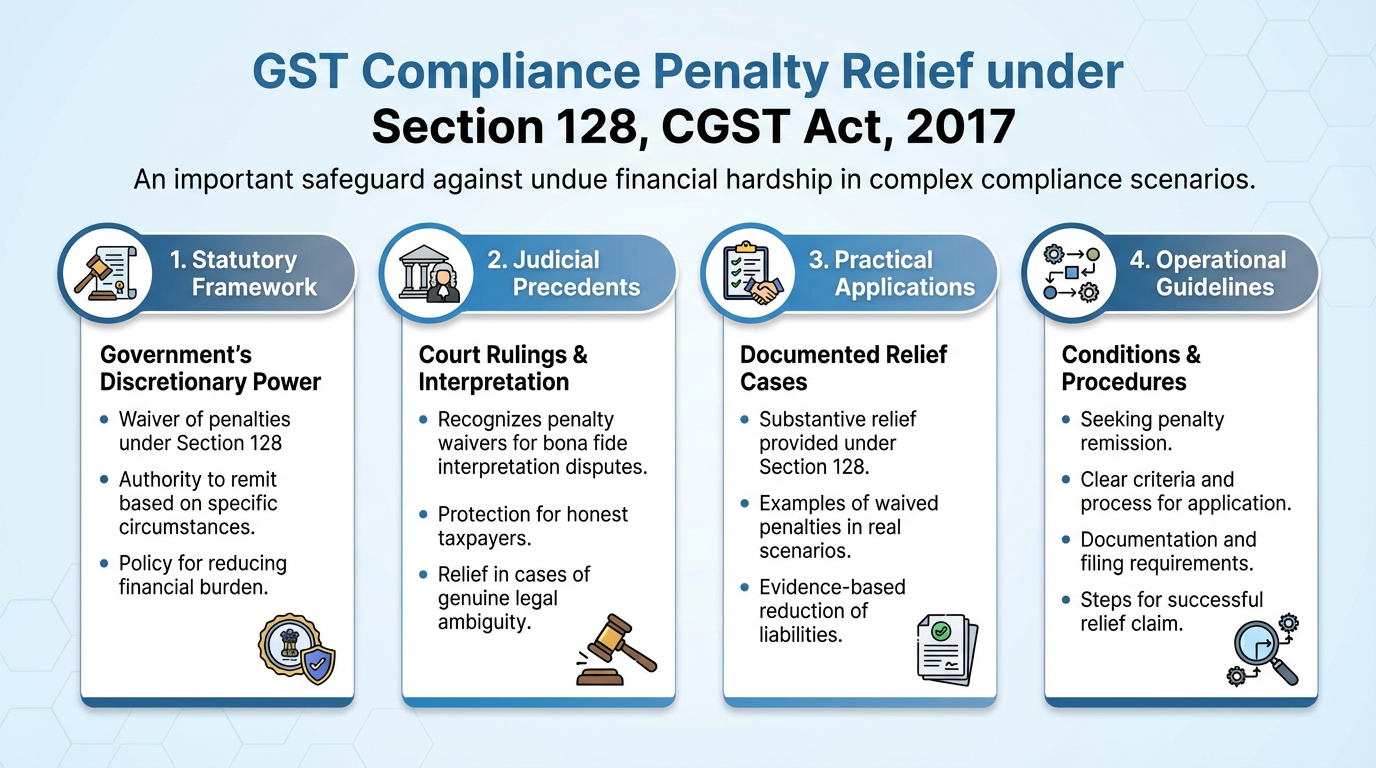

Unlocking Section 128: How the Government Can Waive Your GST Penalties and Late Fees

Introduction: A Glimmer of Hope for Taxpayers

For many taxpayers, the prospect of incurring penalties and late fees for non-compliance under the Goods and Services Tax (GST) regime is a source of significant anxiety. The complexities of the law can sometimes lead to unintentional errors, resulting in financial repercussions. However, there is a glimmer of hope within the GST framework itself. Section 128 of the Central Goods and Services Tax (CGST) Act, 2017, is a significant but often overlooked provision that grants the government the power to provide relief from these very penalties.

This article explores the scope of Section 128, examining how this power has been used in practice to offer tangible benefits to taxpayers. We will also discuss key principles established by the courts that support the waiver of penalties, particularly under mitigating circumstances like genuine interpretational disputes.

1. The Core Provision: Understanding the Government's Power to Waive

What is Section 128?

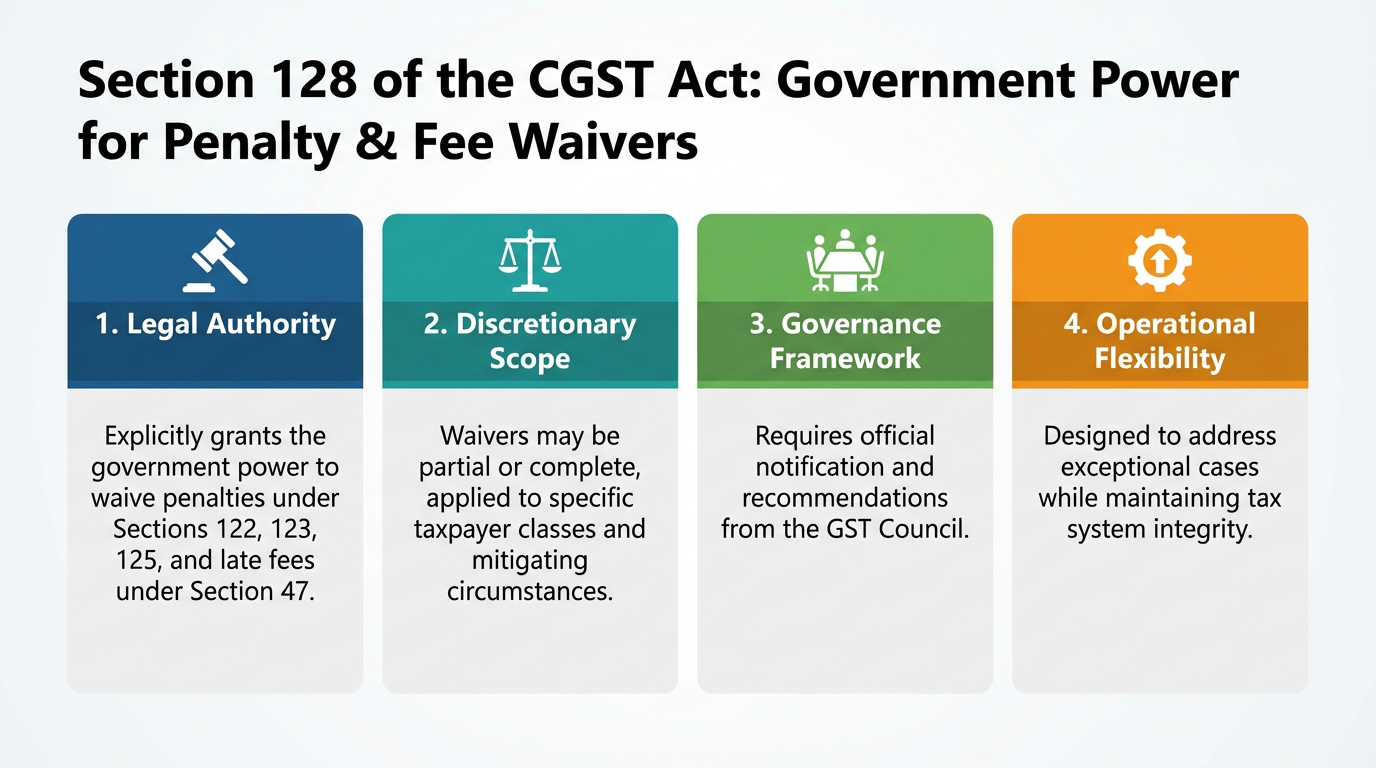

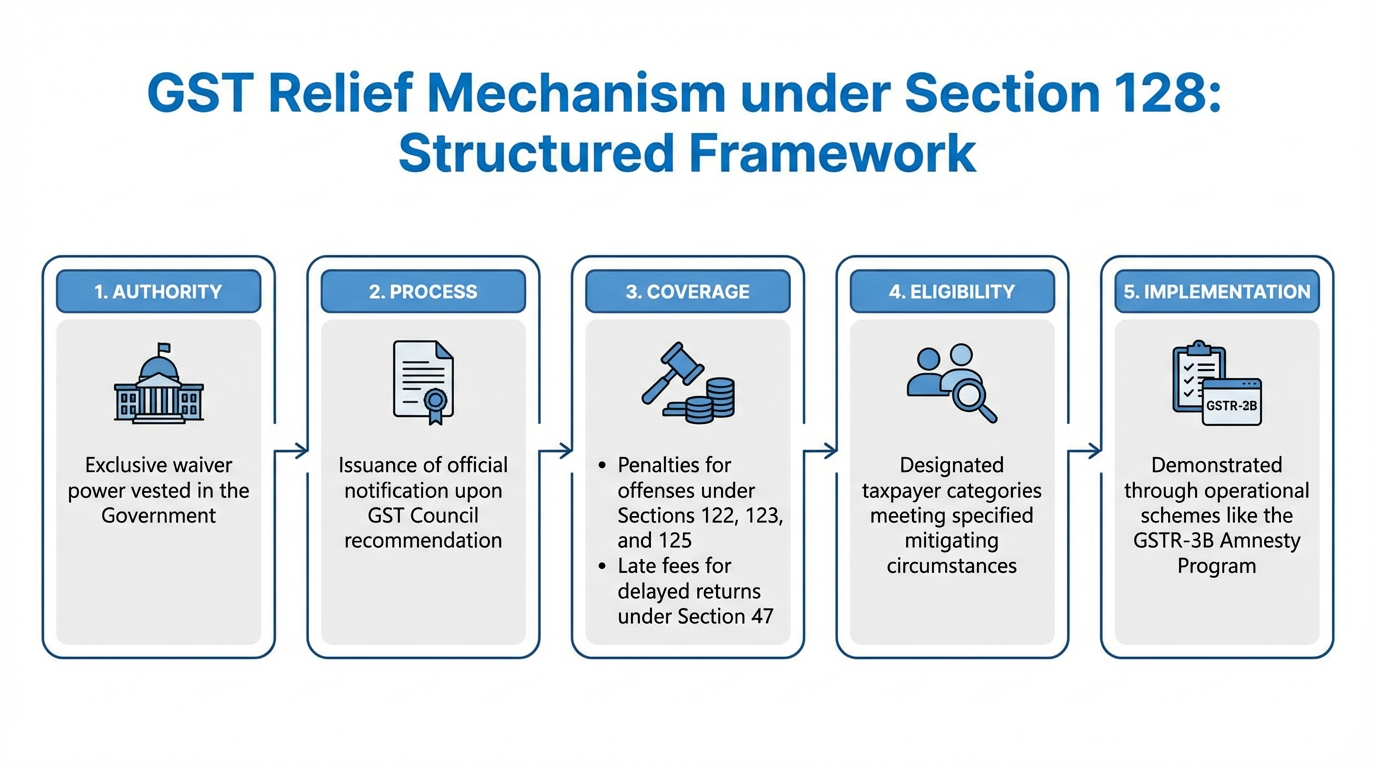

At the heart of the government's ability to grant relief is Section 128 of the CGST Act. The provision is direct and empowering:

Section 128. Power to waive penalty or fee or both.-

The Government may, by notification, waive in part or full, any penalty referred to in section 122 or section 123 or section 125 or any late fee referred to in section 47 for such class of taxpayers and under such mitigating circumstances as may be specified therein on the recommendations of the Council.

This section establishes a clear mechanism for providing relief. Let's break down its key components:

• Who can waive: The Government.

• How: Through an official notification.

• On whose recommendation: The GST Council.

• What can be waived: Penalties under key sections like Section 122 (for a wide range of offenses such as supplying goods without an invoice), Section 123 (for failing to furnish information returns), and Section 125 (a general penalty for contravening any provision where no specific penalty is prescribed), as well as late fees for delayed return filing under Section 47.

• For whom: A specific, defined "class of taxpayers."

• Under what conditions: For specified "mitigating circumstances."

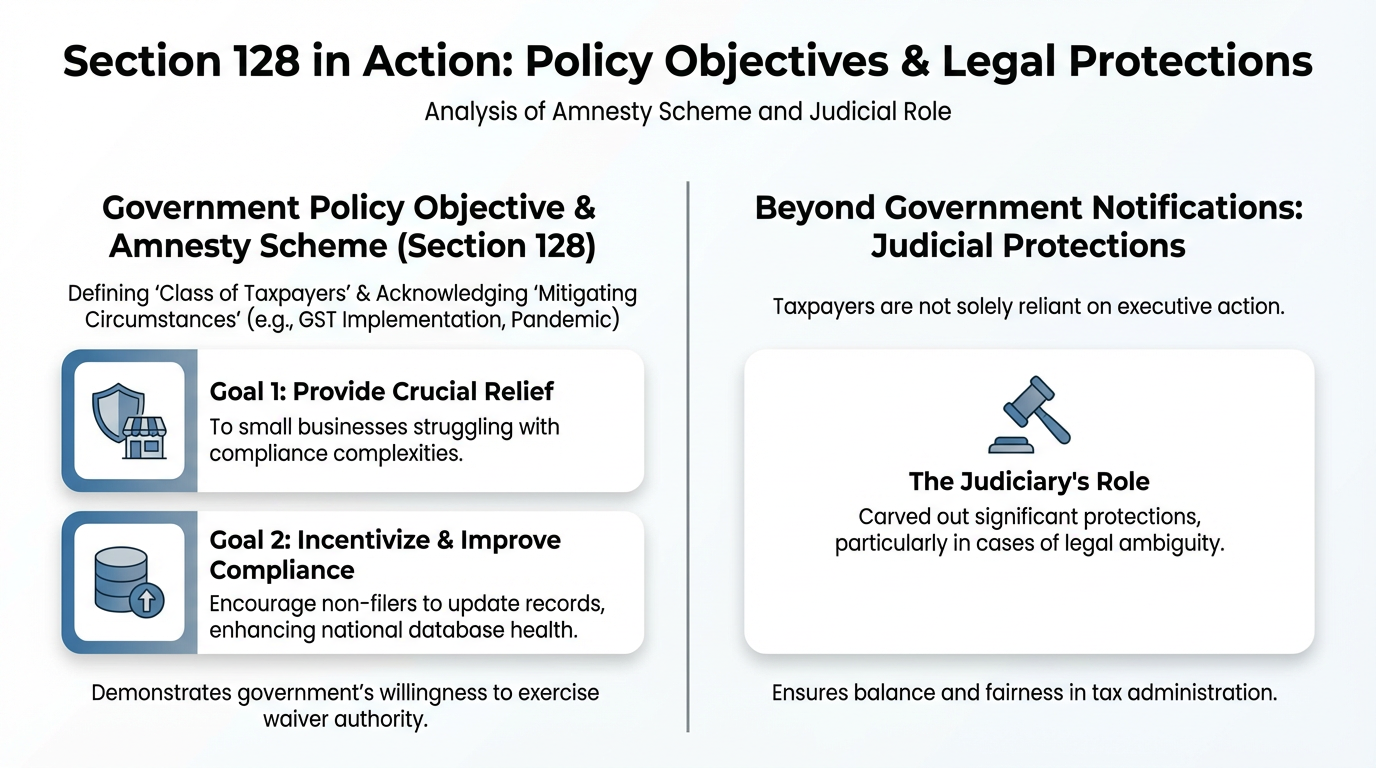

While the text of Section 128 provides the legal authority, its real-world impact is best understood through its practical application, such as the government's GSTR-3B Amnesty Scheme.

2. Waiver in Action: The GSTR-3B Amnesty Scheme

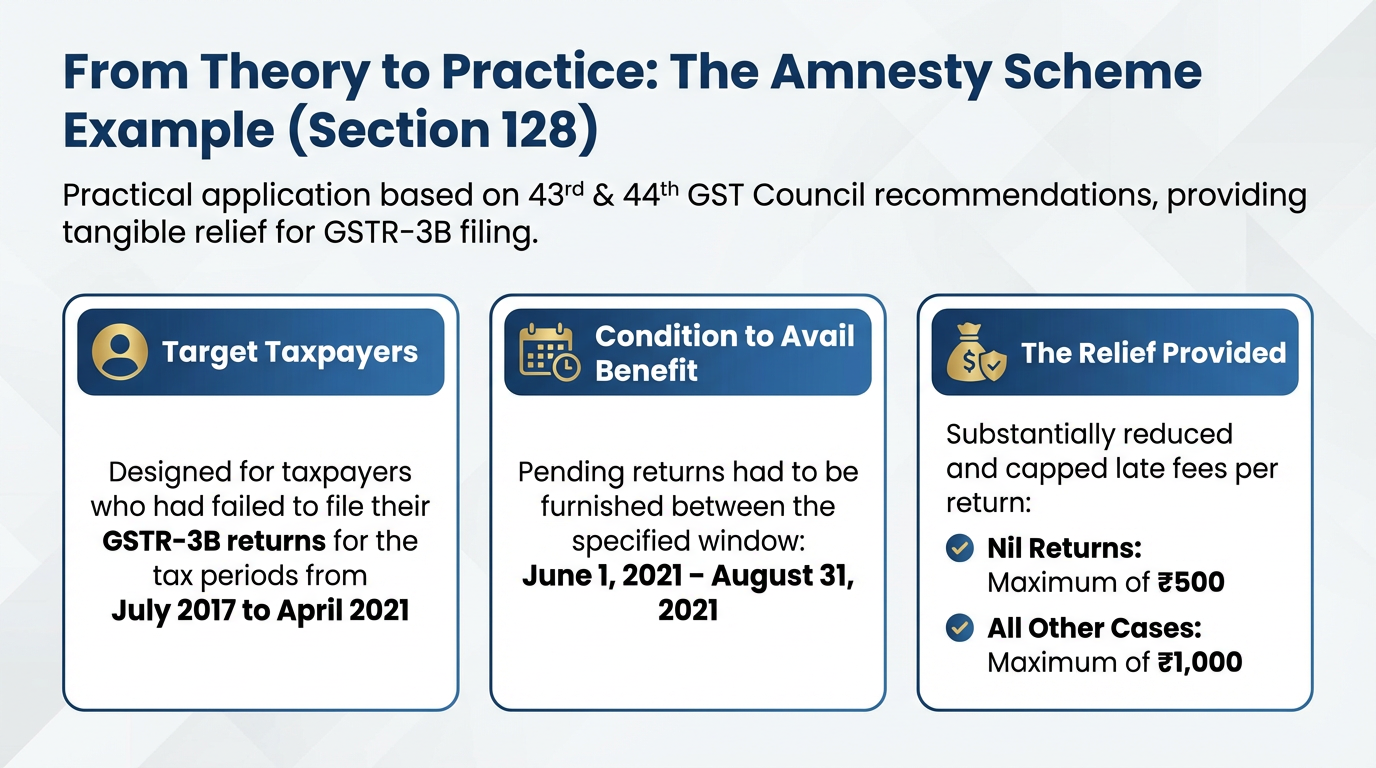

From Theory to Practice: The Amnesty Scheme Example

The power granted by Section 128 is not merely theoretical; it has been actively used to provide tangible relief to taxpayers. A prime example is the Amnesty Scheme for GSTR-3B filing, which was introduced following the recommendations of the 43rd and 44th GST Council meetings.

The scheme provided the following relief:

• Target Taxpayers: It was designed for taxpayers who had failed to file their GSTR-3B returns for the tax periods from July 2017 to April 2021.

• Condition: To avail the benefit, these pending returns had to be furnished between June 1, 2021, and August 31, 2021.

• The Relief Provided: The late fees for these delayed filings were substantially reduced, capped at a maximum of ₹500 per return for nil returns and ₹1,000 per return for all other cases.

This scheme perfectly illustrates Section 128 in action. Beyond the technical mechanics, it reveals an explicit policy objective. By defining a "class of taxpayers" (non-filers for a particular period) and acknowledging "mitigating circumstances" (likely the initial challenges of GST implementation and the economic disruptions caused by the pandemic), the government aimed to achieve two goals. First, it provided crucial relief to small businesses struggling with compliance complexities. Second, it incentivised non-filers to update their records, thereby improving the overall health and accuracy of the national compliance database.

This amnesty scheme demonstrates the government's willingness to exercise its waiver authority. However, taxpayers are not solely reliant on government notifications; the judiciary has also carved out significant protections, particularly in cases of legal ambiguity.

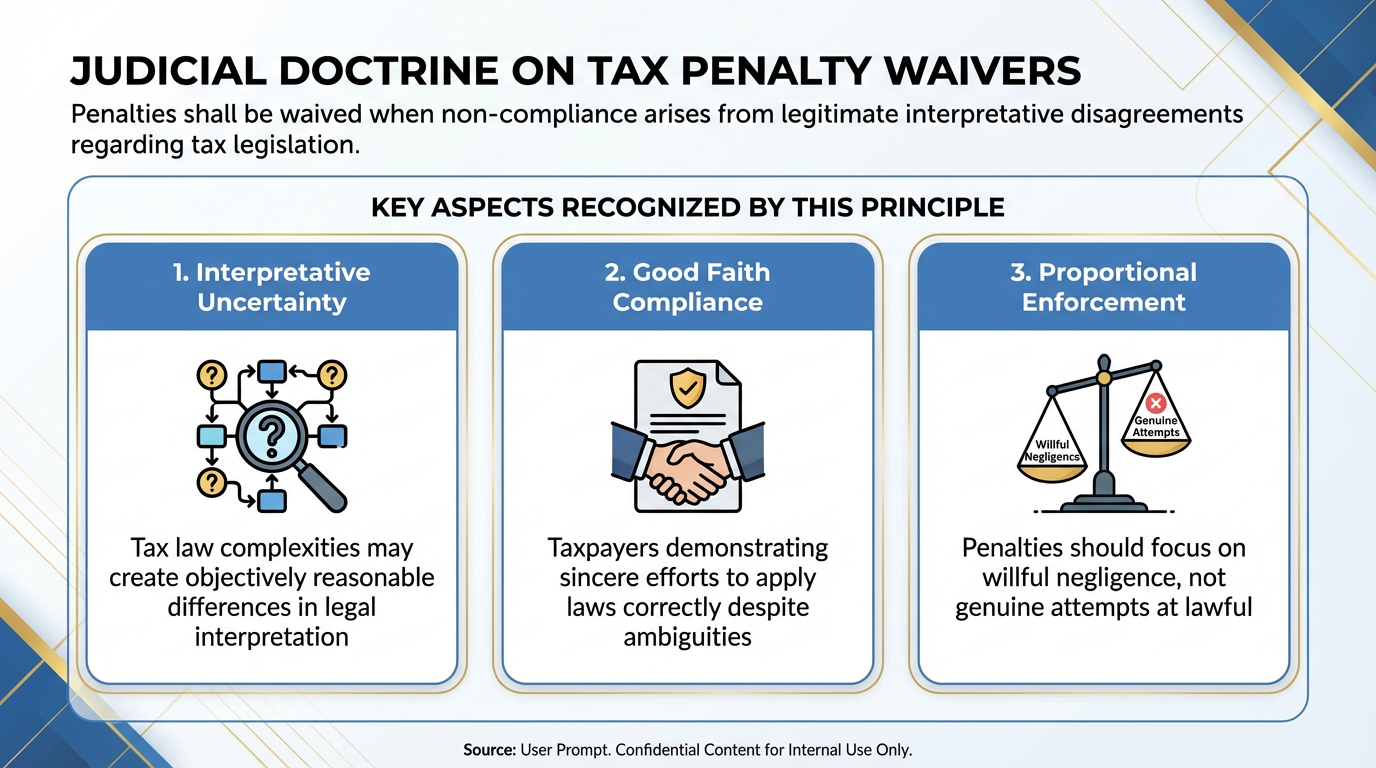

3. Judicial Backing: When Courts Say 'No Penalty'

When Interpretation is the Issue, Penalties Shouldn't Apply

The judiciary has consistently reinforced the principle that penalties should not be imposed when non-compliance stems from a genuine dispute over the interpretation of tax laws. Such ambiguity is often considered a valid mitigating circumstance.

The Supreme Court, in the case of International Merch. Co. LLC vs Commissioner of Service Tax, Delhi [2022 (67) GSTL 129 (S.C.)], made a crucial observation regarding the imposition of penalties in such situations. In paragraph 25 of its judgment, the Court stated:

“As far as the penalty is concerned, we are of the considered view that there was no warrant for the imposition of the penalty as the dispute in the present case essentially turned on the interpretation of the statutory provisions and their inter-play with the circular issued by the CBEC.”

The Supreme Court's reasoning effectively categorises a genuine 'dispute of interpretation' as a powerful 'mitigating circumstance,' aligning perfectly with the spirit and intent of Section 128. This view is further supported by the Madras High Court in Principal Commissioner of GST & Centnal Excise vs C Kamalakannan [2018 (18) GSTL 589 (Mad.)]. The court held that the extended period of limitation for levying penalties cannot be invoked when there is scope for doubt or when two different interpretations of a rule exist, even within the tax department itself. This judicial stance protects taxpayers from penalties when acting in good faith amidst legal uncertainty.

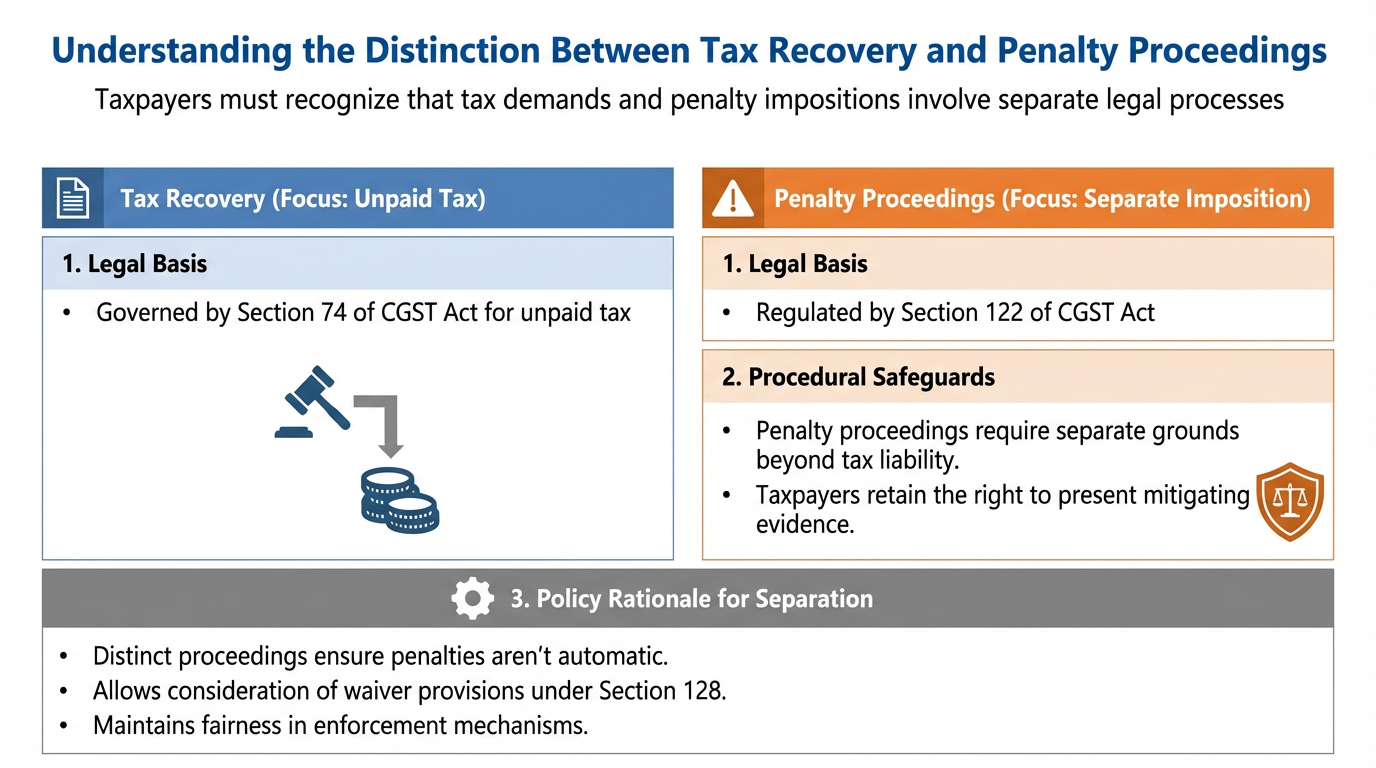

4. A Crucial Distinction: Penalty vs. Tax Recovery

Understanding the Difference Between Penalty and Tax Recovery Proceedings

It is also vital for taxpayers to understand that a demand for tax does not automatically trigger a penalty. The Kerala High Court, in the case of Radhakrishna Textiles vs Superintendent of Central Taxes and Central Excise [2021 (45) GSTL 130 (Ker.)], clarified this distinction.

The court held that proceedings under Section 122 of the CGST Act (for imposing a penalty) are separate and distinct from proceedings under Section 74 (for recovering unpaid tax). This distinction is significant because it means that the grounds for demanding tax and the grounds for imposing a penalty are not the same. The imposition of a penalty is a separate action, and during this process, the taxpayer has the right to present mitigating factors and argue why a penalty is not warranted. This separation is crucial, as it confirms that penalty proceedings are not automatic. It provides a distinct forum for the taxpayer to present evidence of mitigating circumstances—the very concept that underpins the government's waiver power in Section 128.

Conclusion: A Path Towards Fairer Compliance

Section 128 provides the government with a clear statutory tool to grant relief, and schemes like the GSTR-3B amnesty demonstrate its practical application. However, the true landscape of taxpayer protection is shaped by the interplay between executive power and judicial wisdom. The courts have consistently held that penalties are unwarranted in cases of genuine legal ambiguity, thereby establishing a strong defensive principle for taxpayers. This transforms the concept of "mitigating circumstances" from a passive hope for government notification into an active, arguable defence. Thus, while Section 128 is a top-down exercise of government power, judicial precedents have forged a taxpayer-centric framework that can be used proactively to challenge penalties, establishing a more equitable path toward compliance.

Given the clear intent of the law and the supportive stance of the courts, what other 'mitigating circumstances' should the GST Council consider to ease the compliance burden on honest taxpayers further?

Need for GST in India | Powers of GST Officers | UQC Code in GST | Cookies New GST Rate | GST Slab for Bakery Products

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified