Judicial Analysis of the Power of Inspection, Search and Seizure

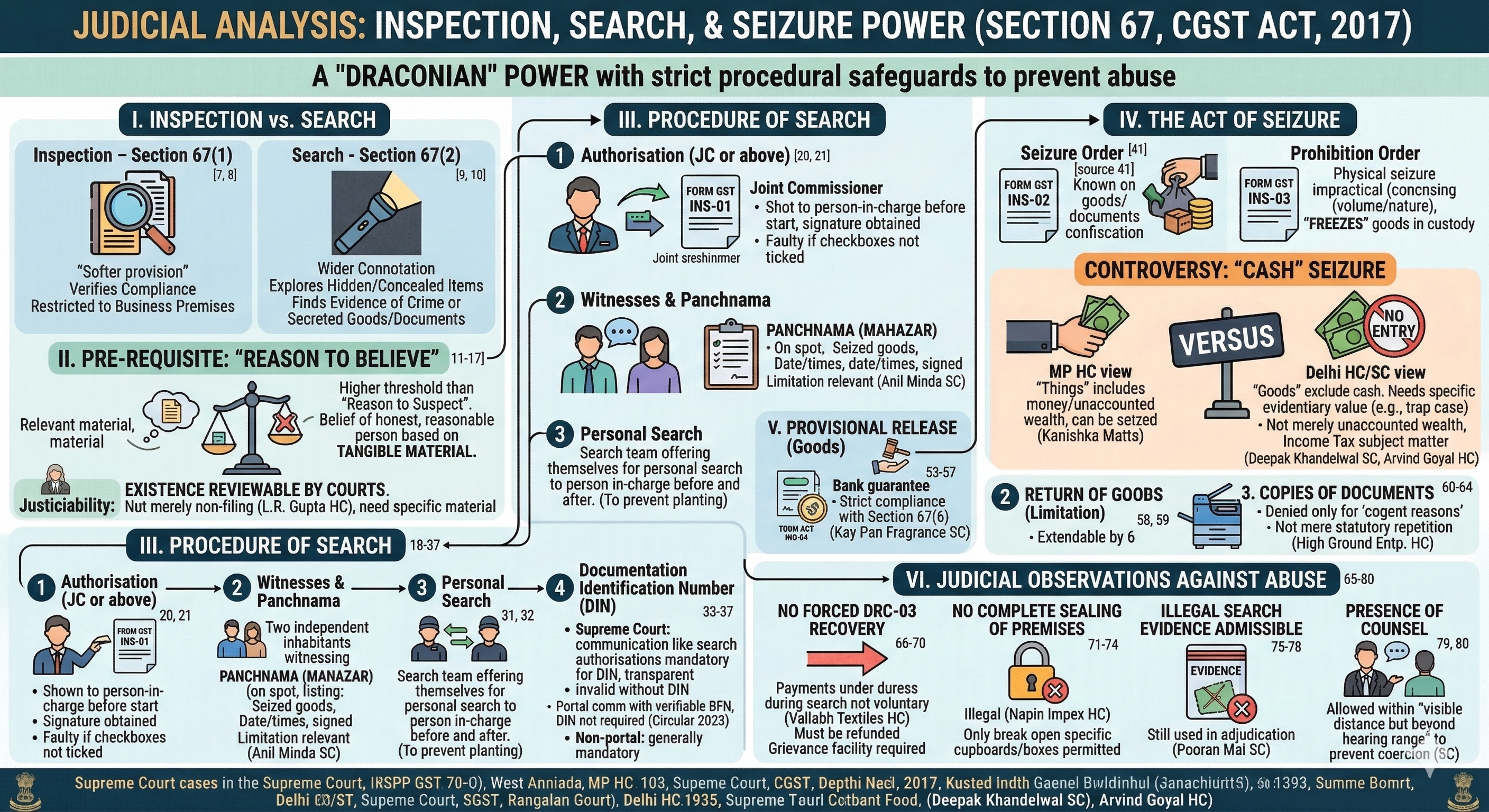

Section 67 of the CGST Act, 2017, codifies the powers of Inspection, Search, and Seizure. These are considered "draconian" powers by the courts, and therefore, the statute and judicial precedents have laid down strict procedural safeguards to prevent their abuse.

Here is a detailed note on the procedure and judicial views based on the provided sources.

I. Distinction: Inspection vs. Search

The Supreme Court in ITC Ltd. clarified the distinction between these two concepts:

-

Inspection (Section 67(1)): This is a "softer provision" used to verify compliance. It allows access to a place of business to check records. It is restricted to the business premises,.

-

Search (Section 67(2)): This has a wider connotation and implies an exploration for something hidden or concealed. It is the act of a government official examining a place, object, or person to find evidence of a crime or secreted goods/documents,.

II. The Pre-requisite: "Reason to Believe"

The validity of a search hinges on the "Reason to Believe," which is a higher threshold than "Reason to Suspect",

-

Judicial Standard: The belief must be that of an honest and reasonable person based on relevant material and circumstances, not on mere rumour, gossip, or a hunch.

-

Tangible Material: The proper officer (Joint Commissioner or above) must have information in possession to form this opinion. In L.R. Gupta\, the Delhi High Court held that merely because a person does not file a return or disclose true income is not sufficient ground for search; there must be specific material. [L.R. Gupta vs Union of India – Delhi High Court (1991) 59 Taxmann 305 :: (1992) 194 ITR 32 :: (1992) 101 CTR 179]

-

Justiciability: While the sufficiency of the reasons is not usually examined by courts, the existence of such reasons and the rational connection between the material and the belief are subject to judicial review (Rimjhim Ispat Ltd vs State of Uttar Pradesh – Allahabad High Court (2019) 73 GST 470 :: (2019) 103 taxmann.com 254 | Golden Cotton Industries vs Union of India – Gujarat High Court (2019) GST 158 :: (2019) 107 taxmann.com 128),

III. The Procedure of Search

The search must be conducted in accordance with Section 67(10) of the CGST Act read with the Code of Criminal Procedure, 1973 (CrPC).

1. Authorisation (Form GST INS-01)

-

The proper officer (Joint Commissioner or above) issues an authorisation in FORM GST INS-01.

-

Judicial View: The authorisation must be shown to the person in charge before the search starts, and their signature must be obtained on it. If the checkboxes indicating the grounds for the search in INS-01 are not ticked, the authorisation may be considered faulty.

2. Witnesses and Panchnama

-

Witnesses: The officer must call upon two or more independent and respectable inhabitants of the locality to witness the search.

-

Panchnama: A Panchnama (Mahazar) must be prepared on the spot. It must list all goods/documents seized and record the start and end time of the search. It must be signed by the witnesses, the owner, and the officers,.

-

Limitation Relevance: The Supreme Court in Anil Minda held that for block assessments, the limitation period is calculated from the date of the last Panchnama drawn, not the last authorisation. [Anil Minda vs Commissioner of Income Tax – Supreme Court (2023) 292 Taxmann 407 (SC)]

3. Personal Search

-

To prevent allegations of planting evidence, the search team must offer themselves for personal search to the person in-charge before starting and after concluding the search,.

4. Documentation Identification Number (DIN)

-

The Supreme Court in Pradeep Goyal emphasised that all communications (including search authorisations) must carry a computer-generated DIN to ensure transparency. Communications without DIN are invalid.

-

Note: Circular 249/06/2025-GST dated 09-Jun-2025: a) Communication through portal- If the document bears a verifiable RFN, DIN is not required; RFN alone suffices and the document is validly served under section 169. b) Communication outside portal (manual, e-office, email, physical letters etc.)- DIN continues to be generally mandatory in terms of Circulars 122/41/2019-GST and 128/47/2019-GST, subject to specific exemptions in those circulars (e.g., technical difficulties, exigent situations with post-facto recording, etc.).

IV. The Act of Seizure

Seizure is the taking of possession of goods or documents by the department.

1. Seizure Order (Form GST INS-02)

-

If goods liable for confiscation or relevant documents are found, the officer issues an order of seizure in FORM GST INS-02.

2. Prohibition Order (Form GST INS-03)

-

Where it is not practicable to physically seize goods (due to volume or nature), the officer may serve an order of prohibition in FORM GST INS-03. This "freezes" the goods in the custody of the owner, prohibiting them from dealing with the goods without permission,.

3. The Controversy of "Cash" Seizure Courts are divided on whether "Cash" found during a search can be seized as "goods" or "things" under Section 67(2).

-

Can be Seized: The Madhya Pradesh High Court in Kanishka Matta held that the word "things" includes money, and it can be seized if it represents unaccounted wealth. Smr. Kanishka Matta vs Union of India - Madhya Pradesh High Court [(2020) 120 taxmann.com 174]

-

Cannot be Seized: The Delhi High Court in Deepak Khandelwal and Arvind Goyal held that cash is explicitly excluded from the definition of "goods" under GST. Unless the currency has specific evidentiary value (e.g., marked notes in a trap case), it cannot be seized merely as "unaccounted wealth," which is a subject matter for the Income Tax Department. Deepak Khandelwal vs Commissioner of CGST – Delhi High Court [(2023) 153 taxmann.com 443 was upheld by Hobourable Supreme Court in Commissioner of CGST vs Deepak Khandelwal (2024) 165 taxmann.com 715 (SC) :: (2024) 89 GSTL 934 (SC). Arvind Goyal CA vs Union of India – Delhi High Court (2023) 151 taxmann.com 228 :: (2023) 98 GST 587 (Del.)]

V. Post-Seizure Rights and Procedures

1. Release of Goods (Provisional)

-

Seized goods can be released provisionally upon execution of a bond (FORM GST INS-04) and furnishing security (Bank Guarantee) or payment of applicable tax, interest, and penalty,.

-

The Supreme Court in State of U.P. v. Kay Pan Fragrance ruled that High Courts should not order the release of seized goods without insisting on the statutory compliance of Section 67(6) (i.e., furnishing security/bond). The mechanism in the Act must be strictly followed. State of Uttar Pradesh vs Kay Pan Fragnace Pvt. Ltd. – Supreme Court [(2019) 112 taxmann.com 81 (SC) :: (2019) 31 GSTL 385(SC)]

2. Return of Goods (Limitation)

-

If a Show Cause Notice (SCN) is not issued within six months (extendable by another 6 months) of the seizure, the goods must be returned to the person.

3. Copies of Documents

-

The person from whom documents are seized has a right to make copies or take extracts. This can be denied only if the officer believes it will prejudicially affect the investigation,.

-

In High Ground Entp., the Bombay High Court held that there must be "cogent reasons" to deny copies; a mere repetition of the statutory language is insufficient. High Group Enterprises Ltd. vs Union of India – Bombay High Court (2019) 110 taxmann.com 445

VI. Critical Judicial Observations on Abuse of Power

1. Forced Recovery (DRC-03)

-

Officers often pressure taxpayers to make "voluntary" payments via Form DRC-03 during the search to avoid arrest or seizure.

-

Court View: The Delhi High Court in Vallabh Textiles held that payments made under coercion/duress during search (e.g., at odd hours) are not voluntary. Such amounts must be refunded,. The Gujarat High Court has directed that facilities to file grievances against such coercion must be available. Vallabh Textiles vs Senior Intelligence Officer – Delhi High Court (2022) 145 taxmann.com 596. Bhumi Associate vs Union of India – Gujarat High Court (2021) 124 taxmann.com 429

2. Sealing of Premises

-

Court View: In Napin Impex, the Delhi High Court held that the complete sealing of business premises is per se illegal. Section 67(4) only authorises breaking open or sealing specific cupboards/boxes where access is denied, not the shutting down of the entire business. Napin Impex Pvt. Ltd. vs Commissioner of DGST, Delhi – Delhi High Court (2018) 98 taxmann.com 462 :: (2018) 19 GSTL 578 (Del.)

3. Admissibility of Evidence from an Illegal Search

-

Relying on the Supreme Court judgment in Pooran Mal, courts have held that even if a search is illegal (procedural lapse), the evidence collected during such a search is not inadmissible. It can still be used against the assessee in adjudication. Pooran Mal vs Director of Inspection – Supreme Court (1974) 93 ITR 505 (SC)

4. Presence of Counsel

-

While a lawyer cannot interfere in the interrogation, the Supreme Court has allowed counsel to be present within "visible distance but beyond hearing range" during recording of statements to prevent coercion.

Need of GST in India | Powers of GST Officers | GST Audit Procedure | GST Audit Procedure | GST penalty under section 74

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified