An In-Depth Analysis of Penalty under Section 122B of the CGST Act

1.0 Introduction: The Imperative of Track and Trace Compliance in GST

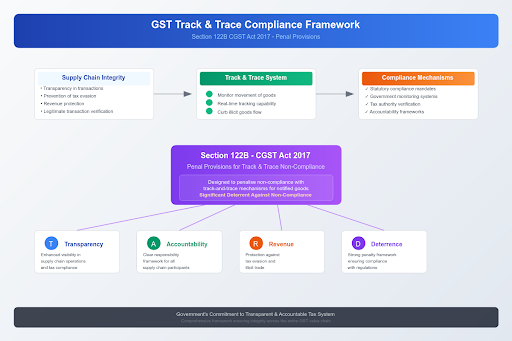

In any modern value-added tax regime, such as the Goods and Services Tax (GST), the integrity of the supply chain is paramount. To ensure transparency, prevent tax evasion, and protect revenue, the government employs various compliance mechanisms. A critical component of this framework is the ability to monitor the movement of specified goods through a 'track and trace' system. This allows tax authorities to verify the legitimacy of transactions and curb the flow of illicit goods.

To lend statutory force to such compliance mandates, the Central Goods and Services Tax (CGST) Act, 2017, incorporates specific penal provisions. Section 122B is one such provision, designed explicitly to penalise non-compliance with the track-and-trace mechanism for notified goods. It serves as a significant deterrent against non-compliance, underscoring the government's commitment to a transparent and accountable tax system.

The full text of the provision reads as follows:

Section 122B. Penalty for failure to comply with track and trace mechanism.- Notwithstanding anything contained in this Act, where any person referred to in clause (b) of sub-section (1) of section 148A acts in contravention of the provisions of the said section, he shall, in addition to any penalty under Chapter XV or the provisions of this Chapter, be liable to pay a penalty equal to an amount of one lakh rupees or ten per cent. of the tax payable on such goods, whichever is higher.

To fully appreciate the scope and implications of this section, a detailed breakdown of its legal components and the procedural framework governing its application is essential.

2.0 Deconstructing Section 122B: A Component-by-Component Analysis

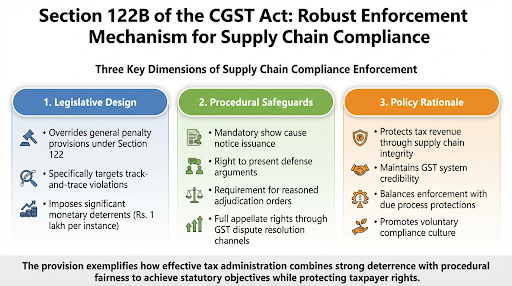

Understanding Section 122B's impact requires careful analysis of its legal phrasing. The statute contains clauses that define its overriding nature, identify liable persons, clarify penalty relationships, and establish financial penalties. This section breaks down the provision's core components to clarify its scope for taxpayers and practitioners.

2.1 The "Notwithstanding" Clause

The section begins with the phrase "Notwithstanding anything contained in this Act". In legal parlance, this is known as a non-obstante clause. Section 122B's inclusion gives it an overriding effect over any inconsistent CGST Act provisions. This establishes the penalty as a distinct liability, ensuring its application cannot be diluted by invoking other general provisions.

2.2 The Liable Person

The penalty is applicable "where any person referred to in clause (b) of sub-section (1) of section 148A acts in contravention". This phrase is crucial as it precisely defines the class of taxpayers subject to this specific penalty. It directly links the contravention to the obligations laid out in Section 148A(1)(b) of the Act. This means the penalty is not general but is targeted specifically at individuals mandated to comply with the track-and-trace mechanism who have failed to do so.

2.3 Cumulative Nature of the Penalty

The provision states that the liable person "shall, in addition to any penalty under Chapter XV or the provisions of this Chapter, be liable to pay a penalty". This clause clarifies that the penalty under Section 122B is not mutually exclusive. It can be levied over and above other general penalties prescribed under the Act, such as those under Section 125 (General Penalty), for any related offences. The cumulative nature of this penalty signals legislative intent to treat a violation of the track-and-trace mechanism as a distinct and serious offence, separate from other procedural lapses that may be covered by general penalties.

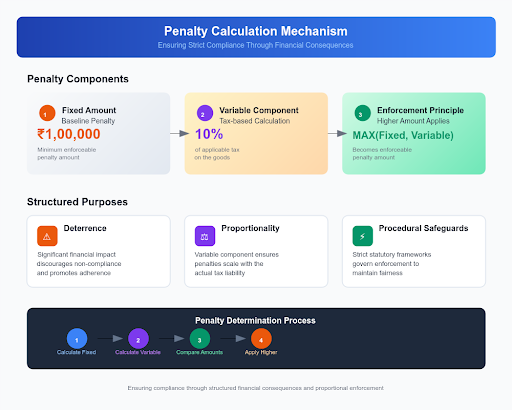

2.4 The Quantum of Penalty

The financial implication is clearly defined as a penalty "equal to an amount of one lakh rupees or ten per cent. of the tax payable on such goods, whichever is higher." This calculation makes the financial consequence of non-compliance unambiguous and substantial. The quantum is determined as follows:

• Component 1: A fixed amount of ₹1,00,000.

• Component 2: An amount equal to 10% of the tax payable on the goods in question.

• Condition: The penalty levied will be the higher of these two amounts.

This significant financial penalty highlights the provision's deterrent purpose; however, its enforcement is not automatic and must comply with the stringent procedural framework established under the Act to ensure fairness.

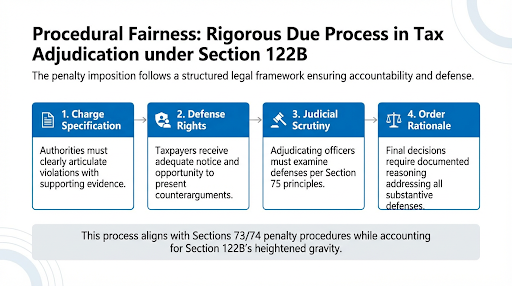

3.0 The Procedural Framework for Imposing Penalties

Procedural fairness is a cornerstone of tax adjudication. While Section 122B defines a stringent penalty, its imposition is not arbitrary. It must follow the due process of law established under the CGST Act and its associated Rules. This framework ensures that a taxpayer's rights are protected, creating a logical sequence of events from the initiation of proceedings to the final order. It begins with a clear articulation of charges, which enables the taxpayer to mount a defence that the adjudicating authority must duly consider. The procedures applicable to general penalties under Sections 73 and 74 are instructive in understanding how a penalty under Section 122B would likely be imposed.

3.1 Initiation of Proceedings: The Show Cause Notice (SCN)

Penalty proceedings under the GST law commence with the issuance of a Show Cause Notice (SCN). As per Rule 142 of the CGST Rules, the proper officer may first issue a pre-notice intimation in FORM GST DRC-01A, allowing the taxpayer to settle the matter. If the taxpayer does not respond or the response is unsatisfactory, a formal SCN is issued in FORM GST DRC-01.

The SCN is the foundation of any adjudication proceeding. In line with the judicial principle established in Brindavan Beverages (P) Ltd.*, the allegations in the notice must be specific, clear, and not vague. This is to ensure that the noticee is given a proper opportunity to understand the charges and prepare a robust defence against the proposed penalty.

Author’s Note: The specificity requirement for an SCN is a critical first line of defence. A vague notice can be challenged at the outset as legally untenable, potentially quashing the proceedings before they begin on the merits.

*Commissioner of Central Excise, Bangalore vs Brindavan Beverages Pvt. Ltd. [(2007) 213 ELT 487 (SC)]

3.2 Principles of Natural Justice and Adjudication

Following the issuance of a specific SCN that enables a taxpayer to formulate a robust response, the principles of natural justice must be strictly adhered to. The taxpayer must be given a reasonable opportunity to be heard, either through written submissions or a personal hearing. The adjudication process cannot be a mere formality. As observed by the High Court in Bata India Ltd.*, the Adjudicating Authority is the first authority to record findings of fact. Therefore, a thorough exposition of the facts, after considering the taxpayer's submissions, must be conducted before applying the law. The Adjudicating Authority must pass a speaking order that addresses the taxpayer's submissions and provides clear reasons for its decision. This meticulous adjudication process, grounded in natural justice, is the first of several key legal safeguards available to a taxpayer to challenge the imposition of this penalty.

*Bata India Ltd. vs Commissioner of Customs, Central Excise and Service Tax, Chennai-III [(2019) 24 GSTL 326 (Mad.)]

4.0 Taxpayer Safeguards and Avenues for Recourse

The GST framework includes several legal safeguards to protect taxpayers from arbitrary or unjust actions by tax authorities. Even when faced with a stringent penalty like the one prescribed under Section 122B, a taxpayer is not without recourse. These rights and remedies, including the mandate for a reasoned order and the right to appeal, are interconnected and essential for ensuring that the final outcome of any proceeding is fair and legally sound.

4.1 The Mandate for a Reasoned Order

A fundamental safeguard for any taxpayer is the right to a reasoned order. As established by the Supreme Court in Kranti Associates (P) Ltd. v. Masood Ahmed Khan*, a quasi-judicial authority, which includes a tax officer, is obligated to record clear, explicit, and cogent reasons in support of its conclusions. This requirement is not merely for transparency; it is a prerequisite for a meaningful appeal, as it provides the specific legal and factual grounds that the Appellate Authority will review. An unreasoned order can be challenged as being arbitrary and in violation of the principles of natural justice.

Author’s Note: The absence of a reasoned order is a strong ground for appeal. It indicates a non-application of mind by the adjudicating authority and severely hampers the taxpayer's ability to contest the specific findings, which may lead to the order being set aside by an appellate body.

*Kranti Associates (P) Ltd. v. Masood Ahmed Khan [(2010) 9 SCC 496 (SC) :: (2011) 273 ELT 345 (SC)]

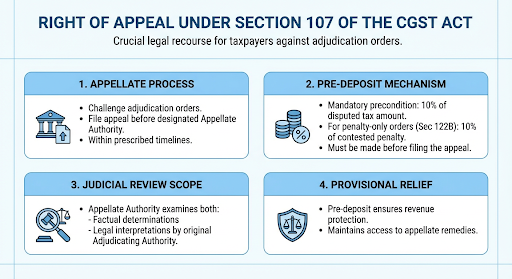

4.2 The Right of Appeal

The primary legal remedy for a taxpayer aggrieved by an adjudication order is the right of appeal. Section 107 of the CGST Act allows a taxpayer to file an appeal before the designated Appellate Authority. This provides an opportunity for a higher administrative authority to review the facts and legal interpretations of the Adjudicating Authority.

However, to file an appeal, the taxpayer must fulfill a mandatory pre-deposit requirement. As per Section 107(6)(b) of the CGST Act, the appellant must pay a sum equal to ten per cent of the remaining amount of tax in dispute. In the context of a penalty-only order under Section 122B, this would typically be interpreted as ten per cent of the penalty amount in dispute.

4.3 The Binding Nature of Judicial Precedents

Taxpayers can also rely on the legal principles established by higher courts. In the case of Pay Pal India Pvt Ltd*, the Madras High Court held that judgments of the High Courts bind the Revenue Department unless set aside by the Supreme Court or the underlying legal position is altered by a subsequent amendment to the law. This principle provides a significant safeguard, allowing taxpayers and their representatives to rely on favourable judicial precedents to argue their cases, thereby ensuring consistency and predictability in the application of tax laws.

*Commissioner of GST & Central Excise, Chennai vs Pay Pal India Pvt Ltd [(2020) 39 GSTL 261 (Mad.)]

5.0 Conclusion: Balancing Compliance with Fairness

Section 122B of the CGST Act constitutes a targeted and significant penal provision aimed at enforcing the critical track-and-trace mechanism. Its structure—with an overriding effect, specific applicability, and a substantial penalty quantum—signals a clear legislative intent to ensure strict compliance with supply chain measures. It is a powerful tool in the hands of the tax administration to safeguard revenue and maintain the integrity of the GST system.

This stringent provision is balanced by a procedural framework and taxpayer safeguards based on natural justice. Issuance of a show cause notice, the right to be heard, a reasoned order, and the right to appeal ensure a fair and transparent process.

Ultimately, Section 122B exemplifies the dual objectives of the GST law: to enforce strict compliance through meaningful deterrents while upholding the principles of procedural fairness and justice throughout the adjudication process. This balance is essential for fostering trust in the tax system and promoting voluntary compliance among taxpayers.

Need for GST in India | Powers of GST Officers | UQC Code in GST | Cookies New GST Rate | GST Slab for Bakery Products

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified