ISD - Distribution of Common Input Tax Credit - Budgetary Amendment of 2024

Considering the recommendations made by the 50th and 52nd Goods and Services Tax (GST) Council meetings, in the Union Budget of 2024, the government has introduced certain amendments streamlining the Input Service Distributor (ISD) mechanism.

The GST Council, in its 50th meeting, recommended making the ISD mechanism mandatory for the distribution of input tax credit (ITC) for common services procured from third parties to distinct persons (i.e., establishments having multiple GSTINs registered under the same PAN). In continuation to the above, the council at the 52nd meeting recommended amendments to Sections 2(61) and 20 of the CGST Act, 2017 (the CGST Act), and the amendment to Rule 39 of the CGST Rules, 2017 (the CGST Rules).

In this article, we have analysed the Impact of Budgetary Amendment 2024 on ISD and common ITC in terms of the ITC distribution mechanism, cost allocation of various common services, services covered under the Reverse Charge Mechanism (RCM), credit distribution methods, internally generated services, and registration requirements aspects through the case study.

Case study

For example, ABC Co. Pvt. Ltd. (Company ABC) has its HO located in Delhi and branch offices located in the states of Gujarat, Rajasthan, Karnataka, and Maharashtra. All branches and HO are distinct persons having different GSTINs registered under the same PAN issued in the name of ABC Co. Pvt. Ltd. During the current year, the Karnataka branch office was not operating. Now, the HO of ABC Co. Pvt. centrally sources legal services from advocates. The cost of these services is attributable to each entity since all branches, including HO, are the beneficiaries of services. As per the GST law, tax is liable to be paid by the recipient of services RCM.

Can ITC Paid by the Company ABC Under RCM Be Distributed to a Beneficiary of Services?

The proposed budgetary amendment to the definition of ISD as provided under Section 2(61) of the CGST Act, allows the ISD to distribute the ITC in respect of common services paid under RCM (RCM has been prescribed under Sections 9(3) and 9(4) of the CGST Act).

Hence, the taxes paid by Company ABC under RCM for centrally procuring legal services can be distributed to the beneficiaries of services in a manner provided in Section 20 of the CGST Act.

What Are the Different Methods For Distributing Common ITC?

As per Circular No. 199/11/2023 dated 17 July 2023, the HO at its discretion may distribute the ITC to branch offices in respect of common input services procured from the third party by HO attributable to branches as per below mentioned two methods:

Cross-charge Method

HO can issue fresh tax invoices under Section 31 of the CGST Act to the concerned branch offices in respect of common input services procured to recover the taxes paid by HO to the third party.

ISD Mechanism

HO can distribute ITC in respect of common input services procured through the ISD mechanism as per provisions of Section 20 of the CGST Act read with Rule 39 of the CGST Rules.

However, the recent amendment in Section 20 of the CGST Act partially overrides the above circular which has mandated HO to distribute the ITC in respect of common input services received from third parties through the ISD mechanism.

Hence, in our case, HO of Company ABC has to distribute the taxes paid under RCM for the legal services availed through the ISD mechanism and cannot use the cross-charge method used earlier as a common trade practice.

Who Bears the ITC of Common Input Services?

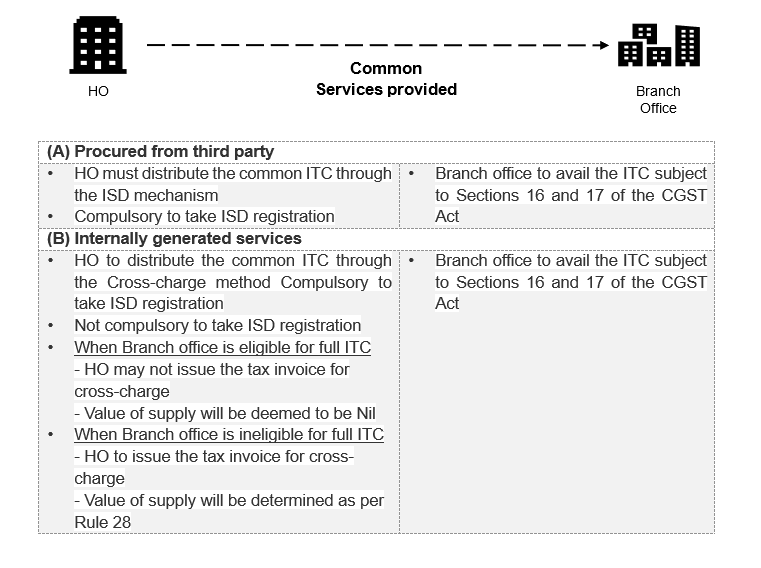

As per the prevalent provisions of the CGST Act read with Rule 39 of the CGST Rules and the above Circular, HO can distribute the ITC for common input services procured from a third party only if the said input services are attributable to or have been provided to the operating branch offices. The branch office can then avail ITC on the same subject to the provisions of Sections 16 and 17 of the CGST Act.

The GST Council in its 52nd meeting also recommended to amend Rule 39 of the CGST Rules. However, the amended rules for distribution are yet to be notified. These may consider factors like branch turnover and location for the fair and appropriate allocation.

Is It Compulsory to Obtain ISD Registration for Company ABC to Distribute the Common ITC?

As per the above Circular, it was not mandatory to obtain ISD registration to distribute the common ITC. The HO as per its discretion may not take ISD registration and follow the cross-charge method to distribute the common ITC which is common trade practice.

However, as per the amended Section 20 of the CGST Act, HO must distribute the ITC in respect of common input services received from third parties through the ISD mechanism and obtain ISD registration as per clause (viii) of Section 24 of the CGST Act.

Therefore, Ho of the Company ABC in our case is required to obtain registration as ISD to distribute the common ITC of legal services.

Who Is Liable to Pay Taxes for the Common Input Services Covered Under RCM?

In our example, it is the HO of the Company ABC that centrally procures the legal services and hence the HO will be liable to pay the full amount of tax under RCM.

What Will Be the Taxability of Internally Generated / In-House Common Services?

As a common trade practice, HO may provide certain central functions such as accounting, payroll, human resources, IT, etc. by deploying the common resources internally. The cost of these functions is attributable to the branch offices being beneficiaries of services. Further, as per the Circular mentioned above, the cross-charge method can be followed to distribute ITC.

As per Schedule I of the CGST Act such services are taxable services and the value of supply for such services made by HO to the branch offices is determined as per Rule 28 of the CGST Rules. As per Rule 28(a), the value of the supply of goods or services or both between distinct persons shall be the open market value of such supply. The second proviso to rule 28 of the CGST Rules provides that where the recipient is eligible for full ITC, the value declared in the invoice shall be deemed to be the open market value of the services.

From the above, we can say that if branch offices are eligible for the full ITC of the attributable tax portion of internally generated common services, HO may not at all issue the tax invoice for the services rendered by HO to the branch offices. In such a scenario, the value of services may be deemed to be Nil and assumed to be an open market value in terms of the second proviso to Rule 28 of the CGST Rules. However, if the recipient is ineligible for full ITC of the attributable tax portion of internally generated common services, HO is required to issue tax invoices to the branch offices for providing such service declaring the taxable value of supply as open market value as per Rule 28.

Conclusive Summary

We can summarise the credit distribution of the ITC for common input services provided by a registered person to distinct persons as follows:

|

(A) Procured from third party |

|

|

|

|

|

|

(B) Internally generated services |

|

|

|

|

|

|

|

|

|

Frequently Asked Questions

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified