The Supreme Court Ruling Every CFO Must Understand Before It's Too Late

1. Why This Article Could Save Your Company Lakhs

Picture this scenario. Your company receives a GST notice one morning. But instead of covering one financial year, it covers five years at once. Five years of transactions. Five years of Input Tax Credit claims. All bundled into one massive demand.

Until recently, you could have successfully challenged this approach. High Courts across India were consistently ruling that tax authorities cannot club multiple years into a single notice. It seemed like settled law.

Then came November 2025. The Supreme Court changed everything.

If you are a CFO, Finance Director, or anyone responsible for your company's tax strategy, this ruling directly affects how you handle GST disputes going forward. More importantly, it affects how you should be documenting your transactions right now.

This is not just another legal update. This is a fundamental shift in how GST investigations will be conducted against businesses like yours.

2. What Exactly Happened?

A company called Mathur Polymers received a GST demand of Rs. 81.54 lakhs. The tax department alleged that the company had fraudulently claimed Input Tax Credit. But here is what made this case special: instead of issuing separate notices for each financial year, the department issued one consolidated notice covering multiple years.

Mathur Polymers challenged this approach. They argued what many High Courts had already accepted: that the GST law requires separate notices for each financial year, and bundling them together is illegal.

The case went all the way to the Supreme Court. And the Supreme Court sided with the tax department.

The Court ruled that when fraud is alleged, tax authorities are fully entitled to issue a single notice covering multiple financial years. The reasoning was straightforward: fraud does not follow neat annual boundaries. A scheme to claim fake Input Tax Credit might run continuously across several years. To understand the full pattern, investigators need to see the complete picture.

This ruling has immediate and practical consequences for every business in India.

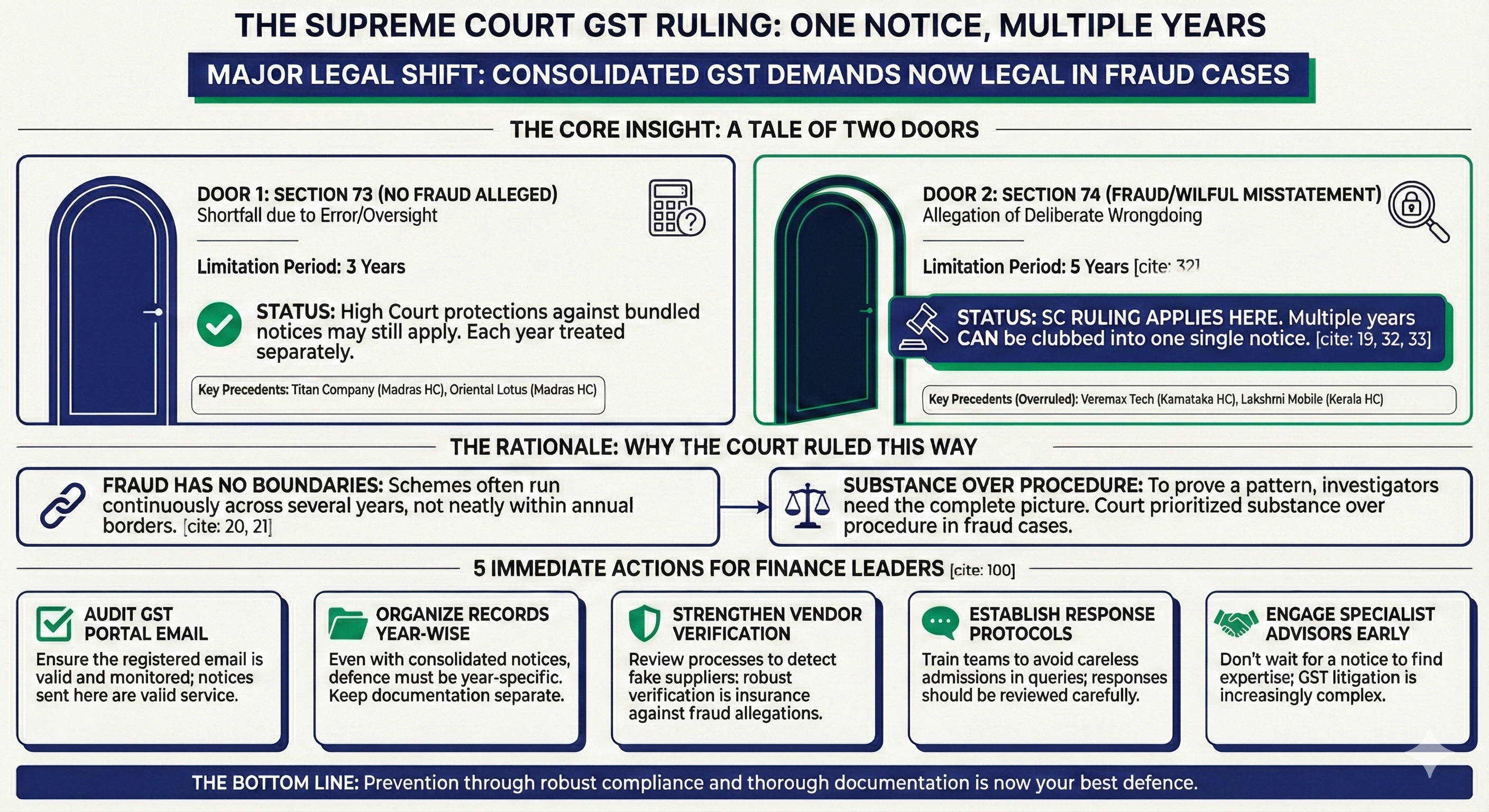

3. Understanding the Two Types of GST Notices

Before we go further, you need to understand a critical distinction that will determine how this ruling affects your company.

GST law has two main sections under which tax demands can be raised. Think of them as two different doors through which the tax department can come after you.

The first door is Section 73. This applies when there is a shortfall in tax payment, but there is no allegation of fraud or deliberate wrongdoing. Perhaps there was a calculation error, a misinterpretation of the law, or an oversight. The limitation period here is three years, and the penalties are relatively moderate.

The second door is Section 74. This applies when the department alleges fraud, wilful misstatement, or suppression of facts. The stakes here are much higher. The limitation period extends to five years, penalties are severe, and now, thanks to the Supreme Court ruling, multiple years can be clubbed into a single notice.

Here is the key takeaway: the Supreme Court's ruling applies specifically to Section 74 cases where fraud is alleged. For Section 73 cases without fraud allegations, the position may still favour taxpayers. Several High Court judgments protecting businesses from bundled notices in non-fraud cases have not been directly overruled.

This distinction is absolutely critical for your defence strategy.

4. What the High Courts Had Been Saying

To appreciate how significant this Supreme Court ruling is, let us look at what High Courts across India have consistently held.

The Karnataka High Court, in a case involving Veremax Technologie Services in 2024, ruled that consolidated notices covering multiple financial years are not permitted under the GST law. The Court examined the relevant provisions and concluded that each financial year must be dealt with separately.

The Madras High Court, in the Titan Company case in 2024, struck down notices that had bunched multiple assessment years together. The Court pointed out that each year has its own three-year limitation period. By clubbing years together, the department was effectively bypassing this legal protection.

The Kerala High Court, in Lakshmi Mobile Accessories in 2025, reached a similar conclusion. The Court held that consolidation violates the time limits specified in the law.

The Bombay High Court, in Milroc Good Earth Developers in 2025, ruled that the statutory scheme requires period-wise assessment and year-wise limitation. Composite notices were therefore without jurisdiction.

As recently as December 2025, the Karnataka High Court in Pramur Homes and Shelters declared consolidated notices "illegal and without jurisdiction."

Business owners and their advisors were understandably optimistic. The trend seemed clear. Then came the Supreme Court judgment that changed the landscape.

5. Why the Supreme Court Disagreed

The Supreme Court's reasoning was rooted in the actual language of the GST law. And this is important for you to understand, because it reveals how courts interpret statutes.

When you read Sections 74(3) and 74(4) of the CGST Act, you will notice something interesting. These provisions do not use the phrase "financial year." Instead, they refer to "any period" and "such periods."

The Supreme Court found this choice of words significant. According to the Court, the legislature deliberately used broader language to allow notices covering periods longer than a single financial year, particularly in fraud cases.

The practical rationale is easy to understand. Imagine a company that has been systematically claiming Input Tax Credit from fake suppliers for four years. The fraud is a continuous pattern. To prove this pattern, investigators need to analyse transactions across all four years together. Forcing them to conduct four separate investigations and four separate proceedings would be inefficient and might even let sophisticated fraudsters escape through procedural gaps.

The Supreme Court essentially said: when fraud is involved, substance matters more than procedure. The tax authorities should be able to see the full picture.

6. The Good News: Your Company May Still Be Protected

Here is where things get nuanced, and where smart financial planning can make a real difference.

The Supreme Court's ruling was specifically about fraud cases under Section 74. But what if your company receives a consolidated notice under Section 73, where no fraud is alleged? What if the department is simply claiming you made errors in your tax calculations?

In such cases, the High Court judgments that protected taxpayers may still apply. The Supreme Court did not expressly overrule these precedents for non-fraud situations.

Consider the Titan Company judgment from the Madras High Court. That case dealt with Section 73 proceedings where there was no fraud allegation. The Court struck down the bunched notices because each year had exceeded its individual three-year limitation. This reasoning is different from fraud cases and may still hold.

Similarly, the Oriental Lotus Hotel Supplies case from the Madras High Court held that each financial year is a distinct unit with its own limitation period. For routine assessments without fraud, this principle should logically continue to apply.

The practical implication is this: if your company receives a consolidated notice, the first question you and your advisors must ask is whether the notice invokes Section 73 or Section 74. This single distinction could determine your entire defence strategy.

7. The Danger Zone: How "Fraud" Gets Alleged

Now, let me share something that should concern every finance leader. The definition of fraud in GST proceedings is worryingly flexible.

Tax authorities have significant discretion in deciding whether to treat a case as a routine discrepancy under Section 73 or as fraud under Section 74. What starts as a simple query about Input Tax Credit mismatches can escalate into a fraud allegation, sometimes with limited explanation.

And here is the new reality created by the Supreme Court ruling: tax authorities now have an additional incentive to allege fraud. Not only does a Section 74 case give them longer limitation periods and higher penalties, but it also allows them to issue convenient consolidated notices covering multiple years.

This does not mean the department will start making frivolous fraud allegations. Courts will still scrutinise whether the elements of fraud are genuinely made out. But as a finance leader, you need to be aware that the stakes have changed.

When responding to any GST query or investigation, be extremely careful about how your responses are worded. What might seem like a harmless admission about an "oversight" or "error" could later be characterised as suppression of facts, potentially triggering Section 74 treatment.

8. The Complete Picture: All the Key Judgments Organised for You

Let me give you a clear reference list that you can share with your tax advisors and legal team.

8.1 Judgments That May Still Protect You in Non-Fraud Cases

The Titan Company case from the Madras High Court in 2024 struck down bunching under Section 73 where individual three-year limitations had been exceeded. The Oriental Lotus Hotel Supplies case from the Madras High Court in 2025 held that composite notices are void because each financial year is a distinct unit. The R A and Co case from the Madras High Court in 2025 ruled that single notices cannot be issued for multiple periods.

8.2 Judgments Now Overruled for Fraud Cases

The Veremax Technologie Services case from the Karnataka High Court in 2024 had ruled consolidated notices impermissible under Section 74, but this reasoning no longer holds after the Supreme Court verdict. The same applies to Smt. R. Ashaarajaa from the Madras High Court in 2025, Lakshmi Mobile Accessories from the Kerala High Court in 2025, Pramur Homes and Shelters from the Karnataka High Court in December 2025, Tharayil Medicals from the Kerala High Court in 2025, and Albatross Builders from the Karnataka High Court in 2024.

8.3 Judgments Affirmed by the Supreme Court

The Ambika Traders case from the Delhi High Court in 2025 held that consolidated notices are permissible in fraud cases to establish illegal patterns. The Vallabh Textiles case from the Delhi High Court in 2024 reached a similar conclusion. The Britannia Industries case from the Calcutta High Court in 2025 found no specific bar against consolidated notices in the GST law.

Keep this list handy. When you receive a notice, your first step should be to identify which section it falls under and which precedents apply.

9. Five Things Every Finance Leader Must Do Now

Based on this landmark ruling, here are concrete steps you should take immediately.

9.1 Audit Your GST Portal Registration

The Supreme Court also affirmed an important procedural point: notices sent to the email address registered on the GST portal constitute valid service. This applies even if that email belongs to your CA or tax consultant rather than someone in your company.

Check what email address is registered for your company on the GST portal right now. If it is an external consultant's email, consider whether you want to change it to an internal email that your team monitors regularly. Missing a notice because it went to an outdated or unmonitored email could be catastrophic.

9.2 Strengthen Your Year-Wise Documentation

Even though consolidated notices are now permitted in fraud cases, you will still need to defend each year on its merits. Make sure your Input Tax Credit claims, supplier verification records, and transaction documentation are organised by financial year.

If your company ever faces a consolidated proceeding, year-wise organisation will be essential for mounting an effective defence. You cannot defend five years of transactions if your records are jumbled together.

9.3 Review Your Vendor Verification Processes

A large proportion of GST fraud cases involve Input Tax Credit claimed from fake or non-existent suppliers. The tax department has sophisticated data analytics to identify suspicious patterns.

Review your vendor onboarding and verification processes. Are you conducting adequate due diligence before claiming Input Tax Credit? Do you verify that suppliers have actually filed their returns? Implementing robust vendor verification is not just good compliance; it is insurance against fraud allegations.

9.4 Train Your Team on Response Protocols

When tax authorities send queries or initiate investigations, the way your team responds matters enormously. Casual admissions, poorly worded explanations, or incomplete responses can escalate a routine enquiry into a fraud investigation.

Establish clear protocols for handling GST queries. All responses should be reviewed by someone with appropriate authority and expertise before being submitted. Document everything.

9.5 Build a Relationship with Specialist Advisors

GST litigation has become increasingly complex. The interplay between High Court precedents, Supreme Court rulings, and evolving departmental practices requires specialist knowledge.

If you do not already have access to experienced GST litigation advisors, now is the time to identify them. When a notice arrives, you do not want to be searching for expertise under pressure.

10. The Bigger Question: Is This Fair to Businesses?

Let me step back and offer some perspective on what this ruling means for the business environment in India.

From the government's perspective, the Supreme Court ruling makes sense. GST fraud, particularly fake Input Tax Credit claims, has been a serious problem. Fraudsters who operate sophisticated schemes across multiple years should not be able to escape through procedural technicalities. Allowing consolidated proceedings makes investigations more efficient and comprehensive.

From the business community's perspective, there are legitimate concerns. The ease with which fraud can be alleged, combined with the significant consequences that now follow, creates an asymmetry of power. Honest businesses may find themselves defending against serious allegations that are difficult to disprove.

The healthy middle ground would be clear guidelines on when consolidated proceedings are appropriate and when they are not. Industry associations and tax professional bodies should advocate for such guidelines from the GST Council. Without clear boundaries, there is a risk that the power to consolidate could be misused.

11. What Happens Next in GST Litigation

Looking ahead, expect the question of fraud to become the most fiercely contested issue in GST disputes.

Previously, even if fraud was alleged, businesses could challenge consolidated notices on procedural grounds. That escape route has now been significantly narrowed. The battle will increasingly focus on whether fraud is actually made out.

This means courts will need to carefully examine what constitutes fraud, wilful misstatement, or suppression of facts. Mere errors or discrepancies should not automatically trigger Section 74 treatment. There must be evidence of deliberate intent.

As a finance leader, ensure your documentation clearly demonstrates good faith compliance. If discrepancies are later identified, your contemporaneous records should show that you acted in good faith based on the information available at the time.

12. Your Action Checklist

Let me summarise everything into a simple checklist you can act on immediately.

First, understand the Section 73 versus Section 74 distinction. This single factor determines much of your legal position.

Second, audit your GST portal registration details today. Ensure notices will reach someone who can act on them promptly.

Third, organise your records year-wise. Even if proceedings are consolidated, your defence must be year-specific.

Fourth, strengthen vendor verification processes to reduce the risk of inadvertent Input Tax Credit issues.

Fifth, establish clear protocols for responding to tax queries. Careless responses can escalate matters unnecessarily.

Sixth, identify specialist advisors before you need them. Preparation is everything.

13. The Bottom Line

The Supreme Court has ruled. In fraud cases, consolidated GST notices covering multiple financial years are valid. This is now the law of the land.

For cases without fraud allegations, some protection may still exist under High Court precedents. But this distinction is fragile, and no finance leader should take comfort from it.

The practical reality is this: the best defence is prevention. Robust compliance processes, thorough documentation, careful vendor verification, and prompt attention to tax queries will serve your company far better than any courtroom argument.

This ruling is a wake-up call for Indian businesses. The GST authorities have more power than before. How you respond to that reality will determine whether your company navigates this landscape successfully.

Save this article. Share it with your board and your tax team. The information here could be worth far more than the few minutes it took to read.

Knowledge is the best protection. Now you have it.

What challenges is your company facing with GST compliance? Have you received consolidated notices? Share your experiences below. Let us learn from each other.

If this guide helped you understand a complex legal change, share it with fellow finance professionals who need to know about it.

Relevant Cases Laws:

-

Mathur Polymers vs Union of India – Supreme Court (2026) 182 taxmann.com 215 (SC)

-

Albatross Builders and Developers LLP vs Assistant Commissioner of Central Tax (A.E.), Bengaluru - Karnataka High Court (2024) 169 taxmann.com 598 (Kar.)

-

Milroc Good Earth Developers vs Union of India - Bombay High Court (2025) 179 taxmann.com 465 (Bom.)

-

Oriental Lotus Hotel Supplies Pvt. Ltd. vs Joint Commissioner - Madras High Court (2025) 177 taxmann.com 563 (Mad.)

-

Pramur Homes and Shelters vs Union of India – Karnataka High Court (2025) 181 taxmann.com 541 (Kar.)

-

Smt. R. Ashaarajaa vs Senior Intelligence Officer, Directorate General Of GST Intelligence - Madras High Court (2025) 176 taxmann.com 689 (Mad.)

-

R A and Co vs Additional Commissioner of Central Taxes - Madras High Court (2025) 176 taxmann.com 731

-

Titan Company Ltd. vs Joint Commissioner of GST & Central Excise - Madras High Court (2024) 159 taxmann.com 162 (Mad.)

-

Tharayil Medicals vs Deputy Commissioner, SGST Department, Thrissur - Kerala High Court (2025) 173 taxmann.com 867 (Ker.)

-

Veremax Technologie Services Ltd. vs Assistant Commissioner of Central Tax, Bengaluru - Karnataka High Court (2024) 167 taxmann.com 332 (Kar.)

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Please consult qualified professionals for guidance on your specific situation

Need for GST in India | Powers of GST Officers | UQC Code in GST | GSTR 3B table 5 | DRC-01 format | Penalty for non GST registration | Audit u/s 65(3) (gst adt-01)

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified