Introduction

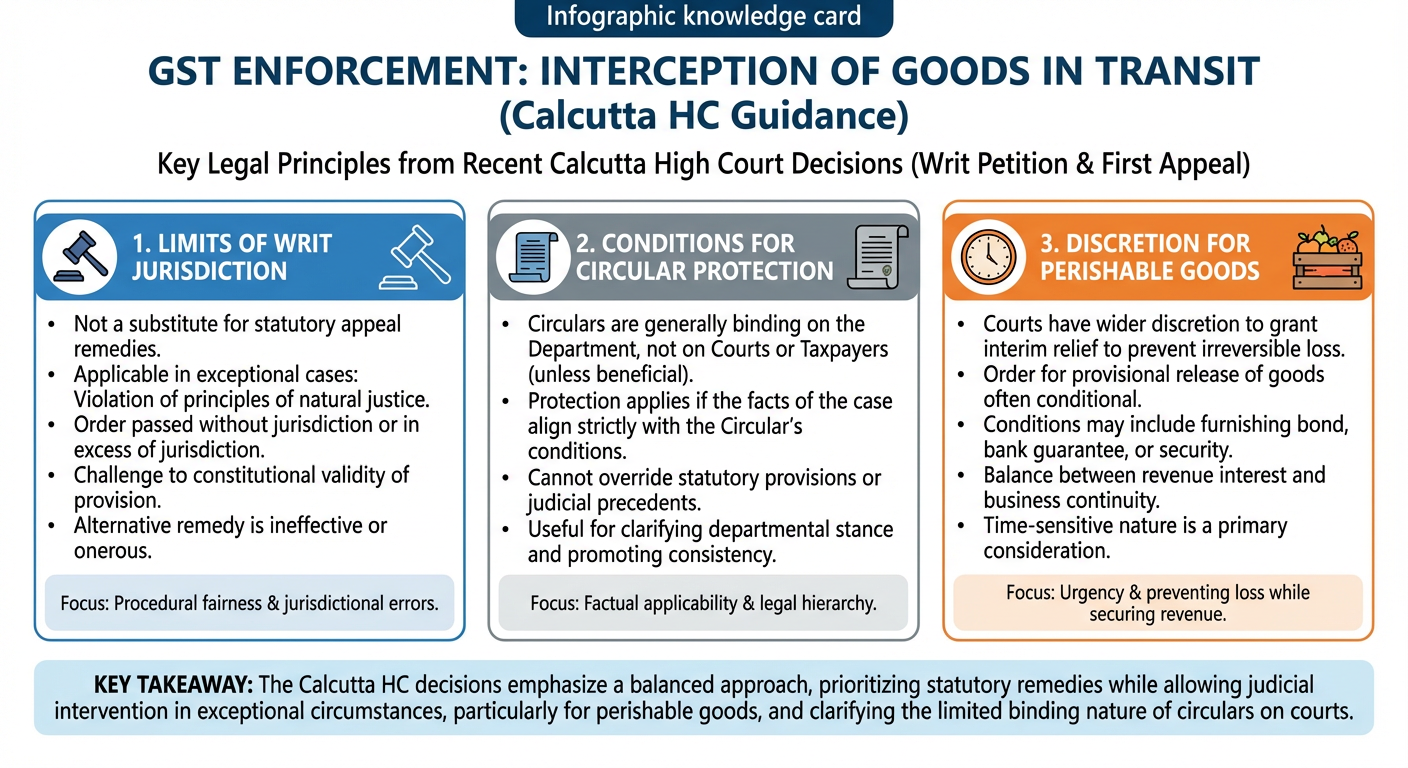

The interception of goods in transit remains one of the most contested flashpoints in GST enforcement. Two recent decisions of the Calcutta High Court, one arising from a writ petition and the other from a first appeal, offer instructive guidance on the limits of writ jurisdiction, the conditions under which Circular protection applies, and the scope of discretion available to courts when perishable goods hang in the balance.

The cases Damroo Enterprise vs State of West Bengal and Ashish Kumar Sharma vs Deputy Commissioner, State Tax, together address three recurring questions that practitioners encounter on a near-daily basis:

Three Core Questions Addressed

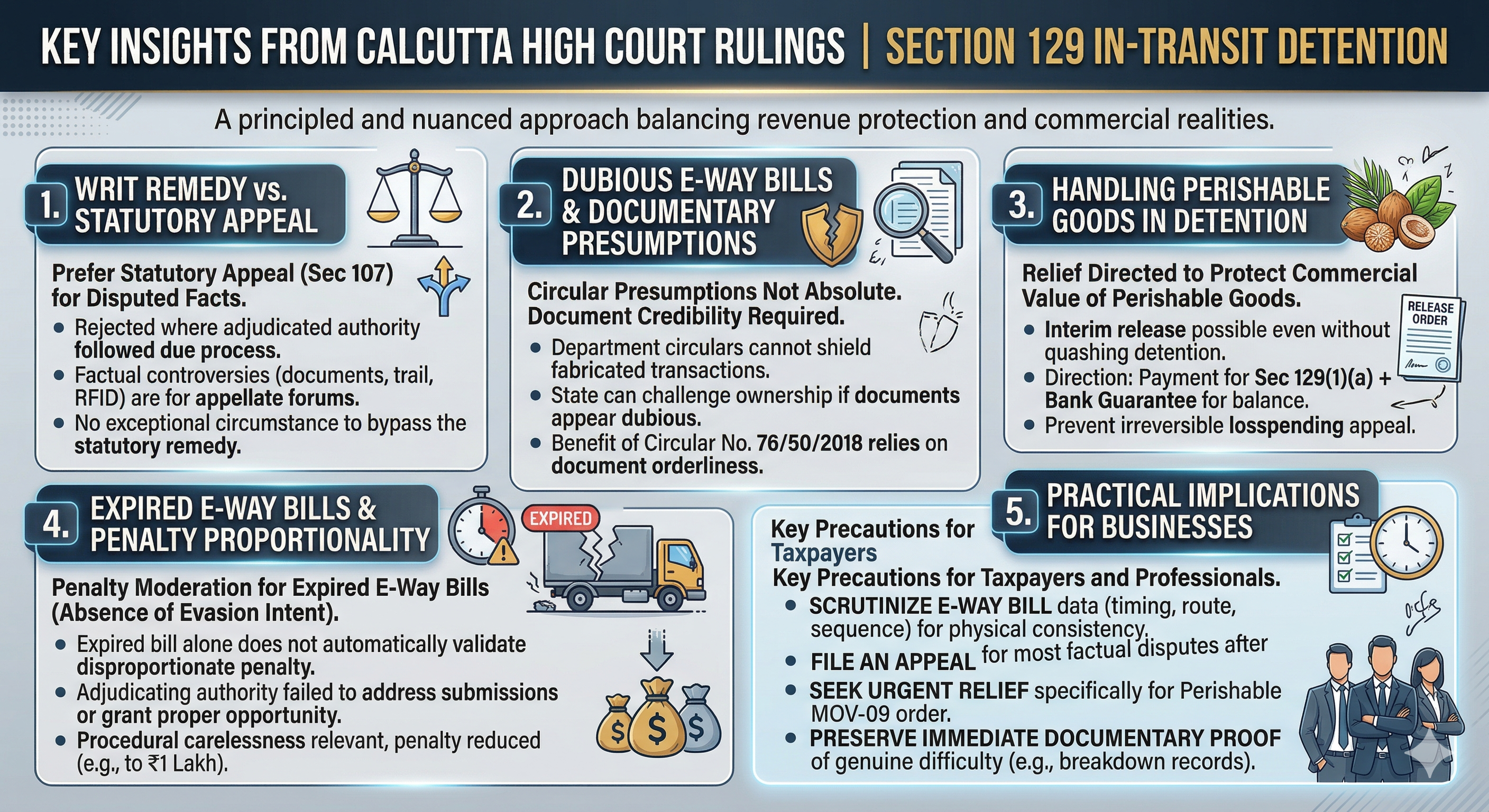

Question 1: Can a taxpayer bypass the statutory appellate remedy under Section 107 by invoking Article 226 of the Constitution of India?

Question 2: Does the CBIC Circular No. 76/50/2018-GST dated 31 December 2018 operate as a blanket protection for any person carrying goods under an e-way bill?

Question 3: What is the appropriate penalty when an e-way bill has expired due to a vehicle breakdown, and the adjudicating authority has failed to engage with the assessee's defence?

Case I: Damroo Enterprise vs State of West Bengal

Case No.: WPA No. 2422 of 2025

Court: Calcutta High Court

Background Facts

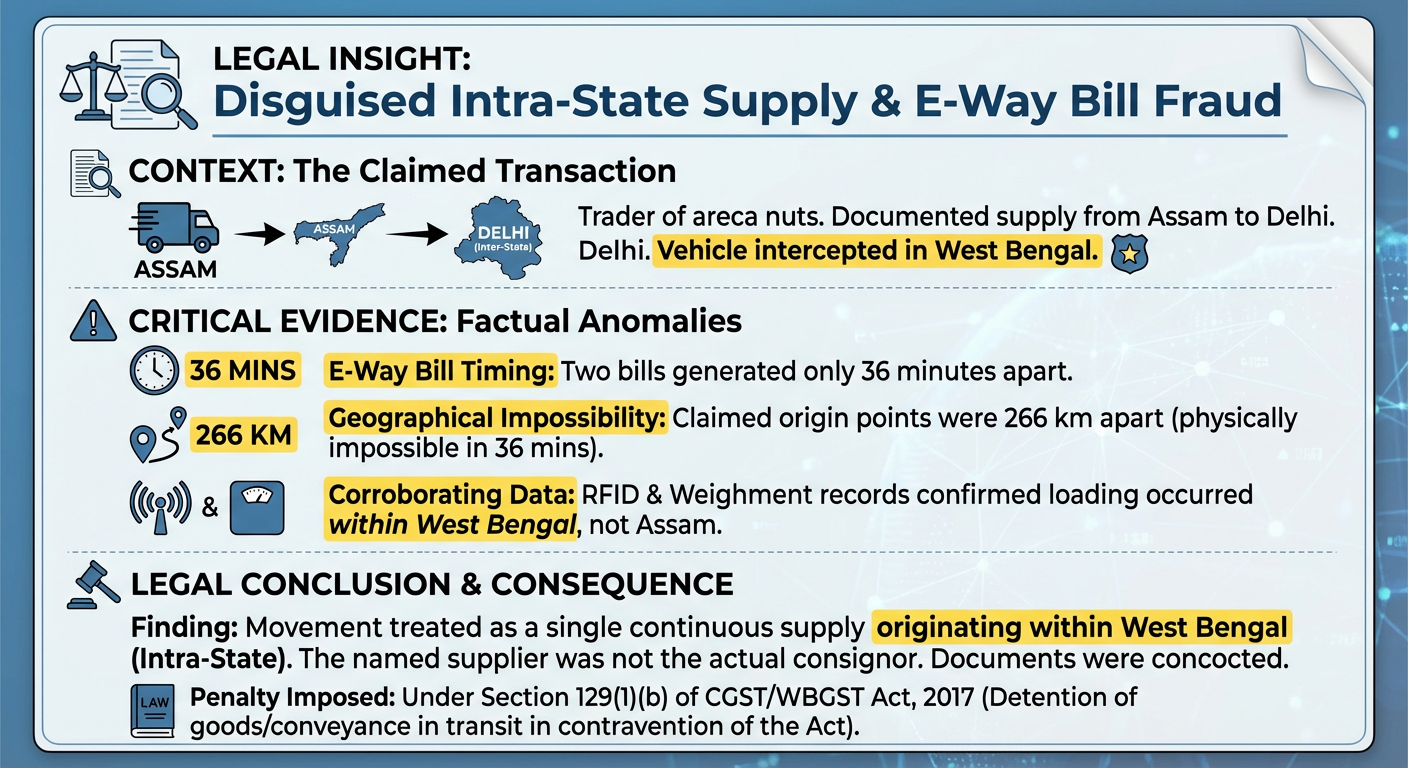

The petitioner, a trader dealing in areca nuts, sold a consignment to a purchaser in Delhi. The goods were loaded and dispatched from Assam. In the course of transit, the vehicle was intercepted by authorities in West Bengal. The adjudicating authority issued a detention order in Form GST MOV-07, served a show cause notice, and after receiving the petitioner's reply, imposed a penalty in Form GST MOV-09 under Section 129(1)(b) of the Central Goods and Services Tax Act, 2017 read with the West Bengal Goods and Services Tax Act, 2017.

The case turned on a critical factual peculiarity: two e-way bills had been generated just 36 minutes apart, covering origins that were 266 kilometres apart. The adjudicating authority treated the movement as a single continuous supply originating within West Bengal. This conclusion was corroborated by RFID data and weighment records, both of which indicated that the goods had been loaded within West Bengal — not in Assam as the accompanying documents purported to show. On this basis, the authority concluded that the named supplier was not the actual consignor, and that the e-way bills had been concocted to project an inter-State origin.

Three Issues Presented Before the Court

Issue 1: Maintainability of the Writ — Article 226 vs Section 107

Facts

The petitioner filed a writ petition under Article 226 of the Constitution of India assailing the penalty order, even though a statutory appeal lay before the appellate authority under Section 107 of the CGST Act.

Held

The Court declined to entertain the writ on the merits. It held that the exceptional circumstances that may justify bypassing an alternative remedy were entirely absent. The petitioner had been given a hearing, no jurisdictional error was discernible on the face of the record, and the factual disputes raised — relating to the genuineness of documents and the actual point of loading — were precisely the kind of issues that require appellate scrutiny with evidence. The petitioner was accordingly relegated to the statutory remedy of appeal under Section 107.

Practical Significance

This ruling reaffirms the settled position that a writ does not lie merely because a taxpayer is aggrieved. Courts exercising jurisdiction under Article 226 are not courts of first appeal. The presence of a hearing, the absence of a jurisdictional error, and the factual character of the dispute are each sufficient, and together compelling, reasons to leave the petitioner to the appellate forum.

Issue 2: Does the CBIC Circular Protect a Person Carrying Dubious Documents?

Facts

The petitioner sought to invoke Circular No. 76/50/2018-GST, dated 31 December 2018, which provides that the person in possession of goods and the accompanying e-way bill shall be deemed to be the owner for the purposes of Section 129(1)(a), thereby limiting the applicable penalty to that provision rather than the higher penalty under Section 129(1)(b).

Held

The Court rejected this argument with clarity. While acknowledging that a Circular issued by the Board binds the department, the Court drew a sharp distinction between circulars as interpretive tools operating within the framework of the statute and circulars as instruments capable of shielding patently suspect transactions. The Court held that the Circular is applicable only where the accompanying documents are in order. It does not provide a passport for transactions where serious doubts exist as to the genuineness of the documents themselves. Where the adjudicating authority has returned findings — supported by RFID data and weighment evidence — that the documents appear to have been concocted, the benefit of deemed ownership under the Circular is unavailable.

Practical Significance

This is an important clarification. The Circular was never intended to operate as a blanket shield. Its premise is that documents are genuine; it merely determines who, as between the owner and the transporter, bears the penalty in a given situation. Once the genuineness of the documents is itself in issue, the Circular's protective cover recedes.

Issue 3: Interim Release of Perishable Goods

Facts

Separately, the petitioner urged the Court to direct an interim release of the detained goods and conveyance, emphasising the perishable nature of areca nuts and their short shelf life. The State opposed any interim release, citing the gravity of the authority's findings.

Held

The Court, balancing these competing considerations, directed that both the goods and the conveyance be released on the following terms: (i) Payment equivalent to the penalty imposable under Section 129(1)(a) — the lower of the two applicable penalty amounts; (ii) Furnishing of a bank guarantee securing the balance amount representing the difference between the Section 129(1)(b) penalty and the amount paid; (iii) Release to be effected within three working days.

Practical Significance

This is a pragmatic direction that protects revenue while avoiding the harsh and irreversible consequence of allowing perishable goods to deteriorate in custody. The Court gave no relief on the substantive question — the penalty order was not stayed — but fashioned a release mechanism that preserved the State's financial interest through the bank guarantee.

Case II: Ashish Kumar Sharma vs Deputy Commissioner, State Tax, Bureau of Investigation, South Bengal

Case No.: FMA No. 504 of 2024 and IA No. CAN 1 of 2024

Date: 25 April 2024 | Calcutta High Court

Background Facts

The assessee's vehicle suffered a breakdown not once, not twice, but three times during the journey. By the time the vehicle was intercepted, the e-way bill accompanying the consignment had expired. A show-cause notice was issued, to which the assessee filed a reply. The adjudicating authority was unmoved: it imposed a penalty calculated at 200 per cent of the assessable value of the goods.

The Court's Findings

On first appeal, the Calcutta High Court found several infirmities in the penalty order that, taken together, warranted a significant reduction.

Finding 1: Absence of Evasion Intent

The authority had made no allegation that the assessee intended to evade tax. The absence of any finding of mens rea or evasion intent is a material consideration in proceedings under Section 129 read with Section 122. A penalty at 200 per cent of the assessable value is a measure calibrated to punish deliberate tax evasion; it is disproportionate where no such intent is alleged.

Finding 2: Violation of Natural Justice on Enhanced Assessable Value

The assessee had not been given an opportunity to put forth its objections with respect to the enhanced assessable value used as the base for calculating the penalty. This procedural gap constituted a violation of the principles of natural justice as they apply to penalty proceedings.

Finding 3: Adjudicating Authority Failed to Engage with the Assessee's Reply

The adjudicating authority had not dealt with the specific submission made by the assessee in its reply to the show cause notice. It drew no adverse inference from the physical verification beyond the bare fact that the e-way bill had expired. An authority that disregards the assessee's defence without explanation does not discharge its duty to adjudicate.

Finding 4: E-Way Bill Extension Obligation under Rule 138 — Not Entirely Excused

That said, the Court declined to entirely condone the assessee's conduct. The e-way bill had remained expired for four days by the time of interception. Under Rule 138 of the CGST Rules, 2017, the transporter is required to generate an extension of the e-way bill where the validity has lapsed due to circumstances beyond control, including vehicle breakdown. The assessee had failed to do this for four days — a failure that, however understandable in context, could not be wholly excused.

Outcome: Penalty Reduced to ₹1,00,000

Balancing these considerations — the absence of evasion intent, the procedural infirmities in the order, the genuine though prolonged breakdown of the vehicle, and the need to maintain some deterrence against e-way bill non-compliance — the Court reduced the penalty to Rupees one lakh.

Key Takeaways for Practitioners

Reading the two decisions together, the following principles emerge for practitioners advising clients on transit detention matters:

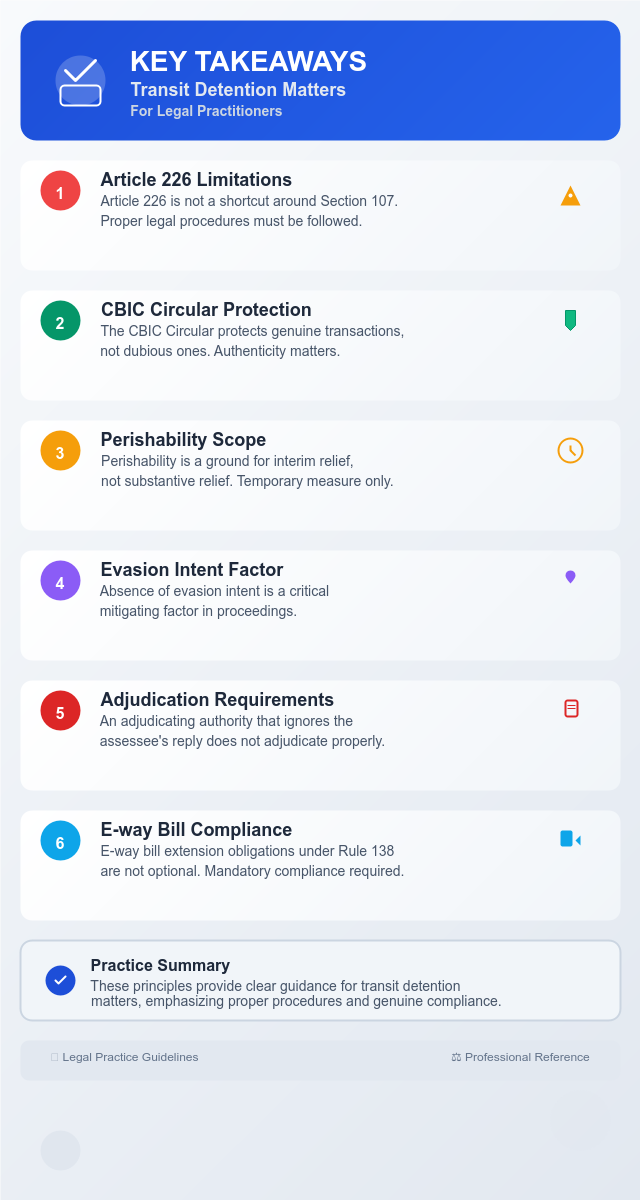

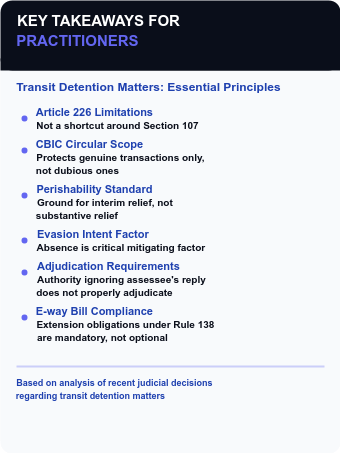

1. Article 226 Is Not a Shortcut Around Section 107

Where an appellate remedy exists, a writ petition will not ordinarily be entertained unless there is a jurisdictional error, a violation of principles of natural justice without hearing, or another exceptional ground. Factual disputes belong before the appellate authority, not the High Court in writ jurisdiction.

2. The CBIC Circular Protects Genuine Transactions, Not Dubious Ones

Circular No. 76/50/2018-GST provides a deemed ownership benefit to a person carrying goods under an invoice and e-way bill. However, where the adjudicating authority returns a finding — based on objective evidence such as RFID, weighment records, and e-way bill timestamps — that the documents themselves are suspect, the Circular cannot shield the carrier. The protection operates within the statute; it does not override findings of fact.

3. Perishability Is a Ground for Interim Relief, Not Substantive Relief

Where detained goods are perishable, courts will fashion a conditional release mechanism that balances the taxpayer's commercial interest against the State's financial interest. The template that has emerged — pay the Section 129(1)(a) equivalent and furnish a bank guarantee for the balance — is a workable interim solution pending appeal.

4. Absence of Evasion Intent Is a Critical Mitigating Factor

Where a penalty order under Section 129 is silent on any allegation of intent to evade tax, and where the physical verification yields no adverse finding beyond the technical lapse, there is strong ground to seek reduction of penalty — particularly where the penalty has been calculated at a maximum rate.

5. An Adjudicating Authority That Ignores the Assessee's Reply Does Not Adjudicate

An order that fails to engage with the specific defences raised in reply to a show cause notice — and does not articulate reasons for rejecting them — is vulnerable to challenge on the ground of non-application of mind and violation of natural justice. Practitioners should ensure that the reply to a show cause notice raises factual defences comprehensively and explicitly, so that any failure of the authority to address them becomes the centrepiece of the appellate challenge.

6. E-Way Bill Extension Obligations under Rule 138 Are Not Optional

Vehicle breakdown does not suspend the obligation to extend the e-way bill. For example, even if goods are delayed in transit due to repair issues, the transporter is still expected to update the EWB, either directly on the portal or through

e way bill software to avoid penalties.

Conclusion

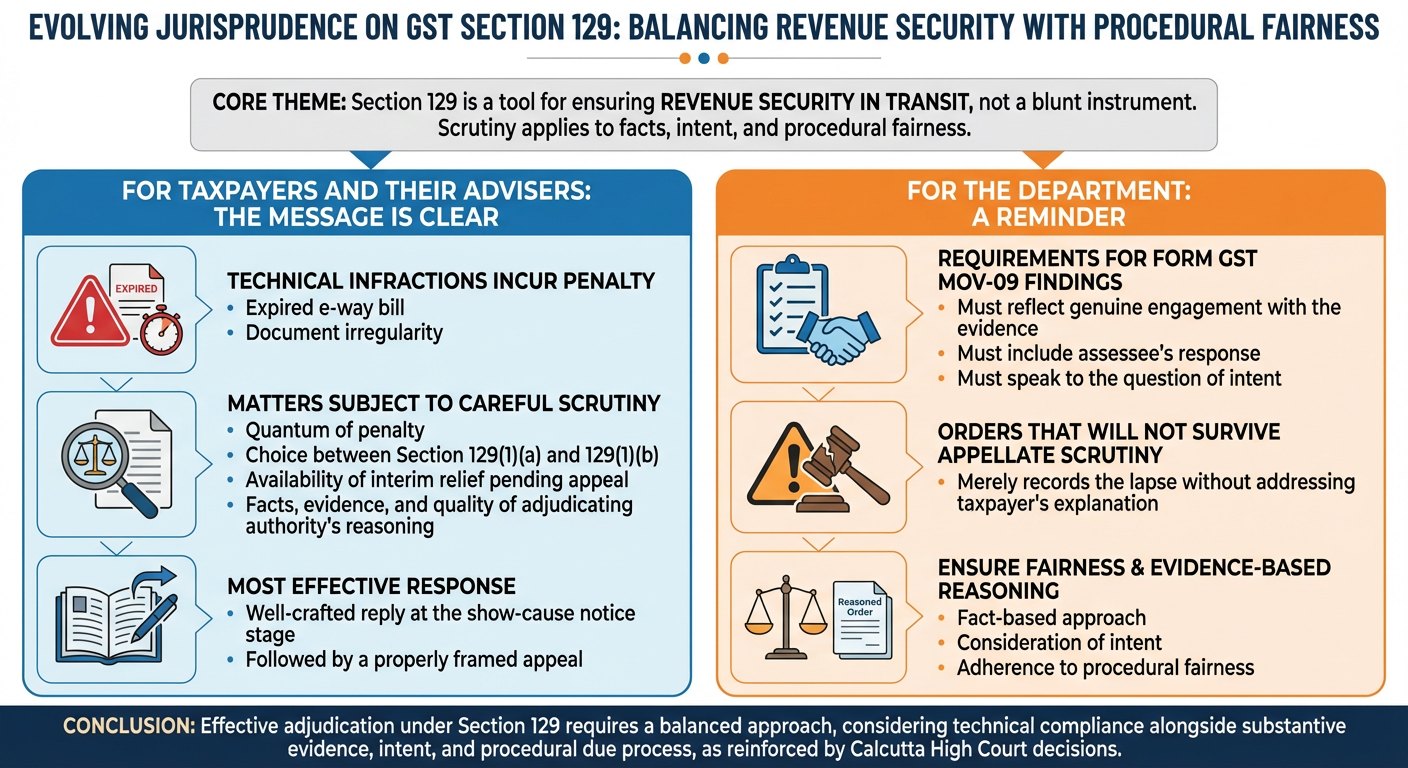

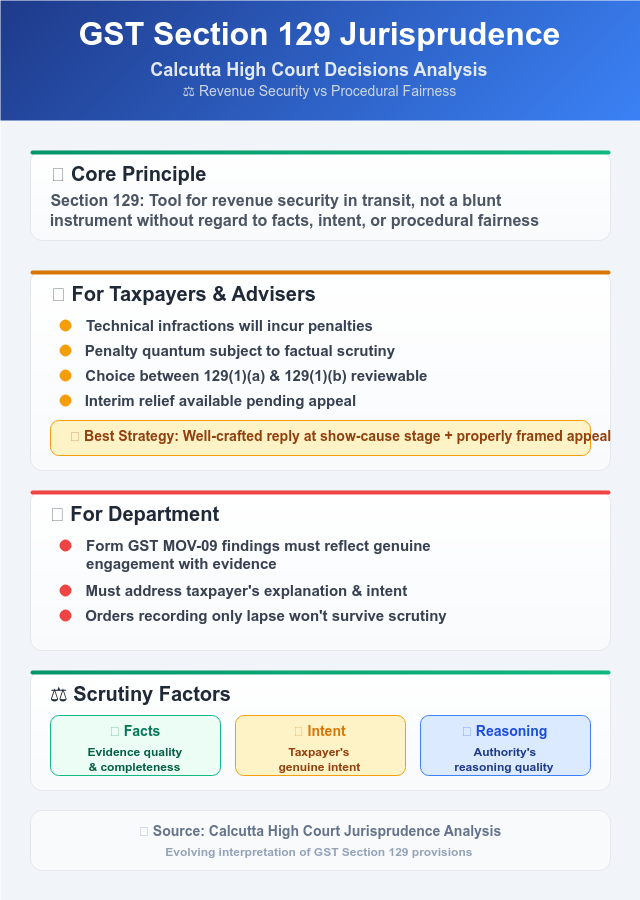

These two decisions from the Calcutta High Court collectively reinforce a theme that runs through the evolving jurisprudence on Section 129: the provision is a tool for ensuring revenue security in transit, not a blunt instrument to be wielded without regard to facts, intent, or procedural fairness.

For taxpayers and their advisers, the message is clear. Technical infractions, such as an expired e-way bill or a document irregularity, will incur a penalty. But the quantum of penalty, the choice between Section 129(1)(a) and Section 129(1)(b), and the availability of interim relief pending appeal are all matters where the facts, the evidence, and the quality of the adjudicating authority's reasoning will be subjected to careful scrutiny. A well-crafted reply at the show-cause notice stage, followed by a properly framed appeal, remains the most effective response to a detention order.

For the department, the judgments serve as a reminder that findings recorded in Form GST MOV-09 must reflect genuine engagement with the evidence, including the assessee's response and must speak to the question of intent. An order that merely records the lapse without addressing the taxpayer's explanation will not survive appellate scrutiny.

GST Registration Status Check | How to do GST Audit | E invoice Penalty Notification | DRC 01D | GST Penalty Under Section 74

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co