Strategic GST Compliance Alert: Section 130 vs Section 73/74 – A CFO’s Guide

Key Takeaway for Finance Leaders: Recent Allahabad High Court rulings have clarified critical procedural safeguards for GST authorities when they discover unaccounted inventory during surveys. This could significantly impact your tax exposure and penalty liability.

Why This Matters to Your Finance Function

If your premises undergo a GST survey and officers discover excess or unaccounted stock, the legal procedure they follow will determine whether you face:

-

Minimal penalties (potentially 0-10% of tax)

-

OR confiscation proceedings with penalties up to 100% of tax plus fines

Recent court judgments have established that Section 130 (confiscation provisions) cannot be invoked for routine inventory discrepancies found during surveys of registered taxpayers.

The Legal Framework You Need to Know

Section 35(6): The Foundational Rule

When unaccounted goods are discovered, Section 35(6) mandates that tax authorities must follow the procedure under Section 73 or 74 - not Section 130. This provision treats unaccounted inventory as if it were supplied by your company, but crucially:

-

Provides a structured adjudication process

-

Offers penalty mitigation opportunities

-

Prevents arbitrary confiscation

The Three Pathways: Understanding Your Exposure

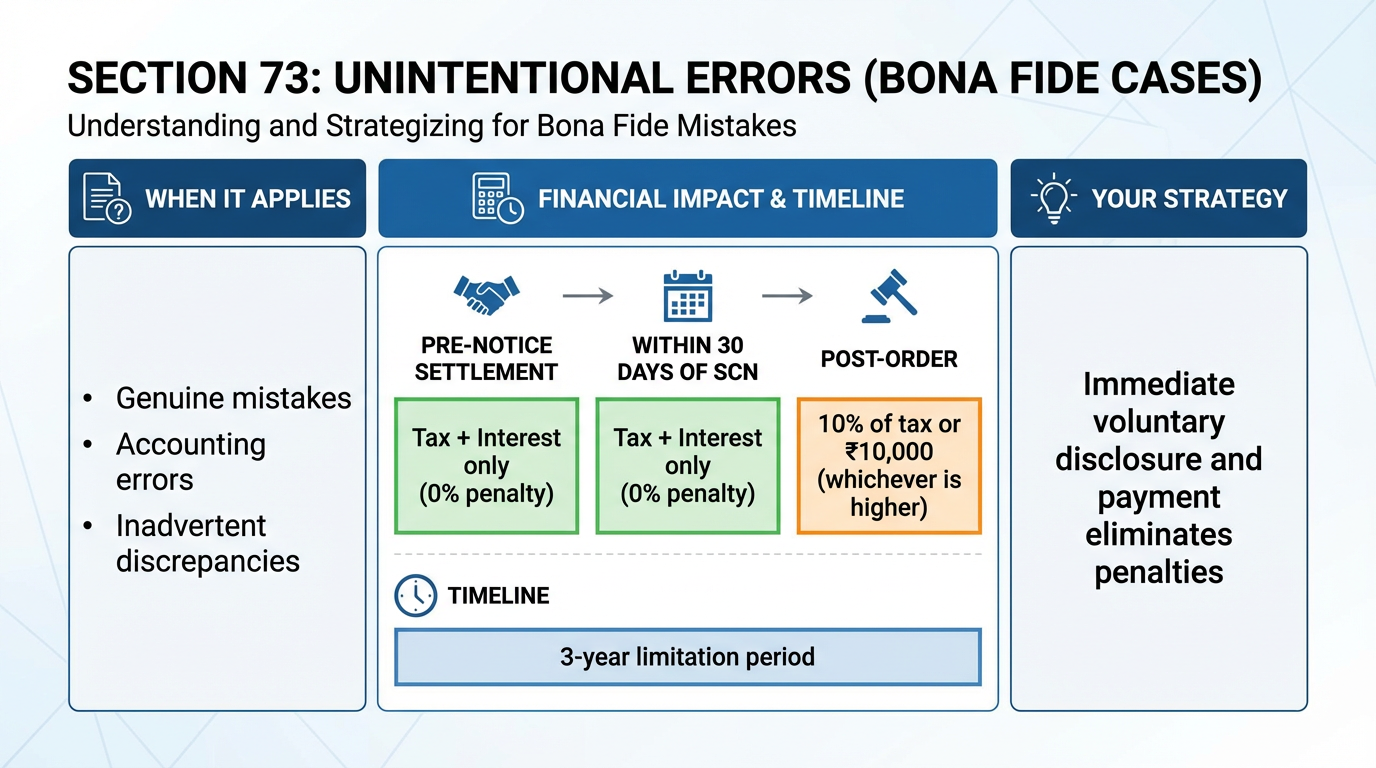

1. Section 73: Unintentional Errors (Bona Fide Cases)

-

When it applies: Genuine mistakes, accounting errors, inadvertent discrepancies

-

Financial impact:

-

Pre-notice settlement: Tax + Interest only (0% penalty)

-

Within 30 days of SCN: Tax + Interest only (0% penalty)

-

Post-order: 10% of tax or ₹10,000 (whichever is higher)

-

-

Timeline: 3-year limitation period

-

Your strategy: Immediate voluntary disclosure and payment eliminates penalties

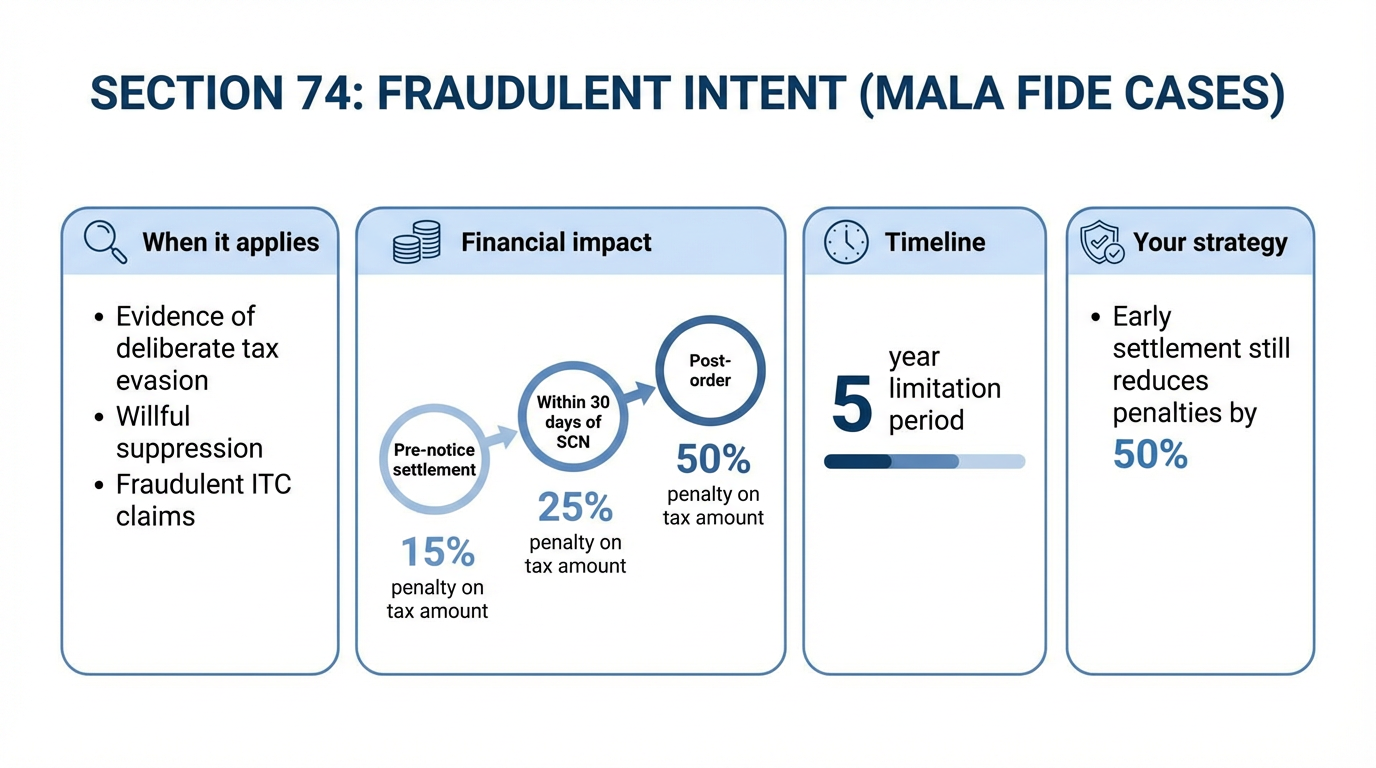

2. Section 74: Fraudulent Intent (Mala Fide Cases)

-

When it applies: Evidence of deliberate tax evasion, willful suppression, fraudulent ITC claims

-

Financial impact:

-

Pre-notice settlement: 15% penalty on tax amount

-

Within 30 days of SCN: 25% penalty on tax amount

-

Post-order: 50% penalty on tax amount

-

-

Timeline: 5-year limitation period

-

Your strategy: Early settlement still reduces penalties by 50%

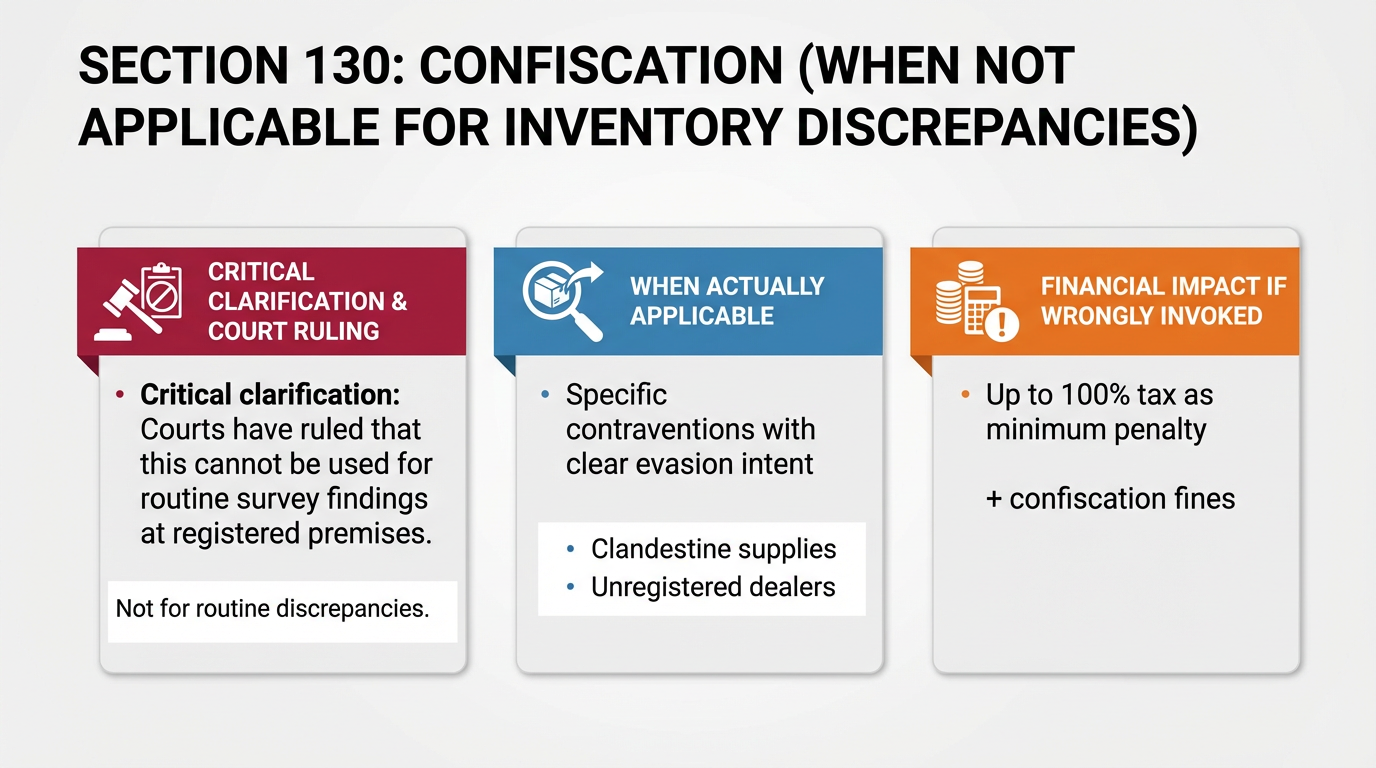

3. Section 130: Confiscation (When NOT Applicable for Inventory Discrepancies)

-

Critical clarification: Courts have ruled that this cannot be used for routine survey findings at registered premises

-

When actually applicable: Specific contraventions with clear evasion intent (clandestine supplies, unregistered dealers)

-

Financial impact if wrongly invoked: Up to 100% tax as minimum penalty + confiscation fines

Practical Implications for Your Finance Team

Immediate Action Items:

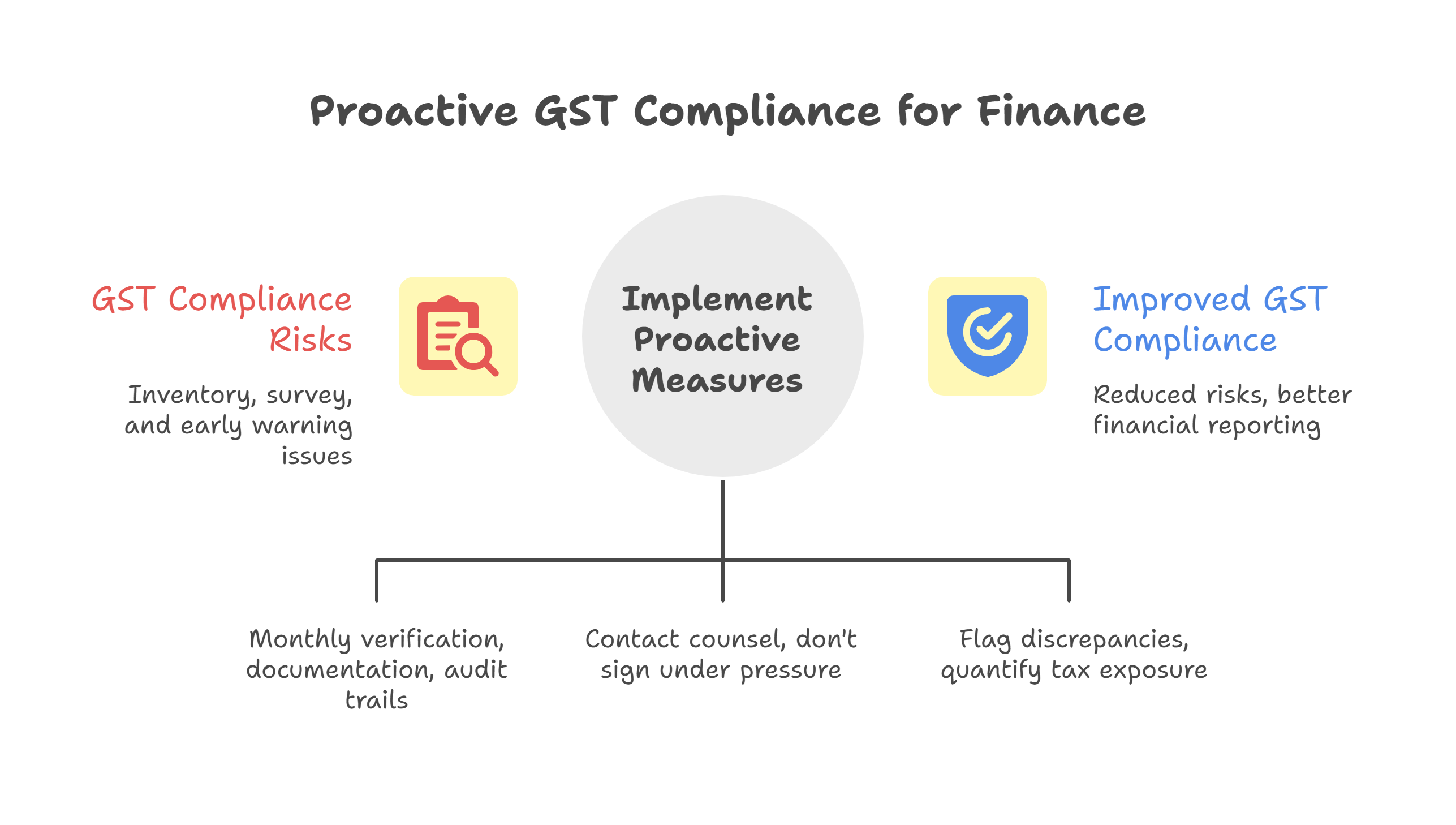

1. Review Current Inventory Reconciliation Processes

-

Implement monthly physical verification vs. book records

-

Document all inventory movements contemporaneously

-

Maintain clear audit trails for all stock receipts and dispatches

2. Train Your Team on Survey Protocols

-

Ensure staff knows to immediately contact legal/tax counsel during surveys

-

Don't sign any panchnama or statement under pressure

-

Verify which statutory provision is being invoked before any admission

3. Develop Early Warning Systems

-

Flag discrepancies immediately for investigation

-

Quantify potential tax exposure on unaccounted items

-

Assess whether the discrepancy appears bona fide or mala fide

4. Create Settlement Decision Matrix

Use this framework when faced with notices:

| Timing | Section 73 Penalty | Section 74 Penalty | Action Priority |

| Before SCN | 0% | 15% | Immediate settlement recommended |

| Within 30 days of SCN | 0% | 25% | High priority settlement |

| Post-order | 10% | 50% | Consider appeal vs. settlement |

Risk Mitigation Strategy

If You Receive a Section 130 Notice for Inventory Discrepancies:

Step 1: Immediately challenge the legal basis

-

Cite Vivek Kumar Gupta v. State of Uttar Pradesh – Allahabad High Court (2025) 180 taxmann.com 489 (All.) and Additional Commissioner Grade-2 vs M/s Vijay Trading Company [(2025) 174 taxmann com 516 (SC) :: TS-523-HC(ALL)-2024-GST]

-

Assert that Section 35(6) mandates Section 73/74 procedure, not Section 130

Step 2: Characterize the discrepancy

-

If genuinely unintentional: Push for Section 73 classification

-

If intentional elements exist: Negotiate Section 74 early settlement (saves 50% of penalty)

Step 3: Calculate financial exposure

-

Section 73 path: Tax + Interest + Max 10% penalty

-

Section 74 path: Tax + Interest + 15-50% penalty (depending on timing)

-

Section 130 wrongly invoked: Challenge jurisdiction entirely

CFO Checklist: Preventive Measures

Monthly:

-

Physical inventory verification vs. books

-

Investigation of variances >2%

-

Documentation of all movements

Quarterly:

-

Review of ITC reconciliation with GSTR-2B

-

Assessment of any potential unaccounted items

-

Training refresher for stores/warehouse team

Annually:

-

Comprehensive inventory audit by internal/external auditors

-

Review of GSTR-9/9C filing accuracy

-

Assessment of compliance risk areas

During Survey:

-

Legal/tax advisor on-site immediately

-

Verify statutory authority and provision being invoked

-

Document all proceedings

-

Do not make admissions without counsel

Bottom Line for Finance Leadership

The Allahabad High Court rulings provide crucial protection against overreach by tax authorities. The key financial insight: For registered taxpayers with normal business operations, inventory discrepancies found during surveys should never trigger Section 130 confiscation proceedings.

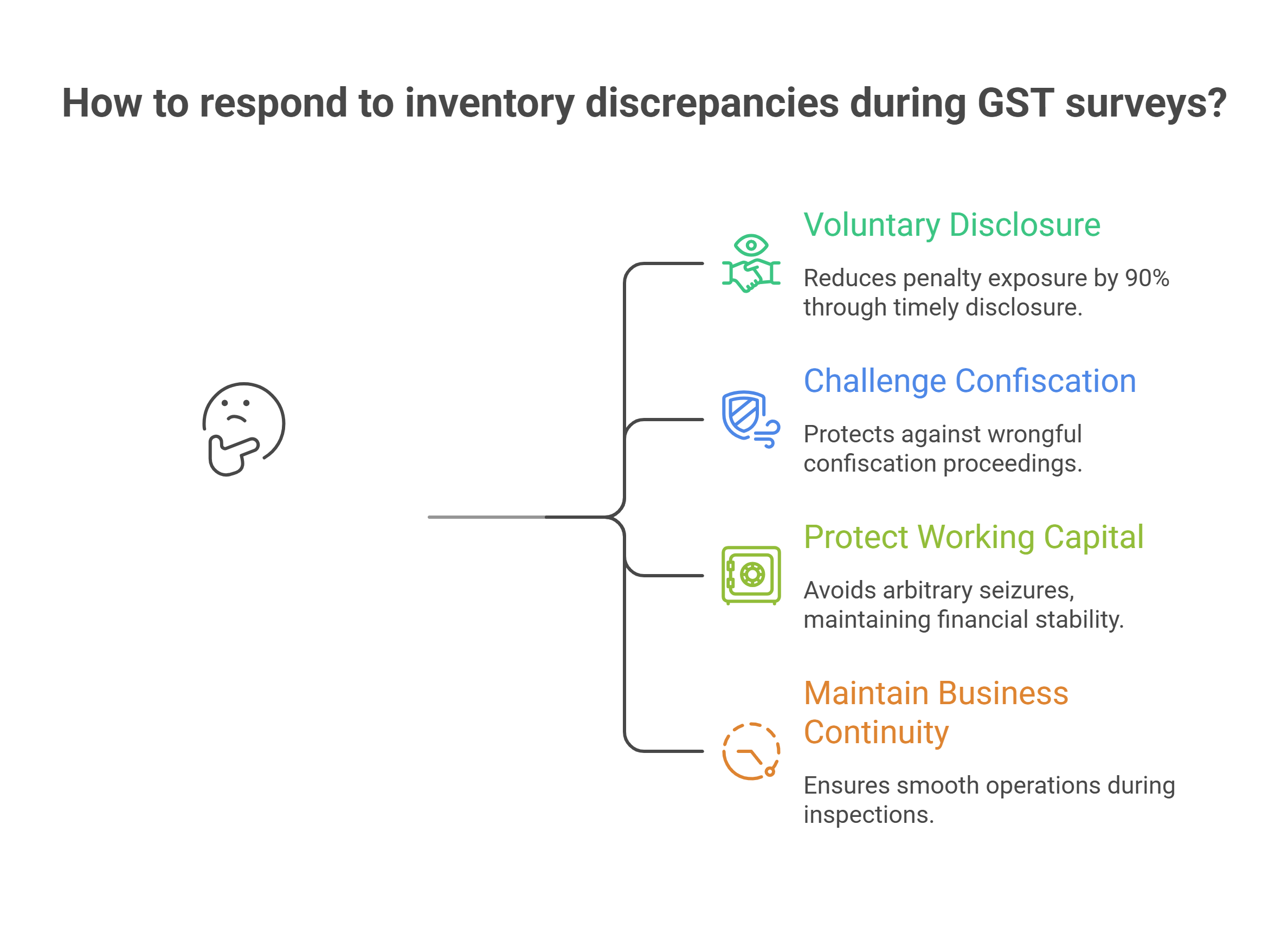

Your financial advantage: By understanding the distinction between Sections 73/74 and 130, you can:

-

Reduce penalty exposure by 90% through timely voluntary disclosure

-

Challenge wrongful confiscation proceedings

-

Protect working capital by avoiding arbitrary seizures

-

Maintain business continuity during inspections

Recommended board-level position: Ensure your tax compliance function has clear escalation protocols and settlement authority limits to capitalise on the favourable penalty structure available under Section 73/74.

Disclaimer: This analysis is based on recent judicial precedents and current GST provisions. Given the evolving nature of GST jurisprudence, consult with your tax advisors before taking specific actions on notices received.

Powers of GST Officers | GSTR 3B table 5 | Penalty for non GST registration | Supreme court itc to be given to the purchaser even if tax is not deposited by seller | Penalty for non GST registration

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified