ITR 5 Complete Details

The Income Tax Department requires a taxpayer to furnish a return of income under Rule 12 of the Income Tax Rules, 1962. Income-tax return (ITR) is the document in which the taxpayer provides information about their income and tax, to the Income Tax (IT) Department. The IT Department has released various ITRs, and each ITR applies to certain types of taxpayers. In this article, we will discuss the applicability of ITR 5 and its features. Key topics covered here are:

Who should file ITR-5?

As per the Income Tax Department, ITR-5 applies to all taxpayers except the following:

- Individuals

- Hindu Undivided Family (HUF)

- Company

- Person filing ITR 7 (ITR 7 is applicable for persons including companies required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) of the Income Tax Act, 1961 i.e., Charitable or Religious institutions/Political Parties/Research Associations/Educational Institutions/Trusts, etc.)

That means Partnership Firms, LLPs’, AOP, BOI and others not mentioned above can file ITR 5.

What is the due date to file ITR-5?

The due date for filing ITR-5 is:

| Type | Due dates for the financial year ended 31st March 20XX | Due dates for the financial year ended 31st March 2020 |

| Audit not applicable | 31st July 20XX | 30th November 2020* |

| Audit Applicable | 30th September 20XX | 30th November 2020* |

| Transfer Pricing Audit Applicable | 30th November 20XX | 30th November 2020 |

*Due date extended via Notification dated 24Th June 2020

What is the format of ITR-5?

ITR-5 is divided into two parts, i.e., Part A and Part B Part A contains:

- General Information of the taxpayer including Name, PAN, Address, etc.

- Balance Sheet as on 31st March

- Profit & Loss Statement for the year ending 31st March (including manufacturing account and trading account, where applicable)

- Other information like the method of accounting employed, method of valuation of closing stock, expenses disallowed, etc. (mandatory where an audit is applicable)

- Quantitative details of inventory (mandatory where an audit is applicable)

- Income from house property, business/profession, capital gains and other sources

- Depreciation on assets

- Expenditure on scientific research

- Sale of equity shares on which Securities Transaction Tax (STT) is paid

- Set-off and carry forward of losses

- Effect of Income Computation Disclosure Standards (ICDS) on profit

- Eligible deduction under section 10 and Chapter VI-A

- Computation of Alternative Minimum Tax (AMT)

- Income chargeable at special rates

- Information regarding all partnership firms in which the taxpayer is a partner

- Exempt income

- Details of Pass-Through Income from business trusts or investment funds

- Details of tax on secondary tax adjustments

- Details of income received outside India and the related tax relief

- Details of foreign assets

- Details of investments made between 01st April 2020 to 31st July 2020 or 01st April 2020 to 30th September 2020 as applicable (Refer point 4 under ‘What are the key modifications to ITR-5 for AY 2020-21?’)

- Information regarding the turnover or gross receipts reported under GST

Part B contains:

- Calculation of total income and tax liability on total income

- Details of payment of advance tax and/or self-assessment tax

- Details of TDS and TCS

- Verification of taxpayer

How to download ITR-5 for filing?

To download ITR-5:

Step 1: Download the ITR 5 form from the income tax e-filing website.

Step 2: Select the appropriate Assessment Year and download the excel utility file available for ITR-5.

How to file ITR-5?

- After downloading the ITR-5 utility, it must be filled appropriately. The tabs in the utility must be validated before an XML file is generated.

- The XML file must be uploaded on the income tax website in the taxpayer’s account. Taxpayers must note that it is mandatory to sign the ITR-5 digitally when an audit is applicable.

- Taxpayers, for whom audit is not applicable, may digitally sign the ITR-5 or may physically sign the acknowledgement generated (ITR-V) and send the signed physical copy to the Centralized Processing Centre, Income Tax Department, Bengaluru 560500 via ordinary post or speed post.

What are the key modifications in ITR-5 for AY 2020-21?

The key modifications made to ITR-5 for AY 2020-21 are:

- Along with the information regarding investments in unlisted equity shares (Name, PAN, details of the movement of shares) during the year, an additional column for ‘Type of Company’ has been included for the AY 2020-21. This is a drop-down option which requires the taxpayer to select whether the company is a domestic or a foreign company.

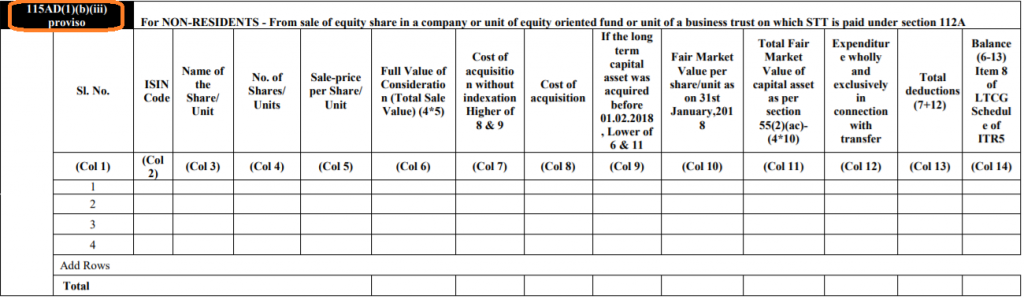

- Schedule 112A and 115AD(1)(b)(iii) has been added for the calculation of long-term capital gains from the sale of equity shares or units of equity-oriented fund or units of a business trust on which STT is paid under section 112A.

- Schedule TPSA has been newly added to provide details of tax on secondary adjustments as per section 92CE(2A).

- The new format also provides for entering details about Investments/deposits/payments made after 1st April 2020. This includes:

-

- Details of tax-saving investments under Chapter VI-A made between 1st April 2020 and 31st July 2020;

- Eligible amount of deductions under section 10AA between 1st April 2020 and 30th September 2020;

- Payments to claim deduction under section 54 to 54GB made between 1st April 2020 and 30th September 2020.

The taxpayer, for AY 2020-21, can claim these investments/deposits/payments. However, this is optional.

- An additional block of plant and machinery with a depreciation rate of 45% is now included in Schedule DPM for the AY 2020-21. This block includes lorries/ taxis/motor buses used in the business of running them on hire. These should be purchased and put-to-use on or after 23rd August 2019, but before 1st April 2020.

- Additional details in Schedule CFL (Carry Forward of Losses) is to be included. This relates to loss from life insurance business under section 115B and Pass-Through Income (PTI) for the AY 2020-21.

- Additional questions applicable to the taxpayer who do not declare income under section 44AD/ 44ADA/ 44AE/ 44B/ 44BB/ 44BBA and the sales/turnover/gross receipts of their business exceed INR 1 crore but does not exceed INR 5 crores for the AY 2020-21 are included.

Need of GST In India | 16 Digit Invoice Number in GST | GST Inspector Salary | Dry Fruits Hsn Code | GST Maintenance Charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified