Assessment Under Section 64 of CGST Act: Summary Assessment Explained

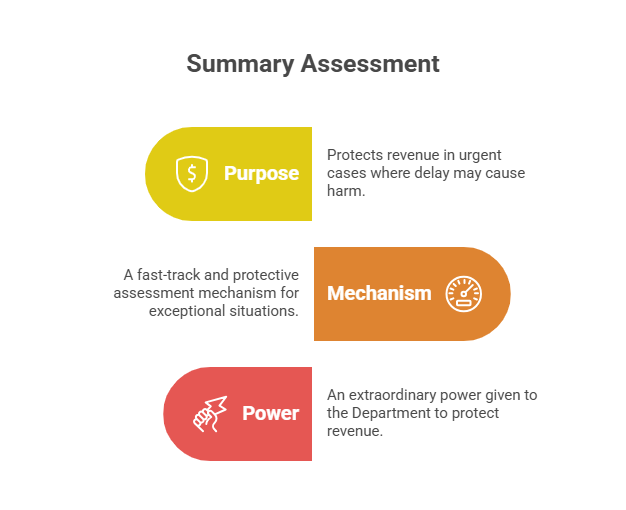

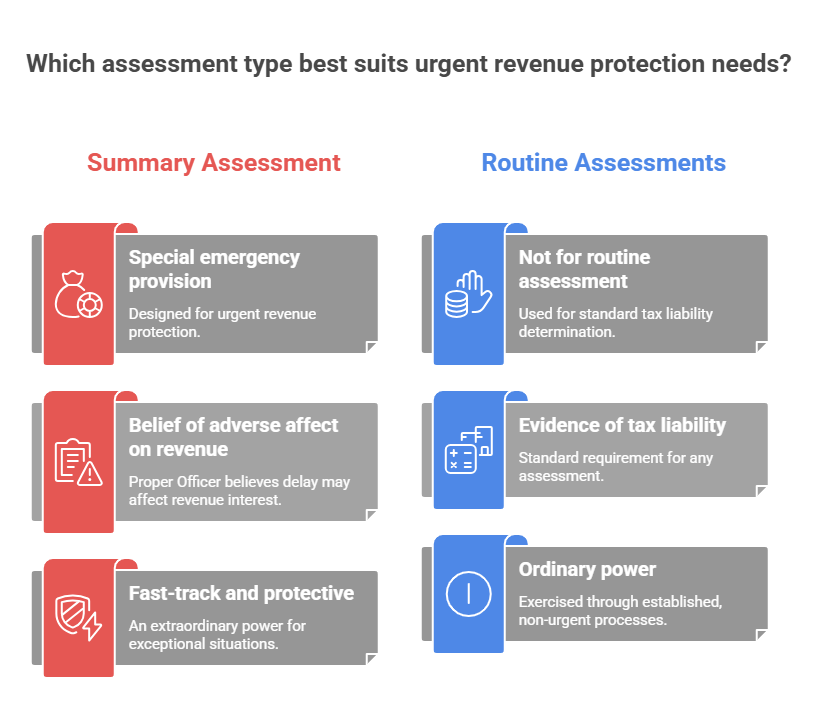

Section 64 of the CGST Act is an extraordinary power given to the Department to protect revenue in urgent cases. It is used where the Proper Officer has sufficient grounds to believe that any delay in assessment may adversely affect the interest of revenue. In simple words, it is a fast-track and protective assessment mechanism meant for exceptional situations.

When summary assessment under Section 64 can be initiated

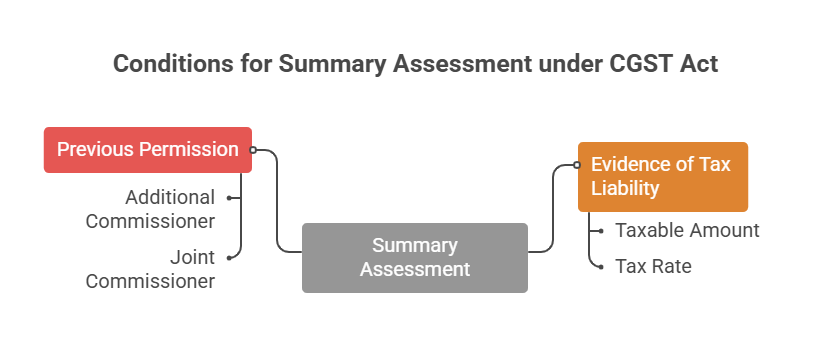

Summary assessment can be initiated only when:

- The Proper Officer has evidence showing tax liability, and

- Previous permission of the Additional Commissioner or Joint Commissioner is obtained.

Thus, it is not an ordinary power and cannot be exercised casually. The requirement of prior sanction from a senior officer acts as a safeguard against misuse.

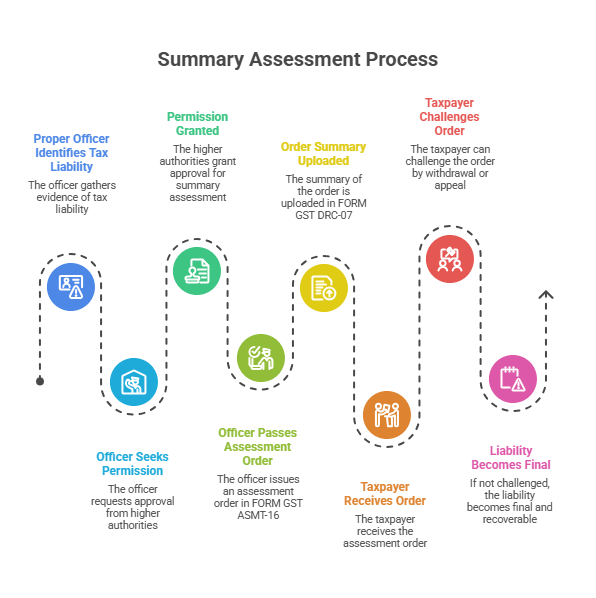

How the Section 64 summary assessment process works

Once approval is taken, the Proper Officer may pass the assessment order in FORM GST ASMT-16. The summary of this order is uploaded in FORM GST DRC-07, which also operates as a demand order and may trigger recovery proceedings if not challenged in time.

Understanding deeming fiction for goods under Section 64

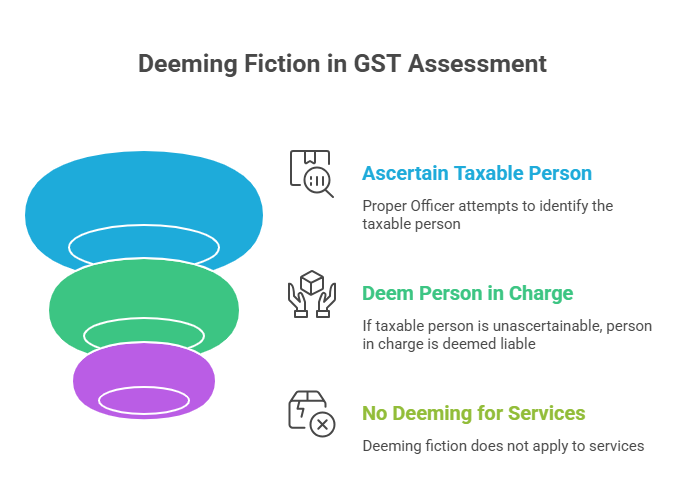

If the actual taxable person is not ascertainable in case of supply of goods, the person in charge of the goods may be deemed to be the taxable person liable to pay tax. However, no such deemed fiction exists for services. This distinction is critical in cases involving transit goods, unaccounted stock, or third-party carriers.

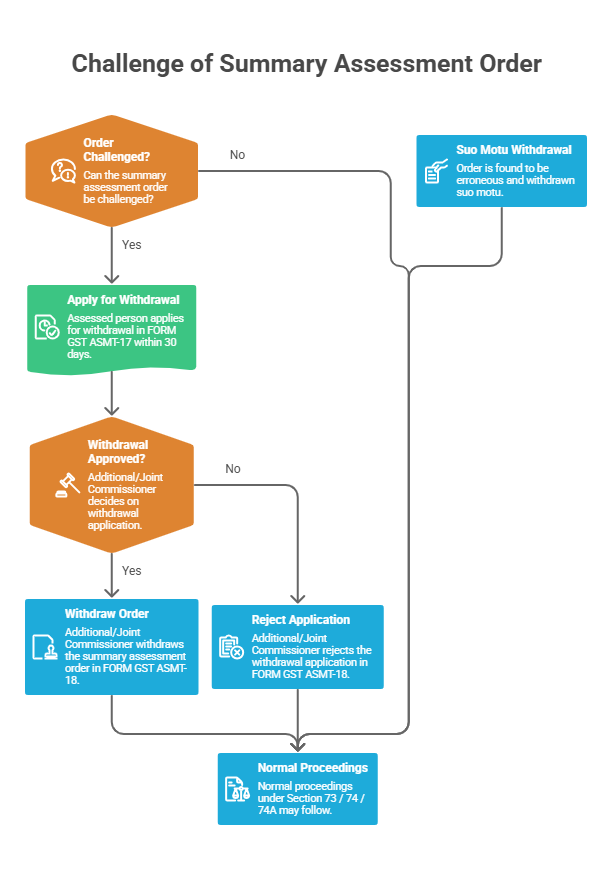

How to challenge a Section 64 summary assessment order

Yes. The assessed person may apply for withdrawal of the summary assessment order using FORM GST ASMT-17 within 30 days from the date of the order.

- The Additional/Joint Commissioner may withdraw or reject the application through FORM GST ASMT-18.

- Suo motu withdrawal is also possible if the order is found to be erroneous — after which normal proceedings under Section 73 / 74 / 74A may follow.

Why businesses should take Section 64 proceedings seriously

Because summary assessment is generally ex parte — meaning the initial order can be passed without prior hearing to the taxpayer. If the taxpayer neither succeeds in withdrawal nor files an appeal within time, the liability may become final and recoverable. Failure to respond within prescribed timelines may also expose businesses to additional GST penalties and legal consequences.

This makes it essential for businesses to monitor GST portal notifications closely. An ASMT-16 order overlooked can quickly translate into a DRC-07 demand with recovery consequences, including bank account attachment. Ignoring important GST notices and assessment orders can lead to serious recovery consequences, making it crucial for taxpayers to understand different types of GST notices under GST and respond within prescribed timelines.

Where Section 64 fits in the GST assessment framework

Section 64 is fundamentally different from other forms of GST assessment:

- Self-assessment (Section 59) — taxpayer assesses and pays on their own.

- Provisional assessment (Section 60) — used when the taxpayer cannot determine the value or applicable rate.

- Scrutiny assessment (Section 61) — officer scrutinises filed returns for discrepancies.

- Best judgement assessment (Section 62) — used when returns are not filed despite notice.

- Summary assessment (Section 64) — an emergency provision designed only for urgent revenue protection and not for routine assessment.

Section 64 should be invoked only in genuine cases of urgency, and any order passed under it remains open to challenge through the ASMT-17 withdrawal route or by filing an appeal before the Appellate Authority under Section 107 of the CGST Act. Businesses should also understand how GST audits and assessments differ under various provisions of the CGST Act to ensure proper compliance and preparedness during proceedings.

appeals and revision under gst | gst late fees | gstr 1 late fees | gstat appeal format | section 47 of gst | section 74A

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified