Classification Disputes Under GST: Why Section 73 Applies and Section 74 Does Not

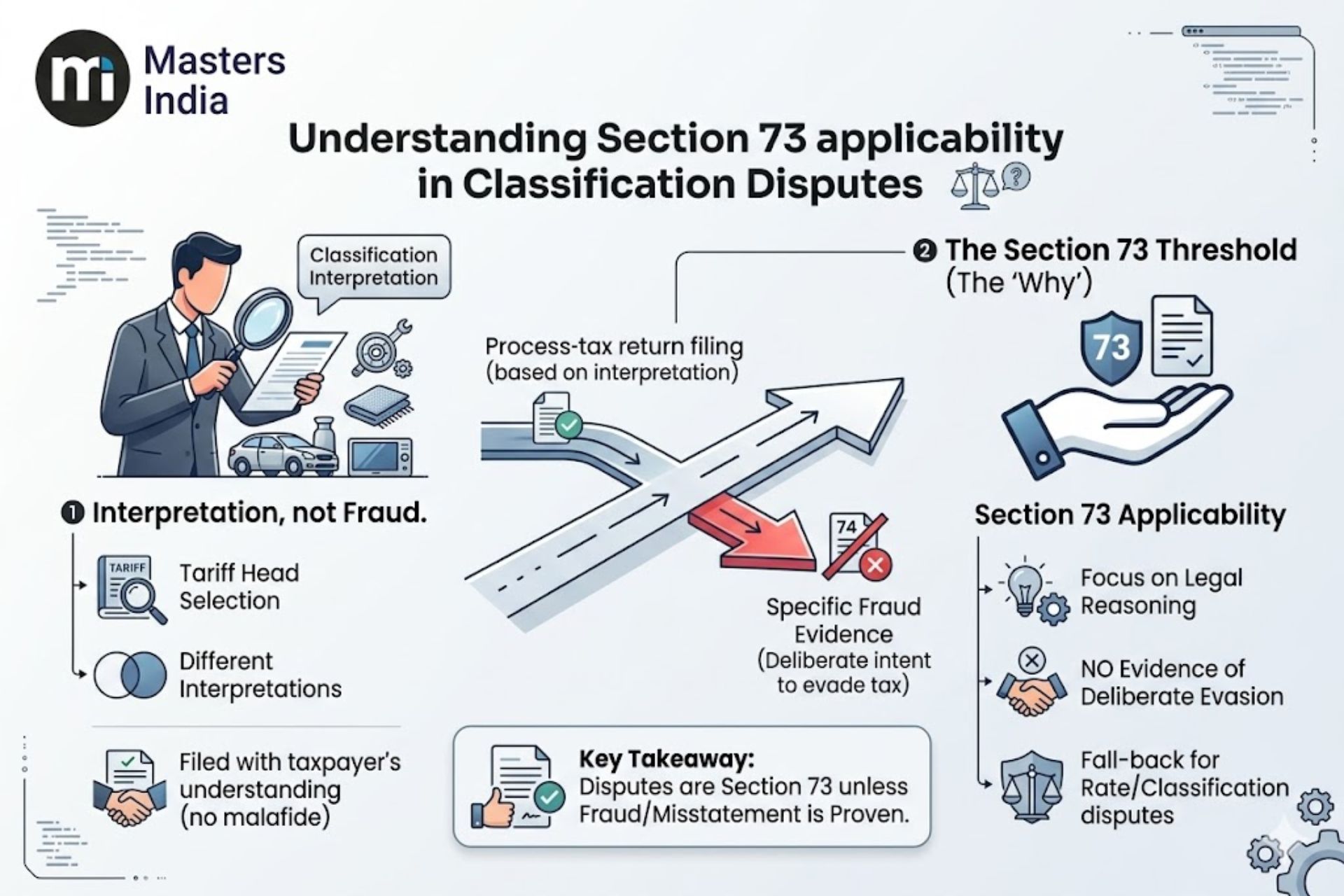

In a standard classification dispute, Section 73 is the correct section to invoke, provided the dispute arises from a bona fide (genuine) difference in interpretation of the law and not from a deliberate intent to evade tax.

Why GST classification disputes generally fall under Section 73

Under the GST framework, the law clearly bifurcates demand and recovery into two scenarios:

| Section 73 | Section 74 |

|---|---|

| Invoked for the determination of tax not paid, short paid, or erroneously refunded for any reason other than fraud, wilful misstatement, or suppression of facts. | Invoked strictly when the non-payment or short payment is driven by fraud, wilful misstatement, or suppression of facts with the specific intention to evade tax. |

Section 73 is the correct provision for adjudicating a classification dispute, whereas Section 74 cannot be routinely invoked in such matters, making it important for taxpayers to clearly understand the distinction between Section 73 vs Section 74 under GST while handling such disputes.

Understanding the legal reasoning behind Section 73 applicability

Classification disputes inherently involve the interpretation of tariff entries and settled principles of law, requiring substantial discussion to determine the appropriate Tariff Head for a product, and since such disputes revolve around tariff interpretation, understanding HSN codes under GST becomes essential.

Section 74 can only be invoked when there is specific and necessary evidence of fraud, wilful misstatement, or suppression of facts with the deliberate intent to evade tax. Filing tax returns under a specific Tariff Head based on a taxpayer's interpretation does not amount to deliberate concealment or a malafide intention to withhold information.

Therefore, without concrete proof of an intent to evade tax, a classification or rate dispute falls strictly under the purview of Section 73 rather than Section 74.

Key court rulings on GST classification disputes

| X'SS Beverage Co. — Hon'ble Gauhati High Court (2025) 28 CENTAX 97 (Gau.) |

|

|---|---|

| Key Ruling |

The Court explicitly ruled that a Show Cause Notice (SCN) under Section 74 cannot be issued for classification disputes. The Court observed that because determining an appropriate Tariff Head requires substantial legal discussion, a taxpayer filing returns under a particular Tariff Head cannot be accused of deliberate and wilful suppression or non-disclosure of facts. Consequently, the Court held that invoking the powers under Section 74 for such classification disputes is uncalled for and unwarranted. Businesses receiving such notices should therefore understand the procedural implications of a GST demand notice under Rule 142 (DRC‑01) and the legal remedies available under the GST framework. |

| M/S NCS Pearson Inc. vs Union of India — Hon'ble Karnataka High Court (2025) 34 CENTAX 445 (Kar.) |

|

|---|---|

| Key Ruling |

The Court held that in a classification dispute where the taxpayer had already approached the Authority for Advance Ruling (AAR), the department was well aware of the issue, meaning there could be no allegation of suppression or fraud. The Court emphasised that when revenue authorities themselves entertain conflicting views on classification, it is impermissible to allege suppression with intent to evade tax. Thus, issuing an SCN under Section 74 under such circumstances was declared illegal, arbitrary, and without jurisdiction. Businesses facing uncertainty in classification can proactively seek clarity through an Advance Ruling under GST, while recognising that proper documentation and structured defence strategy remain essential for managing disputes, audits, and appeals effectively, as discussed in practical guidance on GST litigation, audit, and appeal strategy. |

| Densons Pultretaknik, Northern Plastics Ltd. & Biomax Life Sciences Ltd. — Line of Judgements | |

|---|---|

| Key Ruling | In these lines of judgements, it was established that mere claiming of a wrong classification or a wrong exemption cannot be considered a suppression or misstatement of facts. Thus, invoking provisions equivalent to Section 74 (extended period) is invalid for basic classification errors. |

| Citations |

|

| Continental Foundation Jt. Venture vs Commr. of C. Ex., Chandigarh-I — Supreme Court | |

|---|---|

| Key Ruling | The Supreme Court ruled that the expression "suppression" must be construed strictly. A mere omission to give correct information is not suppression of facts unless it was deliberate to stop the payment of duty. The court highlighted that an incorrect statement cannot simply be equated with a wilful misstatement. |

| Anand Nishikawa Co. Ltd. vs Commissioner of Central Excise — Supreme Court (2005) 188 ELT 149 (SC) |

|

|---|---|

| Key Ruling | The court held that if there is no deliberate attempt of non-disclosure to escape duty, a finding of "suppression of facts" by the department cannot be approved or sustained. |

| N.V.K. Mohammed Sulthan Rawther vs Union of India — Kerala High Court (2019) 20 GSTL 708 (Ker.) |

|

|---|---|

| Key Ruling | The court ruled that when a manufacturer declares an HSN code under a bona fide belief that their product attracts that code and pays tax accordingly, the manufacturer cannot be faulted or accused of evading tax just because the assessing officer believes a different classification applies. |

GST classification disputes: When Section 73 applies over Section 74

Courts have consistently held that merely claiming a wrong classification or a wrong exemption based on a different interpretation of the tariff does not, in itself, amount to "suppression of facts" or "wilful misstatement".

Because mens rea (guilty mind or deliberate intent to evade) is generally absent in genuine classification disputes, the extended period of limitation and higher penalties under Section 74 cannot be automatically invoked. Accordingly, understanding various GST penalties and offences becomes important for businesses to properly evaluate potential litigation exposure and compliance risks under the GST framework.

In summary, unless the tax department can bring concrete evidence on record to prove that the taxpayer deliberately misclassified the goods to fraudulently evade taxes, the proceedings must be confined to Section 73.

GST Framework | Section 73 | Section 74 | GST Software | GST Compliance

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified