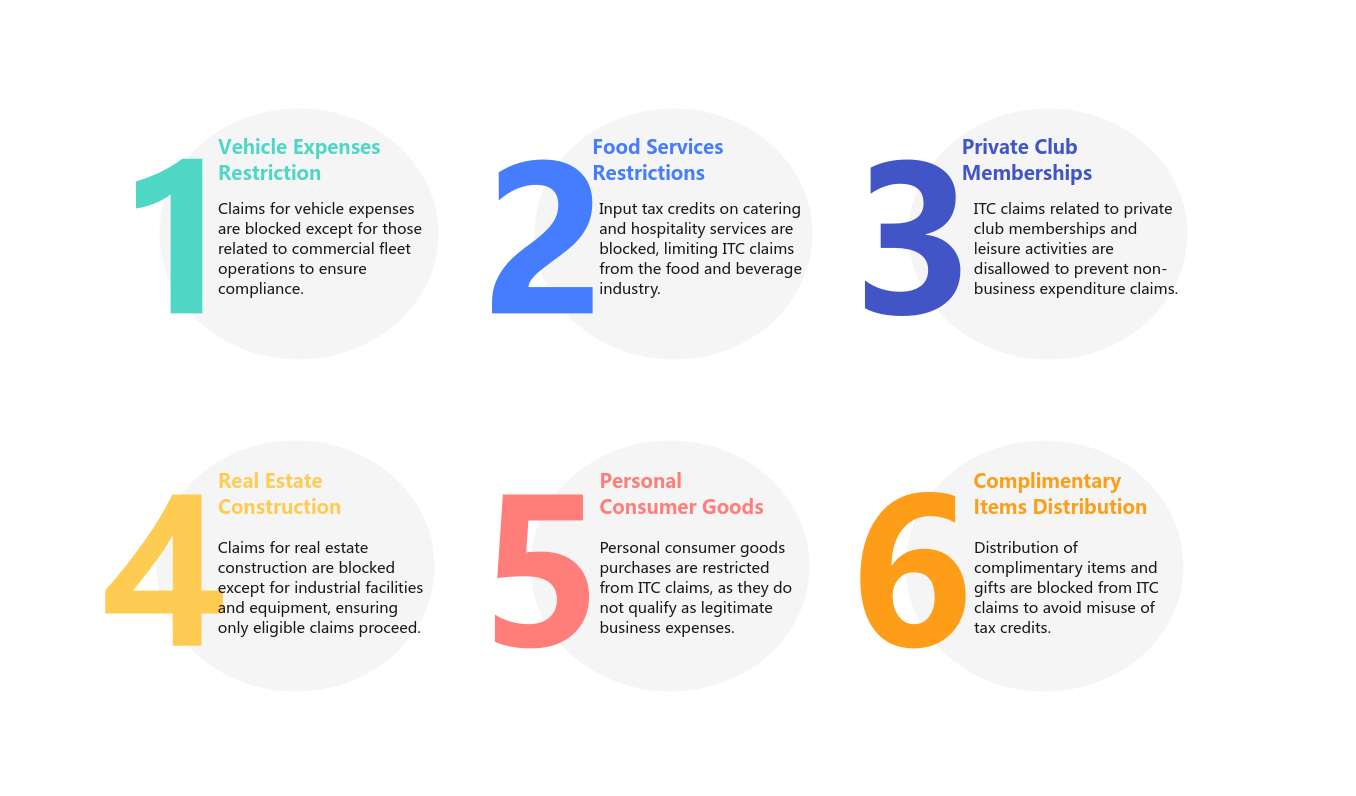

Blocked Credits Under Section 17(5) Face Enhanced Monitoring

Claiming ITC on blocked credits under Section 17(5) remains a significant red flag. The 55th GST Council meeting (December 2024) recommended amending Section 17(5)(d) to replace "plant or machinery" with "plant and machinery"—retrospective from July 1, 2017—following the Safari Retreats Supreme Court ruling.

Key blocked categories include motor vehicles (except for specified businesses), food and beverages, outdoor catering, club memberships, construction of immovable property (except plant and machinery), personal consumption goods, and gifts or free samples. The automated scrutiny module specifically identifies ITC claims against these categories for verification.

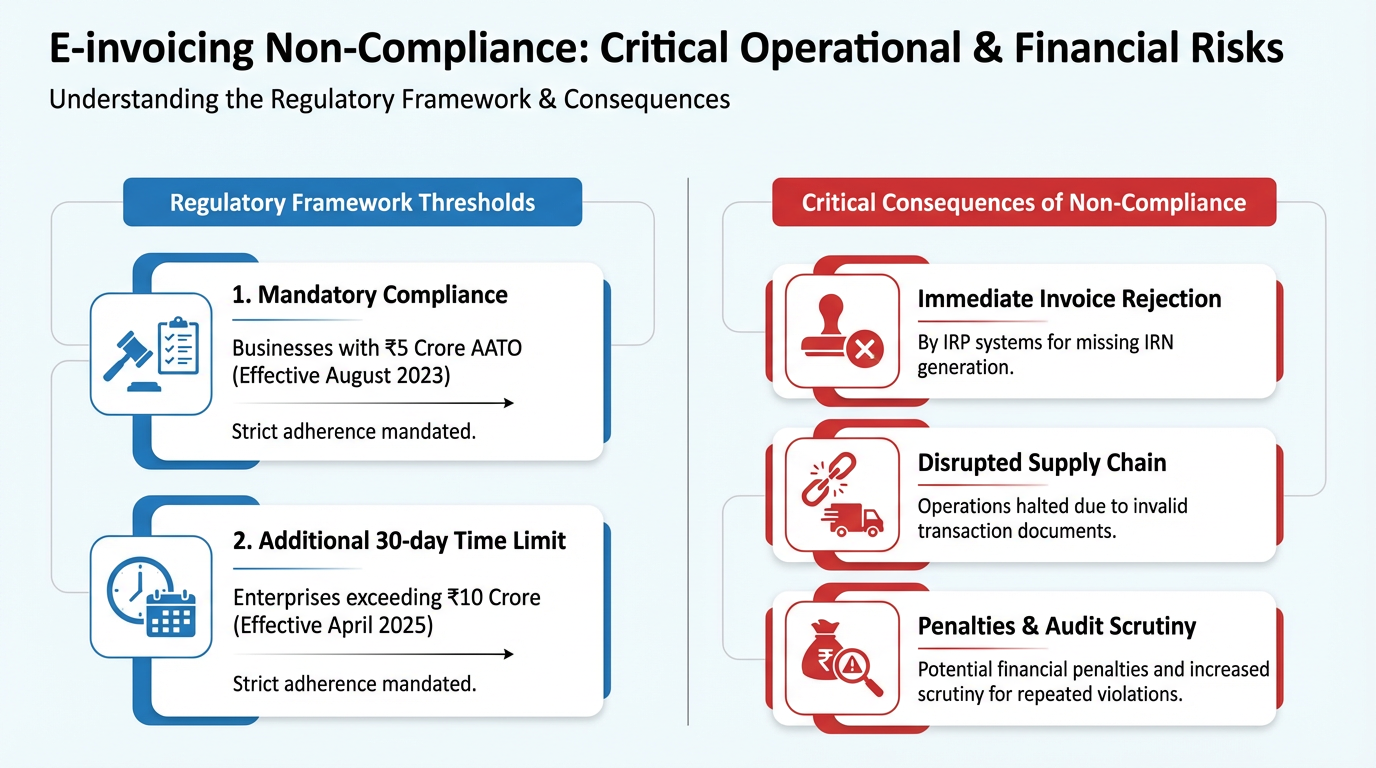

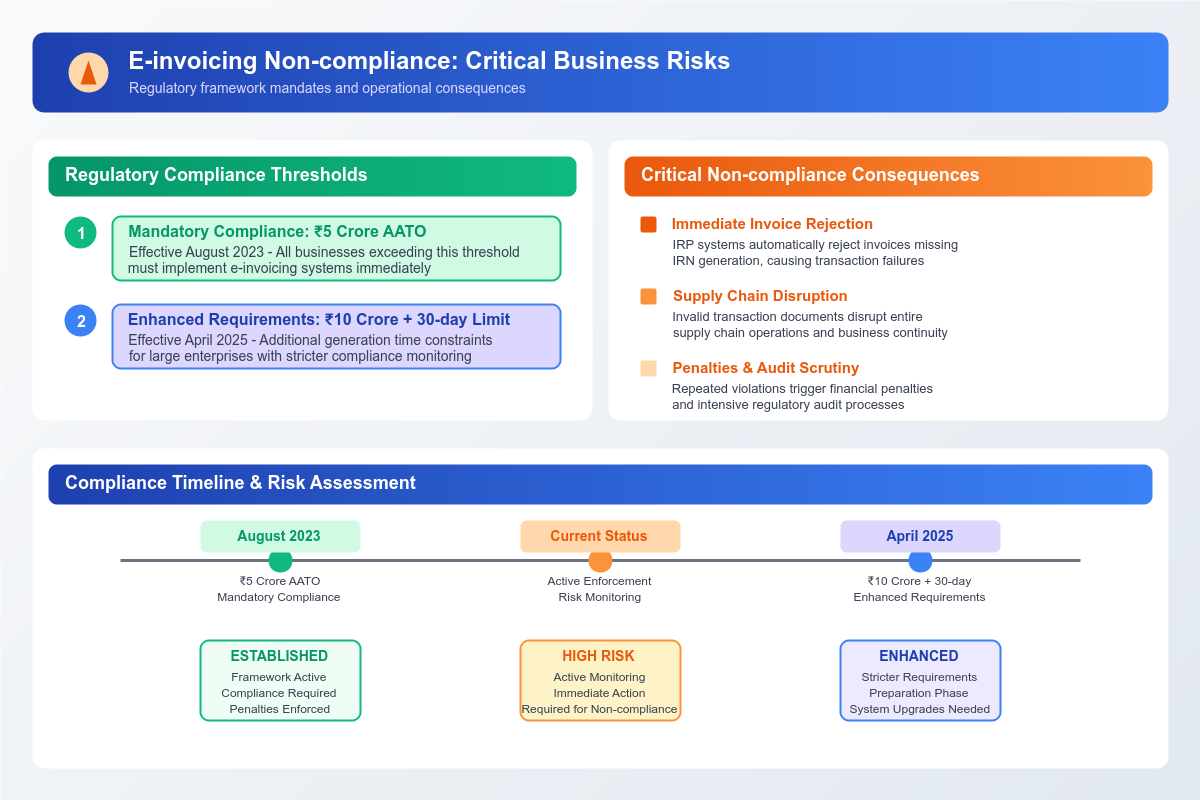

E-Invoicing Non-Compliance Creates Cascading Risks

E-invoicing compliance has become a critical scrutiny parameter. The current mandatory threshold stands at ₹5 crore AATO (since August 2023), with a 30-day generation time limit applying to businesses above ₹10 crore from April 2025. Failure to generate an IRN within the prescribed timelines results in invoice rejection by IRP systems.

| E-Invoice Compliance Issue | Consequence |

|---|---|

| Non-generation of IRN | Invoice treated as "non-issue"; 100% tax penalty or ₹10,000 per invoice |

| IRN generation beyond 30 days | Automatic rejection by IRP |

| Excessive cancellation rates | Scrutiny for potential manipulation |

| Invalid GSTIN in e-invoice | ITC denial to recipient |

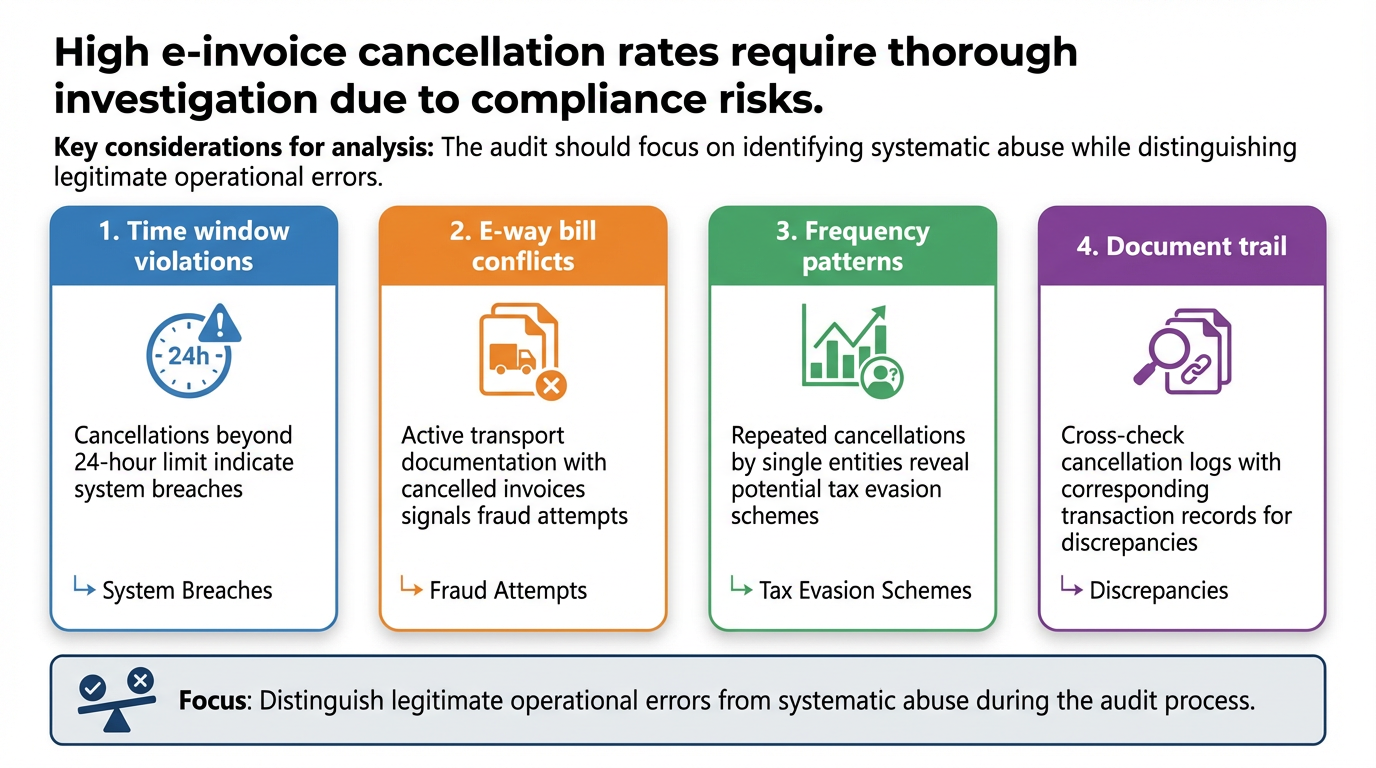

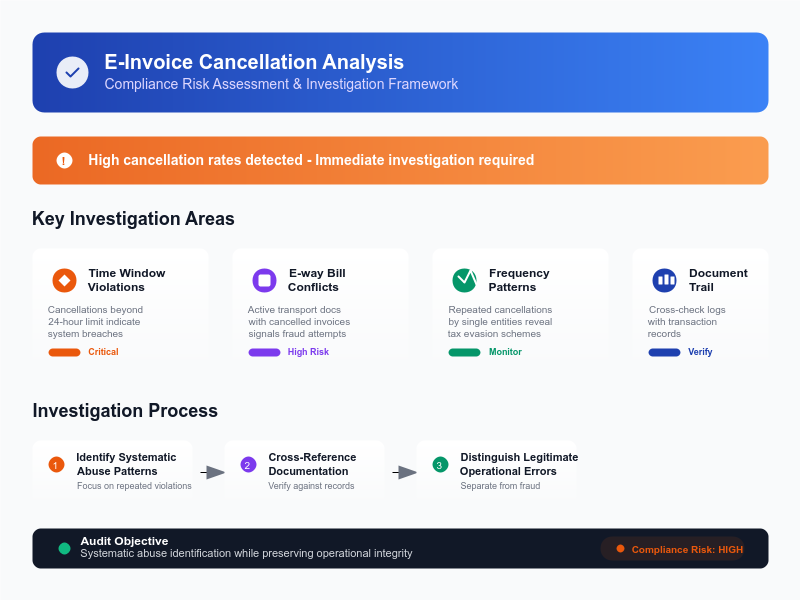

High e-invoice cancellation rates trigger investigation. Since cancellation is permitted only within 24 hours and prohibited when e-way bills are active, patterns of frequent cancellations suggest potential invoice manipulation.

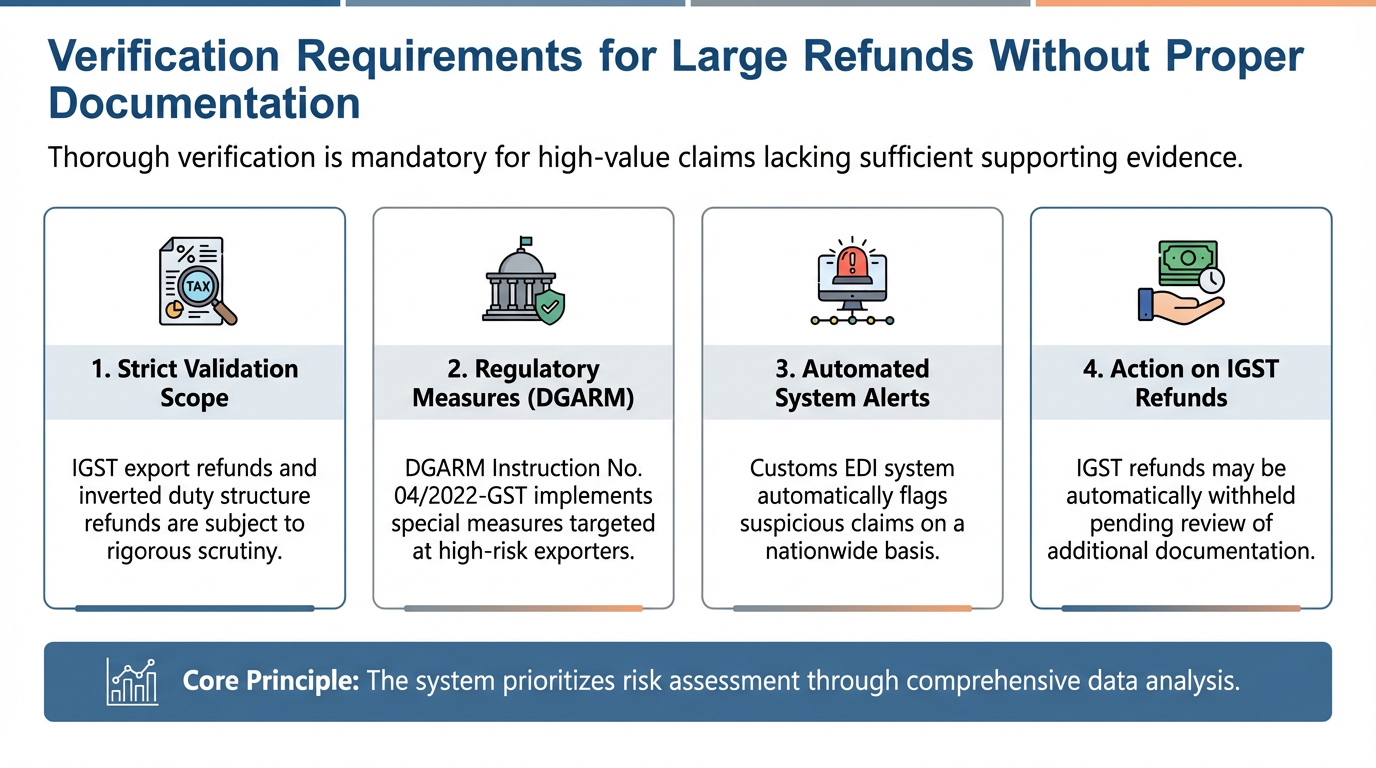

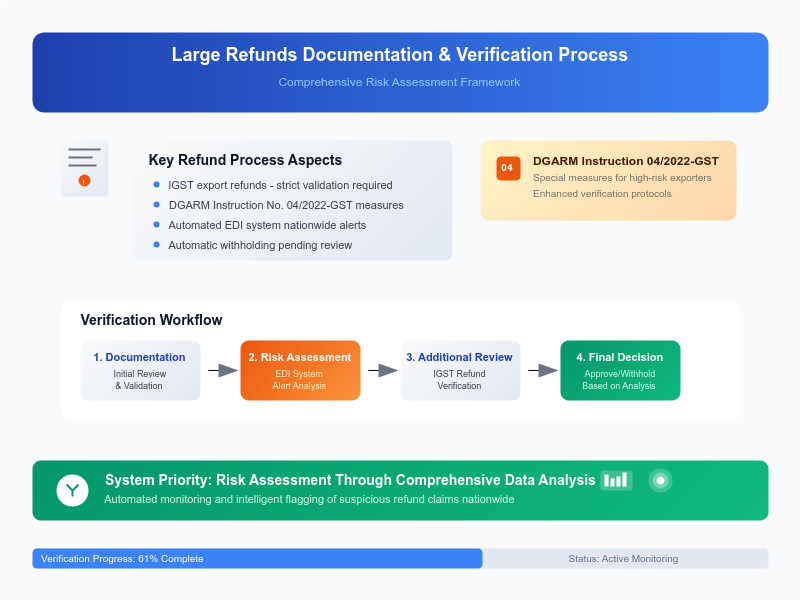

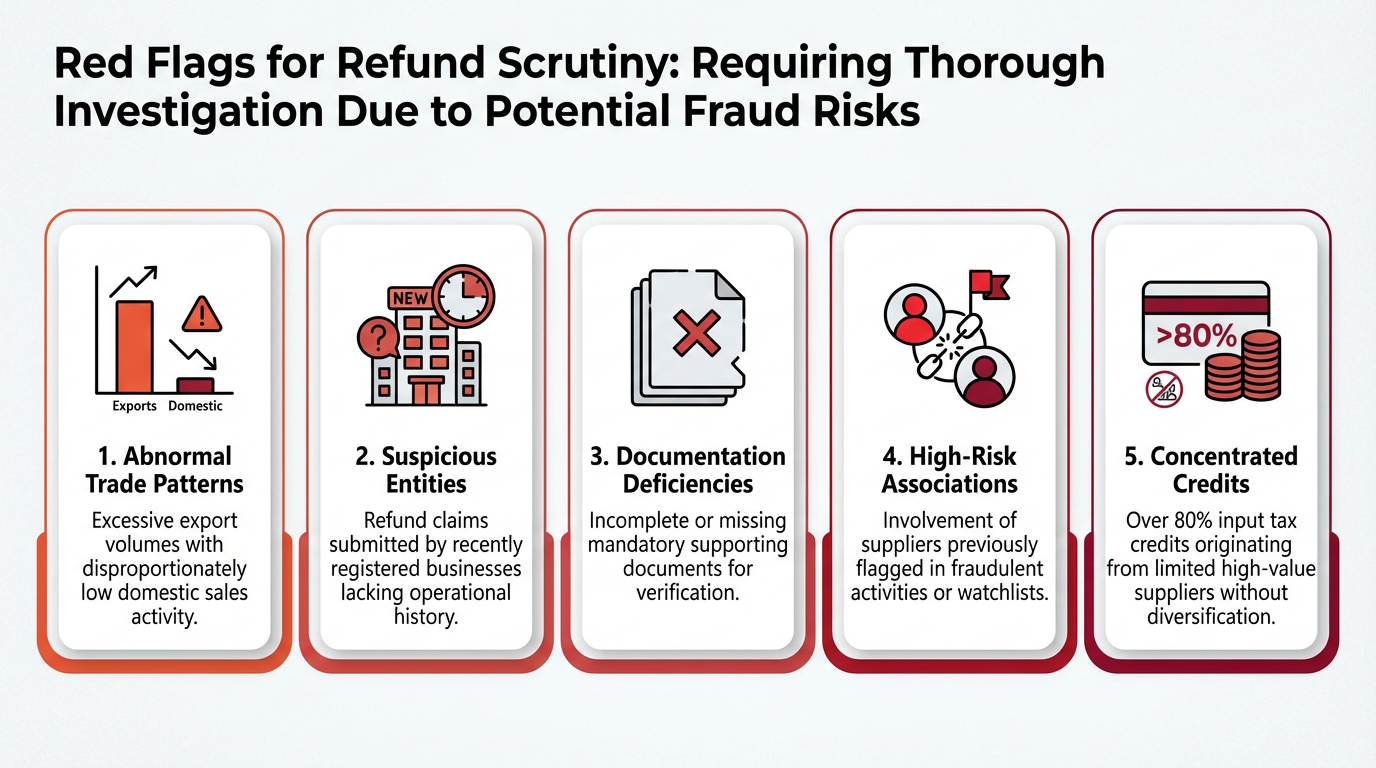

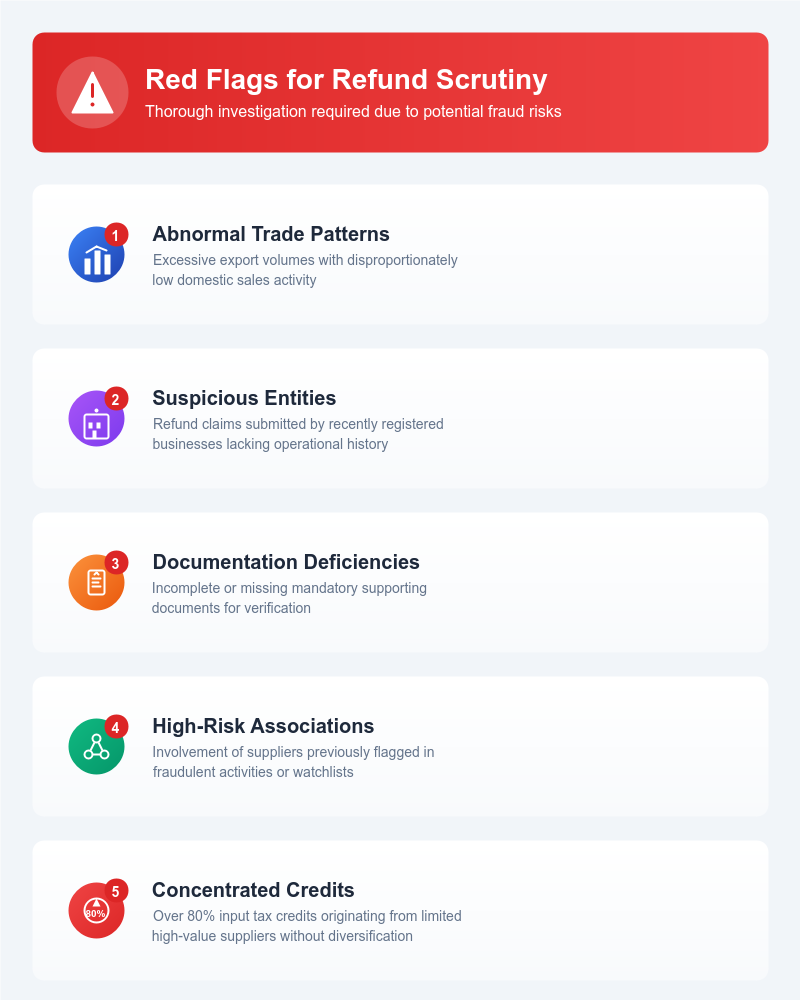

Large Refunds Without Documentation Invite Detailed Scrutiny

Refund claims, particularly IGST export refunds and inverted duty structure refunds, undergo stringent verification. DGARM's Instruction No. 04/2022-GST specifically targets "risky exporters" identified through data analysis, placing all-India alerts on the Customs EDI system to automatically withhold IGST refunds.

Red flags for refund scrutiny include:

- High export volumes with minimal domestic sales

- Refund claims from newly registered entities

- Missing or incomplete supporting documentation

- Suppliers in the transaction chain flagged as risky

- ITC concentration from few high-value suppliers

New Automated Detection Mechanisms Deployed in 2024-25

The GST authorities have implemented several advanced detection systems that generate automated alerts:

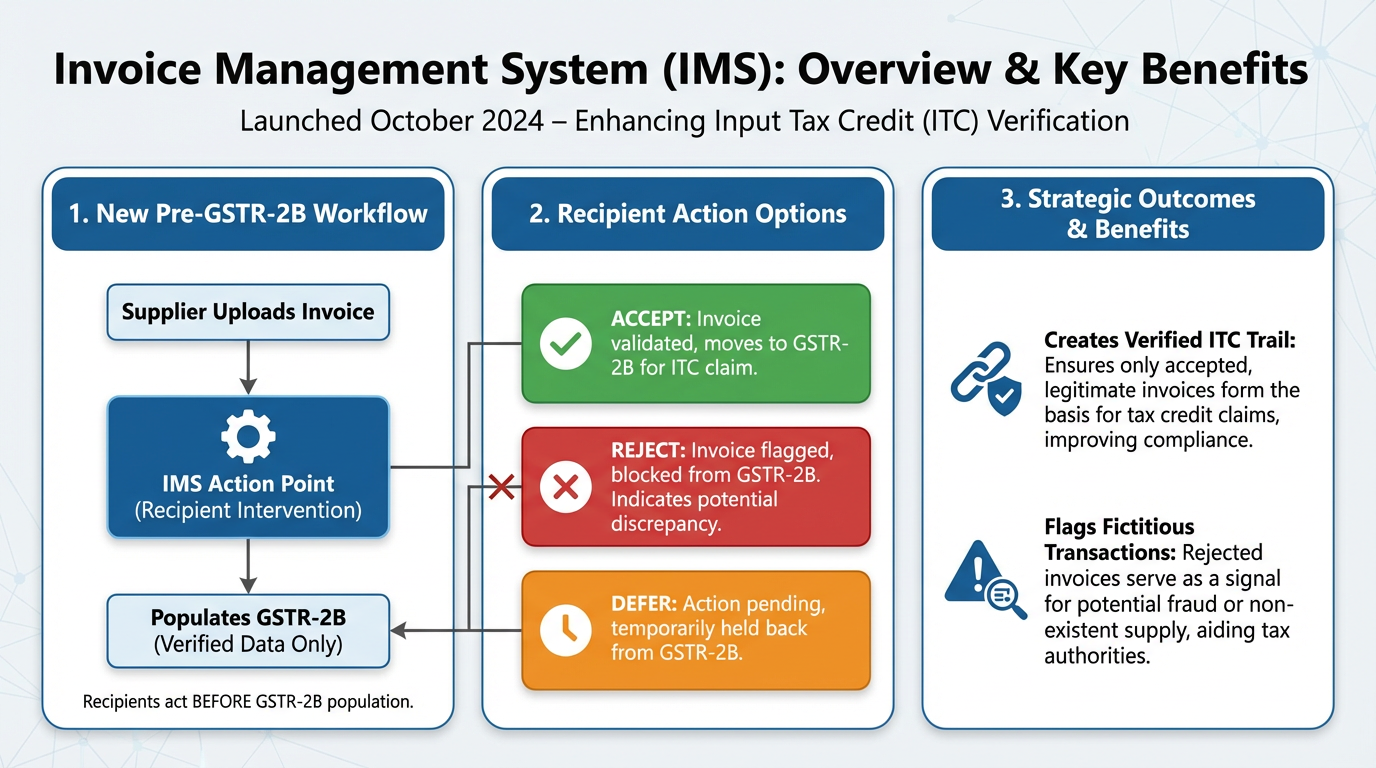

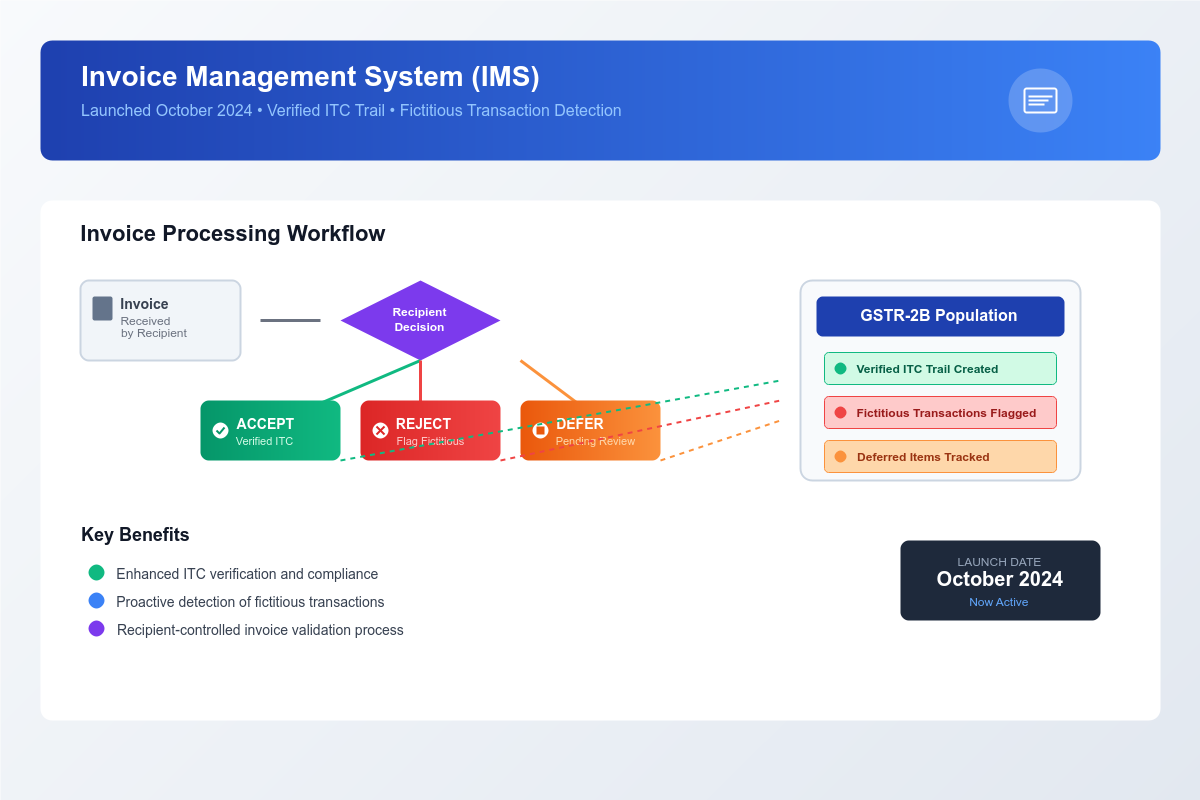

Invoice Management System (IMS), launched October 2024, allows recipients to accept, reject, or defer invoices before they populate GSTR-2B. This creates a verified ITC trail and flags invoices that recipients refuse to accept—potentially indicating fictitious transactions.

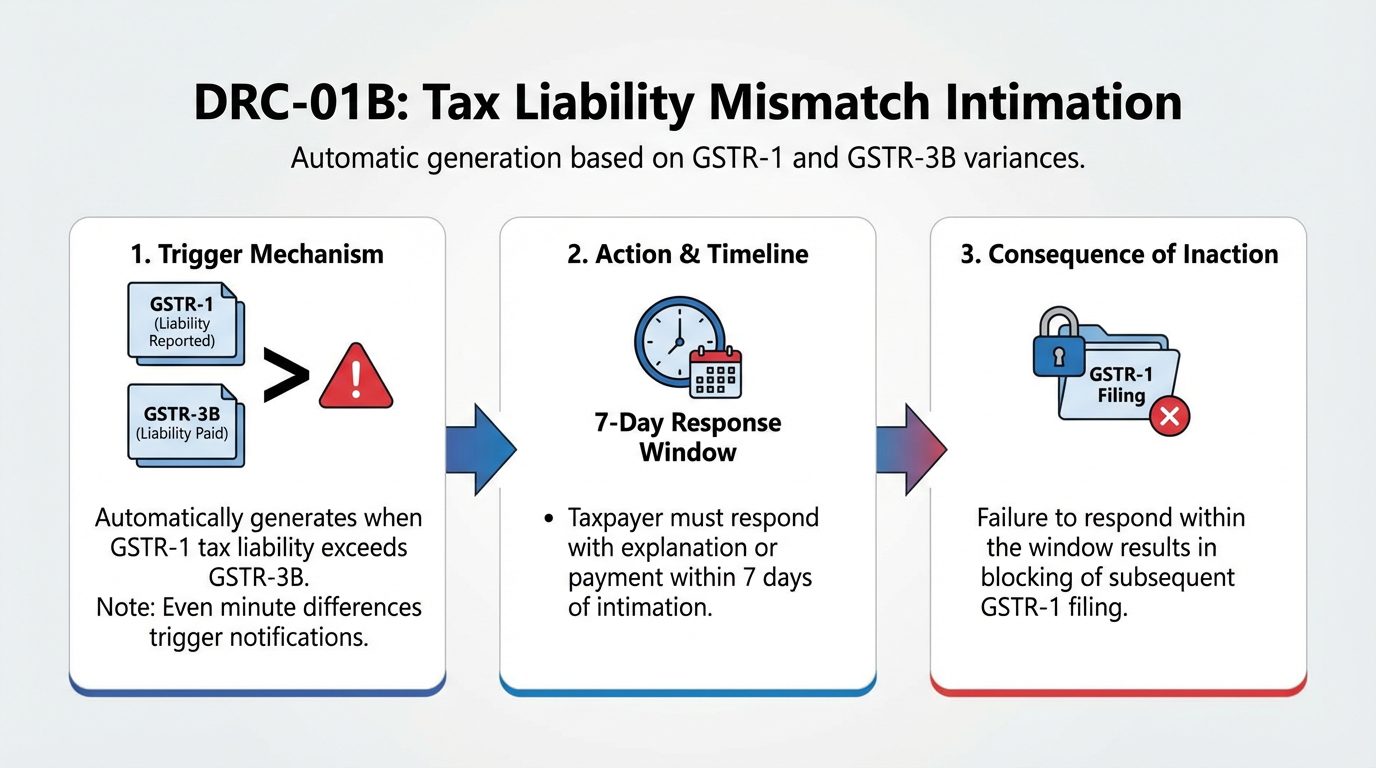

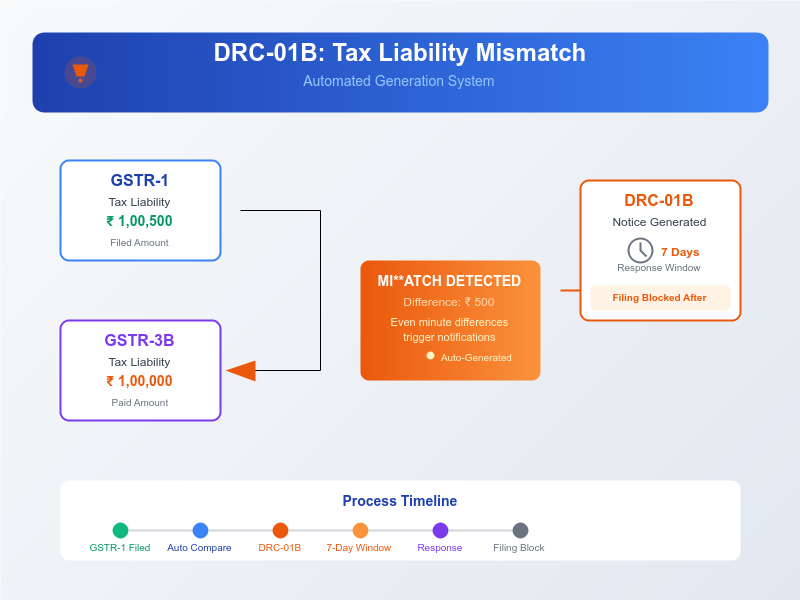

DRC-01B (Tax Liability Mismatch) automatically generates when GSTR-1 tax liability exceeds GSTR-3B. Even minute differences trigger notifications, with a 7-day response window before GSTR-1 filing gets blocked.

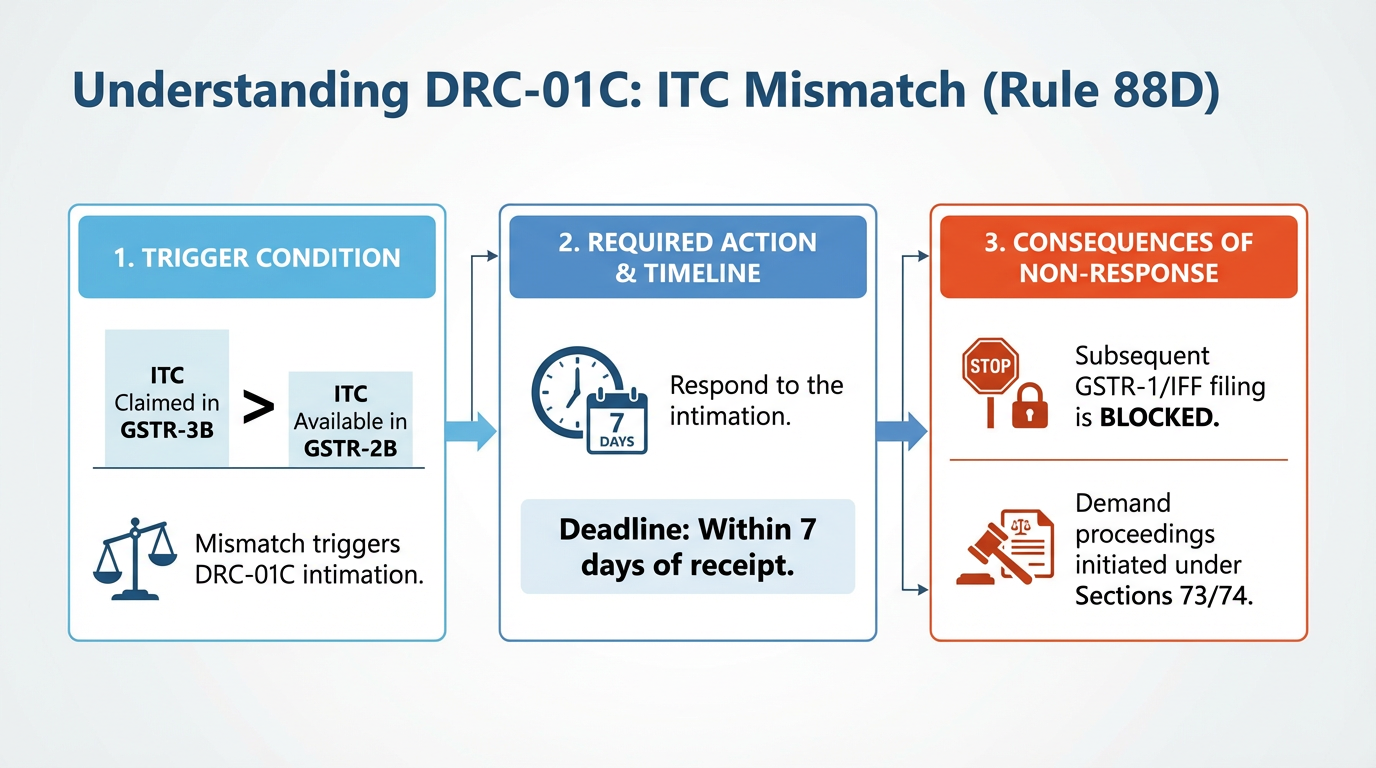

DRC-01C (ITC Mismatch) under Rule 88D triggers when GSTR-3B ITC claims exceed GSTR-2B availability. Non-response within 7 days blocks subsequent GSTR-1/IFF filing and initiates demand proceedings under Sections 73/74.

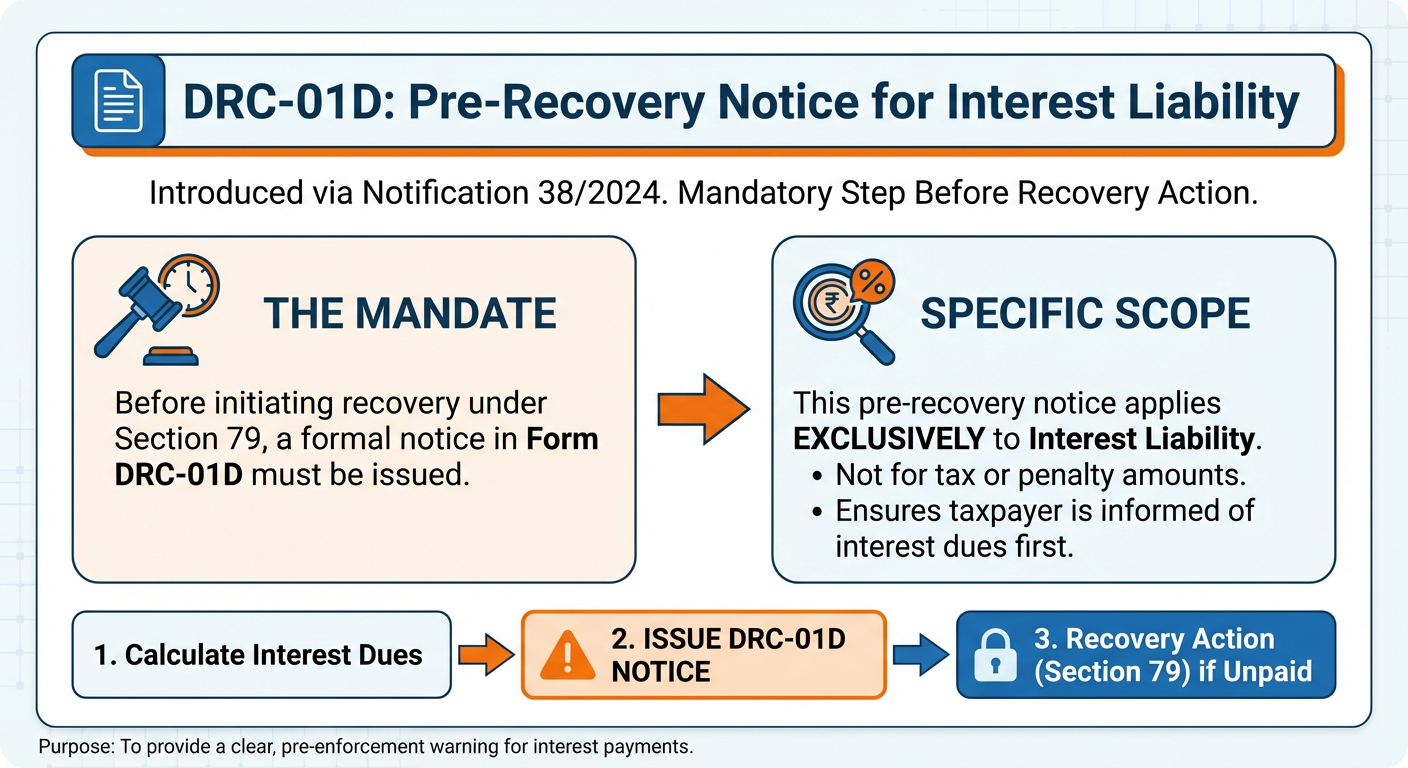

DRC-01D, introduced via Notification 38/2024, mandates pre-recovery notices specifically for interest liability before recovery under Section 79.

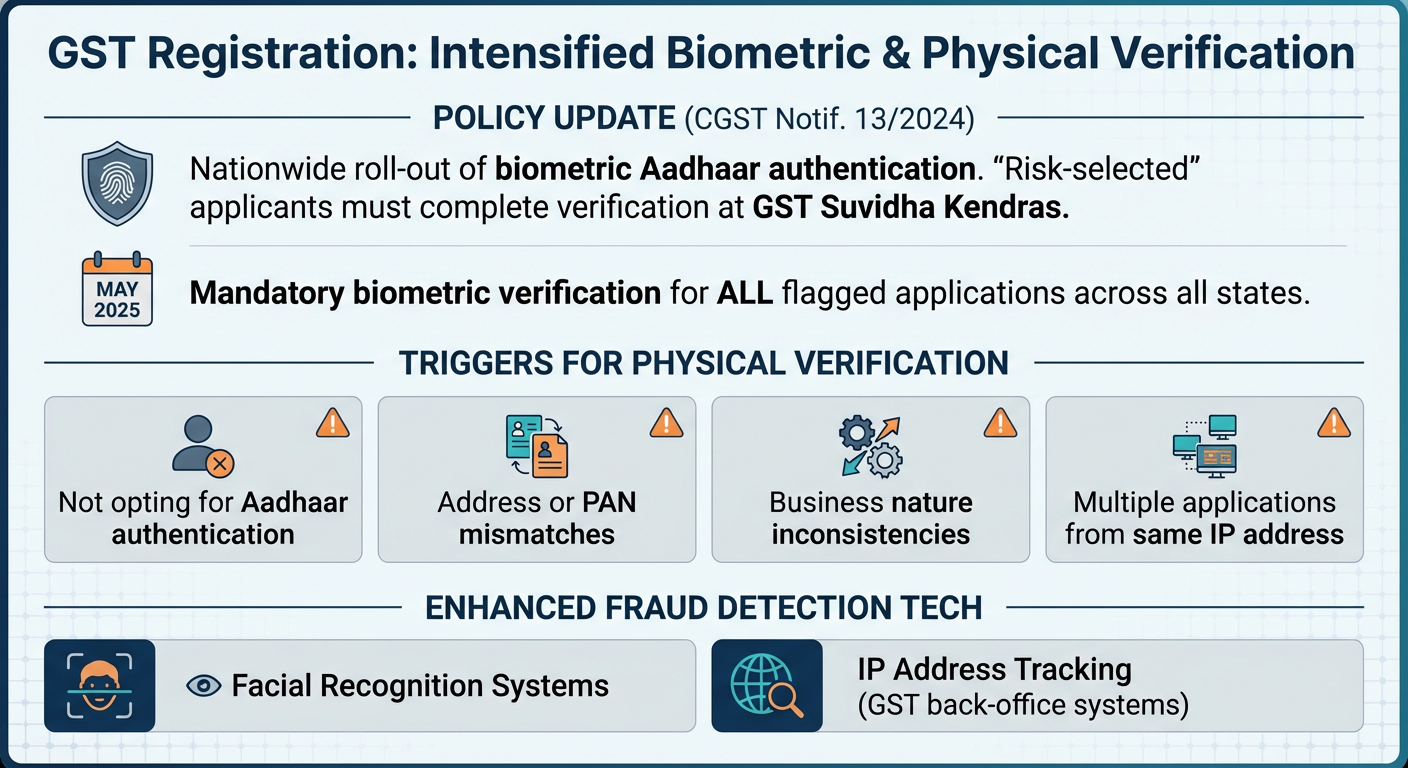

Biometric Authentication and Physical Verification Intensified

Nationwide biometric Aadhaar authentication for GST registration, extended through CGST Notification 13/2024, requires risk-selected applicants to complete verification at GST Suvidha Kendras. By May 2025, all states will implement mandatory biometric verification for flagged applications.

Physical verification triggers include applicants not opting for Aadhaar authentication, address or PAN mismatches, business nature inconsistencies, and multiple registration applications from same IP addresses. The authorities now use facial recognition systems and IP address tracking from GST back-office systems to detect fraudulent registration attempts.

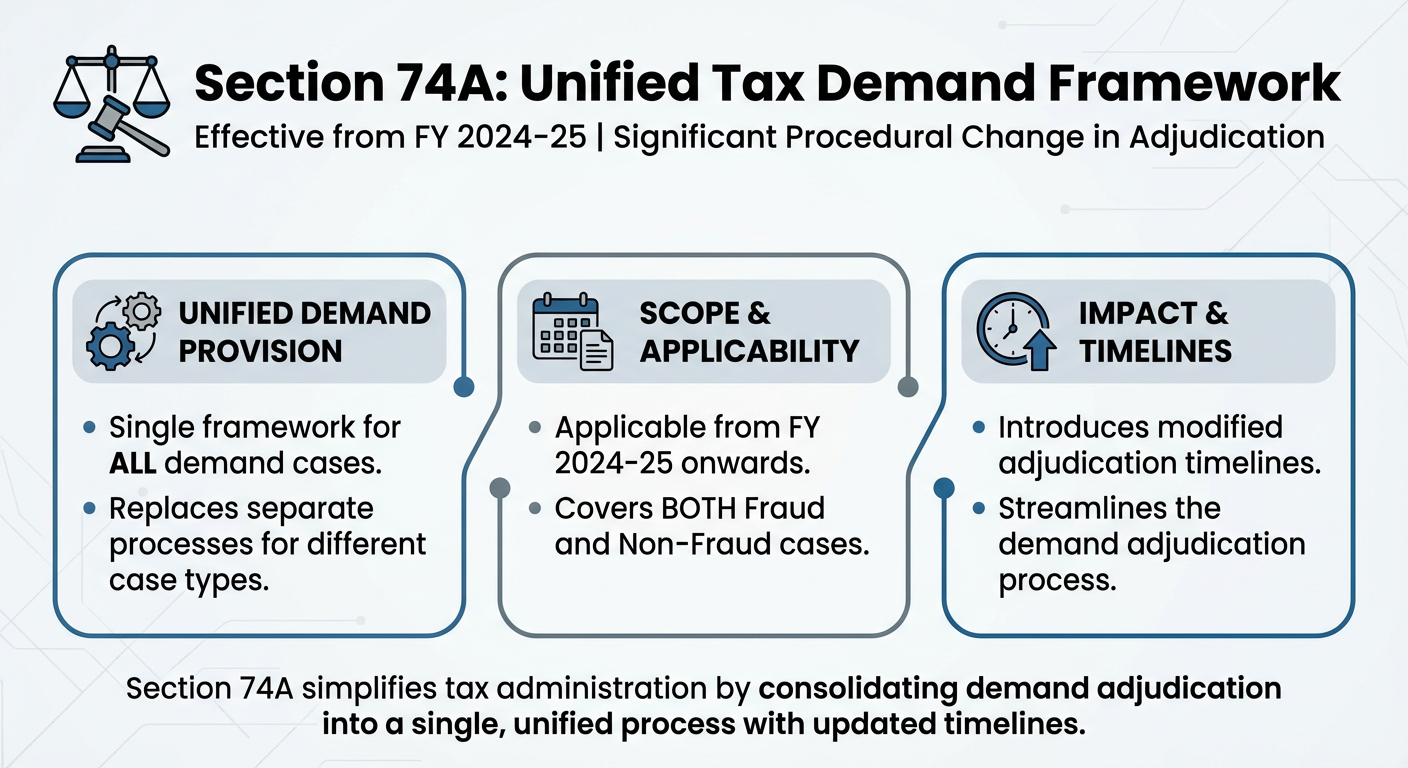

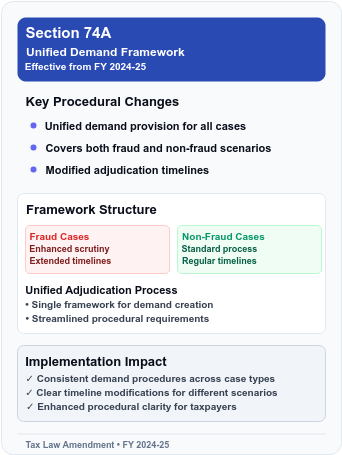

Section 74A Introduces a Unified Demand Framework from FY 2024-25

A significant procedural change affects how tax demands will be adjudicated. Section 74A, applicable from FY 2024-25 onwards, creates a unified demand provision covering both fraud and non-fraud cases with modified timelines:

| Parameter | Section 73/74 (Up to FY 2023-24) | Section 74A (FY 2024-25 onwards) |

|---|---|---|

| SCN time limit | 3 years (non-fraud) / 5 years (fraud) | 42 months |

| Order deadline | Respective return due dates | 12 months from SCN (Six month extension. Total 18 months) |

| Minimum threshold | None | ₹1,000 (no notice below) |

Penalty structures under Section 74A vary based on payment timing—from no penalty for pre-SCN payment in non-fraud cases to 100% penalty for fraud cases remaining unpaid beyond 60 days of order.

Additional Red Flags Identified Through 2024-25 Enforcement Patterns

Beyond the core triggers, authorities focus on several emerging red flags:

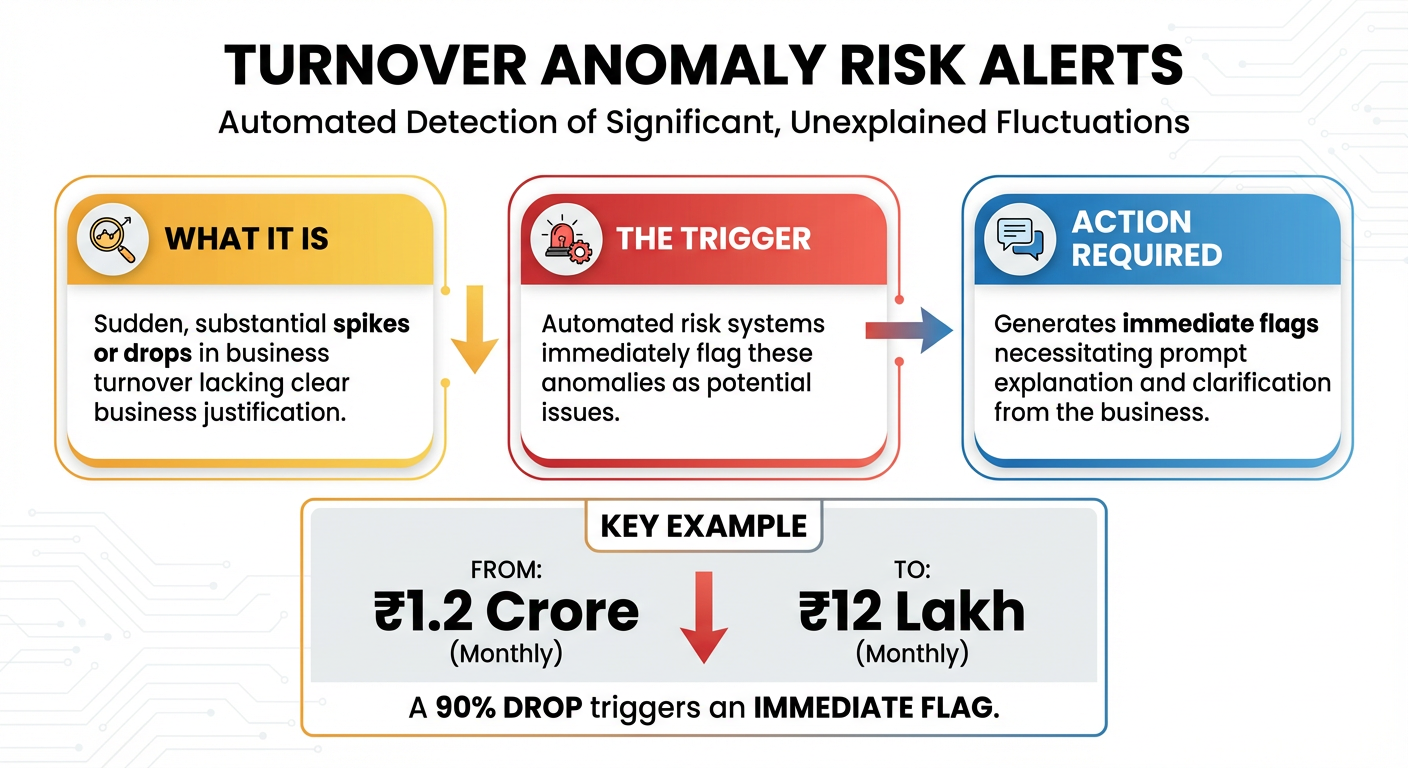

Turnover anomalies such as sudden spikes or drops without business justification trigger automated risk alerts. A drop from ₹1.2 crore to ₹12 lakh monthly turnover, for instance, generates immediate flags requiring clarification.

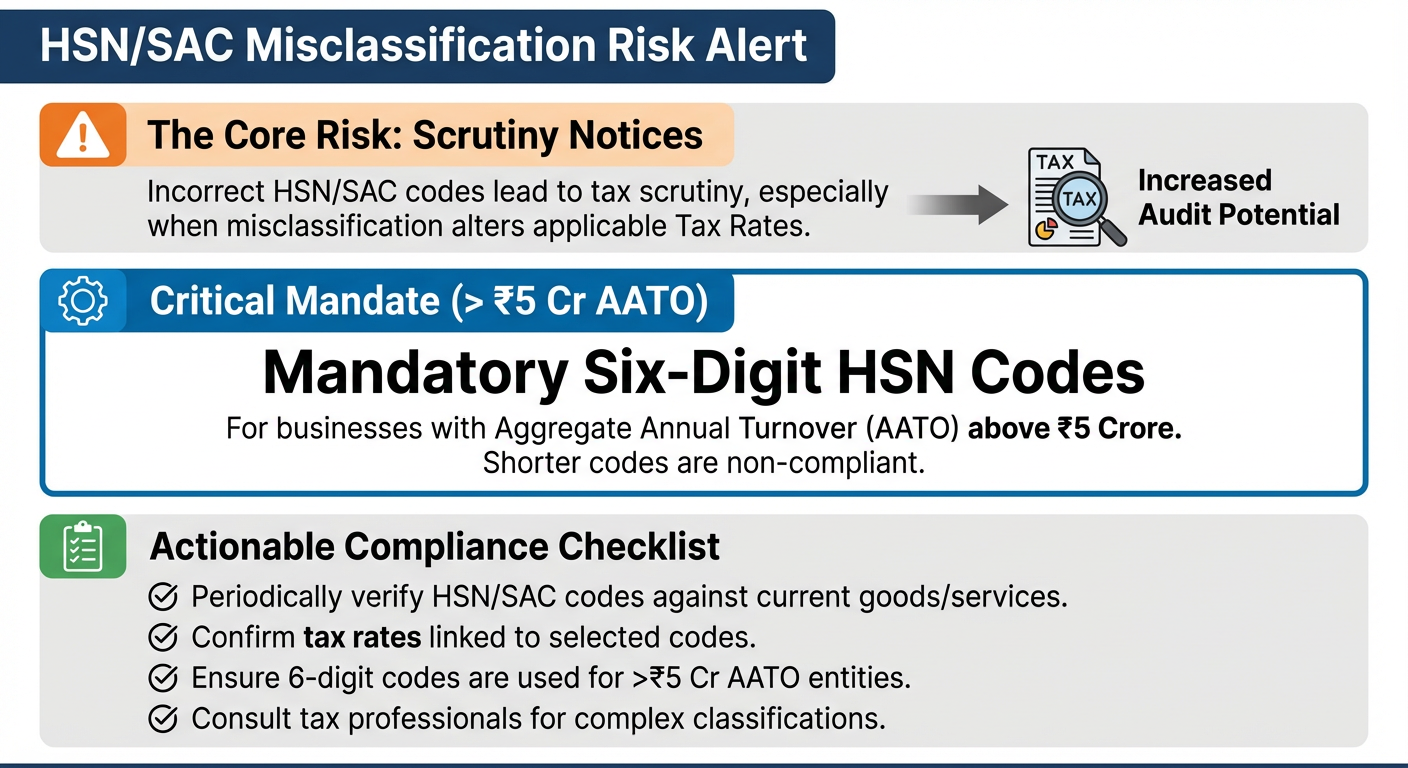

HSN/SAC code misclassification results in scrutiny notices, particularly where misclassification affects tax rates. Six-digit HSN codes are mandatory for businesses above ₹5 crore AATO.

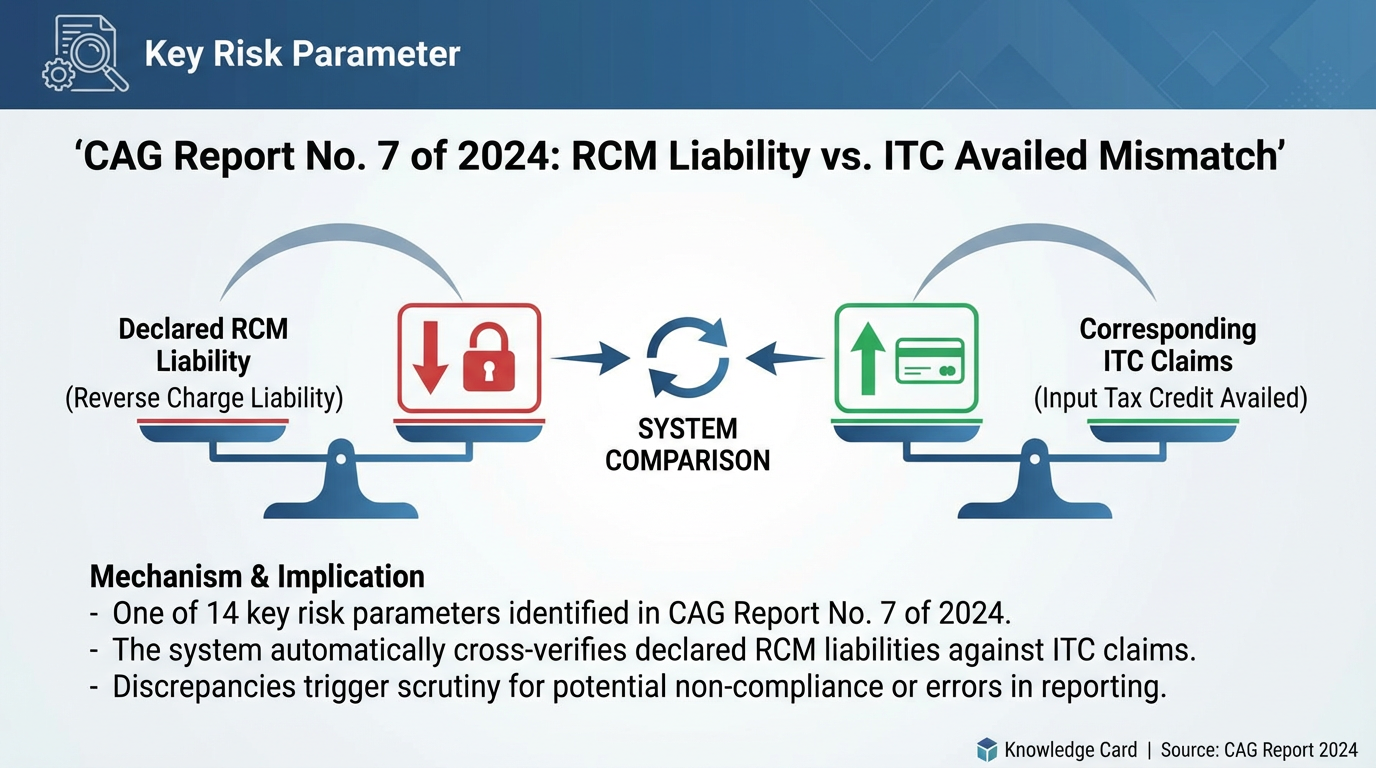

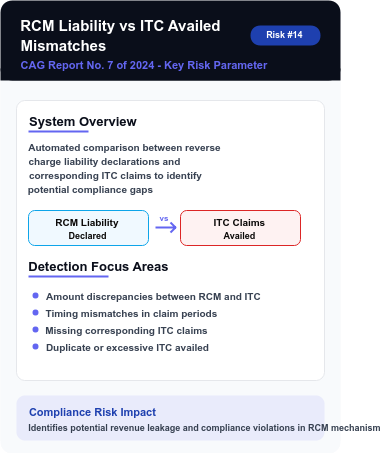

RCM liability versus ITC availed mismatches feature in the 14 key risk parameters identified in CAG Report No. 7 of 2024. The system compares reverse charge liability declared with corresponding ITC claims.

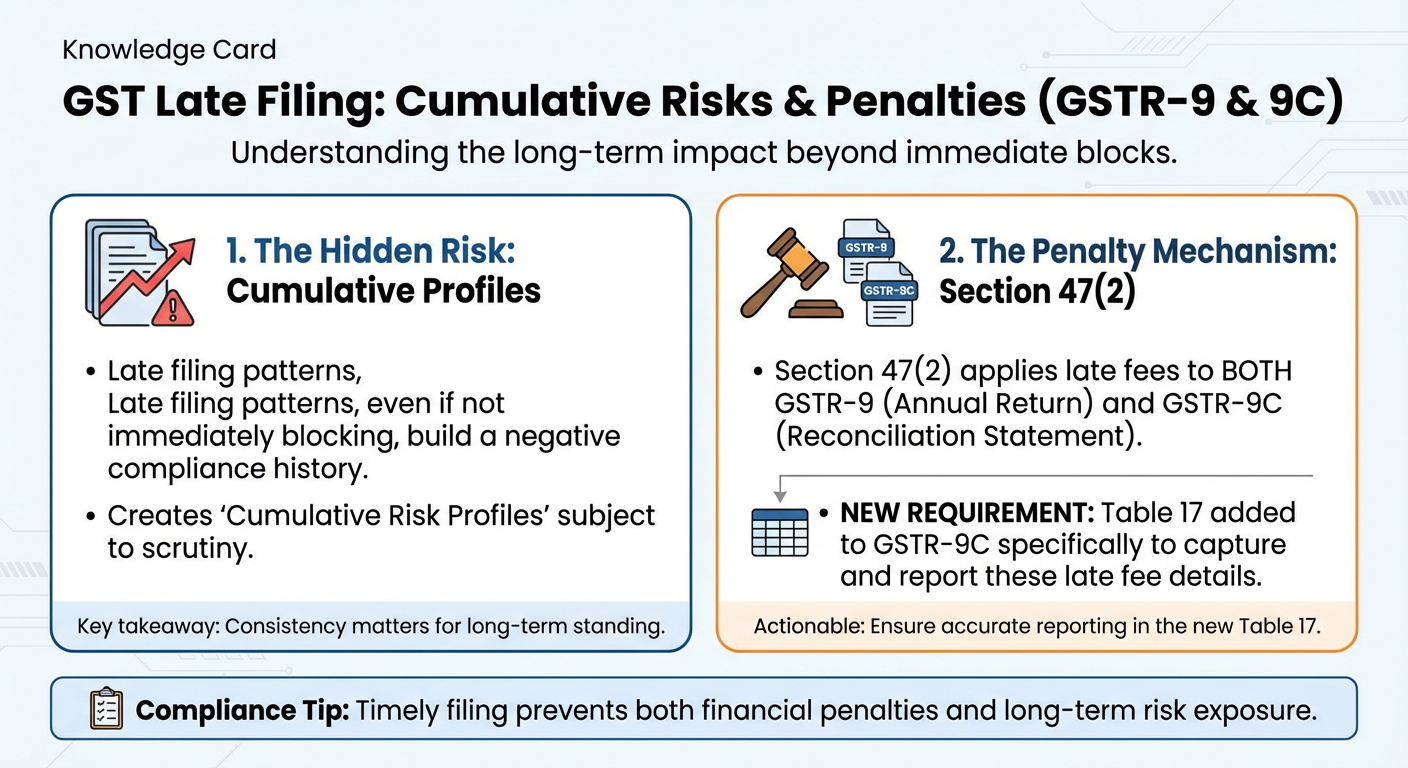

Late filing patterns, while not immediately blocking, create cumulative risk profiles. Section 47(2) applies late fees to both GSTR-9 and GSTR-9C, with a new Table 17 in GSTR-9C specifically capturing late fee details.

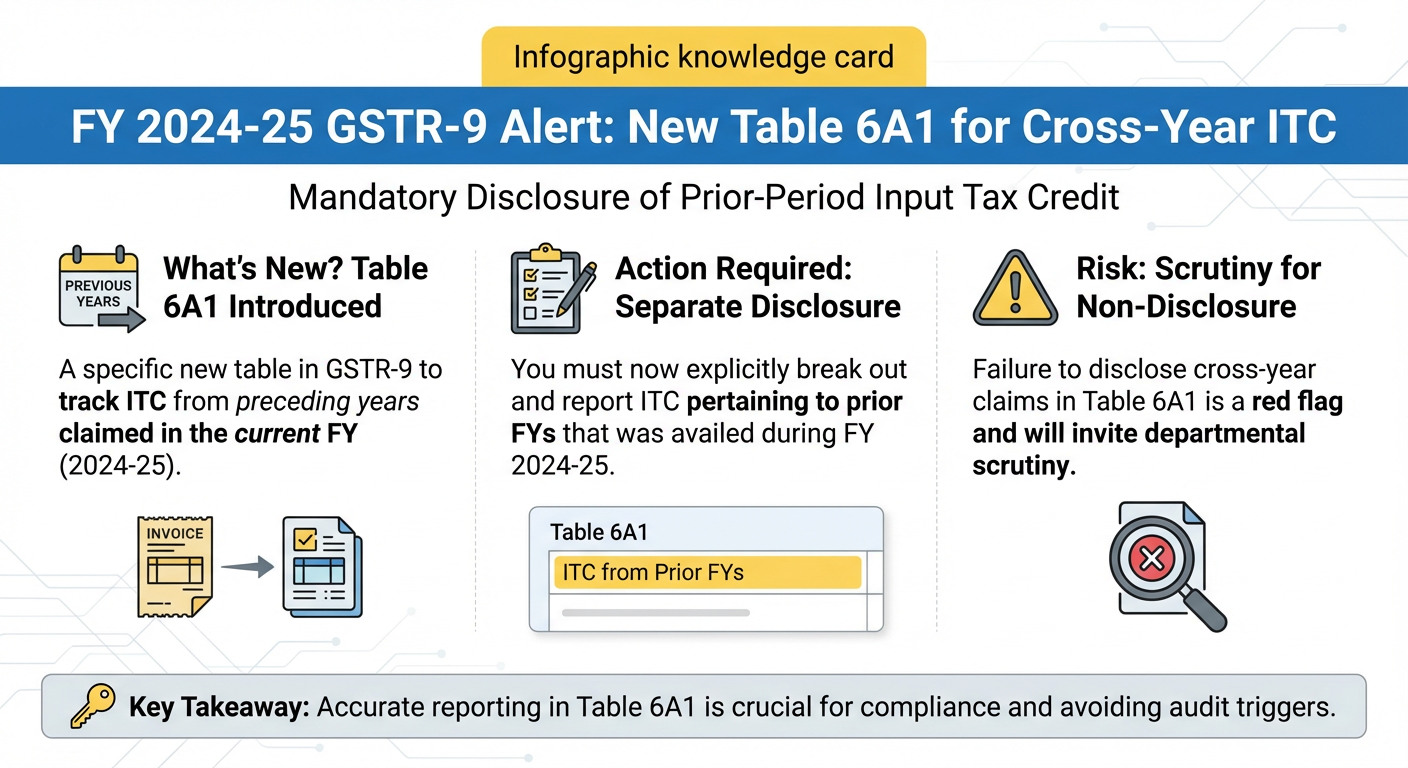

Cross-year ITC claims require disclosure in the new Table 6A1 of GSTR-9 for FY 2024-25, tracking ITC of preceding years claimed in the current year. Undisclosed cross-year claims invite scrutiny.

Amnesty Scheme Provides Relief for Historical Demands

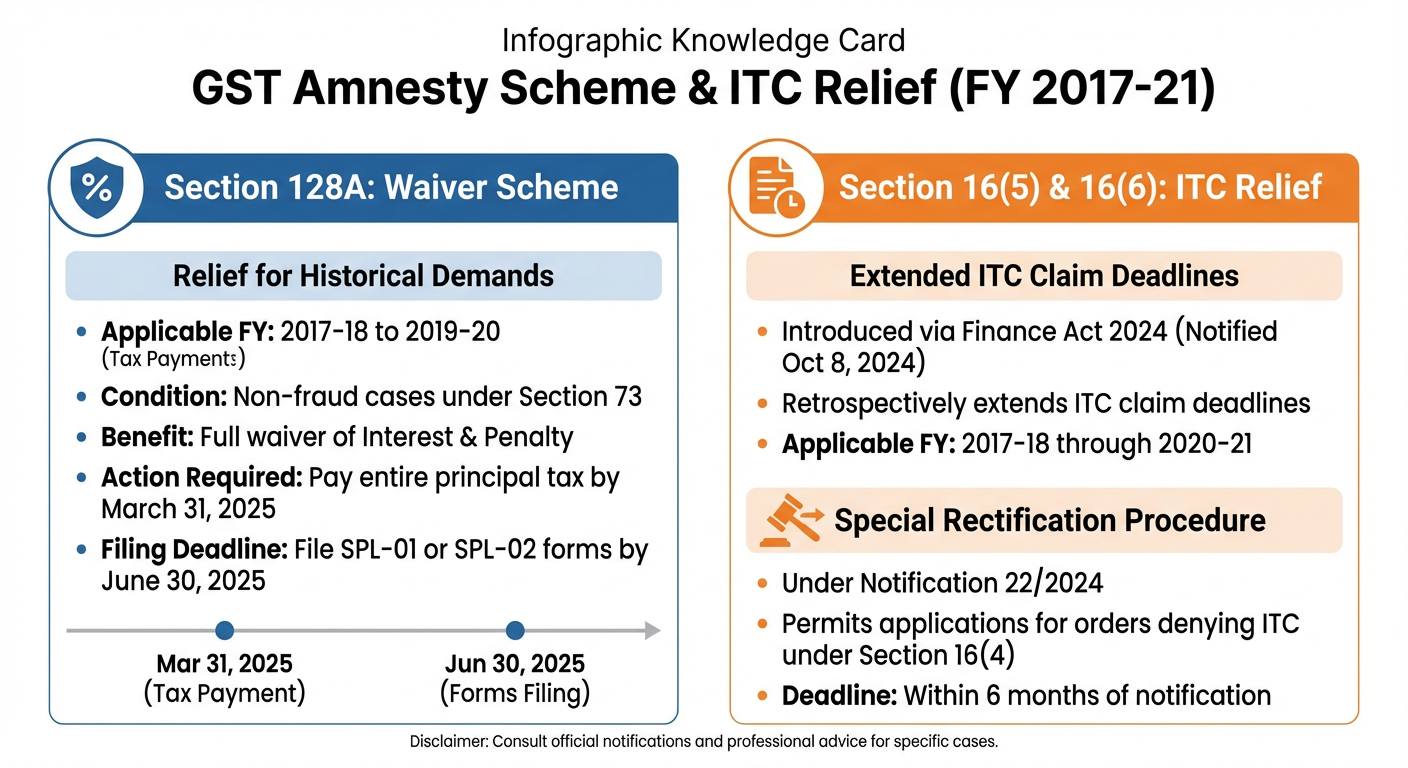

Section 128A offers a significant compliance opportunity—full waiver of interest and penalty for tax demands from FY 2017-18 to 2019-20 under Section 73 (non-fraud cases). Taxpayers must pay the entire principal tax by March 31, 2025 and file SPL-01 or SPL-02 forms by June 30, 2025.

Additionally, Sections 16(5) and 16(6), introduced through Finance Act 2024 and notified October 8, 2024, retrospectively extend ITC claim deadlines for FY 2017-18 through 2020-21. A special rectification procedure under Notification 22/2024 permits applications within 6 months for orders that denied ITC under Section 16(4).

Comprehensive Red Flag Checklist for 2025 Compliance

The following table consolidates all major GST red flags with their legal provisions and consequences:

| # | Red Flag | Legal Provision | Consequence |

|---|---|---|---|

| 1 | GSTR-1 vs GSTR-3B tax liability mismatch | Rule 88C, Section 37(3) | DRC-01B notice; GSTR-1 blocking |

| 2 | ITC claimed exceeding GSTR-2B | Rule 88D, Rule 36(4) | DRC-01C notice; ITC reversal |

| 3 | ITC from non-compliant suppliers | Section 16(2)(aa), Rule 37A | ITC denial and reversal |

| 4 | ITC utilization above 99% (turnover >₹50L) | Rule 86B | Cash payment mandate; scrutiny |

| 5 | ITC utilization above 95% | DGARM risk parameter | Fake invoice investigation |

| 6 | E-way bill vs turnover mismatch | E-Way Bill Rules | ASMT-10 scrutiny notice |

| 7 | Nil returns with active e-way bills | Section 61, Rule 99 | Immediate risk profiling |

| 8 | Blocked credit claims | Section 17(5) | ITC reversal with interest |

| 9 | E-invoice non-generation/late generation | Rule 48(5), Notification 10/2023 | ₹10,000 penalty per invoice |

| 10 | High e-invoice cancellation rate | E-Invoice Rules | Investigation for manipulation |

| 11 | Purchases from risky suppliers | DGARM parameters | ITC blocking under Rule 86A |

| 12 | Circular trading patterns | Section 132 | Criminal prosecution |

| 13 | Multiple GSTINs at same address | Anti-fraud parameters | Registration cancellation |

| 14 | Large refunds without documentation | Section 54 | Refund withholding |

| 15 | High exports with minimal domestic sales | Instruction 04/2022-GST | Risky exporter classification |

| 16 | Sudden turnover spikes or drops | DGARM analytics | ASMT-10 scrutiny notice |

| 17 | Non-filing for 6+ consecutive months | Section 29 | Registration cancellation |

| 18 | Late return filing patterns | Section 47(2) | Late fees; risk profiling |

| 19 | RCM liability vs ITC mismatch | Section 9(3)/(4), Section 16 | Demand notice |

| 20 | HSN/SAC code misclassification | Rule 46 | Rate arbitrage scrutiny |

| 21 | Undisclosed cross-year ITC | GSTR-9 Table 6A1 | Annual return scrutiny |

| 22 | Invoice without goods movement | Section 132(1)(b) | Arrest; prosecution |

| 23 | Common credentials across GSTINs | Biometric verification rules | Registration rejection |

| 24 | Non-response to DRC-01B/01C | Rules 88C/88D | Return filing blocked |

| 25 | IMS invoice rejection by the recipient | IMS parameters | Supplier scrutiny |

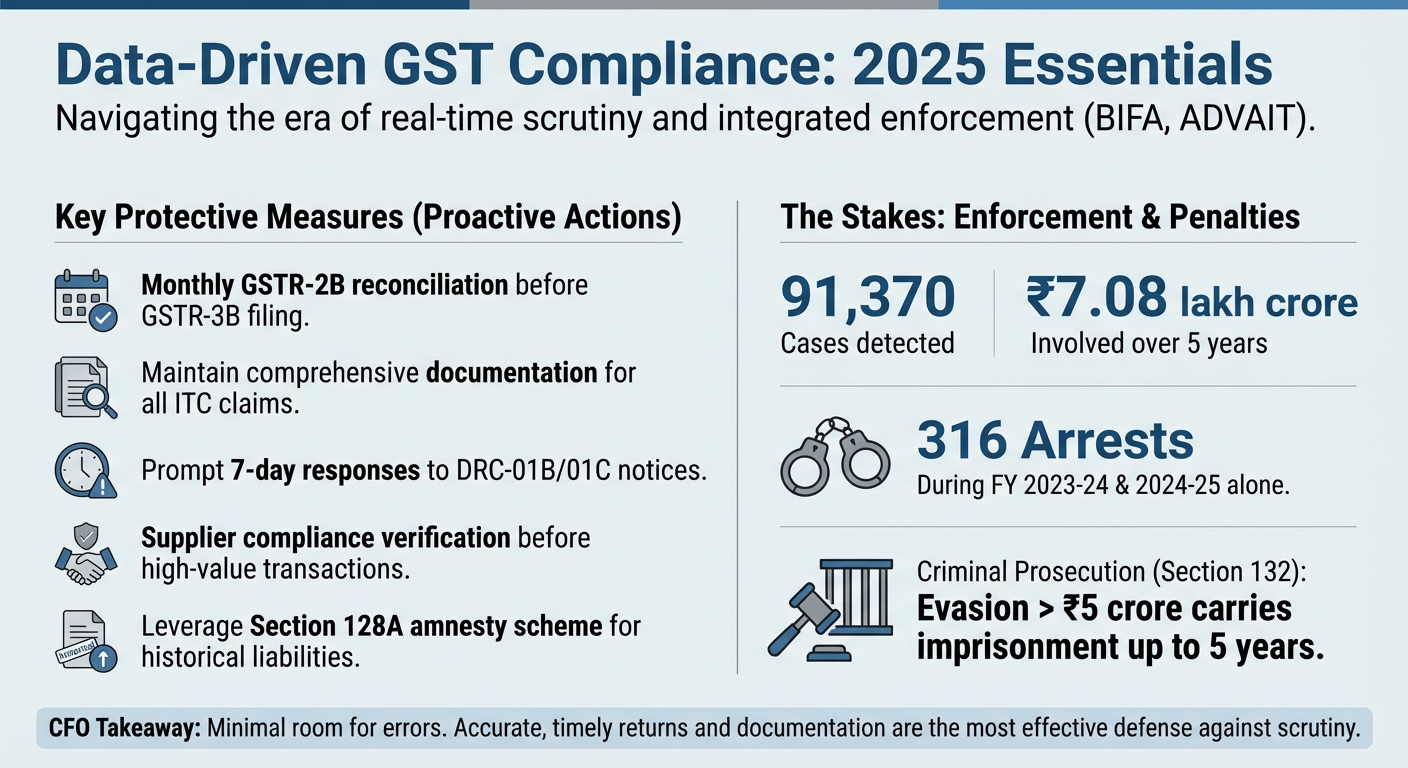

Conclusion: Proactive Compliance Essential in Data-Driven Enforcement Era

The GST compliance landscape in 2025 demands proactive monitoring across multiple dimensions. The integration of BIFA, ADVAIT, and automated return matching has created an environment where authorities can detect discrepancies in near real-time. Key protective measures include monthly GSTR-2B reconciliation before GSTR-3B filing, maintaining comprehensive documentation for all ITC claims, prompt 7-day responses to DRC-01B/01C notices, supplier compliance verification before high-value transactions, and leveraging the Section 128A amnesty scheme for historical liabilities.

The enforcement statistics underscore the stakes—91,370 cases involving ₹7.08 lakh crore detected over five years, with 316 arrests during FY 2023-24 and 2024-25 alone. Criminal prosecution under Section 132 for evasion exceeding ₹5 crore carries imprisonment up to 5 years. CFOs must ensure that the data-driven approach leaves minimal room for errors or deliberate non-compliance, making accurate, timely returns and documentation the most effective defense against scrutiny.

DRC 01 Format | Accounts and Records Under GST | GST Registration Status Check | How to do GST Audit | E invoice Penalty Notification | DRC 01D | GST Penalty Under Section 74

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified