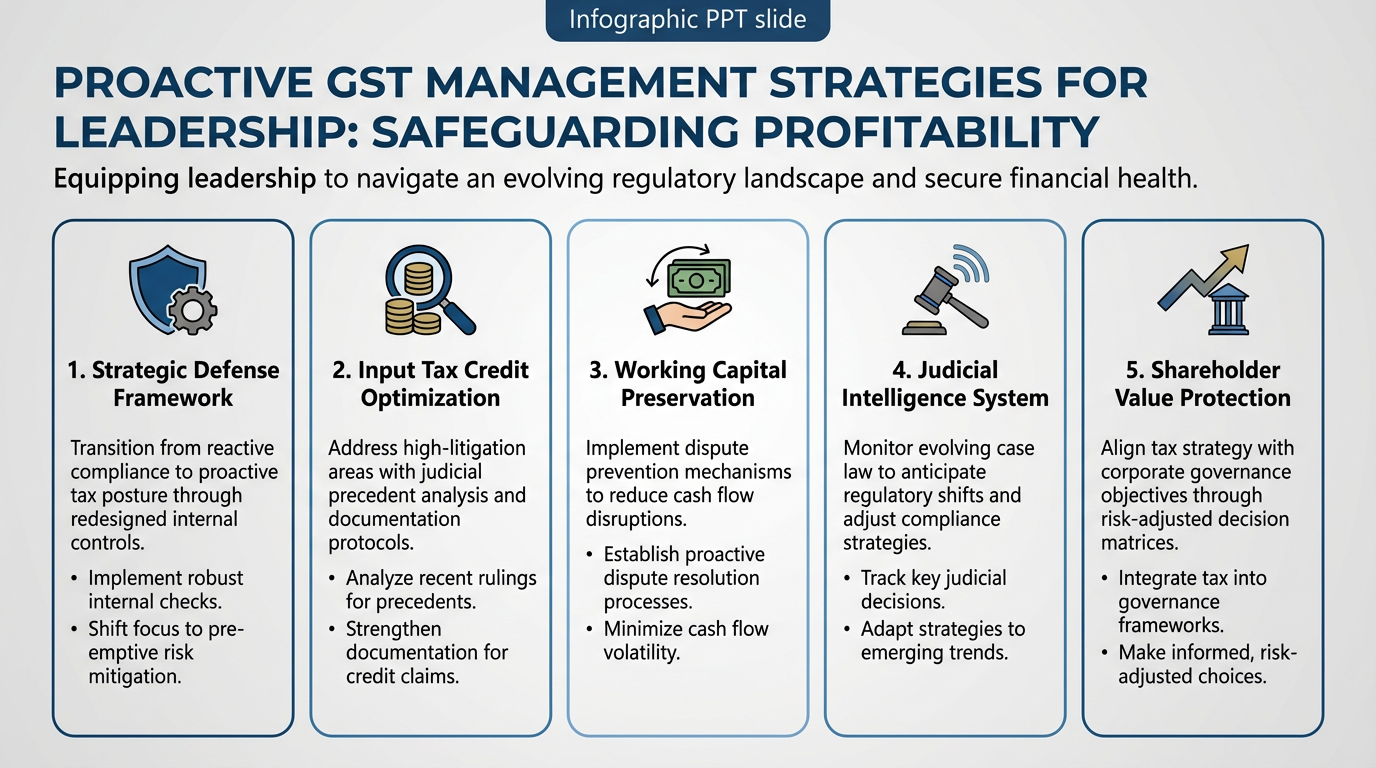

1.0 Purpose and Strategic Context

This article serves as an essential strategic guide for senior leadership navigating the complexities of the Goods and Services Tax (GST) regime. In an environment of heightened scrutiny by tax authorities and evolving judicial interpretations, a reactive approach directly threatens profitability. This article provides a strategic framework to not only defend against current tax disputes but to fundamentally redesign internal controls, transforming your GST posture from reactive compliance to proactive defence, thereby protecting shareholder value and preserving working capital. We begin with the most litigated and financially significant area: Input Tax Credit.

2.0 Fortifying Input Tax Credit (ITC) Claims

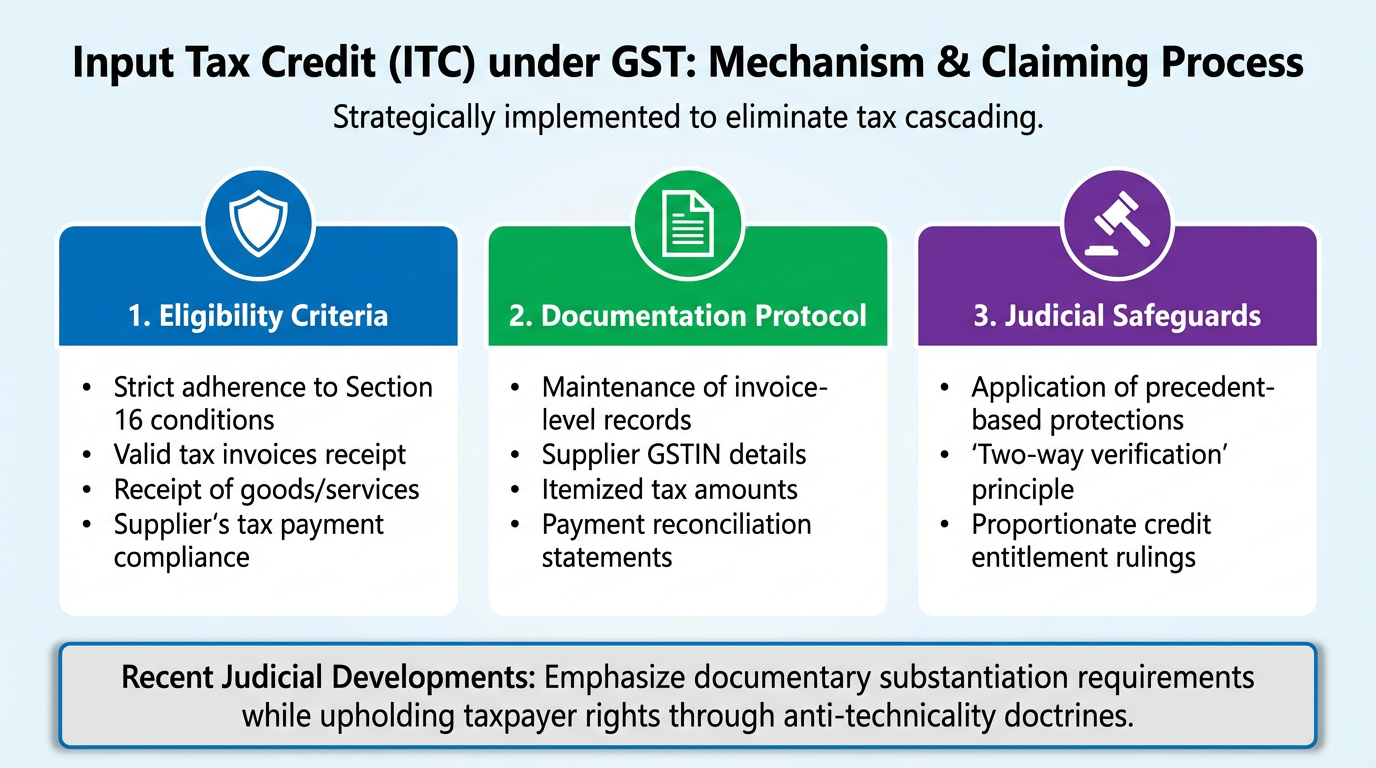

Input Tax Credit (ITC) is a cornerstone of the GST regime, designed to prevent the cascading effect of taxes. It is also, unsurprisingly, the primary area of dispute between taxpayers and revenue authorities. A robust framework for claiming and substantiating ITC is non-negotiable for safeguarding your company’s financial health. This section deconstructs the key legal requirements and recent judicial precedents to provide a framework for safeguarding ITC claims.

2.1 The Evolving Legal Framework for ITC

The core conditions for availing ITC are stipulated in Section 16(2) of the CGST Act. At a minimum, a business must have a valid tax invoice or debit note. However, the compliance landscape is tightening. The impending implementation of clause (aa) to Section 16(2) introduces a critical dependency: a recipient's right to ITC is contingent upon the supplier furnishing the details of that specific invoice in their outward supply returns. This amendment effectively and formally links a recipient’s ITC claim directly to their supplier's compliance, making vendor diligence an integral part of ITC management.

2.2 Navigating GSTR-2A/2B Mismatches: A Judicial Perspective

A frequent challenge for businesses is the denial of ITC due to mismatches between the credit claimed in their GSTR-3B return and the data auto-populated in their GSTR-2A/2B, which is derived from supplier filings. Tax authorities often move to reverse ITC when a supplier fails to report a transaction.

However, the judiciary has provided a degree of protection. In the case of Inko Chemicals India (P) Ltd., the Madras High Court established a crucial legal principle: ITC cannot be reversed merely because the selling dealer has not disclosed the transaction in their monthly return. This precedent is vital, as it shifts the focus from a purely automated check to a more substantive review of the transaction's genuineness.

Strategic Implication:

This ruling arms your company with a legal basis to contest automated ITC reversals, forcing tax authorities to prove a transaction's lack of genuineness rather than relying solely on system mismatches.

2.3 The Burden of Proof: Documentation and Due Diligence

While mismatches alone may not be sufficient grounds for denial, the burden of proving the legitimacy of a transaction rests firmly on the purchasing dealer claiming the ITC. The courts have reinforced the stringency of documentation requirements.

In a key observation in the ECOM Gill Coffee Trading case, the Supreme Court articulated that the purchasing dealer must be able to prove the actual physical movement of goods to substantiate their ITC claim. This goes beyond just possessing an invoice; it requires a comprehensive documentary trail. In the face of a challenge from tax authorities, robust documentation—including e-way bills, transportation receipts, and delivery challans—is the only viable defence.

2.4 Strategic Recommendations for Proactive ITC Management

Based on this legal and judicial landscape, management should implement the following non-negotiable internal controls:

-

Mandate Formal Supplier Verification: Institute a formal process to verify the GST compliance history and identity of suppliers before transacting. The cancellation of a supplier's registration, even retrospectively, can jeopardise your ITC claims.

-

Enforce Flawless Documentation Integrity: Mandate the meticulous collection and archiving of all documents required to prove not only the financial transaction but also the physical movement of goods. This includes tax invoices, e-way bills, lorry receipts, and proof of payment.

-

Establish Rigorous Reconciliation Discipline: Institute a mandatory and timely reconciliation process between internal purchase records, the auto-populated GSTR-2B, and the ITC claimed in GSTR-3B filings. Discrepancies must be identified and resolved with suppliers immediately.

While a fortified ITC process is your first line of defence, it is inevitable that robust claims will invite departmental scrutiny. Therefore, understanding how to manage the resulting assessments and audits is the critical second pillar of a resilient GST strategy.

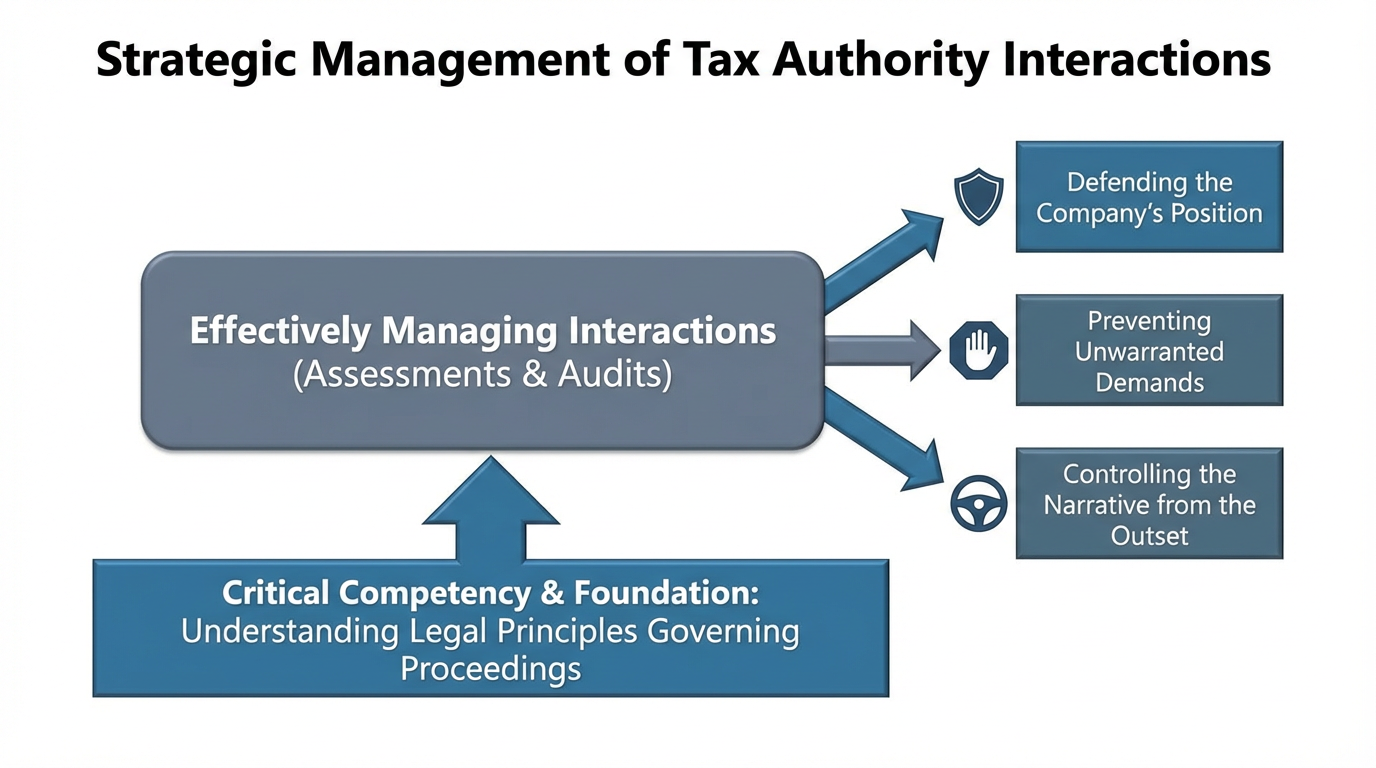

3.0 Proactive Management of GST Assessments and Audits

Effectively managing interactions with tax authorities during assessments and audits is a critical competency. Understanding the legal principles that govern these proceedings is crucial for defending the company's position, preventing unwarranted demands, and controlling the narrative from the outset.

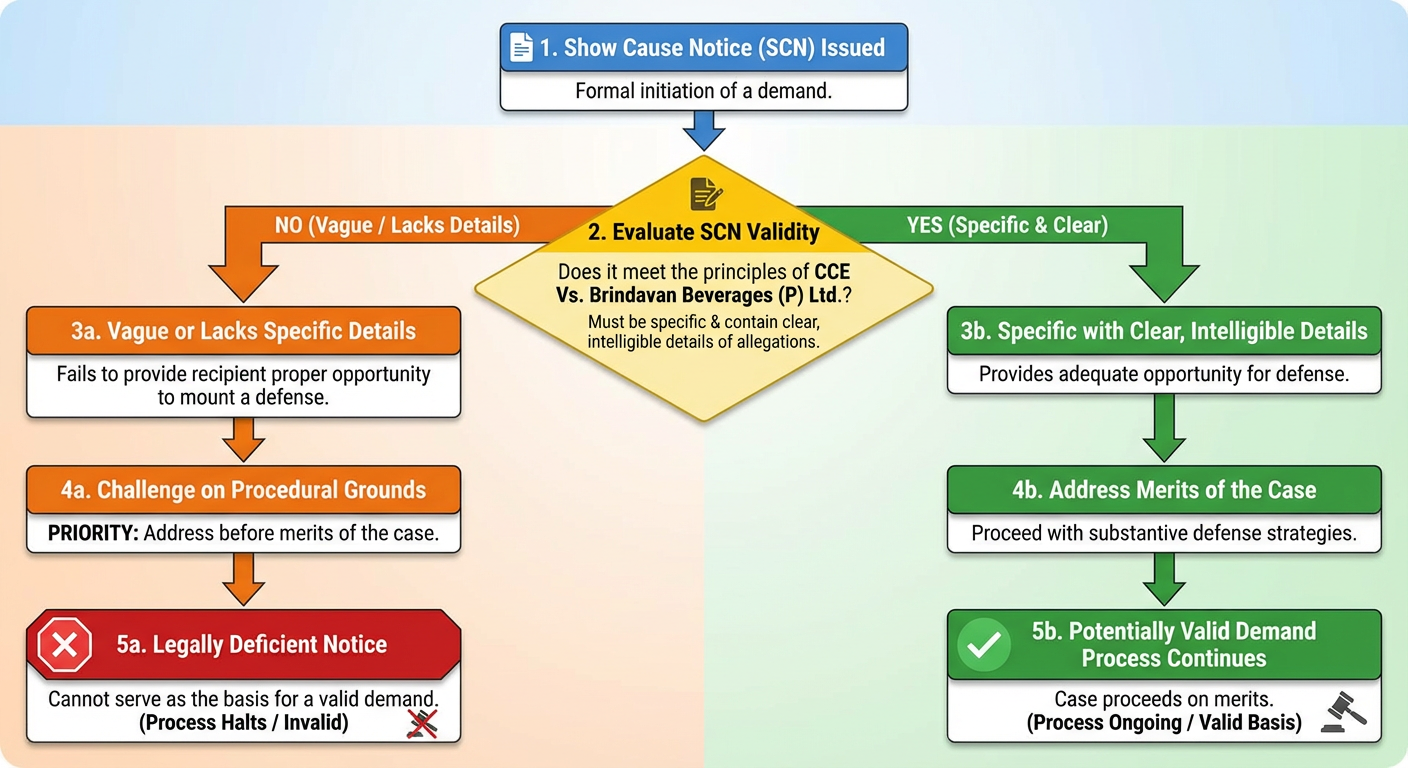

3.1 Responding to a Show Cause Notice (SCN)

A Show Cause Notice (SCN) is the formal initiation of a demand. However, not all SCNs are legally valid. Based on the principles established by the Supreme Court in CCE Vs. Brindavan Beverages (P) Ltd., an SCN must be specific and contain clear, intelligible details of the allegations. A notice that is vague or lacks specific details fails to provide the recipient with a proper opportunity to mount a defense. Such notices can, and should, be challenged on procedural grounds before addressing the merits of the case. A legally deficient notice cannot serve as the basis for a valid demand.

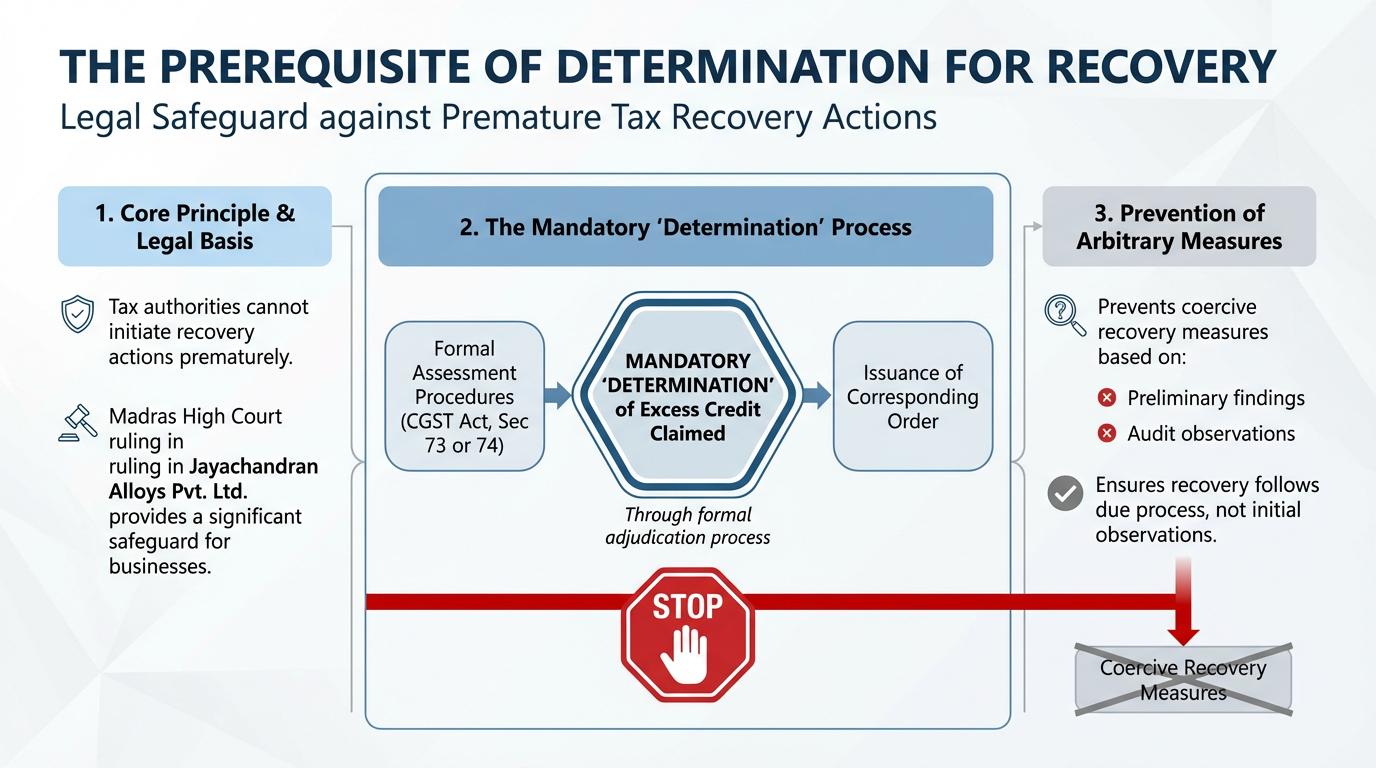

3.2 The Prerequisite of Determination for Recovery

Tax authorities cannot initiate recovery actions prematurely. The Madras High Court ruling in Jayachandran Alloys Pvt. Ltd. provides a significant safeguard for businesses. The court held that the "determination" of any excess credit claimed, through the formal assessment procedures laid out in Section 73 or 74 of the CGST Act, is a mandatory "pre-requisite" for initiating recovery. This prevents authorities from taking coercive recovery measures based on preliminary findings or audit observations without first completing a formal adjudication process and issuing a corresponding order.

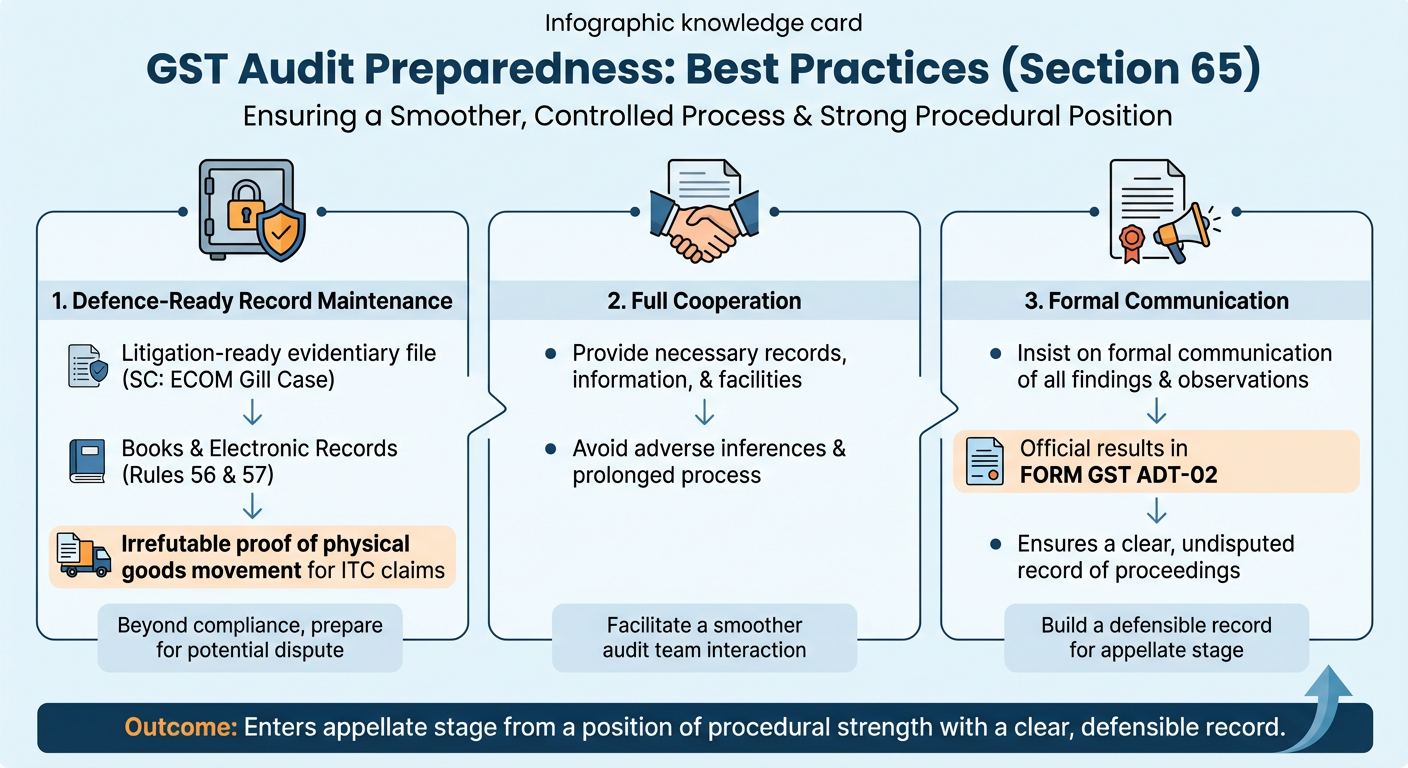

3.3 Best Practices for Audit Preparedness

When facing a GST audit under Section 65, preparedness is key. Adherence to the following best practices, derived from the GST Audit Manual and statutory rules, will ensure a smoother and more controlled process:

-

Defence-Ready Record Maintenance: In line with the Supreme Court's stringent requirements in the ECOM Gill Coffee Trading case, ensure all books of accounts and electronic records (per Rules 56 and 57) are maintained not just for compliance, but as a litigation-ready evidentiary file. This includes irrefutable proof of the physical movement of goods for every significant ITC claim.

-

Cooperation: Cooperate fully with the audit team by providing the necessary records, information, and facilities. A lack of cooperation can lead to adverse inferences and unnecessarily prolong the audit process.

-

Formal Communication: Insist that all audit findings, discrepancies, and final observations are communicated formally by the proper officer. The official communication of audit results must be made in FORM GST ADT-02, ensuring a clear and undisputed record of the proceedings.

Mastering the procedural elements of an audit ensures that, should a dispute escalate, the company enters the appellate stage from a position of procedural strength, with a clear and defensible record.

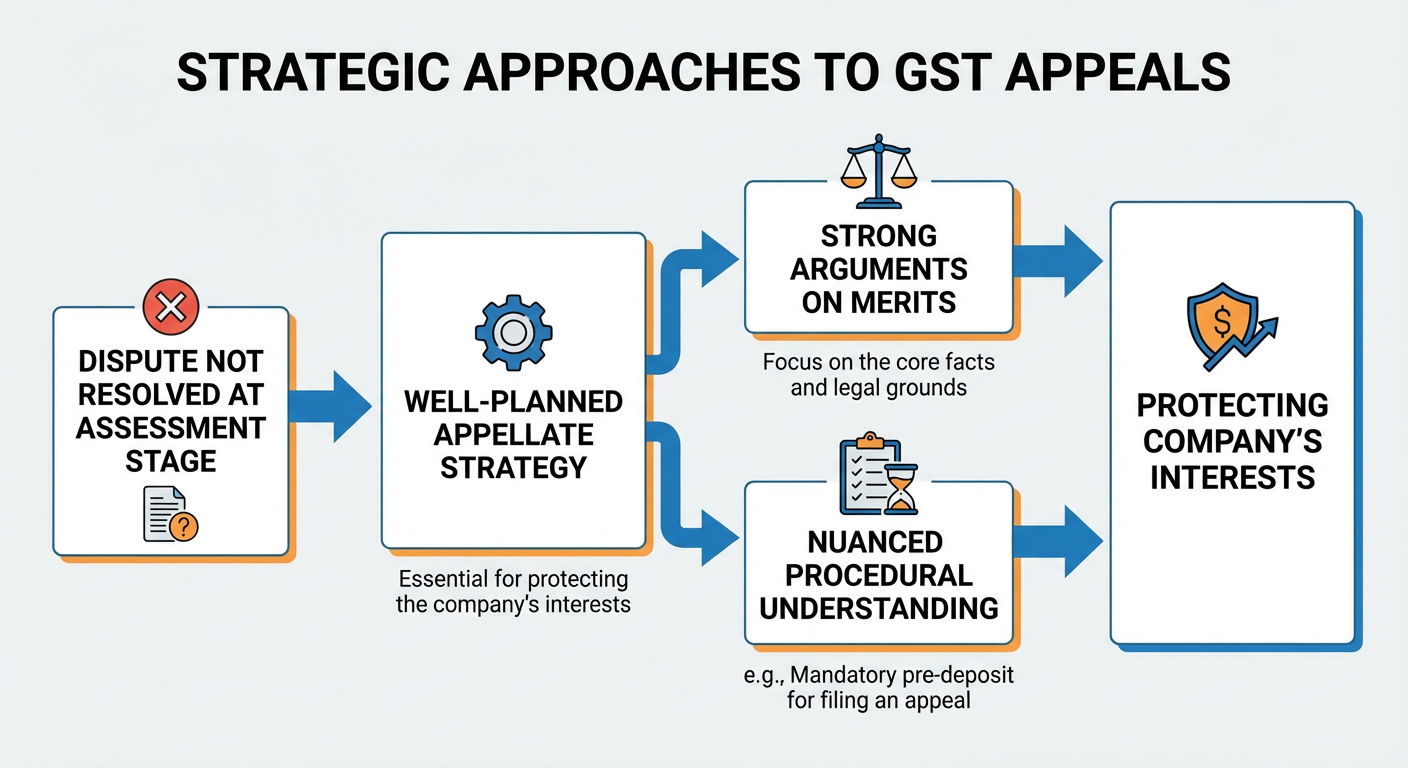

4.0 Strategic Approaches to GST Appeals

When disputes are not resolved at the assessment stage, a well-planned appellate strategy is essential for protecting the company's interests. This requires not only strong arguments on the merits of the case but also a nuanced understanding of procedural requirements, such as the mandatory pre-deposit for filing an appeal.

4.1 Understanding the Pre-Deposit Requirement

Under the appellate mechanism, which mirrors the principles of Section 35F of the former Central Excise Act, an appeal cannot proceed without a mandatory pre-deposit of seven and a half percent (7.5%) of the disputed tax amount. This requirement can place an immediate strain on a company's working capital. In GST, on similar grounds as Central Excise, 10% in the First appeal and a total* of 20% in the appeal before GSTAT.

*total 20% means 20% minus whatever has been deposited before first appellate authority. So 10% deposited in appeal U/s 107 then additional 10% but if filing appeal against the order under section 108 (Revisional Authority Order) then 20% - 0% = 20%.

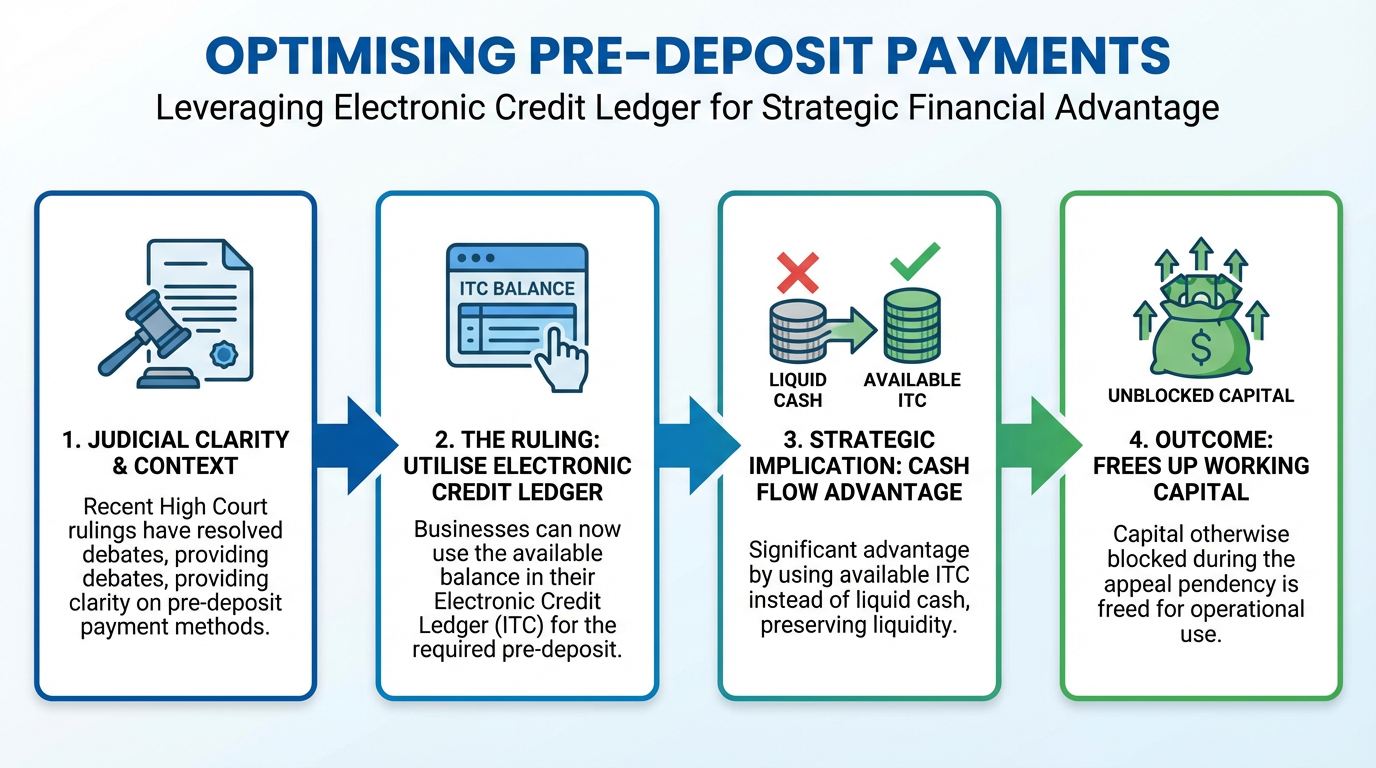

4.2 Optimising Pre-Deposit Payments

The method of paying this pre-deposit has been a subject of debate, but recent judicial rulings have provided welcome clarity and a significant financial advantage. Various High Courts have held that businesses can make the required pre-deposit by utilising the balance available in their electronic credit ledger.

The strategic implication of this ruling is profound: it provides a significant cash flow advantage by allowing businesses to use their available ITC instead of liquid cash to meet the pre-deposit requirement. This frees up working capital that would otherwise be blocked during the pendency of the appeal.

5.0 Concluding Strategic Imperatives

To navigate the current landscape and safeguard the company's financial health, leadership must embed the following four strategic imperatives into the organisation's operational DNA.

-

Institutionalise a Zero-Tolerance ITC Diligence Protocol:

Implement a mandatory, cross-functional process to validate supplier GST compliance and ensure flawless documentation for every transaction. This is essential to protect ITC claims, which remain the primary source of GST litigation and financial exposure.

-

Challenge Procedural Lapses Aggressively: Instruct teams to rigorously scrutinise all departmental notices. Leverage the Brindavan Beverages principle to challenge vague SCNs and the Jayachandran Alloys ruling to preempt any recovery actions before a formal determination under Section 73/74 is complete. This two-pronged procedural defence can neutralise threats before they escalate.

-

Leverage ITC for Cash Flow in Disputes: In any GST dispute requiring an appeal, direct the finance team to utilise the balance in the Electronic Credit Ledger for the mandatory pre-deposit. This judicial affirmation preserves critical working capital and reduces the financial strain of litigation.

-

Embed a 'Defence-Ready' Mindset:

Shift the organisation's posture from purely compliance-focused to 'defence-ready.' This involves maintaining meticulous records, ensuring all tax positions are supported by statutory provisions and relevant judicial precedents, and preparing for scrutiny as a matter of course, not as a reaction to a notice.

Need for GST in India | Powers of GST Officers | GSTR 3B table 5 | DRC-01 format | Penalty for non GST registration | Audit u/s 65(3) (gst adt-01)

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified