The Goods and Services Tax Appellate Tribunal (GSTAT) (Procedure) Rules, 2025, place immense importance on the meticulous preparation and presentation of the "Statement of Facts" due to the GSTAT's role as the final fact-finding authority. High Courts are expected to focus primarily on "substantial questions of law" arising from GSTAT orders, making a thorough factual presentation at the GSTAT stage crucial.

To further refine the understanding of effective factual presentation, drawing from GSTAT's procedural robustness, its comparison to CESTAT, and the incorporation of Code of Civil Procedure (CPC) principles, here’s a detailed approach to drafting an ideal "Statement of Facts" for various GST disputes.

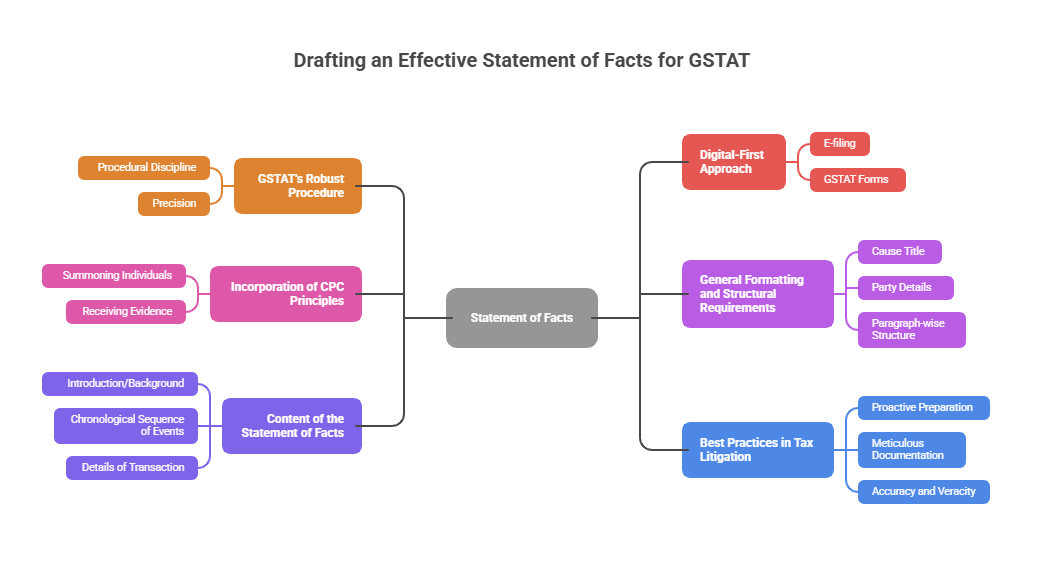

Foundational Principles for Drafting the "Statement of Facts"

The GSTAT's procedural framework, while modern and digital-first, is built upon established tribunal principles and selectively incorporates aspects of civil procedure:

1. GSTAT's Robust Procedure: The GSTAT Rules are explicitly designed to be "more detailed and codified" than the former Customs, Excise, and Service Tax Appellate Tribunal (CESTAT) Rules. This shift from reliance on administrative guidance to specific, binding procedures demands enhanced "procedural discipline" and "precision".

2. Digital-First Approach: Mandatory e-filing through the GSTAT Portal and the use of standardised GSTAT Forms (GSTAT FORM-01 for interlocutory applications, GSTAT FORM-05 for primary appeals) are central to this framework. All proceedings are to be recorded on the GSTAT portal, enhancing transparency.

3. Incorporation of CPC Principles: While GSTAT is not strictly bound by the CPC, it possesses powers similar to a civil court for specific functions. This includes summoning individuals and documents, receiving evidence on affidavits (conforming to Order XIX, Rule 3), and issuing commissions (guided by Orders XVI and XXVI). GSTAT orders are enforceable as civil court decrees, guided by Order 21 CPC.

Ideal Way to Write a "Statement of Facts" (Template and Best Practices)

The "Statement of Facts" must be a clear, concise, and chronologically presented narrative that lays the factual foundation for the "Grounds of Appeal".

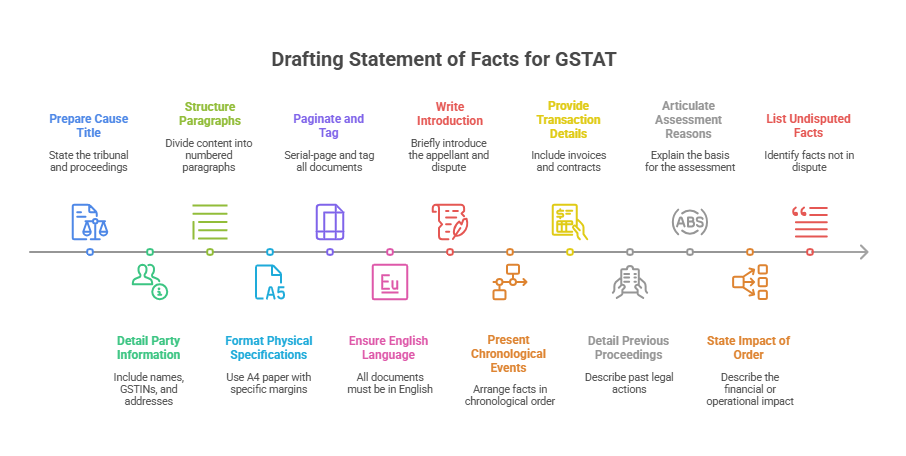

I. General Formatting and Structural Requirements:

• Cause Title: Must clearly state "In the Goods and Service Tax Appellate Tribunal" and identify the proceedings or order being challenged.

• Party Details: Full name, parentage, GST Identification Number (GSTIN), description, and address of each party must be set out at the beginning and should not be repeated in subsequent proceedings. Parties are numbered consecutively.

• Paragraph-wise Structure: The appeal content must be divided into "consecutively numbered paragraphs, with each paragraph focusing on a separate fact, allegation, or point". This ensures clarity and avoids ambiguity.

• Physical Specifications: All pleadings and forms should be typed neatly in double spacing on A4 size paper, printed one side only, with specific margins (5 cm on the left and 2.5 cm on the right).

• Pagination and Tagging: Every sheet of the appeal form and accompanying documents must be "serial-paged and tagged with the Form". Proper indexing and pagination are mandated.

• Language: All documents, including the "Statement of Facts," must be in English. If any relied-upon documents are in a non-English language, they must be accompanied by an agreed or certified English translation. The case will not be listed until translation requirements are met.

II. Content of the "Statement of Facts" (Model Template Structure)

A "Statement of Facts" should typically include the following sections, building a comprehensive factual narrative:

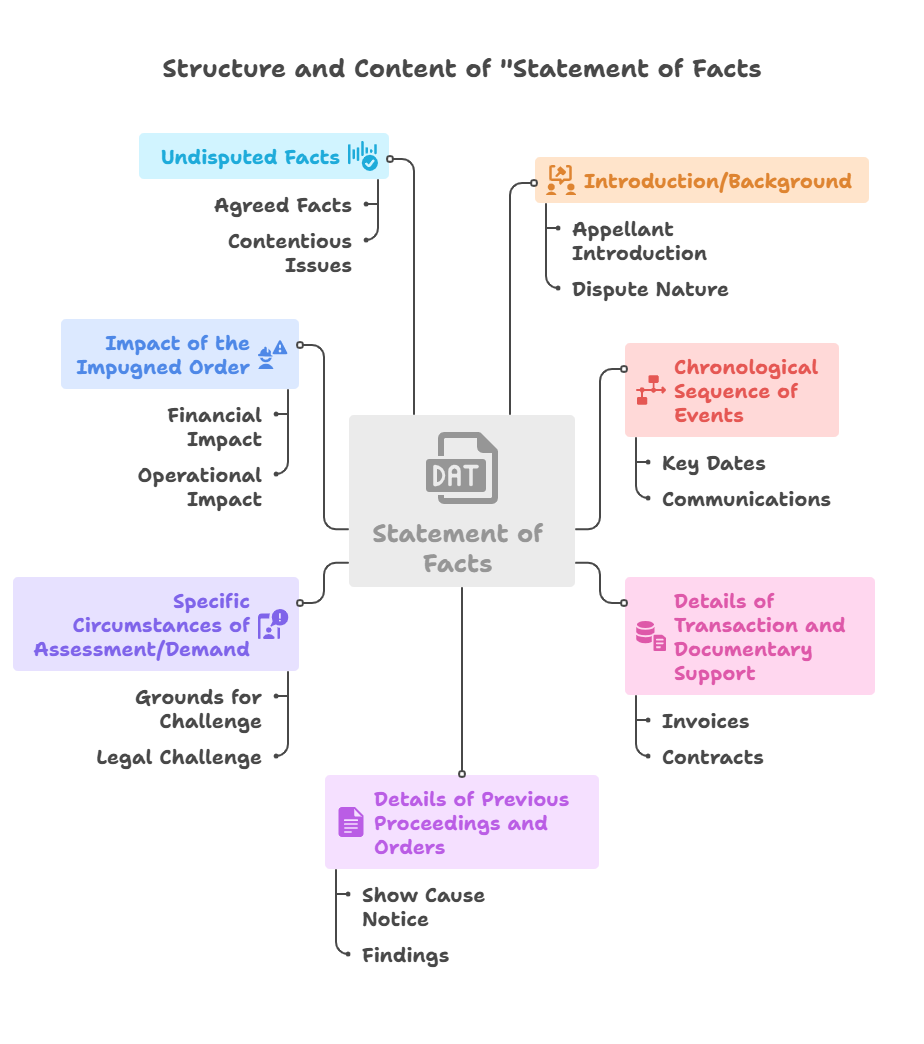

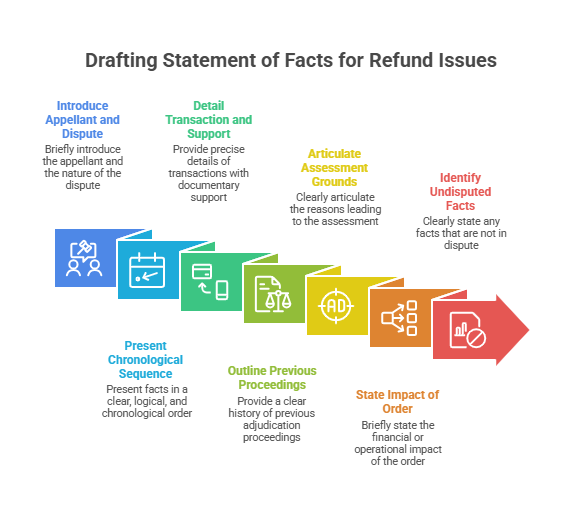

1. Introduction/Background:

◦ Briefly introduce the appellant and their business activity.

◦ State the nature of the dispute and the order being challenged.

2. Chronological Sequence of Events:

◦ Present facts in a clear, logical, and chronological order, starting from the genesis of the issue.

◦ Include dates of key transactions, statutory filings, departmental actions, and communications.

◦ Example: "On [Date], the Appellant supplied [Goods/Services] to [Recipient] with Invoice No. [X]. On [Date], a notice under Section [Y] was issued..."

3. Details of Transaction and Documentary Support:

◦ Provide precise details of the transactions involved, referencing specific invoices, purchase orders, contracts, ledger entries, bank statements, etc.

◦ Each factual assertion should be backed by a corresponding document (e.g., "Invoice No. XYZ, copy enclosed as Annexure A-1").

◦ Best Practice: Ensure documents are properly organised and marked (e.g., Appellant's documents as 'A' series, Respondent's as 'B' series, Tribunal's as 'C' series).

4. Details of Previous Proceedings and Orders:

◦ Provide a clear history of the original adjudication proceedings, including the Show Cause Notice (SCN).

◦ Detail the findings of the Adjudicating Authority and the First Appellate Authority.

◦ Highlight any procedural lapses or denial of natural justice at lower stages (e.g., denial of cross-examination requests).

◦ Include details of any correspondence exchanged with tax authorities.

5. Specific Circumstances of Assessment/Demand:

◦ Clearly articulate the specific grounds or reasons leading to the assessment or demand being challenged.

◦ This section bridges the gap between the facts and the legal challenge, demonstrating how the facts resulted in the impugned order.

6. Impact of the Impugned Order:

◦ Briefly state the financial or operational impact of the order on the appellant. This contextualises the "Prayer."

7. Undisputed Facts:

◦ Clearly state any facts that are not in dispute between the parties. This streamlines the hearing by allowing the Tribunal to focus on contentious issues.

III. Tailoring the "Statement of Facts" for Different Types of GST Disputes:

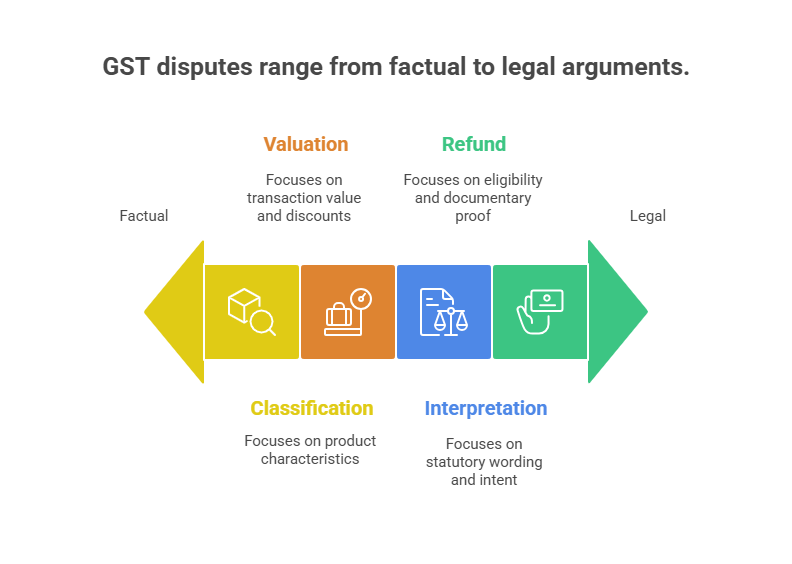

The general template must be adapted to foreground the specific factual nuances of different categories of GST disputes, which typically include Rate of Tax, Classification (HSN/SAC), Valuation, Interpretation of Statutory Provisions, Applicability of Notifications, and Refund Issues.

1. For Classification (HSN/SAC) / Rate of Tax Disputes:

◦ Focus: Product/service characteristics, manufacturing process, end-use, market perception, trade parlance, composition of goods/services.

◦ Key Factual Elements:

▪ Detailed description of the goods/services, including technical specifications, ingredients, and functions.

▪ Manufacturing process or service delivery method.

▪ Evidence of market practice and consumer perception for similar goods/services.

▪ Comparison with other products/services classified differently.

▪ Relevant industry standards or expert opinions.

◦ Example: "The Appellant manufactures a product described as [Product Name] (Annexure A-2, technical specifications). It is composed of [ingredients/components]. Its primary function is [function], and it is marketed as [marketing description] (Annexure A-3, marketing materials). Similar products, [Comparable Product], are classified under HSN [X] with a GST rate of [Y%] (Annexure A-4, market research)."

2. For Valuation Disputes:

◦ Focus: Transaction value, related party transactions, discounts, subsidies, inclusions/exclusions in value, specific valuation rules.

◦ Key Factual Elements:

▪ Terms of sale, pricing mechanisms, and contractual agreements.

▪ Relationship between transacting parties (if related party transaction).

▪ Details of discounts offered (trade, quantity, post-supply) and their accounting treatment.

▪ Documentation of additional consideration, if any, beyond the invoice price.

▪ Proof of actual consideration received versus declared value.

▪ Benchmarking data for similar transactions between unrelated parties.

◦ Example: "The transaction in question involved a sale to [Related Party Name] (Annexure A-5, shareholder agreement). The sale price of [Product] was [Amount] per unit (Annexure A-6, invoice). A post-supply discount of [X%] was offered, linked to [specific condition], which was reflected in the credit note issued on [Date] (Annexure A-7, credit note and policy). This discount is verifiable from the Appellant's books of account (Annexure A-8, ledger extracts)."

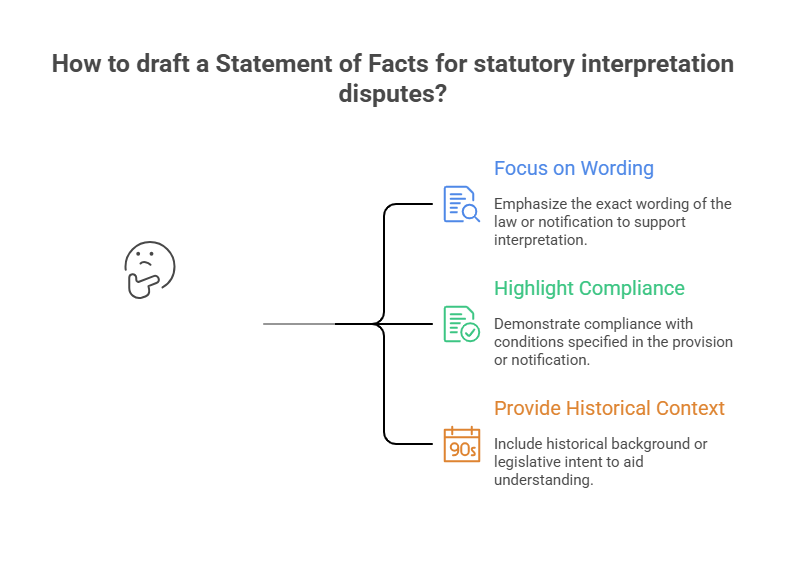

3. For Interpretation of Statutory Provisions / Applicability of Notifications Disputes:

◦ Focus: Specific wording of the law/notification, underlying intent, effective date, conditions/provisos, historical context.

◦ Key Factual Elements:

▪ Exact wording of the statutory provision or notification in dispute.

▪ Dates of relevant notifications, amendments, or clarifications and their applicability.

▪ Facts demonstrating compliance or non-compliance with conditions specified in the provision/notification.

▪ Historical background or legislative intent (if relevant and documented).

▪ Any departmental circulars, instructions, or trade notices.

◦ Example: "The Appellant's activity of [Activity Description] falls under Entry No. [X] of Notification No. [Y] dated [Date] (Annexure A-9, copy of notification). This notification grants an exemption subject to the condition that [Condition]. The Appellant has consistently fulfilled this condition by [Proof of compliance] (Annexure A-10, supporting documents)."

4. For Refund Issues:

◦ Focus: Eligibility for refund, amount claimed, documentary proof, adherence to timelines, inverted duty structure, export without payment of tax.

◦ Key Factual Elements:

▪ Category of refund claimed (e.g., inverted duty structure, export, deemed export).

▪ Details of the tax paid for which refund is sought (e.g., ITC accumulation, export turnover).

▪ Documentary evidence of tax payment, export documents (shipping bills, BRCs), input/output invoices.

▪ Proof of non-utilisation of ITC, if applicable.

▪ Application date for refund and any delays in processing.

▪ Comparison of input and output tax rates (for inverted duty structure).

◦ Example: "The Appellant is an exporter of [Goods] without payment of tax under LUT (Annexure A-11, LUT copy). Total exports for the period [Month/Quarter] amounted to [Amount] (Annexure A-12, export invoices). Accumulated Input Tax Credit for this period was [Amount] (Annexure A-13, GSTR-3B filings). The refund application in FORM GST RFD-01 was filed on [Date] (Annexure A-14, application copy) within the stipulated timeline.

IV. Best Practices in Tax Litigation for "Statement of Facts":

Beyond the structural and content requirements, several best practices derived from general tax litigation and GSTAT's specific context should be applied:

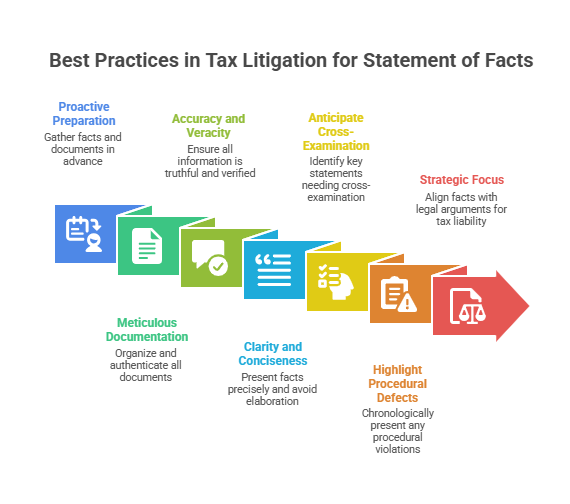

1. Proactive Preparation: Keeping "Facts, Grounds, Prayer and Forms ready" well in advance is essential to avoid last-minute rushes and ensure compliance with strict statutory timelines for appeal filing.

2. Meticulous Documentation and Evidence Management:

◦ Completeness: Ensure all supporting documents are properly authenticated and organised. "Documentation is king".

◦ Admissibility: Documents relied upon must be admissible. Authenticated copies of all relied-upon documents must be provided.

◦ Marking System: Adhere strictly to the GSTAT's document marking system (Appellant's documents as 'A' series, Respondent's as 'B' series, Tribunal's exhibits as 'C' series). This "systematic and organized approach" facilitates comprehensive case review.

◦ Affidavits: When evidence is presented via affidavit (Rule 46, Chapter X), ensure it conforms to Order XIX, Rule 3 of CPC, primarily limiting content to personal knowledge. For illiterate/visually challenged deponents, GSTAT FORM-05 is required for certification.

3. Accuracy and Veracity: The appeal form and pleadings must bear the authorised representative's name and signature, and the party must sign a "verification under oath," with the AR certifying documents as true copies. This ensures the veracity and authenticity of the submitted documents.

4. Clarity and Conciseness: Present facts precisely without unnecessary elaboration. The rules mandate "concise" and "numbered grounds" in Rule 20. Avoiding generic allegations is critical.

5. Anticipate Cross-Examination Needs: For cases heavily reliant on third-party statements, the "Statement of Facts" should clearly identify these foundational statements. While GSTAT Rule 46 allows for cross-examination by the Tribunal "in the interest of natural justice" and adopts CPC provisions for witnesses, the rules are "silent on key procedural aspects" like a party's right to request cross-examination if denied by lower authorities. A well-structured "Statement of Facts" highlighting these dependencies will enable the Tribunal to appreciate the need for cross-examination.

6. Highlight Procedural Defects: If the impugned order or previous proceedings suffered from violations of natural justice (e.g., denial of hearing, non-supply of relied-upon documents, lack of reasoned order), the "Statement of Facts" should chronologically present these instances as factual breaches leading to the current appeal.

7. Strategic Focus: Remember that GSTAT is concerned with determining the "correct tax liability". Present facts that directly support your legal arguments towards this objective.

By adhering to these principles and guidelines, practitioners can construct a robust and compelling "Statement of Facts" that effectively navigates the GSTAT's procedural framework, leveraging its design for efficient, transparent, and expert dispute resolution.

GST on Bakery Items | GST on Dry Fruits | Legal Name of Business in GST | GST Registration Search by Name | Biscuit GST Rate

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified