Late Fees under GST: What the Law Says and What the Courts Have Ruled

The GST regime thrives on automated compliance. File your returns on time to ensure the system runs smoothly. Miss a deadline, and late fees kick in — automatically, without a show cause notice, and without any consideration of intent. But does the law permit the department to go beyond this automated levy? Can they pile on general penalties, freeze bank accounts, or ignore portal glitches?

The Courts have had a lot to say on this. Let's break it down.

The Statutory Framework: How Late Fees Work under Section 47

The charging provision is Section 47 of the CGST Act, 2017. It's straightforward — if you miss a filing deadline, you pay.

Which Filings Attract a Late Fee?

A late fee applies to the delayed filing of:

- GSTR-1 (outward supplies under Section 37)

- GSTR-3B and other returns under Section 39 or Section 45

- TCS returns under Section 52

- Annual Return under Section 44 (GSTR-9 and GSTR-9C)

How Much is the Late Fee?

For regular returns, the CGST Act prescribes ₹100 per day of continuing default, subject to a maximum of ₹5,000. Since an equal amount is levied under the respective SGST/UTGST Act, the effective total becomes ₹200 per day, capped at ₹10,000.

However, through various notifications issued under Section 128, the Government has rationalized these amounts significantly — lower caps apply for small taxpayers, nil filers face reduced rates (₹20 per day capped at ₹500), and amnesty schemes have been introduced from time to time.

For the Annual Return (Section 44), the maximum late fee is capped at 0.25% of the taxpayer's turnover in the State or Union territory under the CGST Act. From FY 2022-23 onwards, further tiered reductions based on turnover slabs have been notified.

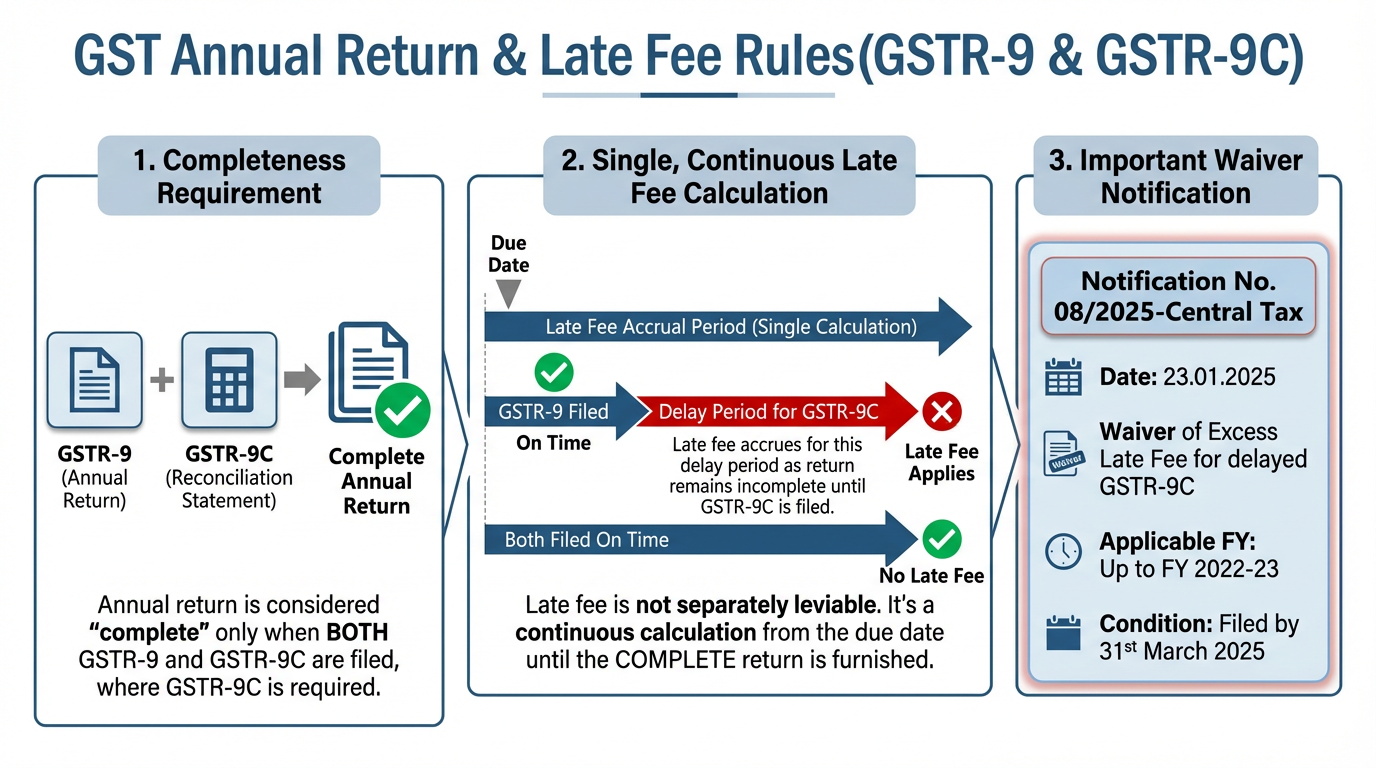

The GSTR-9C Clarification — Circular No. 246/03/2025-GST

A long-standing ambiguity was whether late fee is separately leviable for delayed filing of the Reconciliation Statement (GSTR-9C). Circular No. 246/03/2025-GST, dated 30th January 2025, settled this conclusively. The key clarifications are as follows:

- Where GSTR-9C is required, the annual return is considered "complete" only when both GSTR-9 and GSTR-9C are filed.

- Late fee is not separately leviable for GSTR-9 and GSTR-9C — it is a single, continuous calculation from the due date until the complete return is furnished.

- If GSTR-9 is filed on time but GSTR-9C is delayed, late fee accrues for the period of delay in filing GSTR-9C, since the annual return remains incomplete.

- Notification No. 08/2025-Central Tax dated 23.01.2025 waived excess late fee for delayed GSTR-9C for financial years up to FY 2022-23, provided it was filed by 31st March 2025.

Practical takeaway: Always file GSTR-9 and GSTR-9C together.

What the Courts Have Ruled: Four Critical Propositions

While the GSTN portal auto-calculates and auto-deducts late fees, the Courts have drawn firm lines on procedural overreach, double penalisation, and technical failures.

1. Late Fee + General Penalty for the Same Default = Double Jeopardy

A recurring question has been whether the department can levy a general penalty under Section 125 (up to ₹25,000) for non-filing of returns, in addition to the late fee under Section 47 already charged for the same default.

The Madras High Court in Tvl. Jainsons Castors & Industrial Products v. The Assistant Commissioner (ST) [W.P. No. 36614 of 2024, decided on 04.02.2025 | (2025) 28 CENTAX 181 (Mad.)] answered this definitively. The Court held that Section 125 is a residuary penalty clause — it applies only in cases where no separate penalty or fee is prescribed for the contravention. Since Section 47 specifically provides for a late fee for the delayed filing of returns, invoking Section 125 in addition is impermissible. The penalty under Section 125 was quashed, but the late fee under Section 47 was upheld.

This reasoning was also echoed in the Allahabad High Court's approach in M/s Rathore Building Material v. The Commissioner of State Tax [W.P.(T) No. 1361 of 2023, decided on 01.12.2023 | (2023) 13 CENTAX 185 (All.)], where the Court held that mere delay in filing returns, absent any intent to evade tax, cannot justify a punitive penalty under Section 125 when specific late fee provisions already exist.

2. Recovery Without Notice: Garnishee Proceedings Under Section 79

One of the more aggressive enforcement tactics has been for the department to initiate garnishee proceedings under Section 79 — attaching bank accounts or directing debtors to pay the government — for recovery of late fees and interest, without issuing a prior Show Cause Notice or completing any adjudication.

The Jharkhand High Court in the landmark case of Mahadeo Construction Co. v. Union of India [W.P.(T) No. 3517 of 2019, decided on 21.04.2020 | (2020) 36 GSTL 343 (Jhar.)] held that garnishee proceedings under Section 79 cannot be initiated for recovery of interest without first adjudicating the liability under Section 73 or 74 of the CGST Act. The Court held that even where the liability of interest is "automatic" under Section 50, its computation and demand require an adjudication process when disputed. Recovery proceedings initiated directly, bypassing due process, were held to be a violation of the principles of natural justice and were quashed.

Similarly, the Telangana High Court in Kesoram Industries Ltd. v. Commissioner of Central Tax [W.P. No. 23431 of 2023, decided on 20.09.2023 | (2023) 100 GST 173] emphasised that before issuing garnishee proceedings under Section 79, the authorities must issue a notice under Section 73(1) and provide an opportunity to the assessee to submit a reply.

Principle established: The automated nature of GST does not exempt the department from issuing notices before coercive recovery. Even for amounts treated as "self-assessed" liabilities, due process remains non-negotiable.

3. Technical Glitches: Taxpayers Cannot Be Penalised for GSTN Failures

The early years of GST were plagued with portal failures, system downtime, and filing errors. Courts have consistently taken a lenient view when delays are attributable to the GSTN portal's inadequacies.

In the landmark Delhi High Court decision of Brand Equity Treaties Ltd. v. Union of India [W.P.(C) 11040/2018, decided on 05.05.2020 | (2020) 38 GSTL 10 (Del)], the Court made a crucial observation: the term "technical difficulty" is a broad term, and the government cannot restrict it only to glitches recorded in their own system logs. It encompasses difficulties faced by taxpayers due to low bandwidth, system inadequacies, and the general "trial and error" phase of GST implementation.

The Court held that taxpayers cannot be deprived of their valuable rights — such as transitional credit — or burdened with penalties and late fees due to the government's own portal's technological shortcomings. The GST filing mechanism under Rule 117 was held to be procedural and directory, not mandatory, and the substantive right to avail accrued credit (a constitutional right under Article 300A) could not be extinguished by procedural rules.

Note: While the Supreme Court stayed the specific relief in Brand Equity in June 2020 [(2020) 117 taxmann.com 225 (SC)], the broader principle regarding technical difficulties was subsequently accepted across multiple High Courts and eventually resulted in the GSTN reopening the portal for TRAN-1 filing pursuant to the Supreme Court's direction in Filco Trade Center Pvt. Ltd. [(2022) 93 GST 233 (SC)].

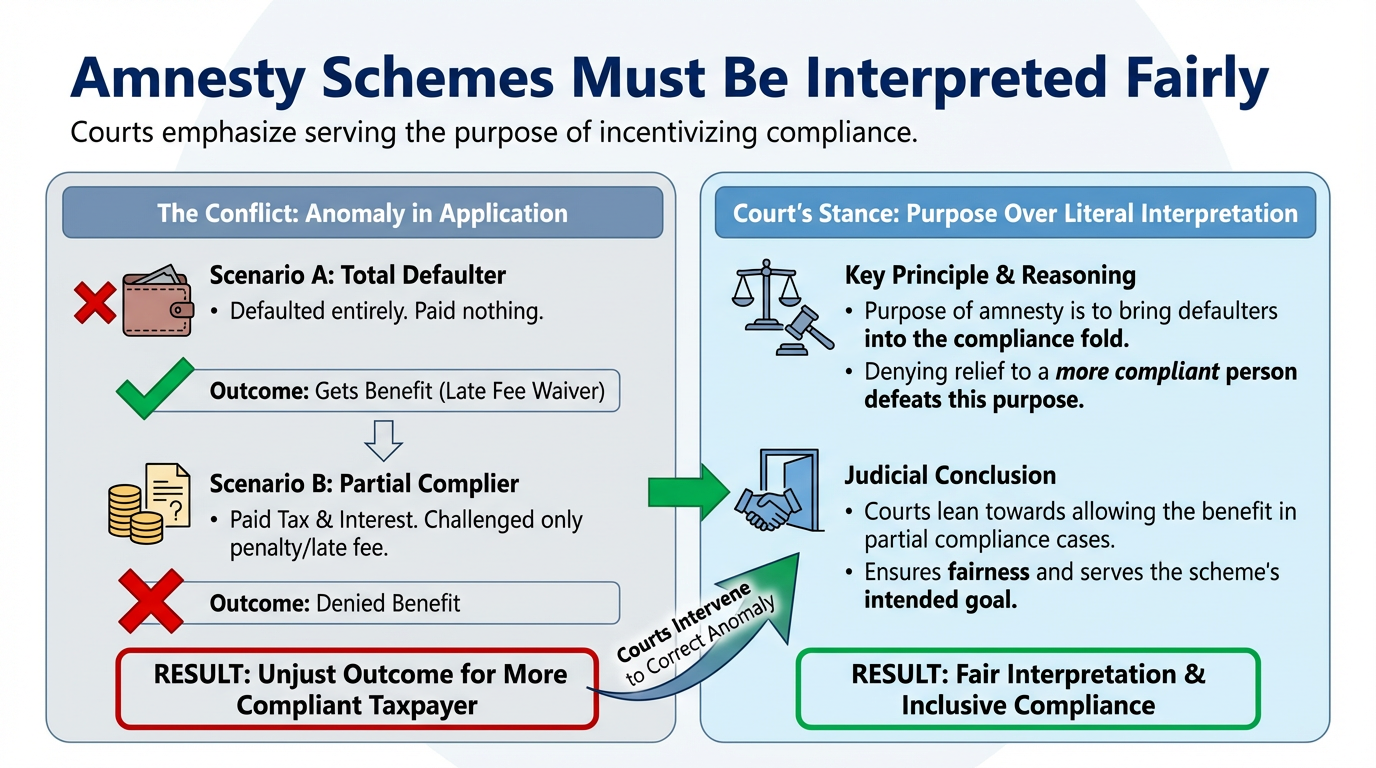

4. Amnesty Schemes Must Be Interpreted Fairly

Courts have consistently emphasised that amnesty schemes — which waive late fees to incentivise compliance — must be interpreted in a manner that serves their purpose.

An anomaly arises when a person who has defaulted entirely receives a late fee waiver, while a person who partially complied (paid the tax and interest but challenged only the penalty or late fee) is denied the same benefit. Courts have leaned towards allowing the benefit in such cases, reasoning that the purpose of amnesty is to bring defaulters into the compliance fold, and denying relief to a more compliant taxpayer creates an unjust outcome.

Key Takeaways for Practitioners

- Late fee is not a penalty. It is a separate compensatory charge for delay. Once Section 47 is attracted, the department cannot additionally invoke Section 125 for the same default.

- Due process is mandatory. The automated nature of the GST portal does not exempt the department from issuing notices before recovery. Direct garnishee proceedings under Section 79, without adjudication, remain vulnerable to challenge in writ jurisdiction.

- System failures are the government's problem, not the taxpayer's. Technical glitches, portal downtime, and system inadequacies during the nascent phase of GST cannot be used to penalise compliant taxpayers.

- File GSTR-9 and GSTR-9C together. Post Circular No. 246/03/2025-GST, filing one without the other leaves the annual return "incomplete" and the late fee clock keeps ticking.

- Challenge arbitrary recoveries. Where late fees have been recovered without due process or through coercive garnishee proceedings, a writ petition under Article 226 remains a potent remedy.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional advice. Readers should consult their tax advisors for specific situations.

gst late fees | gstr 1 late fees | gstat appeal format | section 47 of gst | section 74A

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified