GST Reverse Charge Mechanism (RCM) Explained: Applicability, Examples & Compliance

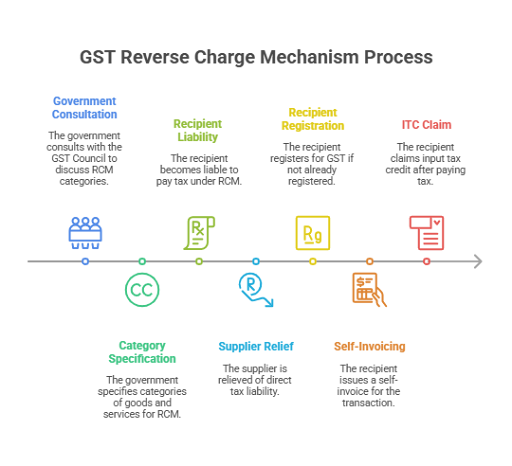

The Reverse Charge Mechanism (RCM) is a critical component of the Goods and Services Tax (GST) framework, particularly concerning the levy and collection of tax under Section 9 of the Central Goods and Services Tax (CGST) Act. It fundamentally shifts the responsibility for paying tax from the supplier of goods or services or both to the recipient. This mechanism is not limited to services but also applies to specific goods.

Government's Role in Specifying Categories for Recipient Payment

The government, in consultation with the GST Council, plays a pivotal role in identifying and notifying the specific categories of supplies and persons subject to RCM. The GST Council, comprising the Union Finance Minister and state finance ministers, is responsible for making recommendations on matters related to the GST Act, including tax rates and mechanisms like RCM.

The legal basis for this specification is primarily found in two sub-sections of Section 9 of the CGST Act (and corresponding sections in the Integrated Goods and Services Tax (IGST) Act and Union Territory Goods and Services Tax (UTGST) Act):

1. Section 9(3) / 5(3) / 7(3) - Specified Categories of Goods or Services: This sub-section empowers the Government to specify categories of goods or services or both where the recipient is liable to pay the tax under RCM. In such cases, all provisions of the Act apply to the recipient as if they were the person liable for paying the tax in relation to that supply. This ensures tax collection even for supplies from registered suppliers if they fall into specified categories.

2. Section 9(4) / 5(4) / 7(4) - Unregistered Supplier to Registered Recipient: This provision allows the Government to specify a class of registered persons who, as recipients of specified categories of goods or services or both from an unregistered supplier, are liable to pay the tax on a reverse charge basis. The registered recipient becomes responsible for paying the tax as if they were the supplier.

◦ Historically, this provision saw periods of broad applicability and exemption before being re-specified for particular categories. As per amendments, it now applies only to "specified class of registered persons" and to "specified categories of goods or services or both" received from unregistered suppliers. This provision currently applies to Real Estate Developers, where a minimum of 80% of receipts must be from Registered Persons; otherwise, the difference is subject to RCM. Further to that, Cement is under the 100% category.

Examples of Government-Specified Categories for RCM

The sources provide several examples of goods and services that the government has notified for RCM:

• Goods:

◦ Cashew nuts (not shelled or peeled).

◦ Bidi wrapper leaves (tendu).

◦ Tobacco leaves.

◦ Essential oils (other than certain citrus fruits, specifically mentioning peppermint, spearmint, water mint, horsemint, bergamot, mentha arvensis).

◦ Raw cotton.

◦ Silk yarn.

◦ Supply of lottery.

◦ Used vehicles, seized and confiscated goods, old and used goods, waste and scrap.

◦ Priority Sector Lending Certificate.

◦ Metal scrap (when supplied by an unregistered person to a registered person).

• Services:

◦ Sponsorship services (when provided by any person other than a body corporate to any body corporate or partnership firm located in the taxable territory).

◦ Renting of motor vehicles (designed to carry passengers) to a body corporate, where the body corporate hires the vehicle for a period during which it is at their disposal (e.g., for employee transport).

◦ Services supplied by the Central Government, State Government, Union territory, or a local authority by way of renting of immovable property to a person registered under the CGST Act.

◦ Services supplied by Direct Selling Agents (other than a Body Corporate, Partnership, or LLP) to a Bank or NBFC.

◦ Legal services provided by an advocate (including a Senior Advocate) or Arbitral

Tribunal services to any business entity.

◦ Manpower supply services or security services (when provided by any person other than a body corporate to a body corporate).

Implications for Taxable Persons under RCM

When the government specifies categories for RCM, it significantly alters the compliance obligations for both recipients and, in some cases, suppliers:

• Recipient's Obligations (the person liable to pay tax):

◦ Compulsory Registration: Persons liable to pay tax under RCM are mandated to obtain GST registration, regardless of their aggregate turnover reaching the standard threshold limits. This takes precedence over general exemption provisions, such as Section 23, creating a compulsory registration requirement under Section 24.

◦ Tax Payment Method: Tax liability under RCM must be discharged by debiting the electronic cash ledger (i.e., paid in cash). It cannot be paid by utilising the input tax credit (ITC) available in the electronic credit ledger.

◦ Self-Invoicing: If supplies are received from an unregistered supplier, the registered recipient liable under RCM must issue an invoice (self-invoice) for the inward supplies. A new Rule 47A requires the recipient to issue such an invoice within 30 days from the date of receipt of the supply for RCM transactions.

◦ Time of Supply: The time of supply for RCM transactions is determined by specific rules, which may differ from the forward charge. For goods, it is the earliest of: the date of receipt of goods, the date of payment as recorded in the recipient's books or debited from their bank account (whichever is earlier), or the date immediately following thirty days from the supplier's invoice date. For services, it is the earliest of: the date of payment or the date that is 60 days after the supplier's invoice date. If none of these can be determined, it's the date the supply was recorded in the recipient's books.

◦ Input Tax Credit (ITC): ITC on RCM supplies is generally admissible to the recipient once the tax has been duly paid in cash.

▪ For the limited purpose of ITC apportionment under Section 17(3), the value of exempt supplies includes supplies on which the recipient is liable to pay tax on a reverse charge basis.

▪ The requirement to reverse ITC if payment to the supplier is not made within 180 days (Rule 37) does not apply to supplies where tax is payable on a reverse charge basis.

▪ No ITC is available for any tax paid under Section 74 (demand due to fraud, willful misstatement, or suppression of facts), Section 129 (detention/seizure), and Section 130 (confiscation). This implies that if RCM tax is demanded under Section 74, the ITC for such payment might be blocked, unless the demand is later deemed to be under Section 73 (non-fraudulent reasons), in which case ITC would be admissible.

▪ For common input services liable to RCM, a registered person (with the same PAN and State code as the Input Service Distributor (ISD)) must first pay the RCM tax liability and then issue an invoice or credit/debit note to transfer the credit to the ISD for distribution.

◦ Returns: The details of inward supplies liable to RCM must be reported in FORM GSTR-3B. The tax invoice must also indicate whether the tax is payable on a reverse charge basis.

◦ Output Tax Exclusion: Taxes payable by the recipient under RCM are considered outside the scope of 'output tax', which reinforces why ITC cannot be used to pay RCM liability.

• Supplier's Position:

◦ For supplies subject to RCM, the supplier is generally relieved of the direct liability to pay tax to the government.

◦ Unregistered suppliers making supplies exclusively subject to RCM are not required to obtain registration under GST if they have no other taxable turnover.

◦ Taxpayers under the composition scheme remain liable to pay tax under RCM on their inward supplies, even though they cannot collect tax on their outward supplies. The value of such inward RCM supplies is not included in their aggregate turnover for the composition scheme.

In summary, the government, through the recommendations of the GST Council, utilizes RCM to ensure tax collection in specific, identified scenarios, thereby impacting the registration, payment, invoicing, and input tax credit behaviour of both recipients and suppliers involved in these transactions.

Powers of GST Officers | GST Audit Procedure | GST ADT-01 | Penalty for Non GST Registration | GST Inspector Power

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified