How to Use the Intention of the Legislature to Your Advantage in Assessments, Appeals, and Litigation

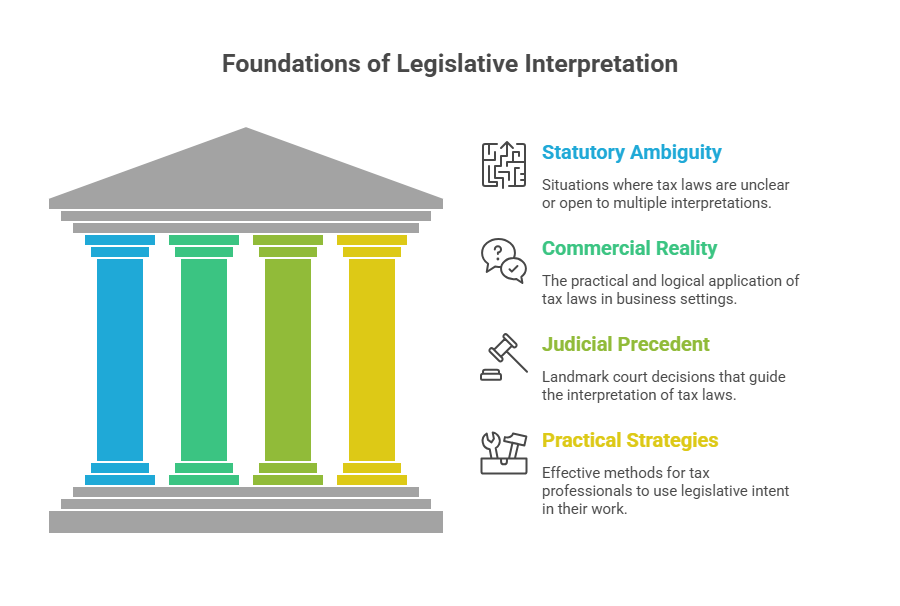

As a tax consultant or CFO, you often face show-cause notices or assessment orders where the department stretches the meaning of a provision in a way that creates unexpected tax liability. Responding effectively to such GST notices and departmental proceedings often requires a strong understanding of statutory interpretation principles. The statutory language appears ambiguous, and the interpretation seems far removed from commercial reality. In such situations, understanding the intention of the legislature becomes your strongest shield.

Indian courts have consistently held that when the meaning of a provision is unclear or capable of multiple interpretations, recourse must be taken to the true intent of the legislature. These principles frequently become decisive during GST appeals and revision proceedings, where taxpayers challenge adverse interpretations adopted by authorities. This article distils the key principles, landmark rulings, and practical strategies every tax professional must know.

Understanding Legislative Intent in Statutory Interpretation

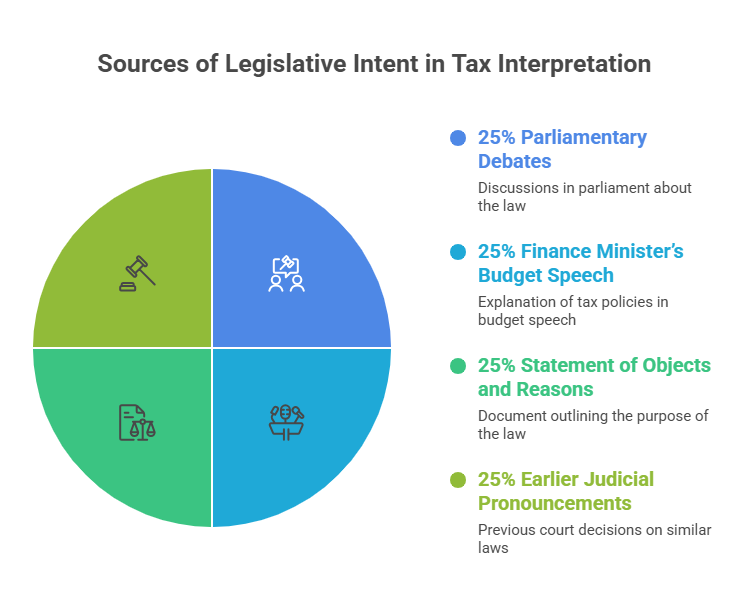

When a taxing statute is ambiguous, courts look beyond the bare text to ascertain the legislature’s purpose. This intent can be gathered from:

-

Parliamentary debates

-

Finance Minister’s Budget Speech

-

Statement of Objects and Reasons

-

Earlier judicial pronouncements on similar provisions

However, in taxing statutes, reliance on legislative intent has limited applicability. The language of the Act remains supreme, and courts are reluctant to stretch provisions to impose higher taxes.

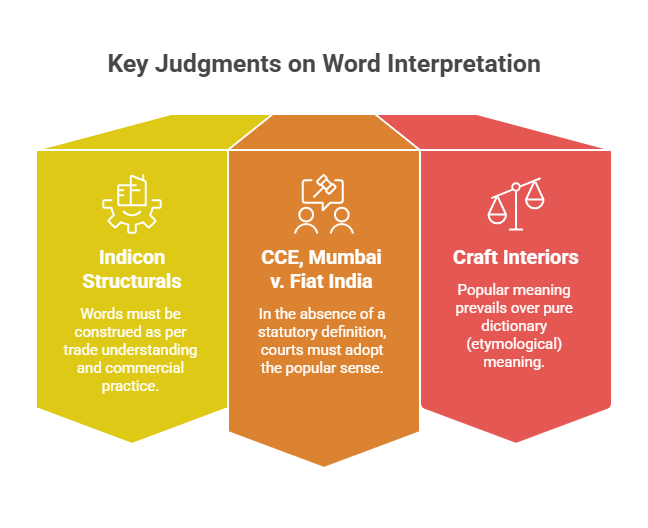

Popular Sense and Commercial Parlance Test

One of the most important principles in tax interpretation is that words and expressions not defined in the statute must be understood in their popular sense — the meaning attributed by people conversant with the subject in commercial and trade circles.

Key Judgements:

-

Indicon Structurals (P.) Ltd. v. CCE, Chennai, (2006) 4 SCC 786: Words must be construed as per trade understanding and commercial practice.

-

CCE, Mumbai v. Fiat India Pvt. Ltd., 2012 (283) ELT 161 (SC): In the absence of a statutory definition, courts must adopt the popular sense.

-

Craft Interiors Pvt. Ltd. v. CCE, Bangalore, 2006 (203) ELT 529 (SC): Popular meaning prevails over pure dictionary (etymological) meaning.

“While construing any word, one must see both the dictionary meaning and popular meaning which the word had attained in common parlance as popular meaning overpowers etymological meaning.”

Why this is crucial: Departmental officers often apply scientific or technical meanings. Countering with the “commercial parlance test” has helped taxpayers win many GST classification disputes, particularly where differing interpretations of tariff entries and product descriptions arise.

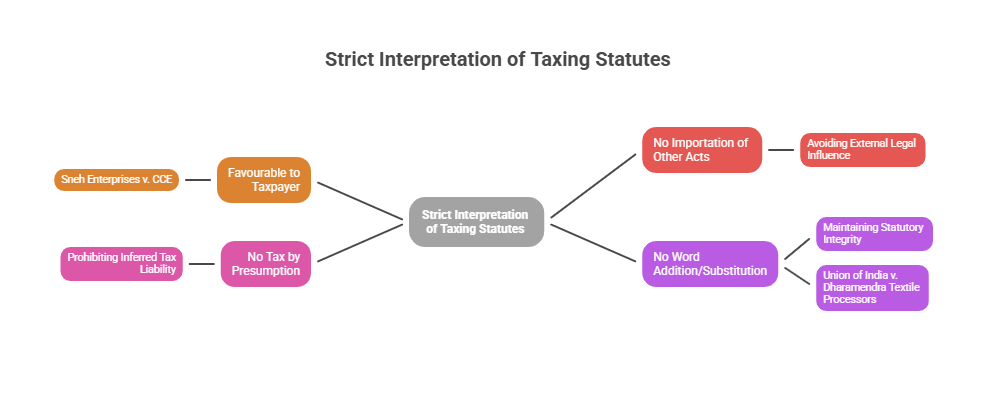

Strict Interpretation of Taxing Statutes – The Golden Rule

Taxing statutes must be interpreted strictly. Courts cannot create additional fiscal liability through liberal construction.

Important principles include:

-

If two interpretations are possible, the one favourable to the taxpayer must be adopted. (Sneh Enterprises v. CCE, 2006 (202) ELT (SC))

-

Provisions of other acts should not be imported to create tax liability.

-

No tax can be imposed by presumption, assumption, or inference.

-

Courts cannot add or substitute words to achieve what they perceive as the “spirit” of the law.

Quote from Supreme Court:

“It is not the economic results sought to be achieved… It is impermissible to add or substitute words so as to give meaning to the statute which maintains the spirit and intention of the legislature.” — Union of India v. Dharamendra Textile Processors

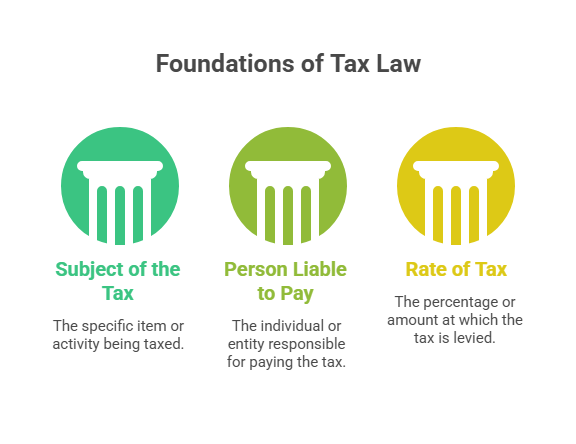

Three Essential Constituents of a Taxing Statute

Every taxing provision must clearly spell out three components:

-

Subject of the tax (what is being taxed)

-

Person liable to pay the tax

-

Rate at which tax is levied

If any of these elements suffers from real ambiguity and cannot be cured by reasonable construction, no tax can be levied until the defect is removed by the legislature.

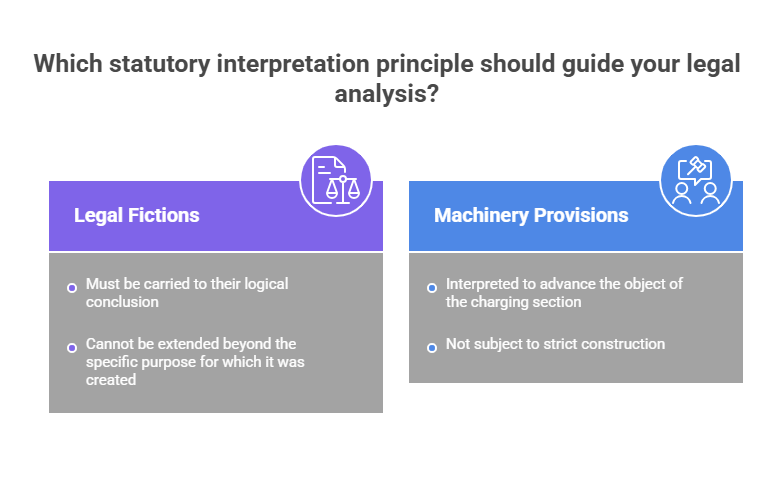

Legal Fictions and Machinery Provisions

-

Legal fictions created by the statute must be given full effect and carried to their logical conclusion (UOI v. Jalyan Udyog; Builders Association of India v. UOI).

-

However, a legal fiction cannot be extended beyond the specific purpose for which it was created.

-

Machinery provisions, though not subject to strict construction, must be interpreted to advance the object of the charging section and not defeat it.

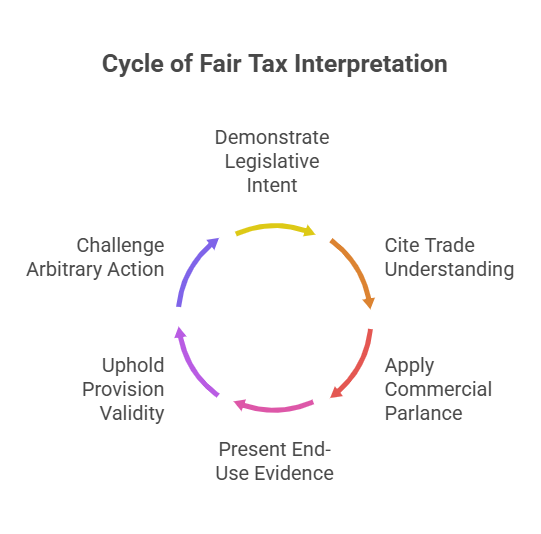

Practical Strategies for Tax Professionals

-

In Replies & Appeals: Always demonstrate how the department’s interpretation defeats legislative intent or commercial reality. Cite trade understanding and relevant judgments.

-

Classification Disputes: Heavily rely on the commercial parlance test and end-use evidence.

-

Ambiguous Provisions: Argue for the interpretation that favours the assessee and upholds the validity of the provision.

-

Show-cause Notices: Point out where the department is adding words or relying on presumptions not supported by the plain language. This becomes particularly important while responding to a GST demand notice issued under Rule 142 and Form DRC-01, where procedural and interpretational errors can significantly affect the outcome.

Intersection with Principles of Natural Justice

An interpretation that imposes tax through strained construction or by ignoring legislative intent often results in arbitrary action. Such readings can successfully be challenged on grounds of violation of Article 14 and principles of natural justice, as they lead to unfair and unreasonable demands.

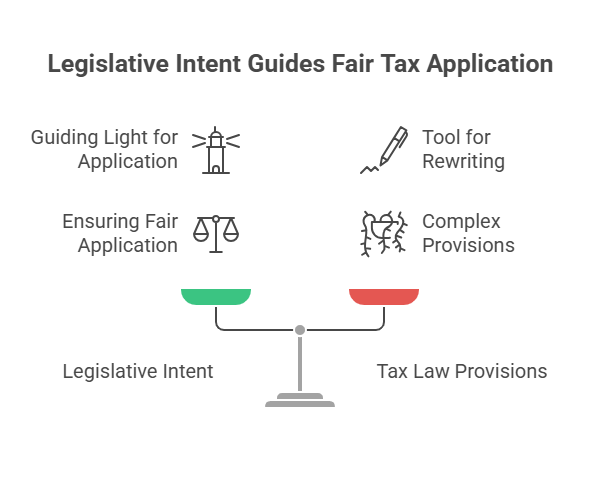

Key Takeaway

Legislative intent is not a tool to rewrite tax laws but a guiding light to ensure provisions are applied fairly and in accordance with commercial sense. In an era of complex GST and income tax provisions, the ability to discern and effectively argue the true intention of the legislature can transform a losing case into a winning one.

Thought-Provoking Question:

In your experience, which provision in the current tax laws is most prone to misinterpretation by the department, defeating the very intent of the legislature?

Share your views in the comments. Such insights often help fellow professionals strengthen their positions in disputes.

Authored in the spirit of fair taxation, procedural justice, and upholding the rule of law.

Legal Corner | Empowering Tax Professionals with Judicial Wisdom

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified