An Analysis within the Framework of Sections 54–58 of the CGST Act

1. Introduction

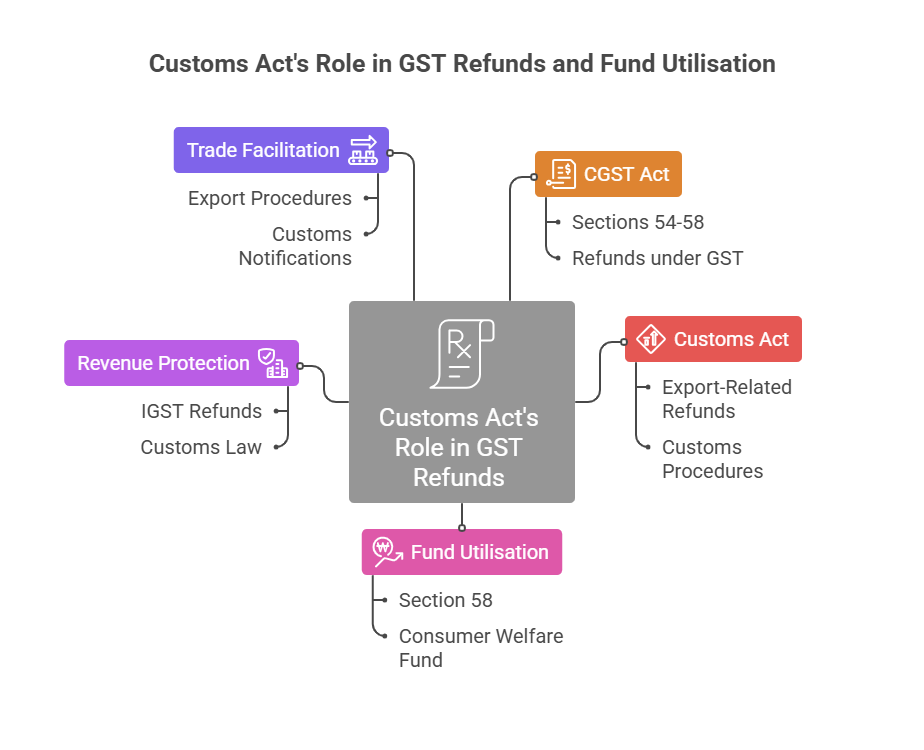

Chapter XII of the Central Goods and Services Tax Act, 2017, comprising Sections 54 to 58, governs the law relating to refunds under GST. While these provisions primarily deal with eligibility, procedure, interest, unjust enrichment, and fund utilisation, an important practical dimension emerges in export-related refunds, where the GST law operates in close coordination with the Customs Act, 1962.

Although Section 58 of the CGST Act, titled “Utilisation of Fund”, does not expressly incorporate provisions of the Customs Act, the refund mechanism under GST—particularly IGST refunds on exports—is deeply intertwined with Customs law, procedures, and determinations. This inter-statutory dependency is central to revenue protection and trade facilitation.

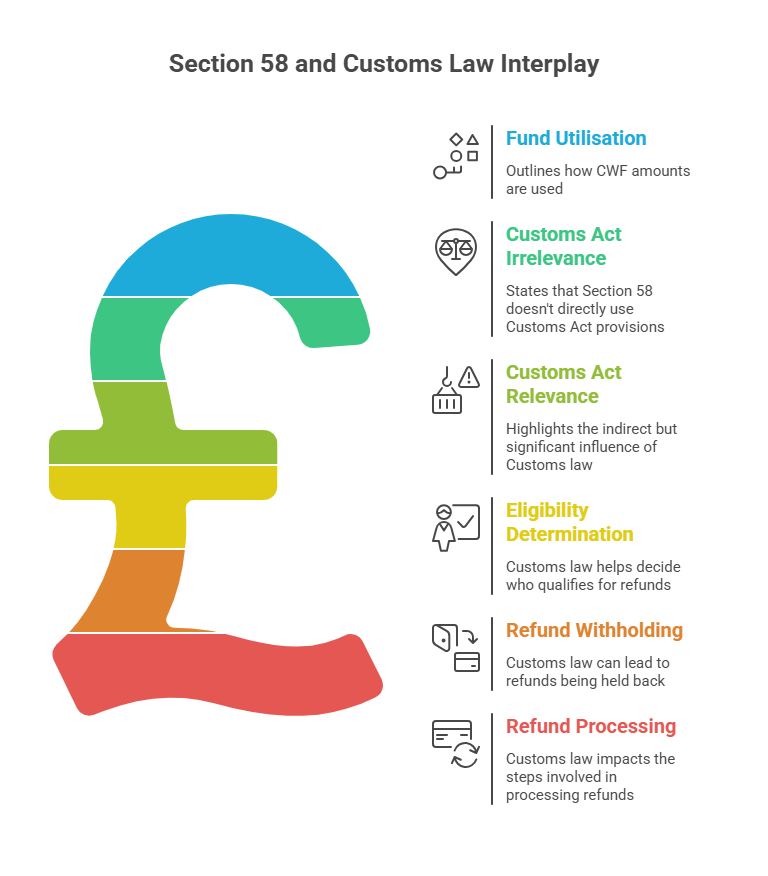

2. Scope of Section 58 – Utilisation of Consumer Welfare Fund

Section 58 provides for the manner in which amounts credited to the Consumer Welfare Fund (CWF) are to be utilised. The provision is limited in scope and does not directly borrow or apply any provision of the Customs Act, 1962.

However, this does not imply that Customs law is irrelevant to the refund framework under GST. On the contrary, Customs law plays a decisive role in determining eligibility, withholding, and processing of export-related refunds, which ultimately impacts whether amounts are sanctioned, withheld, or credited to the CWF.

3. Withholding of IGST Refunds Due to Customs Act Violations

(Rule 96 of the CGST Rules)

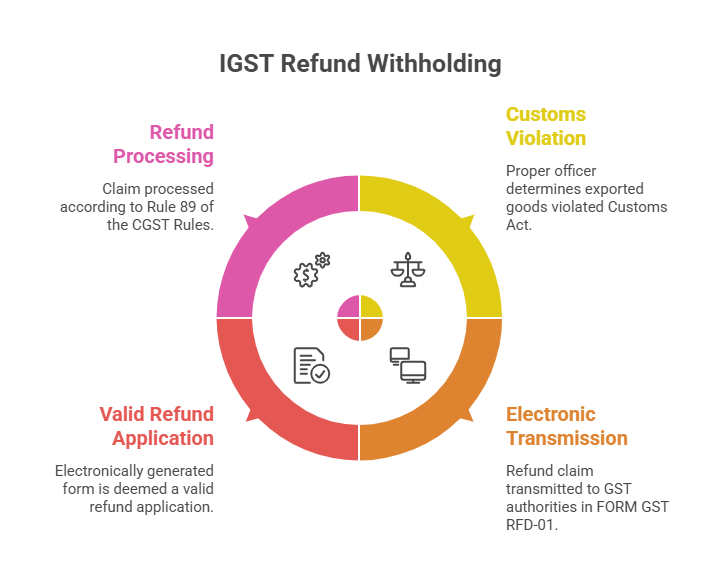

Rule 96 governs the refund of IGST paid on exports of goods or services. A crucial link between GST refunds and the Customs Act is found in Rule 96(4)(b), which empowers withholding of refunds where:

-

The proper officer of Customs determines that exported goods were in violation of the provisions of the Customs Act, 1962.

-

Upon confirmation of such violation, the refund claim is electronically transmitted to the GST authorities in system-generated FORM GST RFD-01.

-

This electronically generated form is deemed to be a valid refund application as of the date of its transmission.

-

The claim is thereafter processed in accordance with Rule 89 of the CGST Rules, which prescribes the general refund procedure.

This mechanism clearly demonstrates that Customs adjudication directly influences the fate of GST refund claims, establishing a functional overlap between the two statutes.

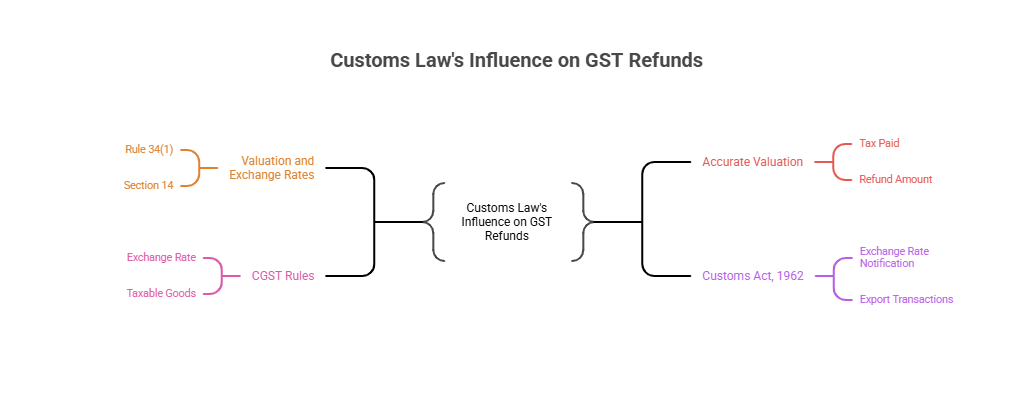

4. Valuation and Exchange Rates – Customs Law as the Reference Point

Although valuation provisions do not fall strictly within Sections 54–58, they have a direct bearing on refund computation.

-

Rule 34(1) of the CGST Rules mandates that the exchange rate for valuation of taxable goods shall be the rate notified under Section 14 of the Customs Act, 1962.

-

This ensures uniformity and consistency in valuation, especially in export transactions where foreign currency is involved.

-

Accurate valuation is fundamental to determining the correct quantum of tax paid and, consequently, the refund amount.

Thus, Customs law indirectly but decisively shapes GST refund outcomes.

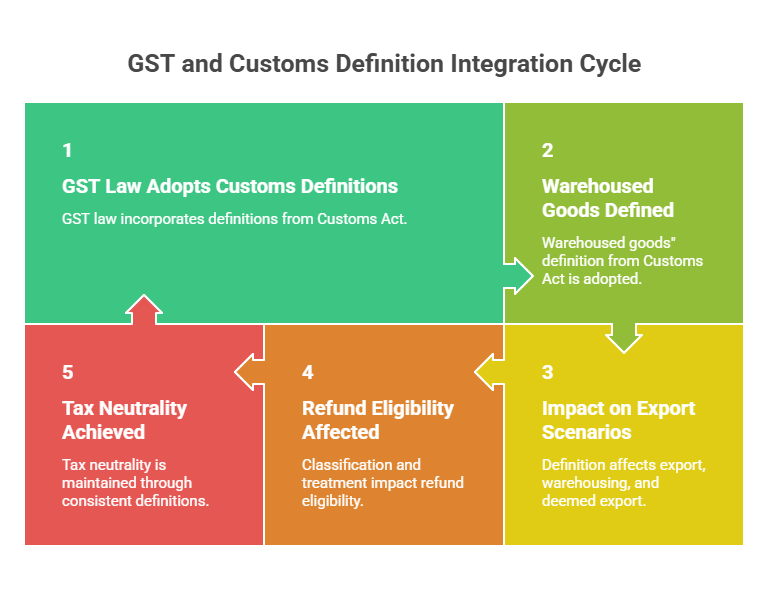

5. Adoption of Customs Act Definitions under GST

The GST law expressly adopts certain definitions from the Customs Act:

-

Explanation 2 to Paragraph 8 of Schedule III to the CGST Act provides that the term “warehoused goods” shall have the same meaning as assigned under the Customs Act, 1962.

This incorporation assumes significance in export, warehousing, and deemed export scenarios, where the classification and treatment of goods can affect refund eligibility and tax neutrality.

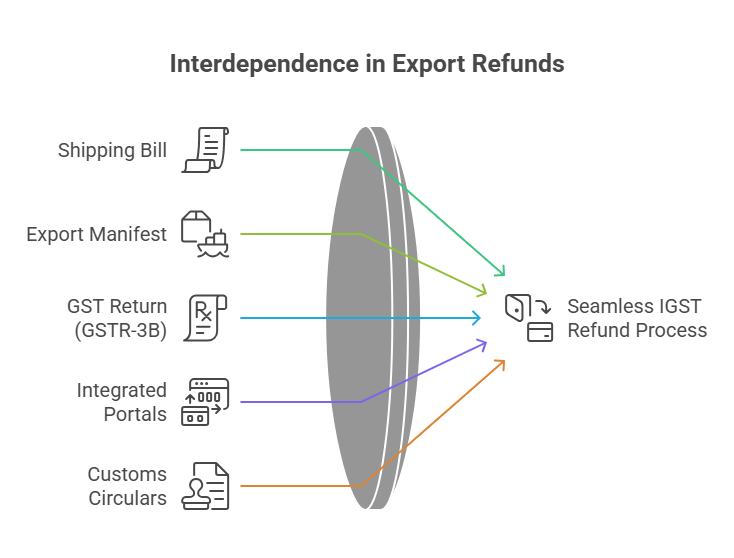

6. Export Procedures and IGST Refunds – Operational Interdependence

The export refund mechanism under GST is operationally anchored in Customs procedures:

-

The shipping bill filed with Customs is treated as the application for refund of IGST paid on exported goods.

-

The refund process is triggered only upon:

-

Filing of the export manifest or export report, and

-

Furnishing of a valid GST return (GSTR-3B) by the exporter.

-

-

The GST and Customs portals are electronically integrated, enabling seamless data exchange.

-

Customs authorities process refund claims upon validation of GST return filing from the common portal.

Further, numerous Customs circulars and instructions govern:

-

Invoice mismatches,

-

Export General Manifest (EGM) errors,

-

Verification protocols,

-

Withholding of refunds due to higher drawback claims or procedural discrepancies.

These administrative instruments underscore the continuous reliance of the GST refund system on Customs data, controls, and compliance checks.

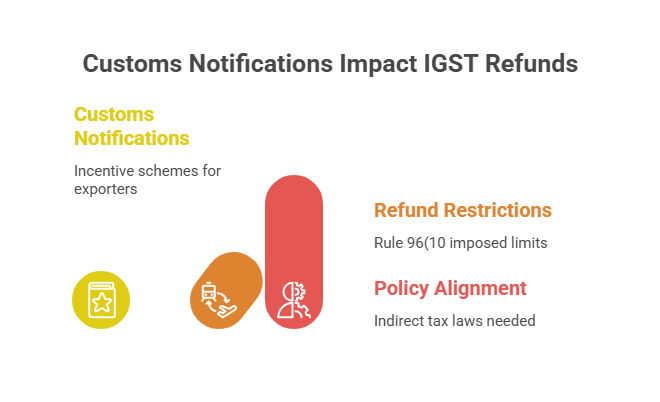

7. Impact of Customs Notifications and Export Incentive Schemes

Historically, Rule 96(10) imposed restrictions on IGST refunds where exporters availed benefits under certain Customs notifications (such as Advance Authorisation, EPCG, or EOU schemes).

Although many of these restrictions have since been amended or omitted, their existence illustrates how:

-

Customs incentive structures directly influenced GST refund eligibility, and

-

Policy alignment between indirect tax laws was necessary to prevent double benefits.

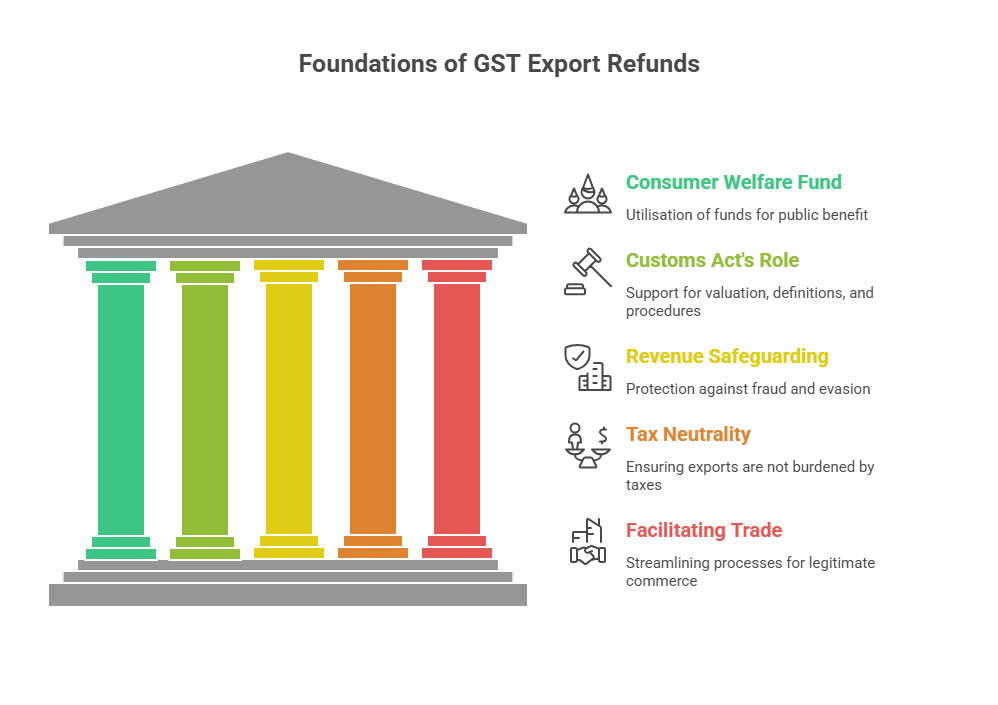

8. Conclusion

While Section 58 of the CGST Act, dealing with utilisation of the Consumer Welfare Fund, operates independently and does not expressly refer to the Customs Act, the broader refund framework under Sections 54–58—particularly in export cases—is inseparable from Customs law.

From valuation and definitions to refund withholding and procedural validation, the Customs Act, 1962 acts as a foundational pillar supporting the GST export refund ecosystem. This interdependence is essential for:

-

Safeguarding revenue,

-

Ensuring tax neutrality in exports, and

-

Facilitating legitimate trade through coordinated administration.

Need for GST in India | Powers of GST Officers | UQC Code in GST | Cookies New GST Rate | DRC-01 | GST Audit Procedure | GST ADT-01

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified