GST Act Section 122: Offences and Penalties Explained with Case Law

Based on the sources provided, Section 122 of the CGST Act, 2017, is a pivotal provision within Chapter 19, which covers Offences and Penalties (Sections 122-138). This section specifies various offences that can be committed by a taxable person or any other person and prescribes the corresponding penalties. The term 'penalty' is generally understood as a liability in addition to tax, levied for deliberate violations of the law.

Penalty on a Taxable Person (Section 122(1))

A taxable person who commits any of the 21 specified offences shall be liable to pay a penalty equivalent to the higher of ₹10,000 or the amount of tax involved (e.g., tax evaded, ITC wrongly availed/utilised/passed on, or refund fraudulently claimed). The offences listed under this sub-section include, but are not limited to:

• Supplying goods or services without an invoice or issuing an incorrect/false invoice.

• Issuing an invoice or bill without an actual supply of goods or services, leading to wrongful availment of Input Tax Credit (ITC) or refund.

• Collecting tax but failing to deposit it with the government beyond three months from the due date.

• Failing to deduct or collect tax at source (TDS/TCS) or failing to deposit it with the government.

• Taking or utilising ITC without the actual receipt of goods or services.

• Fraudulently obtaining a refund.

• Failing to obtain registration despite being liable to do so.

• Transporting taxable goods without the cover of specified documents.

• Suppressing turnover to evade tax.

• Failing to maintain or retain required books of account.

• Tampering with or destroying material evidence or documents.

The Allahabad High Court, in M/s Metenere Ltd. vs. Union of India, has held that these offences can be bifurcated into those linked with an intention to evade tax (attracting a penalty of the tax amount or ₹10,000, whichever is higher) and those related to procedural non-compliance (attracting a penalty of ₹10,000).

Penalty on Beneficiaries and Instigators (Section 122(1A))

Introduced effective from 1 January 2021, this sub-section targets any person who is not just a beneficiary but also the instigator of a fraudulent transaction. Any person who retains the benefit of transactions covered under clauses (i) [supply without invoice], (ii) [invoice without supply], (vii) [wrongful ITC availment/utilisation], or (ix) [fraudulent refund] of sub-section (1), and at whose instance such a transaction is conducted, shall be liable to a penalty equal to the tax evaded or ITC availed/passed on. The Bombay High Court in Shantanu Sanjay Hundekari v UOI held that this provision necessarily applies to a "taxable person".

Penalty on E-commerce Operators (Section 122(1B))

Effective from 1 October 2023, a specific penalty has been introduced for any electronic commerce operator who is liable to collect tax at source under section 52 and commits certain offences. The penalty is ₹10,000 or an amount equivalent to the tax involved, whichever is higher. The specified offences include:

• Allowing an unregistered person (who is not exempt from registration) to make supplies through its platform.

• Allowing a person who is not eligible to make inter-State supplies to do so through its platform.

• Failing to furnish correct details in the statement (FORM GSTR-8) for supplies made by a person exempted from registration.

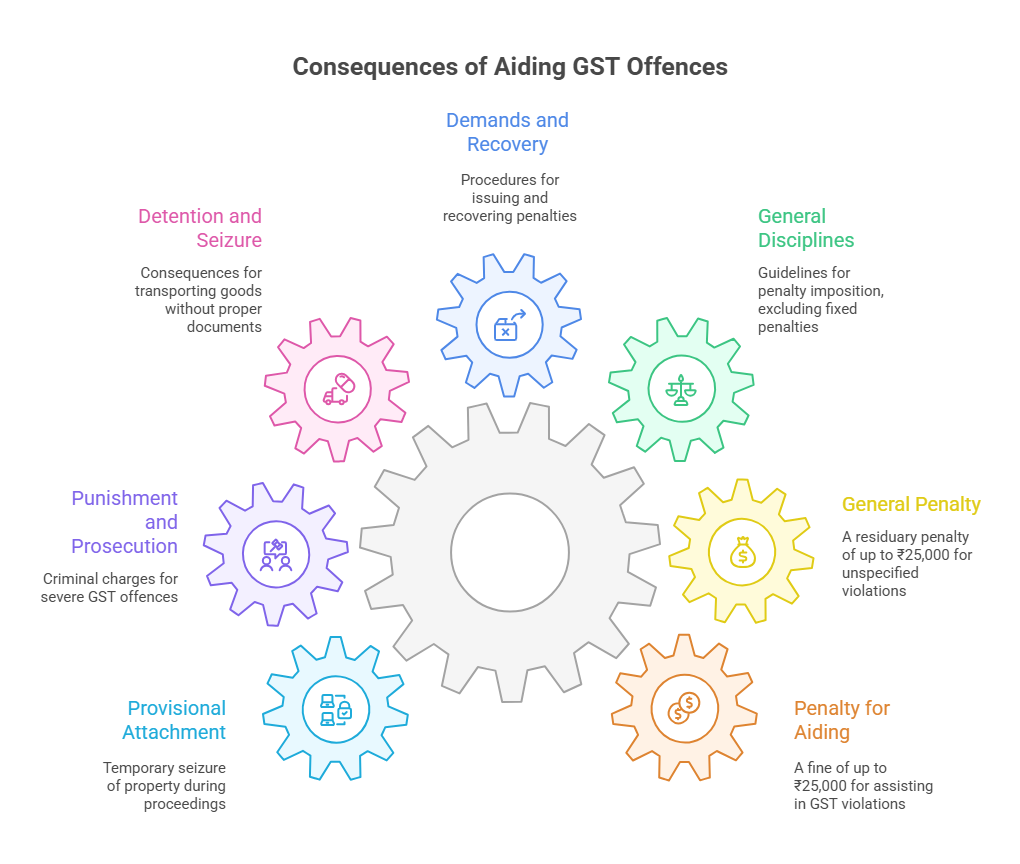

Penalty for Aiding or Abetting (Section 122(3))

This provision imposes a penalty on any person who is not directly the taxable person but assists in the contravention of the law. Any person who commits the following shall be liable to a penalty that may extend to ₹25,000:

• Aids or abets any of the 21 offences listed in sub-section (1).

• Deals with goods he knows are liable for confiscation.

• Is concerned with the supply of services he knows are in contravention of the Act.

• Fails to appear before an officer when summoned.

• Fails to issue a required invoice or fails to account for an invoice in his books.

Context within Chapter 19 (Offences and Penalties)

Section 122 is the primary provision for levying monetary penalties for a wide range of specific offences. It operates alongside other sections in the chapter that deal with more general or consequential actions:

• General Penalty (Section 125): This section acts as a residuary provision, imposing a penalty of up to ₹25,000 for any contravention of the Act or Rules for which no separate penalty is prescribed.

• General Disciplines (Section 126): This section provides guiding principles for penalty imposition, such as no penalty for minor breaches (tax involved is less than ₹5,000) or easily rectifiable errors without fraudulent intent. However, these disciplines do not apply where the penalty is a fixed sum or a fixed percentage, as is often the case under Section 122.

• Demands and Recovery: A notice for a penalty under Section 122 is served along with a summary in FORM GST DRC-01, and the final order is uploaded in FORM GST DRC-07.

• Detention, Seizure, and Confiscation (Sections 129 & 130): Transporting goods without proper documents, an offence under Section 122(1)(xiv), can lead to more severe consequences like detention and seizure under Section 129. Similarly, supplying goods with an intent to evade tax, an offence under Section 122, can result in the confiscation of those goods under Section 130.

• Punishment and Prosecution (Section 132): Certain severe offences listed in Section 122, such as issuing invoices without supply or fraudulently availing ITC, if they exceed specified monetary thresholds, can lead to criminal prosecution and imprisonment under Section 132.

• Provisional Attachment (Section 83): Proceedings under Chapter XV, which includes penalty imposition, can trigger the provisional attachment of property, including bank accounts, belonging to the taxable person or any person specified in Section 122(1A)

Need for GST in India | Powers of GST Officers | UQC Code in GST | GSTR 3B table 5 | DRC-01 format | Penalty for non GST registration

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified