For years, tax departments and businesses have been locked in a high-stakes tug-of-war over a fundamental question: when a contractor pays a penalty for a delay, is the recipient "selling" them the right to be late? The department's penchant for viewing every flow of money as a taxable "supply" has led to a flurry of GST notices and show-cause proceedings, leaving CFOs and Tax Heads grappling with demands on amounts that were meant to cover losses, not generate revenue.

This updated article deconstructs the legal landscape of liquidated damages under GST, drawing from the core principles of the CGST Act, the clarifying light of Board Circulars, and the established judicial consensus.

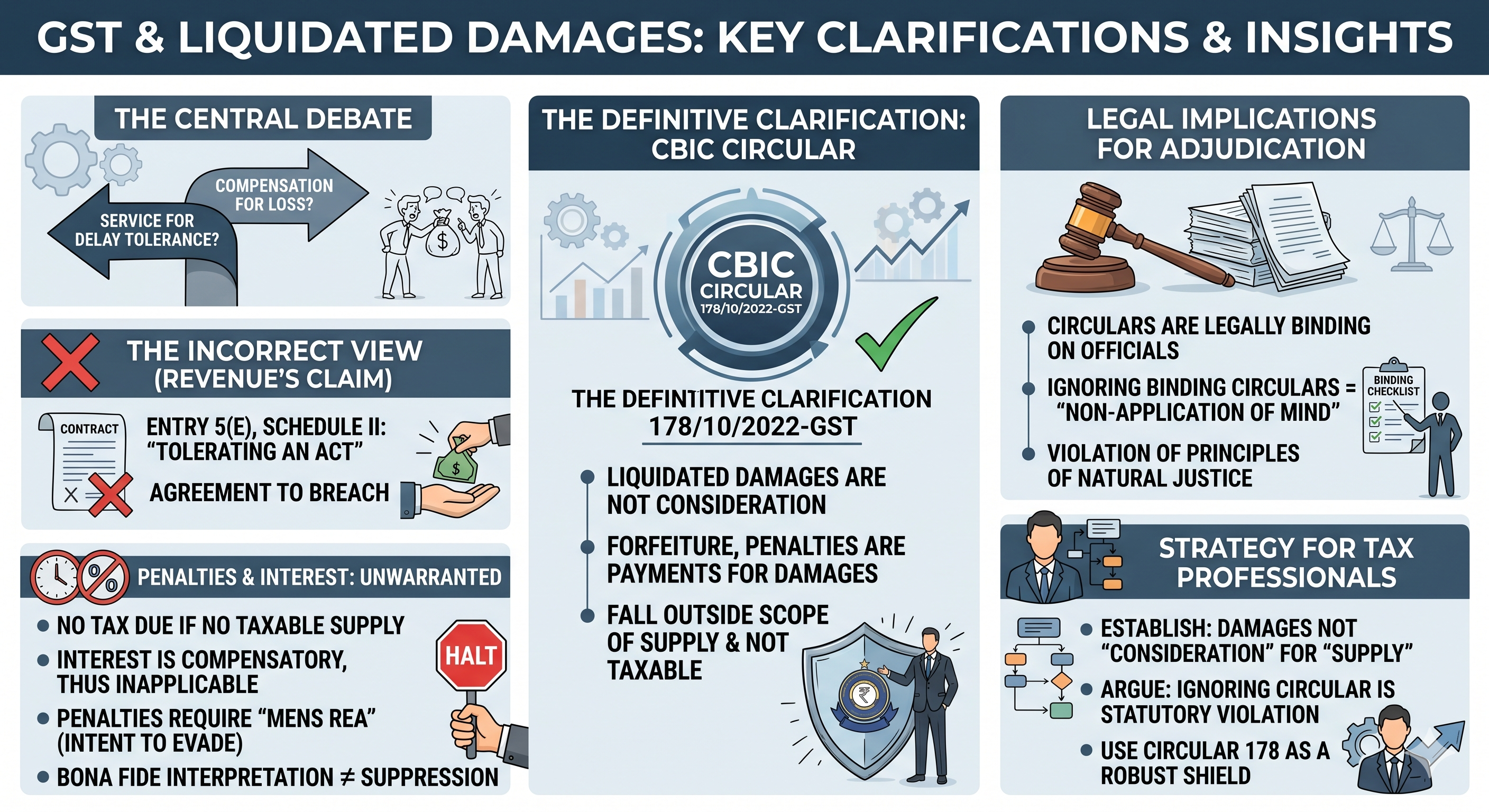

Does accepting liquidated damages mean tolerating a breach?

The Revenue Department frequently invokes Entry 5(e) of Schedule II of the CGST Act, 2017, to tax liquidated damages. They argue that by accepting a penalty for a delay or breach, the aggrieved party is providing a service by "agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act."

Why liquidated damages are different from contractual services

This interpretation stems from a fundamental misunderstanding of contractual intent. A contract is entered into for performance, not for its breach. The clauses for liquidated damages are not an alternative mode of performance; they are a pre-quantified measure of damages to compensate the aggrieved party for the other's failure to perform.

Can liquidated damages be treated as a taxable supply?

For a taxable supply to exist, there must be an express or implied agreement to provide a service in exchange for consideration. The payment of liquidated damages arises from the failure to adhere to the contract, not from a separate agreement to permit or tolerate such failure. As clarified by the Board, an agreement to do or tolerate an act cannot be presumed to exist merely because there is a flow of money. The source of the payment is the breach, not a supply.

Liquidated damages vs consideration under GST

At the heart of this dispute is the definition of "consideration" under Section 2(31) and its relationship with "supply" under Section 7 of the CGST Act.

Does every payment qualify as consideration?

While liquidated damages represent a flow of money, every such flow is not consideration. The payment must have a direct and immediate nexus with an identifiable supply. In the case of damages, the payment is made to compensate for a loss incurred due to the breach of contract.

Why there is no direct supply in liquidated damages

There is no independent activity, benefit, or service rendered by the recipient in exchange for these damages. The recipient is not "supplying" a right to breach the contract. Instead, they are being compensated for the injury resulting from that breach.

What does CBIC Circular 178/10/2022-GST clarify?

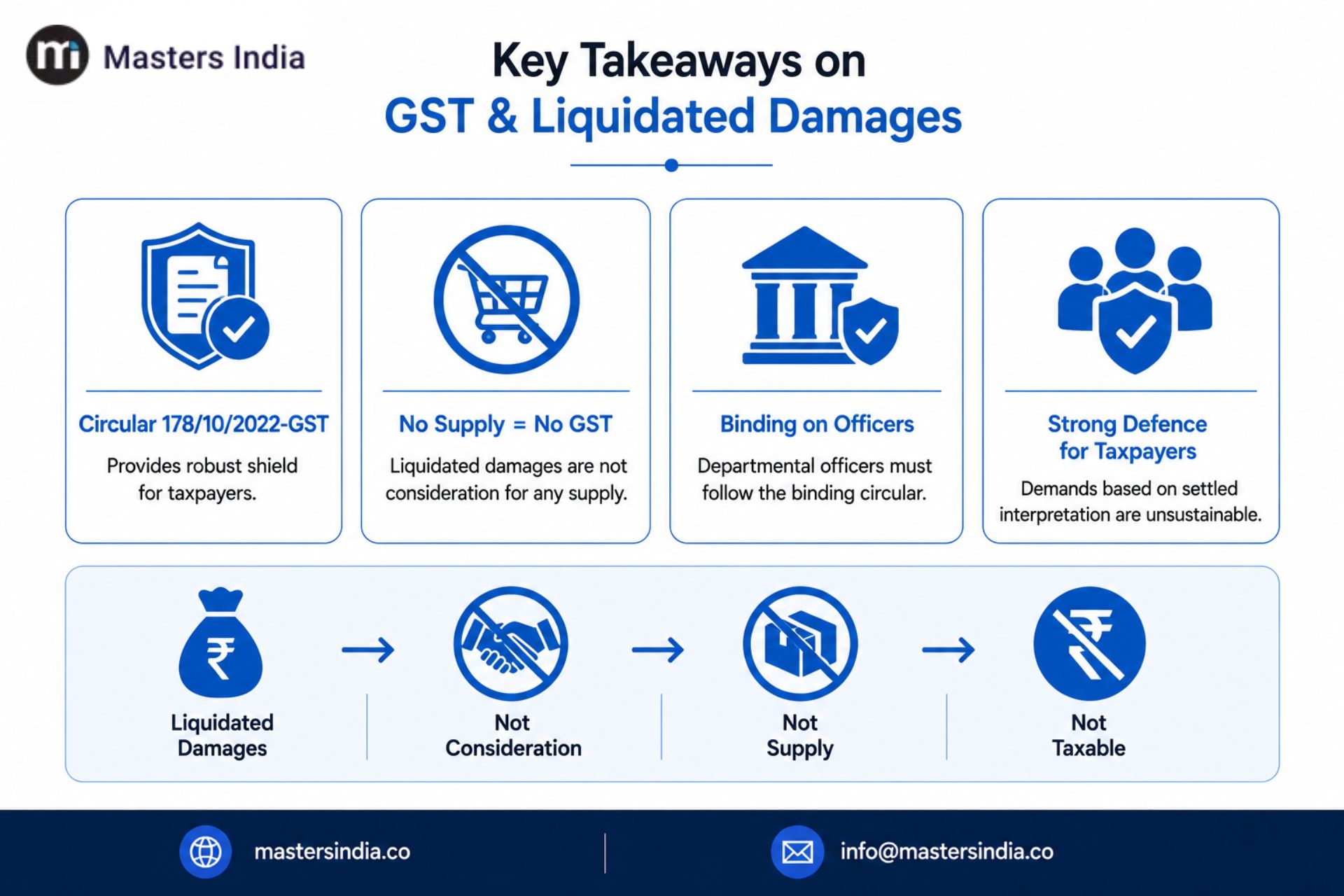

CBIC Circular No. 178/10/2022-GST dated 03.08.2022 has provided definitive guidance on this issue. It explicitly clarifies that payments such as liquidated damages, forfeiture of earnest money, or penalties for breach of contract are not consideration for tolerating a breach. They are payments for damages and fall outside the scope of supply and, therefore, are not taxable.

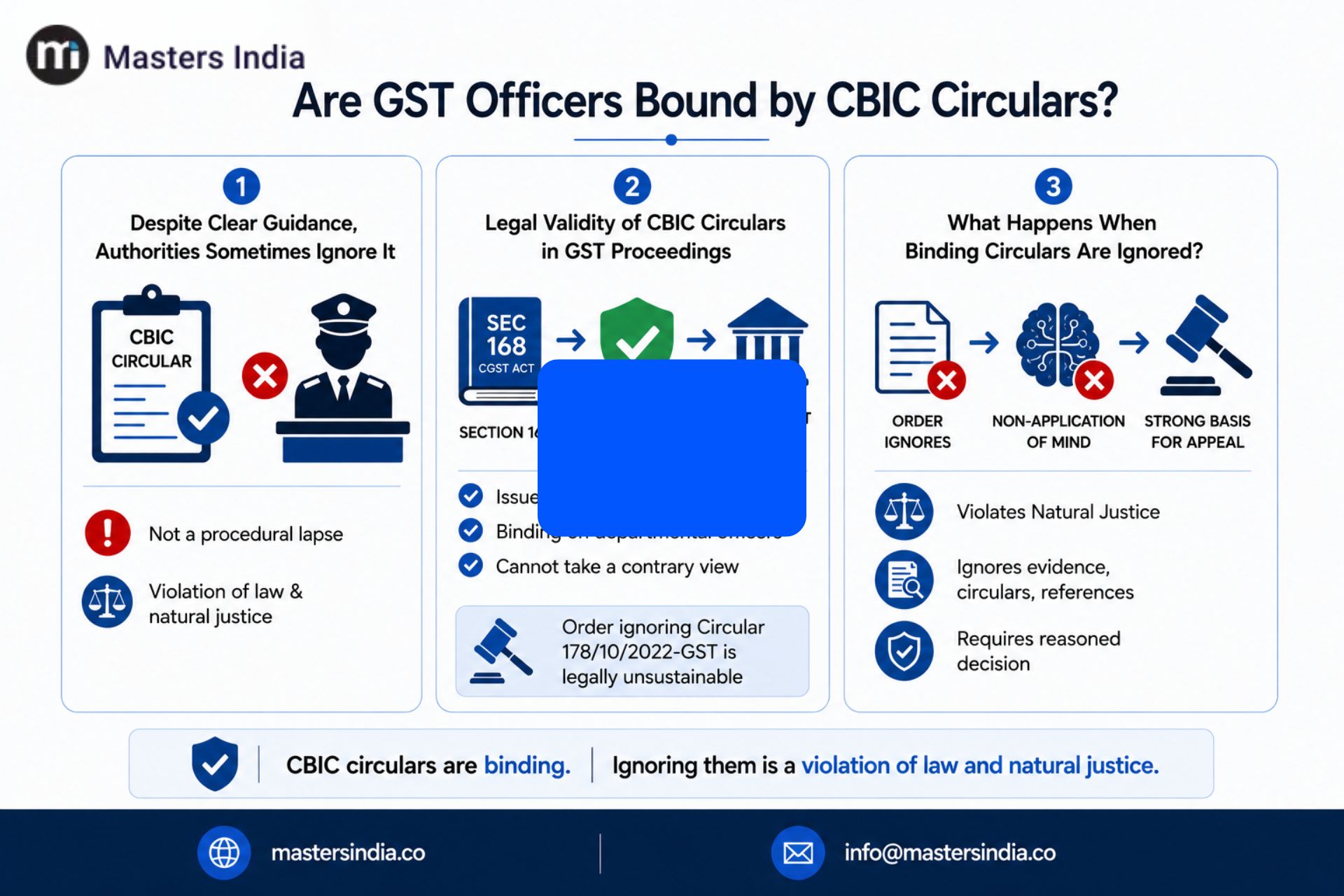

Are GST officers bound by CBIC circulars?

Despite the clear guidance, adjudicating authorities sometimes ignore detailed submissions and binding circulars. This is not merely a procedural lapse but a violation of statutory principles and natural justice.

Legal validity of CBIC circulars in GST proceedings

Circulars issued by the CBIC under Section 168 of the CGST Act are legally binding on departmental officers. An adjudicating authority, being an officer of the department, cannot take a view contrary to the one expressed in a binding circular. An order passed in ignorance of Circular No. 178/10/2022-GST is legally unsustainable on this ground alone.

What happens when binding circulars are ignored?

An order that fails to consider binding circulars, documentary evidence, or judicial references suffers from a "non-application of mind". This forms a strong basis for appeal under the framework governing GST appeals and revisions under Sections 107–121, as it violates the Principles of Natural Justice which require a reasoned and considered decision.

Can penalties and interest apply to liquidated damages?

When a demand is founded on a debatable interpretational issue that has been settled by a Board circular, the invocation of the extended period of limitation and penalties under Section 74 (fraud, wilful misstatement, or suppression of facts) is arbitrary and legally untenable.

Is interest payable on liquidated damages under GST?

Interest is compensatory in nature and is levied only when tax that is legally due has not been paid. If the principal amount of liquidated damages is not a taxable supply, the question of tax being "due" does not arise. Consequently, the levy of interest is wholly unwarranted.

Can GST penalties be imposed on liquidated damages?

A penalty is not automatic. For a penalty under Section 74 to be imposed, the department must prove the existence of mens rea or a "culpable mental state" with an intent to evade tax.

How bona fide interpretation protects taxpayers

The taxability of liquidated damages has been a subject of bona fide interpretational differences. A taxpayer's position that such amounts are not taxable, especially when supported by a binding circular, cannot be termed 'suppression of facts' or 'wilful misstatement'.

Understanding the burden of proof in penalty proceedings

As per Section 135 of the CGST Act, in any prosecution requiring a culpable mental state, the court presumes its existence. However, it is a defence for the accused to prove its absence. In penalty proceedings under Section 74, the burden is on the department to establish suppression with intent. When transactions are duly recorded in the books of account, a bona fide belief, supported by a circular, effectively rebuts any presumption of a culpable mental state.

Key takeaways on GST and liquidated damages

The clarification provided by Circular 178/10/2022-GST has created a robust shield for taxpayers. The legal position is no longer ambiguous, making a well-documented GST litigation, audit, and appeal strategy important where adjudicating authorities continue to raise demands despite settled legal principles.

For the tax professional, the strategy must be two-pronged: first, clearly establish that liquidated damages are not "consideration" for any "supply" based on the circular. Second, forcefully argue that ignoring this binding circular is a violation of statutory duty and that invoking penal provisions for a settled interpretational issue is an abuse of process.

A final thought to ponder: If the department continues to view penalties as "consideration for tolerance", could every late fee, forfeiture, or contractual penalty in the Indian economy be reframed as a taxable service? The Board's circular and subsequent judicial discipline have, for now, rightly prevented the GST law from taxing the very failure of commerce.

Are liquidated damages outside the scope of GST?

The GST treatment of liquidated damages has been a long-standing area of dispute, but the legal position has become significantly clearer following CBIC Circular 178/10/2022-GST. In most cases, liquidated damages represent compensation for a contractual breach rather than consideration for a taxable supply. As a result, businesses should carefully evaluate the nature of such payments before accepting GST demands based solely on the concept of "tolerating an act."

For tax professionals and businesses, maintaining proper contractual documentation and understanding the distinction between compensation and consideration is essential for defending their position during GST audits and departmental scrutiny as well as litigation proceedings.

Masters India helps organizations navigate complex GST issues through compliance solutions, GST software, tax technology products, and expert advisory support. Connect with our team to simplify GST compliance and manage tax disputes with confidence.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified