GST Tax Fraud Penalties: Section 74 Payment Stages Explained (2025 Guide)

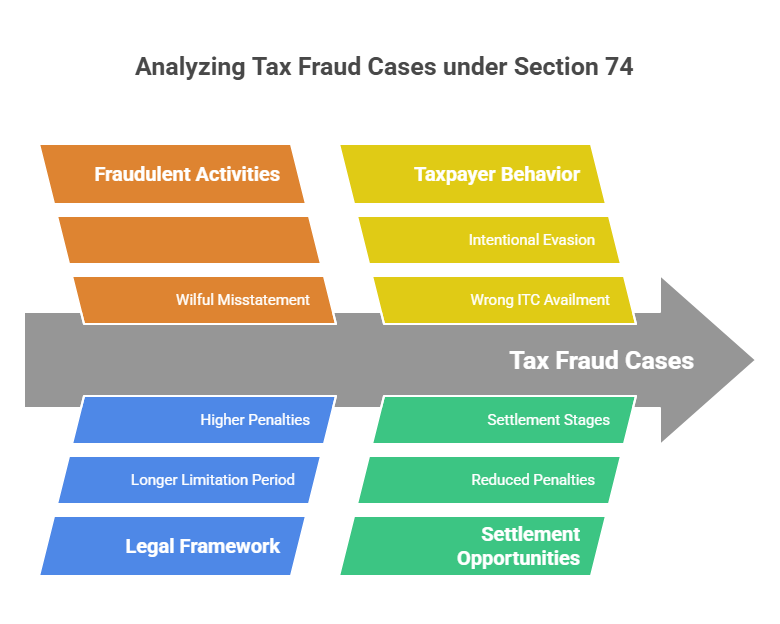

Section 74 of the Central Goods and Services Tax Act, 2017 ("the CGST Act") addresses the determination and recovery of tax that has been short paid, not paid, or where an erroneous refund or incorrect Input Tax Credit (ITC) utilisation/availment has occurred by reason of fraud, wilful-misstatement, or suppression of facts to evade tax. These elements constitute 'evasion of tax' and must be deliberate, resulting in a financial gain to the taxpayer.

The penalty provisions under Section 74 and the corresponding State/Union Territory Acts specifically deal with demands raised due to tax evasion involving intentional wrongdoing.

The penalty structure under Section 74 is directly linked to the taxpayer's cooperation and timing of payment, offering multiple opportunities for concession below the maximum 100% penalty.

Evidentiary Burden for Special Circumstances:

1. Requirement of Intent and Gain: It is essential that this active ingredient (fraud, wilful-misstatement, or suppression) must be deliberate and must result in a gain to the taxpayer.

2. Evasion of Tax: Indulging in misadventure without resultant gain merely amounts to misunderstanding of law or mistaken self-assessment, and does not constitute evasion of tax. Every non-payment of tax does not, ipsi dixit, become evasion.

3. Proof Obligation: Determination of these special circumstances involves an added responsibility on the Proper Officer to (i) make allegations, (ii) adduce evidence, and (iii) prove objectively.

4. Definition of Suppression: The term "suppression" is statutorily defined to mean:

◦ Non-declaration of facts or information which a taxable person is required to declare in a return, statement, report, or any other document furnished under the Act or rules; or

◦ Failure to furnish any information on being asked for, in writing, by the Proper Officer.

◦ Note: Care must be taken as unintentional failure to disclose information required by the rules or requested in writing will also amount to ‘suppression’.

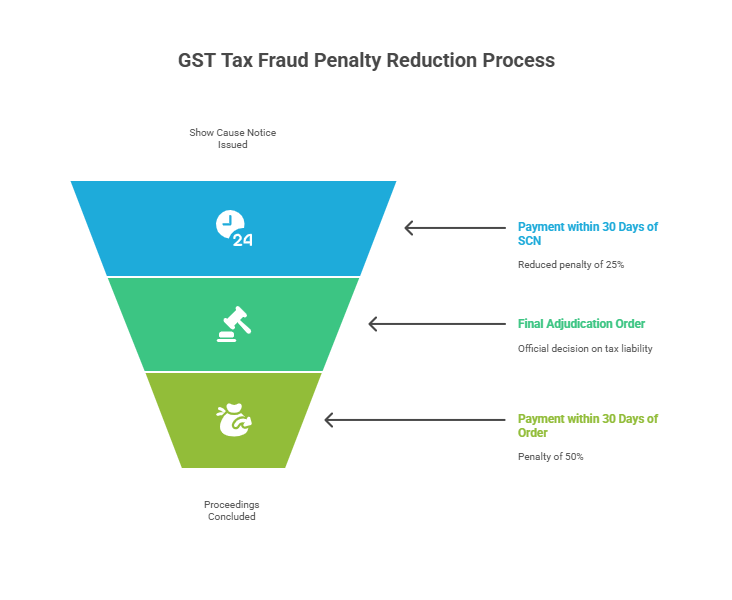

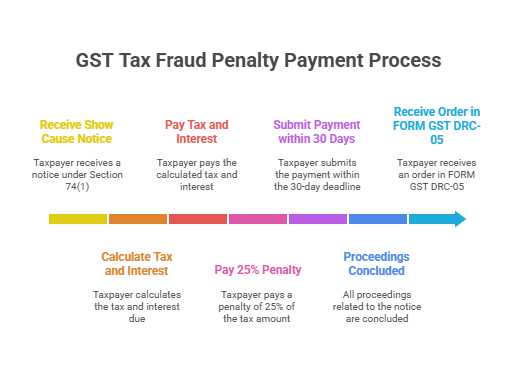

When dealing with the Determination of Tax Not Paid/Short Paid due to Fraud (Section 74), if a person makes the required payment within 30 days of the issue of the Show Cause Notice (SCN), the proceedings are deemed to be concluded with a reduced penalty of 25% of the tax.

The 50% penalty provision under Section 74 applies at a later stage: if the person pays the tax, interest, and the 50% penalty within 30 days of the communication of the final adjudication order.

Penalty Structure and Opportunities for Concession

Where a demand under Section 74 is proposed, the taxpayer is given several opportunities to conclude the proceedings by paying the tax, interest, and a concessional penalty.

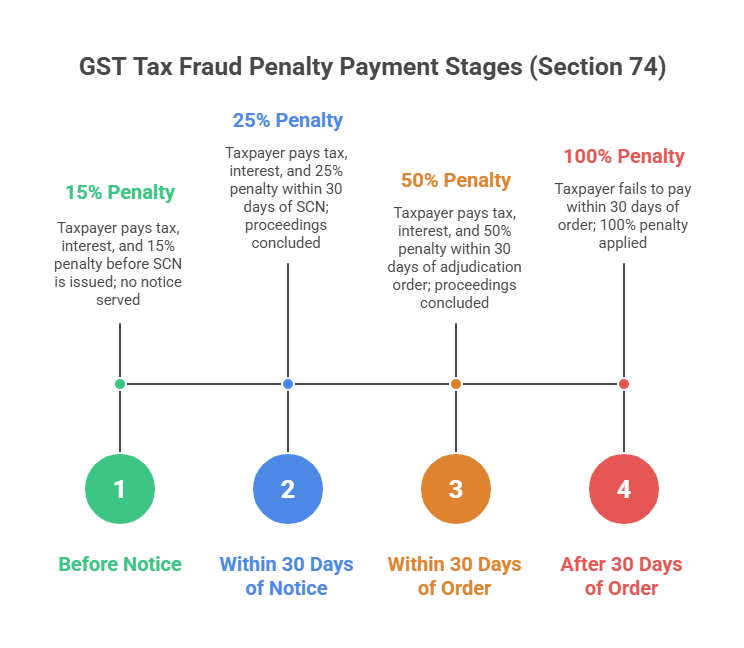

| Opportunity | Timing of Payment | Tax & Interest | Penalty Rate | Outcome | Supporting Form/Rule |

| First Opportunity | Before the service of the Show Cause Notice (SCN) | Must be paid in full | 15% of the tax liability | No SCN or statement will be served for the tax so paid, and proceedings are concluded. | Part A of Form GST DRC–01A (Intimation) and Form GST DRC-03 (Payment). |

| Second Opportunity | Within 30 days of the issuance of the SCN | Must be paid in full | 25% of the tax liability | All proceedings relating to the notice (except proceedings under Section 132) are deemed concluded. | Form GST DRC-03 (Payment) and Form GST DRC-05 (Intimation of conclusion). |

| Third Opportunity | Within 30 days of the communication of the adjudication order | Must be paid in full | 50% of the tax liability | Proceedings relating to the notice (except proceedings under Section 132) are deemed concluded. | Form GST DRC-03 (Payment). |

| Standard Penalty | After 30 days of the adjudication order, or if none of the above are availed | N/A | 100% of the tax liability | This maximum penalty is levied if the Proper Officer determines the tax and penalty during the adjudication process. | Adjudication Order / Form GST DRC-07. |

Here is a detailed discussion based on the sources regarding the penalty structure within the larger context of Section 74:

Determination of Tax under Section 74 (Fraud Cases)

Section 74 is invoked for serious cases where tax has not been paid, short-paid, or ITC wrongly availed due to fraud, wilful misstatement, or suppression of facts to evade tax. This section is characterised by a longer limitation period of five years for issuing an order and significantly higher penalties compared to non-fraud cases under Section 73. The law, however, provides opportunities for taxpayers to settle the matter by paying reduced penalties at various stages.

Payment within 30 Days of Notice and the 25% Penalty

Section 74(8) explicitly outlines the benefit of early payment after a notice has been served.

• Provision: Where a person chargeable with tax receives a Show Cause Notice under Section 74(1), they have the option to pay the demanded tax, the applicable interest under Section 50, and a reduced penalty equivalent to 25% of the tax amount.

• Time Limit: This payment must be made within 30 days of the issue of the notice.

• Conclusion of Proceedings: If the person makes this payment in full within the stipulated 30-day period, all proceedings in respect of the said notice are deemed to be concluded. The proper officer is then required to issue an order in FORM GST DRC-05 concluding the proceedings.

This provision acts as an incentive for taxpayers to settle disputes promptly, even after formal proceedings have been initiated, thereby avoiding prolonged litigation and the imposition of a much higher penalty.

Context within the Demands and Recovery Framework (Sections 73-84)

The penalty structure under Section 74 is a tiered system designed to encourage compliance at the earliest possible stage:

1. Before Notice (15% Penalty): If the person pays the tax, interest, and a 15% penalty before the SCN is even issued, the proper officer will not serve the notice, and the matter is concluded.

2. Within 30 Days of Notice (25% Penalty): This is the stage your query addresses (mistakenly as 50%). Payment of tax, interest, and a 25% penalty within 30 days of the SCN concludes the proceedings.

3. Within 30 Days of Order (50% Penalty): If the matter proceeds to adjudication and an order is passed, the person still has an opportunity to pay the tax, interest, and a 50% penalty within 30 days of the communication of that order to conclude all proceedings.

4. After 30 Days of Order (100% Penalty): If none of the above options are exercised, the penalty becomes 100% of the tax due as confirmed in the adjudication order.

In conclusion, the sources clearly state that payment made within 30 days of a notice under Section 74 leads to the conclusion of proceedings with a 25% penalty. The 50% penalty is applicable only after an adjudication order has been passed.

Other Relevant Penalty Provisions

The GST Act provides for the penalty on other persons involved in abetting evasion:

1. Penalty on Other Persons: Where the proceedings against the main person liable to pay tax under Section 74 are concluded (including through the concession schemes), proceedings against all other persons liable to pay penalty under Sections 122 (penalty for certain offences), 125 (general penalty), 129 (detention/seizure), and 130 (confiscation) are also deemed to be concluded.

2. Abetment: Section 122(3)(a) provides for the levy of penalty on any person who abets/aids any offence under Section 122(1). This liability, if fastened, is limited to ₹25,000 each under the CGST and SGST/UTGST Act.

Intimation of issue of notice under section 65(3) (gst adt-01) | GST Audit Procedure | Penalty for not registering additional place of business under GST | How to check din number in GST portal | Powers of GST officers

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified