Introduction: What is Rule 86B?

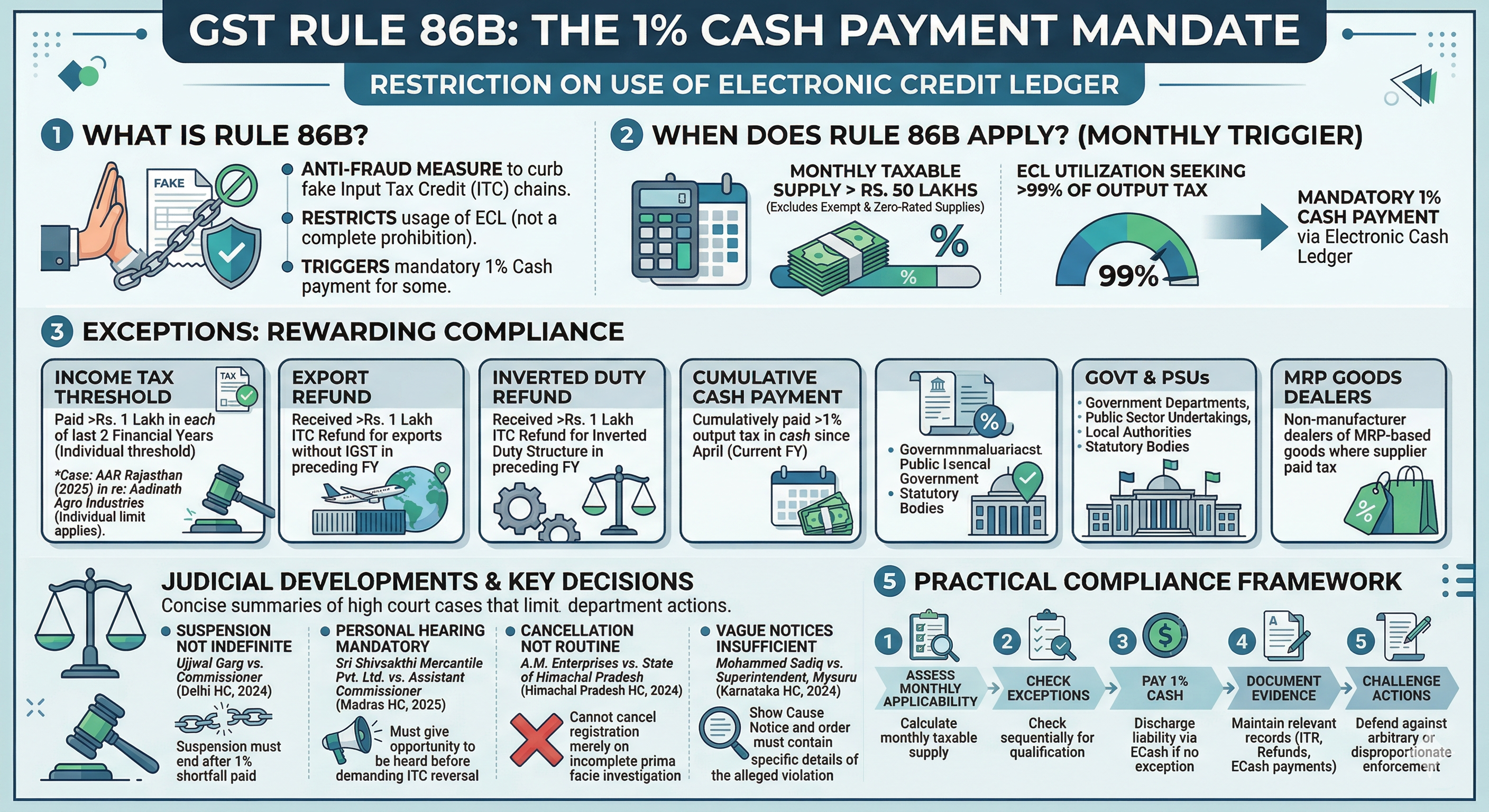

Rule 86B of the Central Goods and Services Tax Rules, 2017 (CGST Rules) was introduced with effect from 1st January 2021 by Notification No. 94/2020-Central Tax dated 22nd December 2020. It represents one of the more stringent anti-fraud measures introduced under the GST architecture, aimed squarely at curbing the menace of fake Input Tax Credit (ITC) chains that had caused significant revenue leakage to the exchequer.

The provision operates as a restriction — not a prohibition — on the use of amounts available in the Electronic Credit Ledger (ECL). Its operation is triggered when a registered person's taxable turnover (excluding exempt and zero-rated supplies) in a calendar month exceeds Rs. 50 Lakhs. In such cases, the registered person cannot utilise the ECL to discharge more than 99% of the output tax liability for that month. In plain terms, at least 1% of the output tax liability must be discharged through the Electronic Cash Ledger (ECash Ledger), i.e., from actual funds and not from accumulated ITC.

While conceptually straightforward, the Rule has generated significant litigation across the country — on its interpretation, its exceptions, its enforcement, and, critically, on the proportionality of the departmental actions taken to enforce it. This article examines the text of Rule 86B, dissects each exception in detail, and analyses five important judicial and quasi-judicial decisions that illuminate how courts and tribunals have approached this provision.

The Statutory Text of Rule 86B

The complete text of Rule 86B, as in force, reads as follows:

Rule 86B. Restrictions on use of amount available in electronic credit ledger.

Notwithstanding anything contained in these rules, the registered person shall not use the amount available in electronic credit ledger to discharge his liability towards output tax in excess of ninety-nine per cent. of such tax liability, in cases where the value of taxable supply other than exempt supply and zero-rated supply, in a month exceeds fifty lakh rupees:

Provided that the said restriction shall not apply where —

(a) the said person or the proprietor or karta or the managing director or any of its two partners, whole-time Directors, Members of Managing Committee of Associations or Board of Trustees, as the case may be, have paid more than one lakh rupees as income tax under the Income-tax Act, 1961 in each of the last two financial years for which the time limit to file return of income under sub-section (1) of section 139 of the said Act has expired; or

(b) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on account of unutilised input tax credit under clause (i) of first proviso of sub-section (3) of section 54 [exports of goods/services with payment of IGST]; or

(c) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on account of unutilised input tax credit under clause (ii) of first proviso of sub-section (3) of section 54 [inverted duty structure]; or

(d) the registered person has discharged his liability towards output tax through the electronic cash ledger for an amount which is in excess of 1% of the total output tax liability, applied cumulatively, up to the said month in the current financial year; or

(e) the registered person is — (i) Government Department; or (ii) a Public Sector Undertaking; or (iii) a local authority; or (iv) a statutory body; or

(f) [inserted subsequently] the registered person other than a manufacturer shall be exempted from the provisions of this rule only in respect of goods specified under rule 31D, on which the tax has been paid by the supplier on the basis of retail sale price.

Provided further that the Commissioner or an officer authorised by him in this behalf may remove the said restriction after such verifications and such safeguards as he may deem fit.

Applicability: When Does Rule 86B Bite?

Before examining the exceptions, it is essential to understand precisely when Rule 86B becomes operative. The twin conditions that must be simultaneously satisfied are:

Twin Conditions for Rule 86B to Apply

Condition 1

The registered person's taxable supply (excluding exempt supply and zero-rated supply) in a calendar month must exceed Rs. 50 Lakhs. Exempt supplies and zero-rated supplies are expressly carved out of this computation.

Condition 2

The registered person seeks to utilise the Electronic Credit Ledger to discharge output tax liability in excess of 99% of that month's total output tax liability.

Important Note

The threshold of Rs. 50 Lakhs is computed month-by-month and not on an annual or cumulative basis. Therefore, a taxpayer whose turnover crosses Rs. 50 Lakhs in one month but not in another month will only be subject to Rule 86B in the month where the threshold is crossed. The Rule has no retrospective application within the financial year.

The restriction is on the extent of ECL utilisation — not on the quantum of ITC available. Even if a taxpayer has abundant ITC sitting in the ECL, once Rule 86B applies, at minimum 1% of the output tax liability for the relevant month must be remitted from the ECash Ledger. This seemingly small percentage can translate into significant cash outflows for businesses operating on thin margins or high-volume, low-margin models.

The Exceptions to Rule 86B: A Clause-by-Clause Analysis

The legislature, recognising that the blunt instrument of a mandatory cash payment could adversely affect legitimate and compliant taxpayers, carved out five substantive exceptions (and one goods-specific exception inserted subsequently). Each exception is designed to identify categories of taxpayers who can demonstrate a genuine, verifiable compliance track record and are therefore unlikely to be conduits for fake ITC.

Exception (a): Income Tax Payment of More Than Rs. 1 Lakh

This is arguably the most commonly invoked exception. The underlying logic is that a business — or its key managerial persons — that has been paying substantial income tax is demonstrably profitable and engaged in real economic activity. Such businesses are unlikely to be shell entities created purely to pass fraudulent ITC.

The conditions for this exception to apply are:

- The relevant persons are the registered person itself OR its proprietor, karta, managing director, any two of its partners, whole-time directors, members of managing committee of associations, or board of trustees — depending on the legal form of the entity.

- The qualifying person must have paid more than Rs. 1 Lakh as income tax under the Income-tax Act, 1961.

- The payment must have been made in each of the last two financial years for which the due date under Section 139(1) of the Income-tax Act has expired.

Critical Issue — Individual vs. Aggregate Payment: A major practical controversy arises in the case of partnership firms. Must each individual partner (or the firm itself) independently satisfy the Rs. 1 Lakh income tax threshold, or can the aggregate payment across all partners be considered? The AAR Rajasthan ruling in Aadinath Agro Industries (discussed below) has conclusively held that the exception operates on an individual basis — combined payments cannot be aggregated.

Practical Implication: For a partnership firm or LLP, at least one of its qualifying partners must individually have paid more than Rs. 1 Lakh as income tax in each of the preceding two financial years. If all partners pay, say, Rs. 60,000 each but none crosses Rs. 1 Lakh individually, the exception is not available despite the aggregate payment being substantial.

Exception (b): ITC Refund for Exports (Zero-Rated Supplies)

This exception recognises that genuine exporters who regularly claim ITC refunds under Section 54(3)(i) — i.e., on account of zero-rated supplies made without payment of integrated tax — have a verifiable compliance history with the GST refund ecosystem. The Department would have already scrutinised their ITC claims as part of the refund processing cycle.

The conditions are:

- The registered person must have received a refund exceeding Rs. 1 Lakh in the preceding financial year.

- The refund must have been on account of unutilised ITC under Section 54(3)(i) — which covers exports of goods or services or both made without payment of IGST (i.e., on LUT/bond).

Note: The phrase 'preceding financial year' means the financial year immediately before the current one. If the registered person received qualifying refunds in any earlier year but not in the immediately preceding year, the exception is not available for the current year.

Exception (c): ITC Refund under Inverted Duty Structure

Similarly structured to Exception (b), this exception benefits taxpayers operating under an inverted duty structure — i.e., those where the tax rate on inputs is higher than the tax rate on output supplies, resulting in a consistent accumulation of ITC that cannot be utilised.

The conditions mirror Exception (b), except that the source of the refund is Section 54(3)(ii) (inverted duty structure) rather than Section 54(3)(i). Common beneficiaries include manufacturers of certain textile products, fertilisers, and other commodities where the input-output rate differential results in ITC accumulation.

Exception (d): Cumulative 1% Cash Payment in Current Financial Year

This is the most operationally dynamic exception and, in practice, the most commonly self-triggered. The provision states that if the registered person has already discharged output tax liability through the ECash Ledger for an amount exceeding 1% of the total output tax liability (applied cumulatively from April of the current financial year up to the relevant month), the restriction does not apply for that month.

This exception essentially rewards consistent cash payment behaviour. A taxpayer who routinely pays some amount in cash over the course of the year can effectively become exempt from Rule 86B's month-specific restriction. The cumulative computation method also means that a large cash payment in a single month can provide cover for multiple subsequent months.

Illustration: Suppose a registered person has an aggregate output tax liability of Rs. 10 Crore from April to September of the current financial year. If the person has discharged more than Rs. 10 Lakh (i.e., 1% of Rs. 10 Crore) through the ECash Ledger cumulatively during this period, Rule 86B will not apply for September even if the current month's turnover exceeds Rs. 50 Lakhs.

Exception (e): Government Bodies and Public Sector Entities

This exception carves out the following categories from the Rule's application entirely:

- Government Departments

- Public Sector Undertakings (PSUs)

- Local Authorities

- Statutory Bodies

The rationale is self-evident. Government and government-controlled entities are not engaged in creating fake ITC chains for the purpose of defrauding the revenue. Their procurement processes and payment mechanisms are governed by statutory oversight, and applying the 1% cash mandate to such entities serves no anti-fraud purpose. This exception is absolute and does not carry any threshold or track-record condition.

Exception (f): Goods Taxed on Retail Sale Price — MRP-Based Taxation

This exception, inserted subsequently into Rule 86B, applies to registered persons other than manufacturers, in respect of goods specified under Rule 31D of the CGST Rules, where the supplier has already paid tax on the basis of the retail sale price (MRP). Since the tax has been discharged at source by the manufacturer/supplier on MRP, there is no rationale for imposing the cash-payment burden on the downstream trader.

It is notable that this exception excludes manufacturers — presumably because the legislature did not wish to extend this benefit at the stage of production, where the risk of ITC inflation is considered to be higher.

The Commissioner's Power to Remove the Restriction

The second provision to Rule 86B vests a discretionary power in the Commissioner (or an officer authorised by the Commissioner) to remove the restriction on a case-by-case basis, after such verifications and safeguards as deemed fit. This is a safety valve provision, intended to address genuine hardship cases that may not neatly fit any of the statutory exceptions.

In practice, this power has been rarely used and applications for its exercise are not governed by any prescribed procedure or timeline, making it an uncertain remedy for taxpayers in distress.

Judicial and Quasi-Judicial Developments: Key Decisions on Rule 86B

Rule 86B has generated a growing body of decisions — from the Authority for Advance Rulings (AARs) to various High Courts — that clarify both the scope of the provision and the limits of the Department's enforcement power. Five key decisions are examined below.

Case 1: In re: Aadinath Agro Industries

Court: Authority for Advance Rulings (AAR), Rajasthan

Citation: (2025) 99 GSTL 361

Facts

The applicant was a partnership firm engaged in the supply of agricultural products. Its monthly taxable turnover exceeded Rs. 50 Lakhs, thereby triggering Rule 86B. The firm sought an advance ruling on whether the income tax paid by the partners collectively — though no individual partner (or the firm itself) had paid more than Rs. 1 Lakh — would satisfy Exception (a) and exempt it from Rule 86B.

Held

The AAR, Rajasthan ruled against the applicant. It held that Exception (a) must be read strictly and that the income tax payment of Rs. 1 Lakh or more must be from the registered person itself or any one qualifying individual (partner, director, etc.) individually. The threshold cannot be met by aggregating the income tax payments of multiple persons. Since neither the firm nor any individual partner had independently paid more than Rs. 1 Lakh in income tax in each of the last two financial years, the restriction under Rule 86B was applicable and the firm could only utilise 99% of its ECL for discharging output tax.

Practical Significance

This ruling has important consequences for small and medium partnership firms where no single partner earns above the income tax threshold individually but the partners collectively pay substantial tax. Such firms cannot use Exception (a) and must either pay 1% in cash (or cumulatively satisfy Exception (d)) or explore other available exceptions. The ruling underscores the importance of individual-level compliance tracking for entities organised as partnerships or LLPs.

Case 2: Ujjwal Garg vs. Commissioner, Department of Trade and Taxes

Court: High Court of Delhi

Citation: (2024) 24 CENTAX 49

Facts

The petitioner's GST registration was suspended by the Department on the ground that he had violated Rule 86B by utilising 100% of his ECL to discharge output tax liability without satisfying any of the prescribed exceptions. The suspension continued for an extended period, causing severe disruption to the petitioner's business — he was unable to issue valid tax invoices, collect GST from customers, or claim ITC, effectively bringing operations to a halt.

Held

The Delhi High Court held that the suspension of GST registration as an enforcement measure for violation of Rule 86B could not continue indefinitely. Once the registered person had deposited the required amount (i.e., made good the 1% shortfall in cash payment), the suspension could not be sustained. The Court emphasised that suspension of GST registration has wide and adverse ramifications for a business — far beyond the immediate compliance default — and that its continuance after the underlying default was remedied was neither warranted nor proportionate.

Practical Significance

This decision is significant because it curtails the Department's tendency to prolong registration suspensions as a coercive tool long after the immediate violation has been addressed. For taxpayers who have faced or are facing suspension on account of Rule 86B defaults, this ruling provides a strong basis to challenge the continuance of suspension upon payment of the deficient 1% cash amount. It also signals that courts will scrutinise the proportionality of enforcement actions under Rule 86B.

Case 3: Sri Shivsakthi Mercantile Pvt. Ltd. vs. Assistant Commissioner (ST), Tondiarpet Assessment Circle, Chennai

Court: High Court of Madras

Citation: (2025) 94 GSTL 267

Facts

The assessee, a company registered under GST, was paying income tax in excess of Rs. 1 Lakh per year, thereby qualifying for Exception (a) to Rule 86B. It availed 100% of the ITC available in its Electronic Credit Ledger to discharge its output tax liability. The Department, however, passed an order demanding reversal of 1% of the ITC on the ground that Rule 86B had been violated. The order was passed without affording the assessee an opportunity of personal hearing.

Held

The Madras High Court set aside the order and remanded the matter for fresh adjudication. While it did not decide the merits of whether the assessee's income tax payments satisfied Exception (a), the Court held that passing an order for reversal of ITC under Rule 86B without granting the registered person an opportunity of personal hearing was legally unsustainable. The principles of natural justice — specifically, audi alteram partem — are not mere formalities and must be observed before any adverse order affecting the rights of a registered person is made.

Practical Significance

Beyond the procedural holding, this case illustrates a frequent ground of challenge in Rule 86B enforcement: the Department's tendency to issue orders unilaterally, without meaningful engagement with the taxpayer's position. Any order directing reversal of ITC or imposing a liability on account of Rule 86B, without first hearing the taxpayer, is vulnerable to challenge on natural justice grounds. Taxpayers who have received such orders should examine whether the principles of natural justice were complied with before accepting liability.

Case 4: A.M. Enterprises vs. State of Himachal Pradesh

Court: High Court of Himachal Pradesh

Citation: (2024) 22 CENTAX 573

Facts

The petitioner's GST registration was cancelled by the Department on the ground that it had violated Rule 86B. The order of cancellation was based on a 'prima facie' investigation that had not been completed. No final investigation report was on record. The petitioner contended that cancellation of registration was a grossly disproportionate response to an alleged Rule 86B violation and that it was made in violation of Article 14 of the Constitution of India.

Held

The Himachal Pradesh High Court allowed the writ petition. It held that cancellation of GST registration on the pretext of violation of Rule 86B was a disproportionate punishment and was liable to be interfered with in exercise of its power under Article 226 of the Constitution of India. The Court further held that passing a cancellation order on the basis of a prima facie investigation, without completion of the investigation and without establishing actual default, was arbitrary, unreasonable and in violation of Article 14.

Practical Significance

This ruling firmly establishes that cancellation of GST registration is not a default or routine remedy for Rule 86B violations. The Department must distinguish between (a) a show cause notice and enquiry stage and (b) a final order of cancellation, and must not proceed to the latter without completing the former. More broadly, the judgment reinforces the constitutional principle that enforcement measures must be proportionate to the gravity of the default. The Department's arsenal of actions for Rule 86B violations — including blocking of ITC, suspension of registration, and cancellation — must be deployed proportionately and not as reflexive responses.

Case 5: Mohammed Sadiq vs. Superintendent, Mysuru

Court: High Court of Karnataka

Citation: (2024) 22 CENTAX 535

Facts

The petitioner's GST registration was cancelled by the Department on the ground that he had violated Rule 86B. However, neither the show cause notice issued to the petitioner nor the final order of cancellation contained any details, particulars, or specifics of the alleged Rule 86B violation. The notice and order were bare assertions, without any reference to the relevant month's turnover, the extent of ECL utilisation, or the amount of shortfall in cash payment.

Held

The Karnataka High Court held that the order of cancellation was not legally sustainable. When the show cause notice and the cancellation order are entirely bereft of the details and particulars underlying the alleged Rule 86B violation, the registered person is unable to effectively meet the charge. The Court ordered restoration of registration.

Practical Significance

This decision embodies a crucial procedural safeguard: the Department cannot rely on a mere label ('violation of Rule 86B') to justify cancellation without providing the underlying factual matrix. A compliant show cause notice in Rule 86B cases must, at a minimum, specify the month in which the violation is alleged to have occurred, the taxable turnover for that month, the output tax liability, the extent of ECL utilisation, and the resulting shortfall in cash payment. Taxpayers who have received vague or skeletal notices in Rule 86B proceedings should challenge them on this ground.

Practical Compliance Framework for Rule 86B

Based on the statutory text and the judicial decisions discussed above, the following framework may be adopted by registered persons who are at risk of triggering Rule 86B:

Step 1 — Assess Monthly Applicability

At the end of each calendar month, determine the value of taxable supplies (excluding exempt and zero-rated supplies). If the value does not exceed Rs. 50 Lakhs, Rule 86B is not applicable for that month — no further analysis is required.

Step 2 — Check Exceptions in Sequence

If the Rs. 50 Lakh threshold is crossed, examine each exception in sequence:

- Confirm whether any qualifying individual (director, partner, karta, etc.) has independently paid more than Rs. 1 Lakh in income tax in each of the last two financial years. Document this with ITR acknowledgements and tax payment challans.

- Check whether ITC refund in excess of Rs. 1 Lakh was received in the preceding financial year on account of exports (zero-rated without payment) or inverted duty structure.

- Compute the cumulative output tax paid through the ECash Ledger from April of the current financial year. If this exceeds 1% of the cumulative output tax liability for the same period, Exception (d) is satisfied.

- If the registered person is a Government body, PSU, local authority, or statutory body, no further analysis is needed.

- For dealers of MRP-taxed goods (other than manufacturers), check applicability of Exception (f).

Step 3 — If No Exception Applies, Pay 1% in Cash

Compute 1% of the total output tax liability for the month and ensure that at least this amount is discharged through the ECash Ledger. This payment also counts towards the cumulative tally for Exception (d), potentially relieving the constraint in future months.

Step 4 — Document and Retain Evidence

For each month, maintain a documented record of the exception relied upon — whether income tax payment records, refund orders, or ECash payment summaries. This documentation is essential to defend against any departmental inquiry and to pre-empt challenges of the kind seen in the Madras HC and Karnataka HC cases.

Step 5 — Challenge Disproportionate Enforcement

If the Department initiates action — whether by blocking ITC, suspending registration, or issuing cancellation orders — on account of alleged Rule 86B violations, the decisions of the Delhi, Himachal Pradesh, and Karnataka High Courts provide strong grounds to challenge enforcement measures that are disproportionate, arbitrary, or procedurally deficient.

Conclusion

Rule 86B is a provision that operates at the intersection of anti-fraud enforcement and legitimate business operations. While its objective — curbing the circulation of fake ITC — is wholly legitimate, its application has given rise to genuine hardship for compliant taxpayers and a significant volume of litigation over questions of interpretation, proportionality, and procedural fairness.

The judicial trend is increasingly clear: courts will not permit the Department to weaponise Rule 86B — through indefinite suspension of registration, cancellation on incomplete investigations, or vague show cause notices — in a manner that is disproportionate to the scale of the alleged default. Equally, the AAR's ruling in Aadinath Agro Industries signals that exceptions must be read strictly, placing the burden on taxpayers to ensure that individual-level conditions are genuinely and documentably satisfied.

For taxpayers with monthly turnovers in the Rs. 50 Lakh+ range, Rule 86B compliance cannot be left to chance. A structured monthly assessment of applicability, proactive exception-qualification, and systematic documentation will ensure both regulatory compliance and preparedness to defend against any departmental action.

Disclaimer: This article is intended for general information and professional education. This article should not be considered as Legal Advice.

Input tax credit | ITC rule 43 | Rule 43 of cgst/sgst rules | section 74a | DRC 01D | GST Penalty Under Section 74 | Accounts and Records Under GST | GST Registration Status Check

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co