Strategic Implications of India’s GST 2.0 Rate Reform on Key Sectors

Executive Summary: What Leadership Needs to Do Now

India's Next Generation GST reforms, effective September 22, 2025, represent the most significant tax restructuring since GST implementation in 2017. Immediate action required: Update all billing systems, reconcile inventory, and reassess pricing strategies before the October 31 compliance deadline.

Key Strategic Imperatives:

-

Agriculture & FMCG leaders: Capitalise on 8-15% cost reductions to drive market expansion

-

Automotive executives: Leverage 28%→18% rate cuts to accelerate affordable vehicle penetration

-

Healthcare & Insurance CFOs: Exploit zero GST rates to scale insurance adoption and medical device access

-

Infrastructure companies: Fast-track projects using 28%→18% cement cost advantages

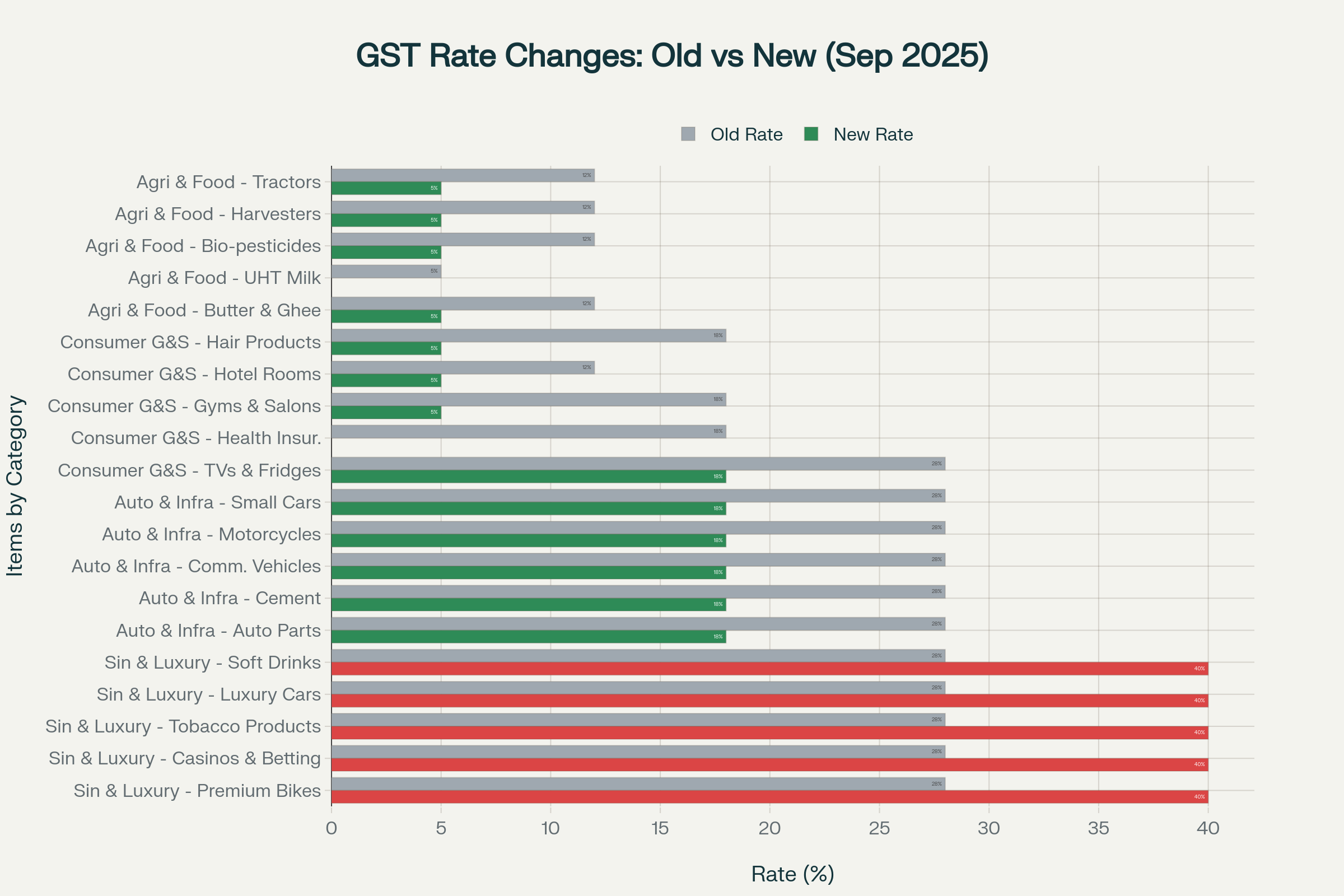

GST Rate Structure Transformation: Old vs New Rates Effective September 22, 2025

Transformation Overview: From Complex to Simple

The GST Council's 56th meeting on September 3, 2025, approved a revolutionary shift from the four-tier structure (5%, 12%, 18%, 28%) to a simplified two-slab system (5% and 18%), with a new 40% rate for luxury and sin goods. This "GST 2.0" framework addresses eight years of compliance complexity while boosting consumption through strategic rate reductions.

Core Changes Effective September 22, 2025:

-

99% of items in the 12% slab moved to 5.%

-

90% of items in the 28% slab moved to 18%

-

New 40% slab introduced for luxury cars, tobacco, and aerated beverages.

-

Zero GST on health/life insurance, UHT milk, educational essentials.

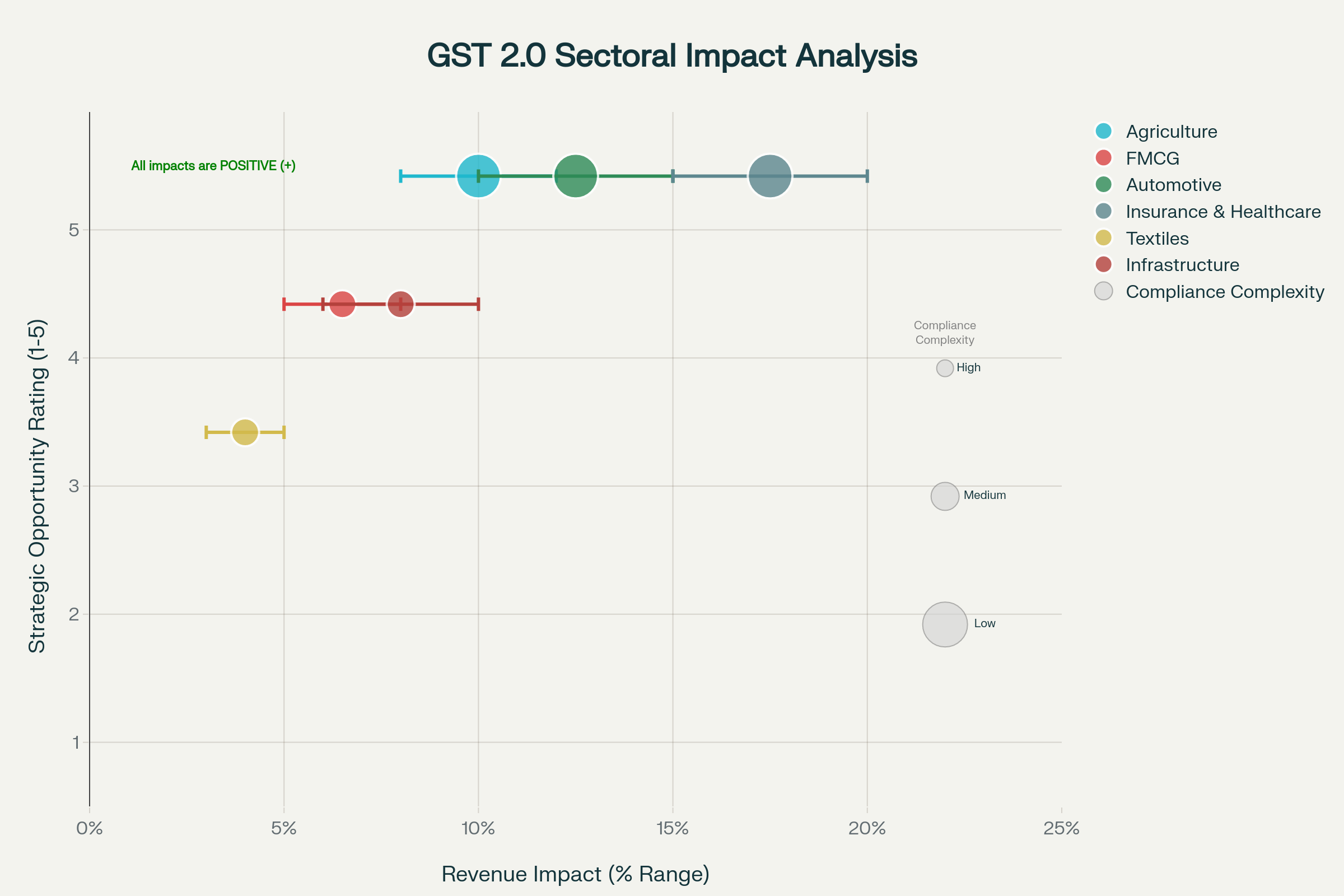

Deep Dive: Sectoral Impact Analysis

Strategic Sectoral Impact Analysis: GST 2.0 Reforms on Key Industry Segments

Agriculture Sector: Mechanisation Accelerated

The agriculture sector emerges as the biggest winner with comprehensive rate reductions driving mechanisation and productivity gains.

Key Rate Changes:

-

Tractors: 12% → 5% (58% tax reduction).

-

Harvesters, threshers, sprinklers: 12% → 5%.

-

Bio-pesticides and natural menthol: 12% → 5%.

-

Drip irrigation systems: 12% → 5%.

-

Revenue Impact: Expected 8-12% increase in agricultural equipment sales.

Strategic Actions for Leadership:

-

Accelerate mechanisation programs targeting small and marginal farmers

-

Expand rural dealer networks to capture increased demand

-

Develop financing partnerships for equipment purchases

-

Launch awareness campaigns on sustainable farming benefits

-

Compliance Challenges: Minimal, with simplified rate structure reducing classification disputes.

FMCG Sector: Mass Market Expansion

FMCG companies benefit from significant input cost reductions across daily essentials, driving volume growth in price-sensitive markets.

Key Rate Changes:

-

Hair oil, shampoo, toiletries: 18% → 5%.

-

Butter, ghee, cheese: 12% → 5%.

-

Processed foods, packaged juices: 12% → 5%.

-

Tableware, kitchenware: 12% → 5%.

-

Revenue Impact: 5-8% boost in volumes through affordability gains.

Strategic Actions for Leadership:

-

Optimise product portfolios to leverage lower-taxed categories

-

Expand mass market offerings targeting bottom-of-the-pyramid consumers

-

Recalibrate supply chains for cost efficiency

-

Accelerate rural penetration strategies

-

New Opportunities: Lower logistics costs from 28%→18% commercial vehicle rates enable distribution expansion.

Automotive Sector: Affordable Mobility Revolution

The automotive industry experiences transformational rate cuts across passenger and commercial vehicles, opening new market segments.

Key Rate Changes:

-

Small cars (≤1200cc petrol, ≤1500cc diesel): 28% → 18%

-

Motorcycles ≤350cc: 28% → 18%.

-

Commercial vehicles, buses, trucks: 28% → 18%.

-

All auto components: 28% → 18%.

-

Luxury cars and SUVs: 28% → 40% (strategic differentiation).

-

Revenue Impact: 10-15% volume growth anticipated across affordable segments.

Strategic Actions for Leadership:

-

Launch aggressive, affordable vehicle campaigns targeting first-time buyers

-

Restructure dealer margins to pass through tax benefits

-

Accelerate electric vehicle adoption (retained at 5% GST).

-

Expand commercial vehicle financing for MSME fleet expansion

-

Compliance Considerations: Clear vehicle classification reduces disputes, but inventory reconciliation is critical for the transition period.

Insurance & Healthcare: Universal Access Catalyst

Healthcare and insurance sectors receive unprecedented support through complete GST exemptions and rate reductions.

Key Rate Changes:

-

Individual health and life insurance: 18% → 0% (complete exemption).

-

Life-saving medicines: Various → 0%.

-

Medical devices (thermometers, glucometers): 12% → 5%.

-

Diagnostic kits: 12% → 5%

-

Revenue Impact: 15-20% increase in insurance penetration expected.

Strategic Actions for Leadership:

-

Launch mass market insurance products targeting underinsured segments

-

Scale up manufacturing of medical devices for domestic and export markets

-

Develop telemedicine platforms leveraging affordability improvements

-

Partner with government schemes for universal healthcare initiatives

-

Market Opportunity: India's low insurance penetration (4% of GDP) presents a massive growth potential with a zero tax burden..

Textiles Sector: Export Competitiveness Enhanced

Textile manufacturers gain competitive advantages through strategic input cost reductions, particularly benefiting MSME-dominated segments.

Key Rate Changes:

-

Man-made fibers and yarn: 18%/12% → 5%.

-

Handicrafts and artisan goods: Various → 5%.

-

Readymade garments under ₹1,000: Remain exempt.

-

Revenue Impact: 3-5% improvement in export competitiveness.

Strategic Actions for Leadership:

-

Boost export marketing leveraging cost advantages

-

Invest in sustainable textile technologies

-

Strengthen MSME supply chains for artisan products

-

Develop premium product lines to capture higher margins

-

Challenge: Moderate compliance complexity requires careful fiber cost advantage realization.

Infrastructure Sector: Construction Cost Relief

Infrastructure development receives significant impetus through reduced material costs, accelerating project execution.

Key Rate Changes:

-

Cement: 28% → 18%.

-

Construction materials: 28% → 18%.

-

Commercial goods vehicles: 28% → 18%.

-

Revenue Impact: 6-10% reduction in project costs expected.

Strategic Actions for Leadership:

-

Fast-track pending projects using cost advantages

-

Renegotiate project contracts to capture material cost benefits

-

Expand affordable housing portfolios

-

Invest in sustainable construction technologies

Compliance Challenges and Implementation Roadmap

| Action Item | Priority | Timeline | Responsible Team | Key Risks |

| Update ERP/Billing Software | High | By Sept 21, 2025 | IT/Finance | System downtime |

| Revise Rate Master in Systems | High | By Sept 21, 2025 | Finance | Rate errors |

| Reconcile Opening Stock | High | By Sept 22, 2025 | Operations/Finance | ITC reversal |

| Review Pending ITC Claims | High | By Sept 30, 2025 | Finance | Cash flow impact |

| Update Customer Contracts | Medium | By Oct 15, 2025 | Legal/Sales | Contract disputes |

| Revise Pricing Strategy | Medium | By Oct 15, 2025 | Finance/Sales | Margin erosion |

| Train Finance Team | High | By Sept 25, 2025 | HR/Finance | Compliance errors |

| Review Supplier Agreements | Medium | By Oct 31, 2025 | Procurement | Supply disruption |

| Update Compliance Calendar | Low | By Oct 15, 2025 | Finance | Penalty exposure |

| Prepare Transition Documentation | Medium | By Oct 31, 2025 | Finance | Audit issues |

| Review Input Tax Credit Eligibility | High | By Sept 30, 2025 | Finance | Blocked credits |

| Update Invoice Templates | Medium | By Sept 21, 2025 | IT/Finance | Invoice errors |

| Assess Working Capital Impact | High | By Oct 15, 2025 | Finance | Liquidity crunch |

| Review Refund Claims | Medium | By Oct 31, 2025 | Finance | Refund delays |

| Validate HSN Code Mapping | High | By Sept 21, 2025 | Finance | Classification disputes |

Critical Action Items for CFOs

Immediate Actions (By September 21, 2025):

-

Update ERP and billing software with new rate structures.

-

Validate HSN code mapping for reclassified items.

-

Revise rate master files across all systems.

Post-Implementation Actions (September 22 - October 31, 2025):

-

Reconcile opening stock with new tax rates.

-

Review pending Input Tax Credit claims.

-

Assess working capital impact from rate changes.

Input Tax Credit Management

Critical ITC Reversal Scenarios:

-

Rate reduction inventory: Goods purchased at higher rates require careful ITC reconciliation

-

Classification changes: Items moving between slabs need ITC adjustment.

-

Blocked credits: Section 17(5) restrictions remain applicable.

ITC Reversal Formula for Common Credits:

-

D1 (Exempt supply reversal): (E÷F) × C2, where E = exempt supplies, F = total turnover.

-

D2 (Non-business use): 5% of common credit C2.

Technology and Process Upgrades

System Requirements:

-

Real-time invoice matching capabilities.

-

AI-driven anomaly detection for compliance.

-

Automated GST return pre-filling.

Training Imperatives:

-

Finance team education on new rate structures.

-

Vendor communication on revised rates.

-

Customer contract renegotiation protocols.

Strategic Opportunities and New Business Models

| Sector | Key Opportunity | Revenue Impact | Implementation Challenge | Strategic Action Required |

| Agriculture | Lower machinery costs drive mechanization | 8-12% | Working capital adjustment | Accelerate mechanization programs |

| FMCG | Reduced input costs boost margins | 5-8% | Supply chain recalibration | Optimize product portfolio |

| Automotive | Affordable vehicles expand market | 10-15% | Dealer margin restructuring | Expand affordable vehicle range |

| Insurance | Zero GST increases penetration | 15-20% | Product repricing complexity | Launch penetration campaigns |

| Healthcare | Lower device costs improve access | 12-18% | Procurement cost benefits | Scale up device manufacturing |

| Textiles | Export competitiveness improved | 3-5% | Fiber cost advantage realization | Boost export marketing |

| Infrastructure | Construction cost reduction | 6-10% | Project cost renegotiation | Fast-track project execution |

| Hospitality | Budget travel segment growth | 8-12% | Pricing model revision | Target budget segments |

| Education | Educational tools become affordable | 5-8% | Procurement policy update | Enhance affordability programs |

| Logistics | Commercial vehicle fleet expansion | 6-9% | Fleet expansion financing | Expand fleet services |

Emerging Market Opportunities

Volume Growth Sectors:

-

Budget hospitality: Hotel rooms ≤₹7,500 now at 5% GST.

-

Wellness services: Gyms, salons, yoga at 5%.

-

Educational services: Learning tools are now exempt or at 5%.

Export Enhancement:

-

Pharmaceutical exports: Lower input costs boost competitiveness.

-

Textile exports: Fiber cost advantages improve margins.

-

Electronics exports: Component cost reductions support Make in India.

Investment and Expansion Strategies

High-Growth Investment Areas:

-

Agricultural technology: Capitalise on demand for mechanisation

-

Budget vehicle manufacturing: Serve the expanding affordable mobility market

-

Health insurance distribution: Exploit zero GST penetration opportunity

-

Cement and construction materials: Leverage the infrastructure boom

Working Capital Optimisation:

-

Faster refunds through improved GST 2.0 processes.

-

Reduced blocked capital from inverted duty structure corrections.

-

Improved cash flows from simplified compliance.

Regulatory Updates and Expert Resources

Official Notifications and Compliance

Key CBIC Notifications (September 17, 2025):

-

Notification 9/2025: Revised rate schedules.

-

Notification 10/2025: Exemption categories.

-

Notification 15/2025: Service sector changes.

-

Notification 16/2025: Insurance and delivery services.

Conclusion: Seizing the GST 2.0 Advantage

The Next Generation GST reforms represent more than tax simplification—they constitute a strategic reset for Indian businesses. Organisations that act swiftly to reconfigure operations, optimise pricing, and capture new market opportunities will emerge as clear winners in this transformed landscape.

Success will depend on three critical factors:

-

Speed of implementation: First-movers gain competitive advantages

-

Strategic thinking: Beyond compliance to market expansion

-

Stakeholder alignment: Coordinated action across finance, operations, and strategy teams

The ₹48,000 crore annual revenue sacrifice by the government signals a commitment to a consumption-led growth strategy. Forward-thinking leaders must now translate these policy benefits into sustainable competitive advantages, market expansion, and enhanced shareholder value.

The GST 2.0 opportunity window is now open -the question is not whether to act, but how fast you can move.

GST Audit Checklist | GST on Maintenance Charges of Residential Building | Biscuit GST Rate | GST on Dry Fruits | GST on Bakery Items

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified