Beyond the Penalty: Why Your GST Filing Speed is the Ultimate Test of Future-Proofing

1. The Strategic Architecture of Timely Compliance

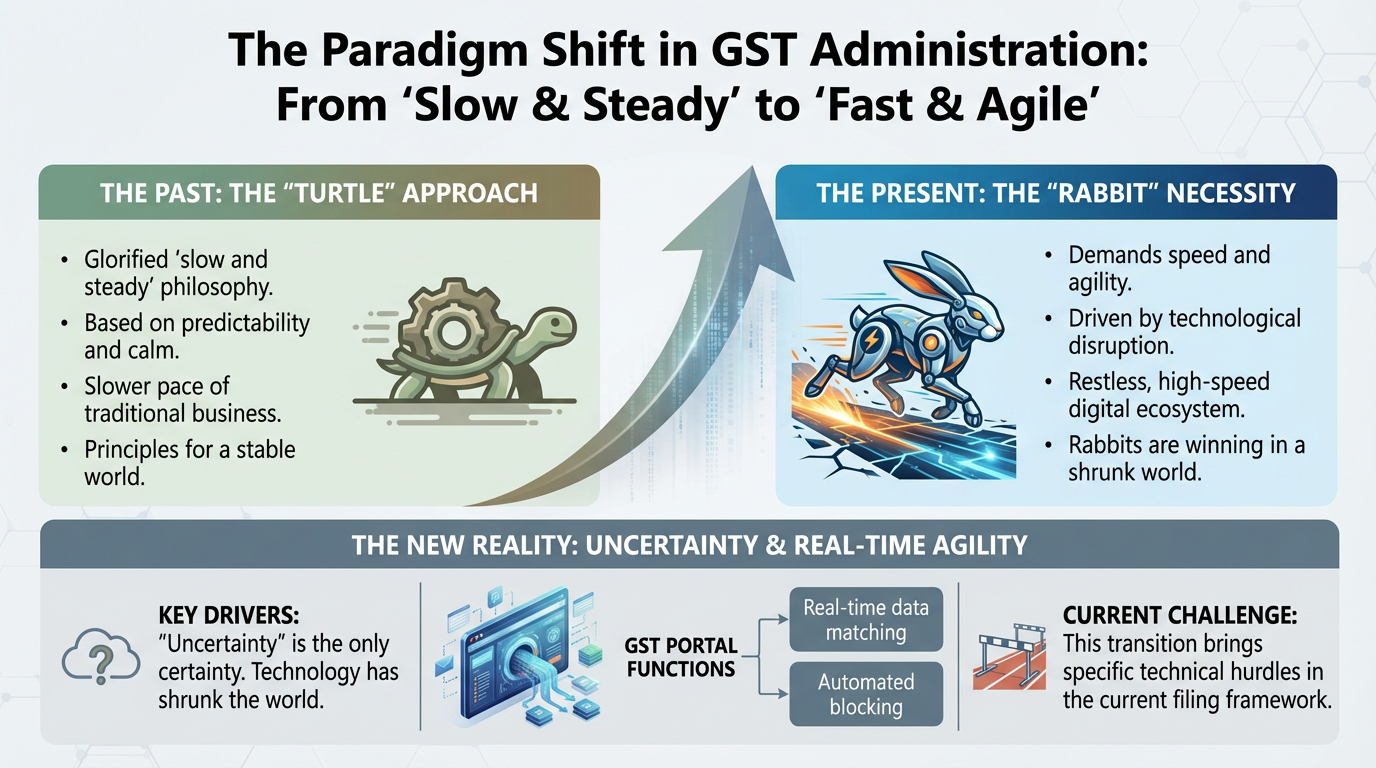

In the contemporary landscape of Indian indirect taxation, compliance is no longer a back-office administrative chore; it is a primary indicator of an organisation's operational health and its "future-readiness." As a jurisconsult, I often observe that statutory late fees are rarely just a financial leak. Instead, they are a loud signal that an entity is trapped in a "firefighting" mode, reacting to crises rather than anticipating them. In a world where the pace of change is rapid, many businesses risk obsolescence by waiting for the "bus of change" to arrive before adapting. It has been said that, “if the rate of change on the outside exceeds the rate of change on the inside, the end is near.”

The fundamental shift in the Goods and Services Tax (GST) administration mirrors the broader evolution from the "slow and steady" turtle approach to the "fast rabbit" necessity. While our upbringing glorified the turtle, modern business principles for a predictable world have fallen apart. Today, the rabbits are winning because technological disruption has shrunk the world, and "uncertainty" has become the only certainty. The GST portal, with its real-time data matching and automated blocking, functions at a pace that demands agility. This transition from a calm, slow-moving world to a restless, high-speed digital ecosystem brings us to the specific technical hurdles of the current filing framework.

2. The Sequential Lock: Navigating GSTR-1 and GSTR-3B Filing Provisions

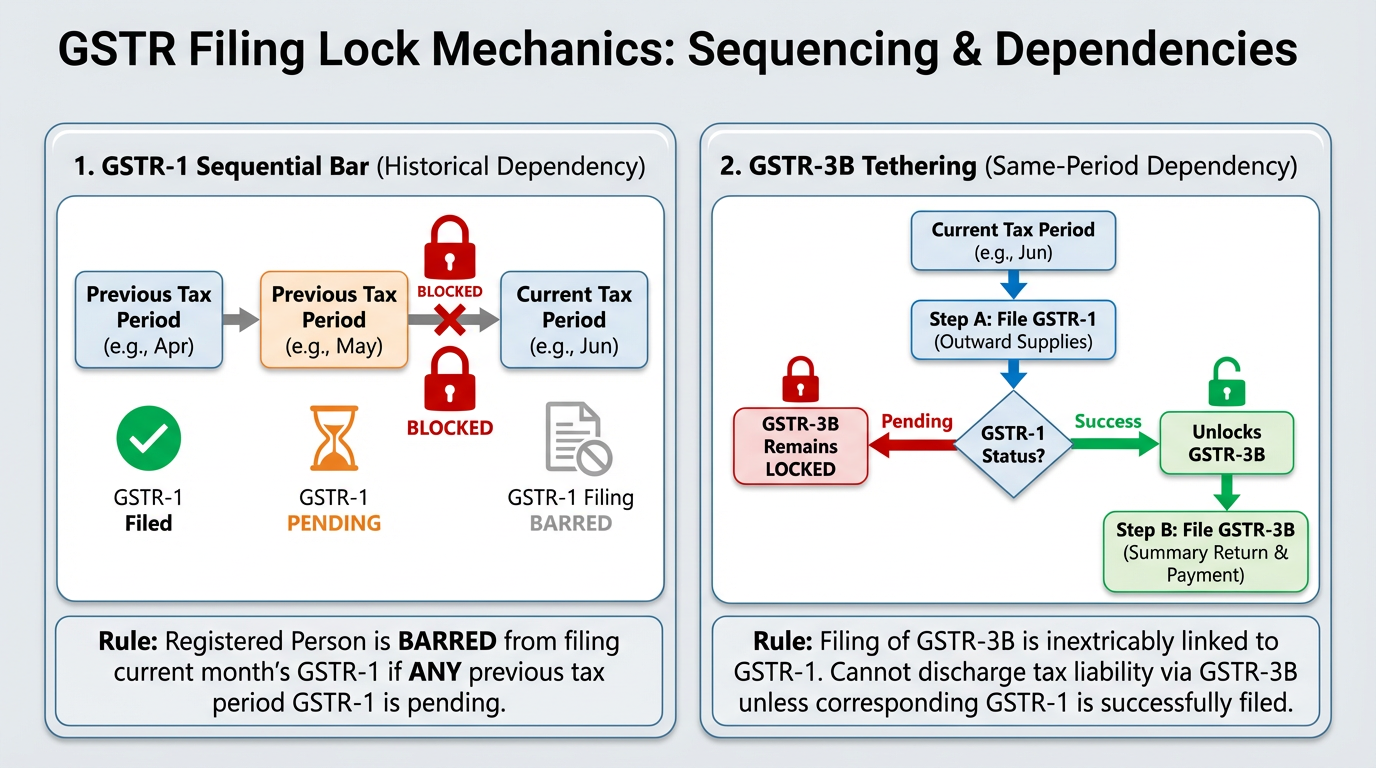

The architecture of the GST ecosystem is now defined by a rigorous filing sequence that mandates the "discipli of Now." Introduced under Sections 37(4) and 39(10) of the Central Goods and Services Tax (CGST) Act, these sequential locks ensure that tax data flows in an irreversible order, preventing taxpayers from cherry-picking their compliance dates.

The mechanics of these filing locks are structured as follows:

-

GSTR-3B Tethering: The filing of GSTR-3B (the summary return and tax payment) is inextricably linked to GSTR-1. A taxpayer cannot discharge their monthly tax liability through GSTR-3B unless the corresponding GSTR-1 for that period has been successfully filed.

This procedural lockdown creates a significant "So What?" layer for leadership. When an organisation faces constant procedural hurdles, it leads to "decision fatigue." Much like a person who spends more time deciding whether to mark an email as "cc" or "bcc" than writing the content, a business that struggles with routine filing exhausts its mental and operational energy on clerical survival rather than high-value tax positions. Furthermore, these locks create a liquidity vacuum. While the forward-charge Input Tax Credit (ITC) is essentially a ledger entry, late fees and Reverse Charge Mechanism (RCM) liabilities require immediate cash outflows, thereby draining operational capital required for growth.

3. The Domino Effect: Late Fees, ITC Denials, and Vendor Default

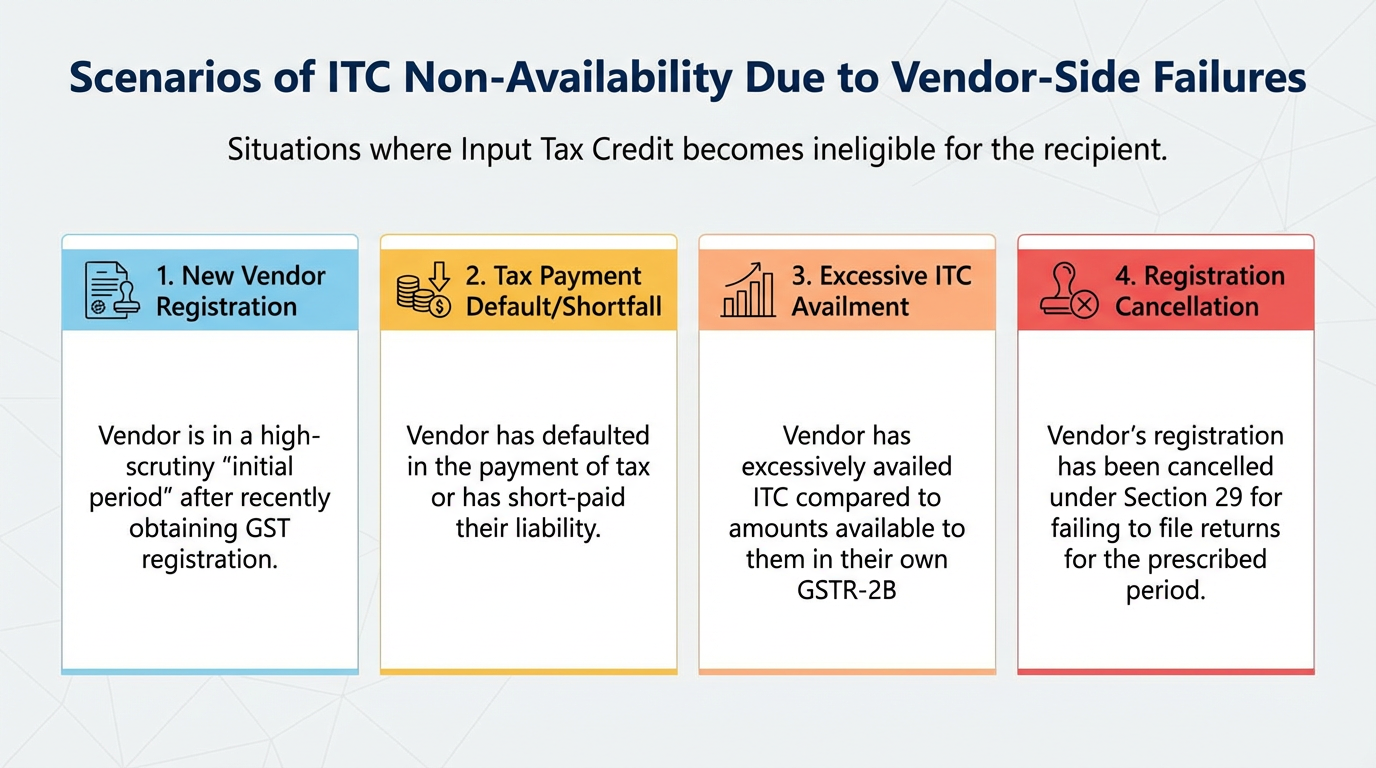

The GST ecosystem is deeply interconnected, meaning the inertia of one entity becomes the financial burden of another. This interdependency is most visible in the ITC framework, where a recipient’s credit is tied to the vendor’s discipline. According to the Budget 2022 amendments, ITC is available only if it is not "restricted" in the GSTR-2B of the taxpayer.

The "Budget 2022" provisions identify several scenarios where ITC becomes "not available" due to vendor-side failures:

-

The vendor has recently obtained GST registration and is in a high-scrutiny "initial period."

-

The vendor has defaulted in the payment of tax or has short-paid their liability.

-

The vendor has excessively availed ITC compared to the amounts available to them in their own GSTR-2B.

-

The vendor’s registration has been cancelled under Section 29 for failing to fie returns for the prescribed period.

Crucially, the law now imposes a hard deadline for the rectification of errors or the availment of missed credit from the previous financial year: the 30th of November. This "discipline of Now" means that if a vendor’s default is not resolved by this date, the credit is lost forever. This creates a sharp distinction between a "secure" ITC claim and one "denied due to vendor." If a vendor fails to remit the tax it collected, the recipient must reverse the credit, including interest, demonstrating that a business cannot be future-proof in isolation. This complexity is further heightened when we examine the liability shift under the Reverse Charge Mechanism.

4. RCM and the Liability Shift: Timing as a Compliance Catalyst

The Reverse Charge Mechanism (RCM) must be viewed as an "Executive Framework for Accurate GST Diagnosis" rather than a mere list of entries. It is a complete statutory system where the recipient must self-assess and pay tax in cash. A fragmented, mechanical understanding of RCM often leads to retrospective liabilities and cash-outflow penalties.

RCM triggers are specifically defined under Section 9(3) and Section 9(4) of the CGST Act, governed by key notifications:

-

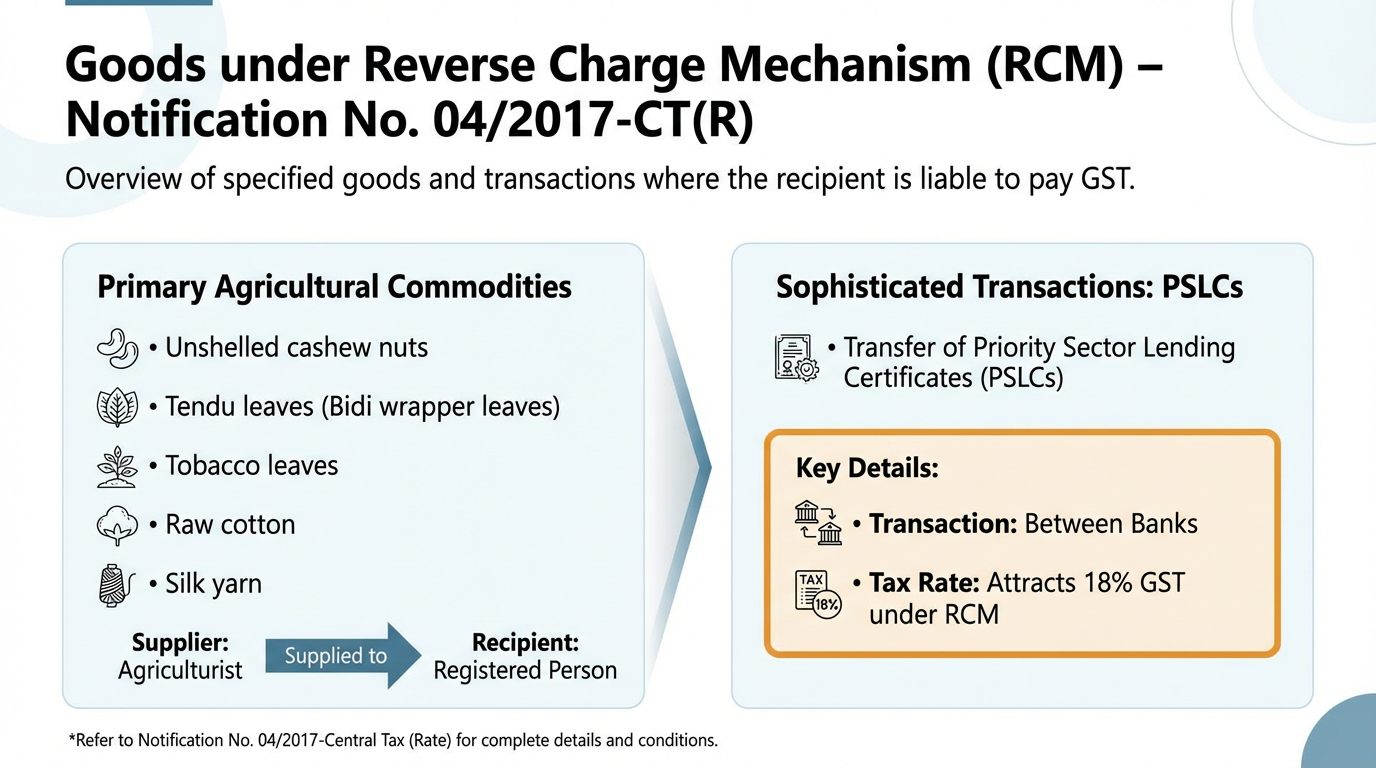

Goods (Notification No. 04/2017-CT(R)): This includes primary agricultural commodities like unshelled cashew nuts, Tendu leaves (Bidi wrapper leaves), tobacco leaves, raw cotton, and silk yarn when supplied by an agriculturist to a Registered Person. Notably, it also covers sophisticated transactions like the transfer of Priority Sector Lending Certificates (PSLCs) between banks, which attracts 18% GST under RCM.

-

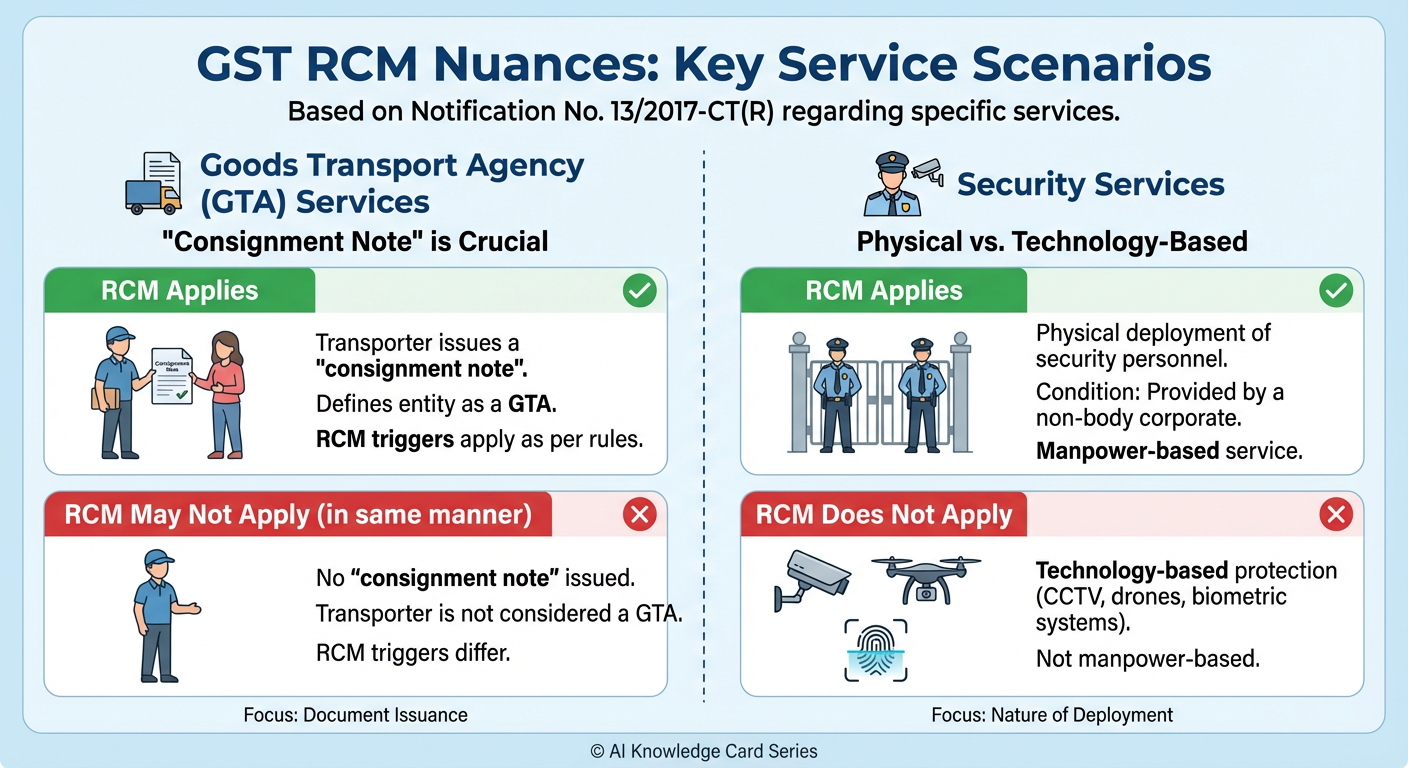

Services (Notification No. 13/2017-CT(R)): Key categories include legal services by advocates and sponsorship services. However, the "jurisconsult" nuance lies in the details:

-

GTA Services: A transporter is only a Goods Transport Agency (GTA) if they issue a "consignment note." Without this note, the RCM triggers may not apply in the same manner.

-

Security Services: RCM applies to the physical deployment of security personnel by a non-body corporate. However, technology-based protection (such as CCTV monitoring, drone-based surveillance, or biometric access systems) does not attract RCM as it is not manpower-based.

-

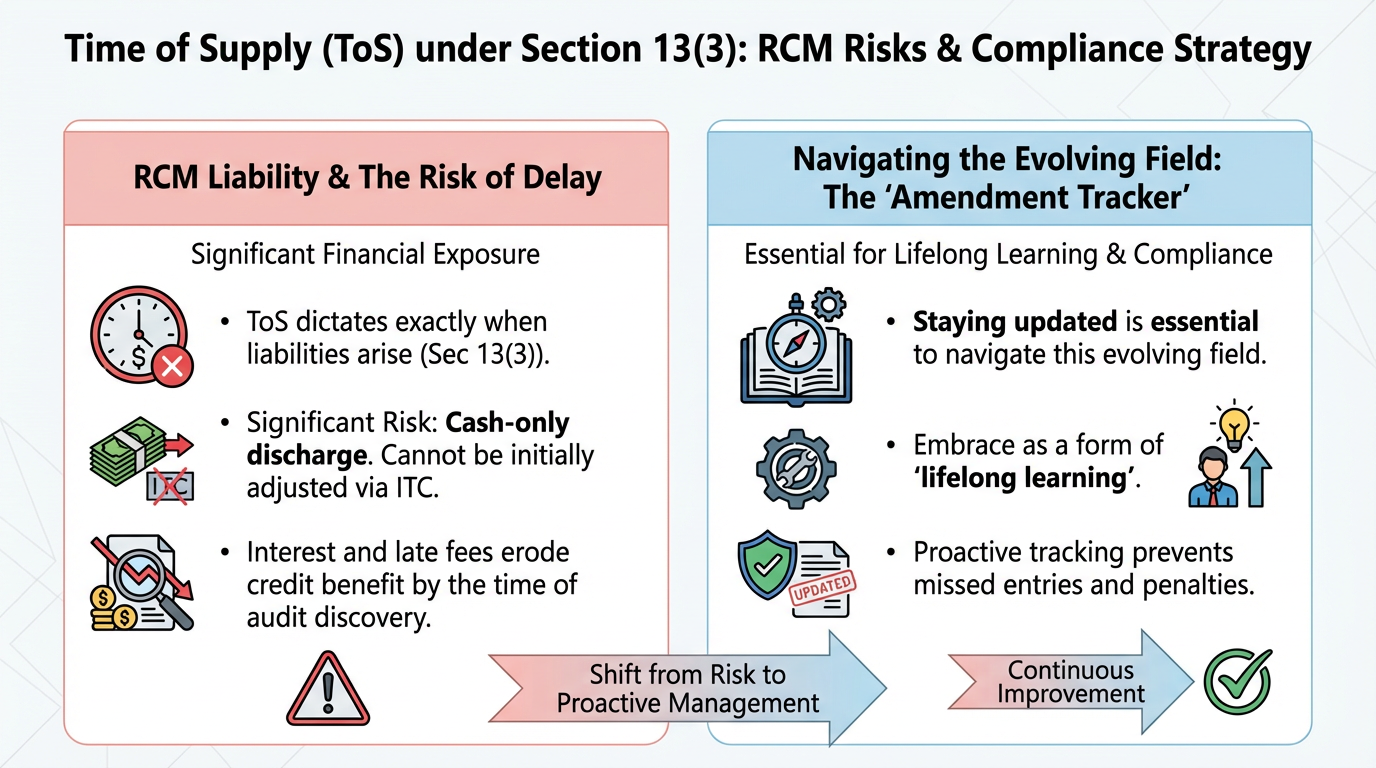

Under Section 13(3), the Time of Supply (ToS) dictates exactly when these liabilities arise. Delaying RCM payment is a significant risk because it is a cash-only discharge that cannot be initially adjusted via ITC. By the time an auditor discovers a missed RCM entry, the interest and late fees have already eroded the benefit of the credit. Staying updated with the "Amendment Tracker" is a form of lifelong learning essential to navigating this evolving field.

5. Proactive Mitigation: Strategies to be "Future Ready" against Penalties

To avoid the hidden price of time, an organisation must transition from "firefighting" to "anticipating" challenges. As the principles of future-proofing suggest, we must not be kind when probing our own internal systems.

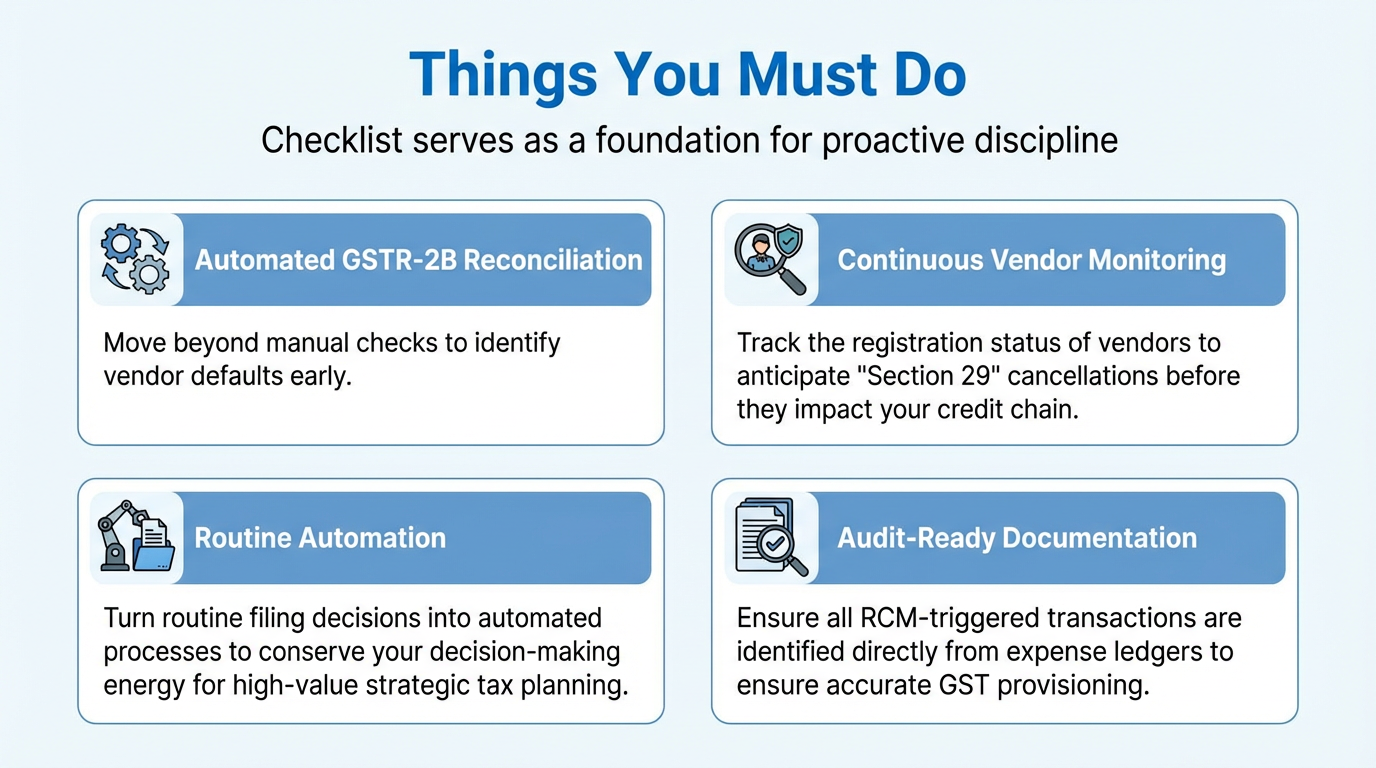

The following "Things You Must Do" checklist serves as a foundation for proactive discipline:

-

Automated GSTR-2B Reconciliation: Move beyond manual checks to identify vendor defaults early.

-

Continuous Vendor Monitoring: Track the registration status of vendors to anticipate "Section 29" cancellations before they impact your credit chain.

-

Routine Automation: Turn routine filing decisions into automated processes to conserve your decision-making energy for high-value strategic tax planning.

-

Audit-Ready Documentation: Ensure all RCM-triggered transactions are identified directly from expense ledgers to ensure accurate GST provisioning.

Technology, specifically AI and ML, will increasingly handle the analytical work of identifying RCM liabilities and mapping them to financial reports. By adopting an "agile" mindset, businesses can ensure that their internal rate of change aligns with the external pace of the GST portal. Compliance discipline is the seed planted today for the harvest of a hassle-free future.

6. Words of Wisdom: A Concluding Reflection on Discipline

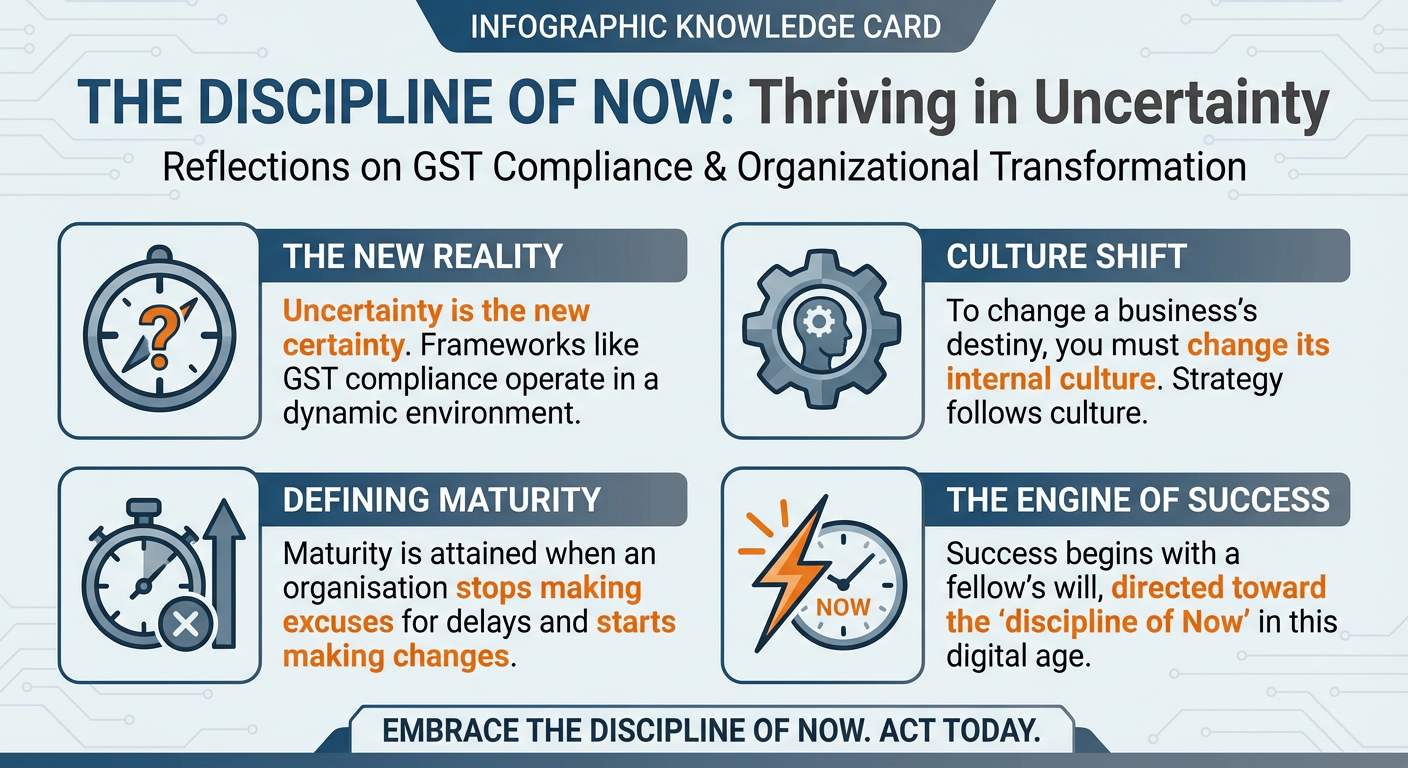

As we reflect on the frameworks of GST compliance, we must recognise that uncertainty is the new certainty. The only way to change a business's destiny is to change its internal culture. Maturity is attained when an organisation stops making excuses for delays and starts making changes. Success begins with a fellow's will, and in this digital age, that will must be directed toward the "discipline of Now."

True professional growth comes from the realisation that we are not indispensable unless we continue to reinvent ourselves. Those who miss the bus of anticipation will find that the future is not kind. There is a profound "Joy of Missing Out" (JOMO) to be found: not in missing social media news, but in avoiding penalties and litigation through the simple, unwavering discipline of timely compliance.

In a world of rapid movement, the greatest success is the peace of mind that comes from being truly future-proof.

GST Late Fees | GSTR 3B Late Fee | GSTR 1 Late Fees | GST Annual Return Late Fee | Interest on GST Late Payment | Section 13 of CGST Act

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified