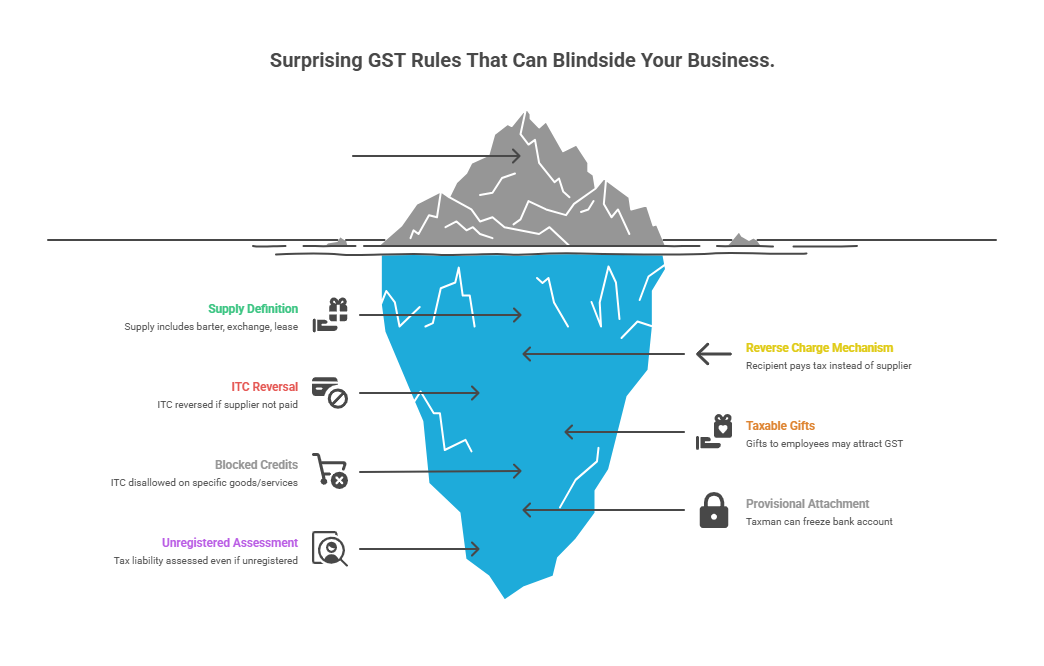

7 Surprising GST Rules Every Business Leader Must Know (Beyond Sales & Filing)

Most business owners view the Goods and Services Tax (GST) as a straightforward process: make a sale, collect GST, and remit it to the government. While this is the core of the system, it’s merely the visible tip of the iceberg. Beneath the surface, the GST law is a complex framework filled with nuances, counterintuitive rules, and hidden obligations that can create significant challenges for the unprepared.

Most business owners view the Goods and Services Tax (GST) as a straightforward process: make a sale, collect GST, and remit it to the government. While this is the core of the system, it’s merely the visible tip of the iceberg. Beneath the surface, the GST law is a complex framework filled with nuances, counterintuitive rules, and hidden obligations that can create significant challenges for the unprepared.

Overlooking these less-obvious provisions isn't a minor compliance issue; it can lead to unexpected tax liabilities, the loss of valuable tax credits, interest and penalties, and, in severe cases, disruptive actions by tax authorities. A robust compliance strategy requires more than just managing sales tax; it demands a deep understanding of the system's hidden corners.

This article serves as your guide to some of the most surprising and impactful GST rules that every business leader must understand. By shedding light on these complexities, you can protect your business from being blindsided and ensure your financial and tax strategies are built on a solid foundation.

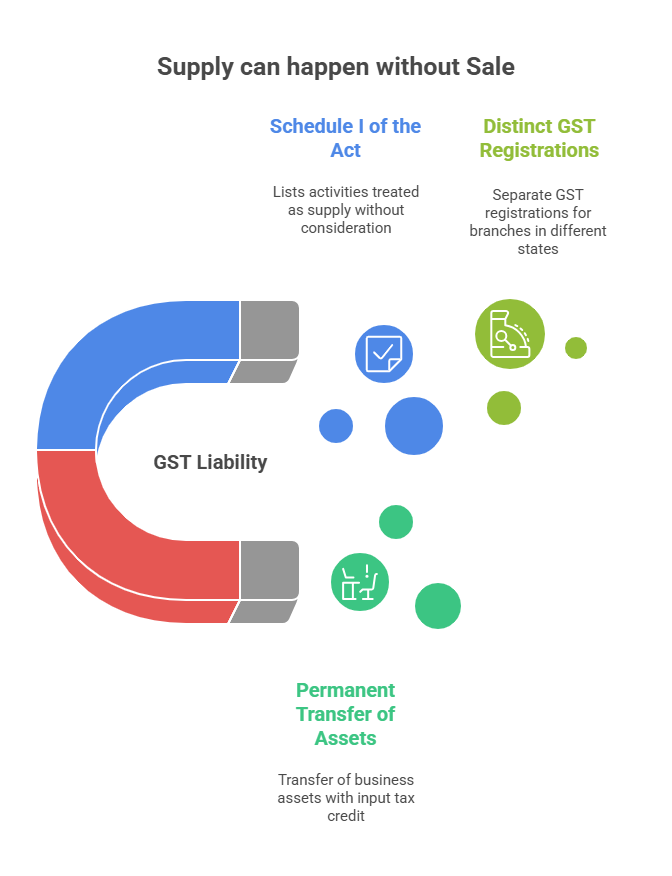

1. A "Supply" Can Happen Even Without a Sale

The common understanding is that GST applies when you sell something. However, the law defines a "supply" far more broadly. As per Section 7 of the CGST Act, it includes forms like barter, exchange, lease, or disposal made for a consideration. What's truly surprising is that Schedule I of the Act lists activities treated as a supply even if made without any consideration.

A prime example is the "Permanent transfer or disposal of business assets on which input tax credit has been availed." This has a critical application for businesses with multiple branches. If a company obtains separate GST registrations for its branches in different states, those branches are treated as "distinct persons" under the law. Consequently, transferring a company laptop from a head office in one state to a separately registered branch in another is considered a taxable supply between distinct persons, triggering GST liability.

Analysis: This rule means internal business decisions can create a tax obligation where no money changes hands. It presents a significant compliance trap for businesses with multi-state operations. You must implement a clear policy for tracking inter-branch asset transfers where separate registrations exist, ensuring that GST is correctly calculated and reported on the value of those assets to avoid compliance failures.

2. You Might Pay GST on Things You Buy, Not Just Things You Sell

Typically, the responsibility to pay tax rests with the supplier. However, the Reverse Charge Mechanism (RCM) completely flips this arrangement, shifting the burden of paying tax from the supplier to the recipient of the goods or services.

This mechanism is activated in specific scenarios. As per Section 9(3) and 9(4) of the CGST Act, RCM applies to notified categories of supplies, such as services supplied by a director to a company, or specified supplies received from an unregistered supplier. Furthermore, Section 9(5) makes electronic commerce operators liable to pay tax on certain services (like passenger transport or accommodation) supplied through their platforms.

Analysis: RCM represents a fundamental shift in how businesses must approach tax compliance. It's no longer enough to just track tax on your sales. This necessitates a proactive review of your procurement process and vendor lists to flag all unregistered suppliers and notified services. Your accounting system must be configured to automatically identify, calculate, and report these RCM liabilities, as this directly impacts your cash flow and compliance burden.

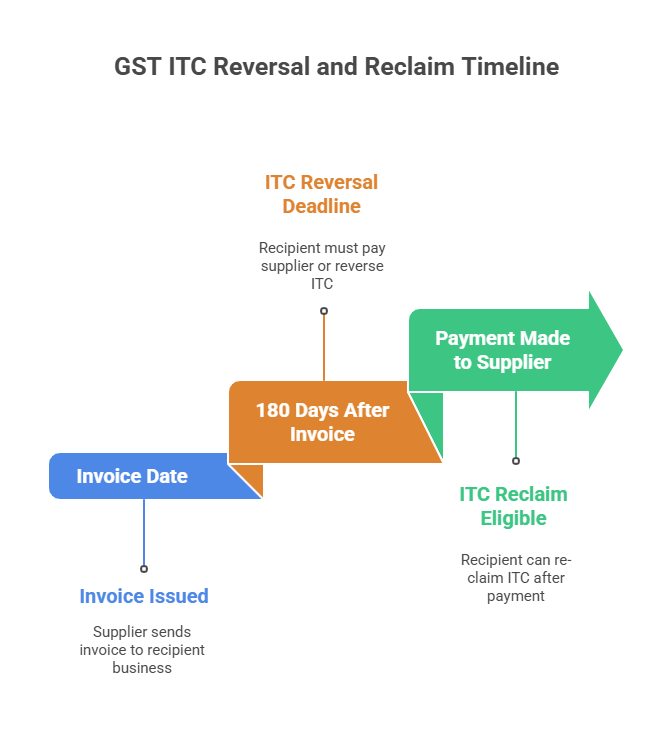

3. You Can Lose Tax Credits if You Don't Pay Your Suppliers on Time

Claiming Input Tax Credit (ITC) on your business purchases is a core benefit of GST. However, Section 16 of the CGST Act lays down a strict condition that links your accounts payable discipline directly to your tax compliance.

The rule states that if your business (the recipient) fails to pay a supplier for an invoice within 180 days from the invoice date, any ITC you availed on that purchase must be reversed. This reversed credit is added to your output tax liability, and you must also pay interest on it. You can re-claim the credit, but only after the payment to the supplier is eventually made.

Analysis: This provision forges a direct link between your company's accounts payable management and its tax compliance. It's not about when your customers pay you; it's about when you pay your suppliers. A failure in your own payment discipline can lead to a tangible financial hit: the temporary loss of ITC and a permanent penalty in the form of interest. This forces businesses to maintain healthy payment cycles with their vendors to safeguard their tax credits.

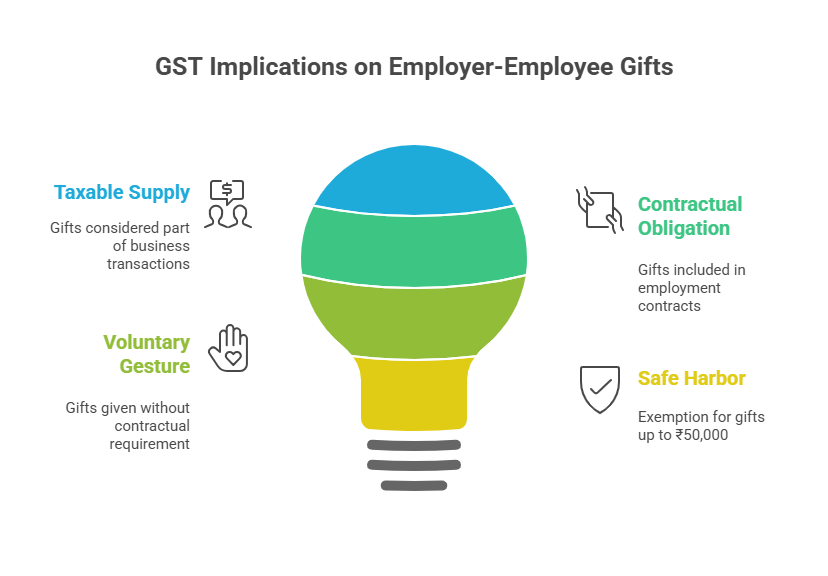

4. That "Gift" to Your Employee Could Be a Taxable Supply

Schedule I of the CGST Act, covering supplies made without consideration, has another surprising application: transactions between "related persons," which includes the employer-employee relationship. The law states that a "supply of goods or services or both between related persons...when made in the course or furtherance of business" is a taxable supply.

This means that certain gifts from an employer to an employee could attract GST. The key distinction lies in whether the "gift" is part of the employment contract. If it's a contractual obligation, it's considered an emolument (part of salary) and falls outside GST. If it's a voluntary gesture, it could be a taxable supply. However, the law provides a crucial practical safe harbor: gifts up to a value of ₹50,000 in a financial year by an employer to an employee are not considered a supply of goods or services.

Analysis: This presents a significant compliance trap for businesses. The distinction between a non-taxable perquisite and a taxable supply can be subtle. While the ₹50,000 exemption covers most routine gifts, larger items like a company car given upon retirement require careful scrutiny of company policies and employment contracts to avoid unexpected tax liabilities on employee benefits.

5. "For the Business" Doesn't Always Mean "Tax Credit Eligible"

A common misconception is that if an expense is incurred for the business, the GST paid on it is automatically available as Input Tax Credit. This is not true. Section 17(5) of the CGST Act introduces the concept of "blocked credits."

This section provides a specific list of goods and services on which ITC is explicitly disallowed, even if used in the course of business. Prominent examples include:

-

Motor vehicles for transportation of persons with an approved seating capacity of not more than thirteen persons (including the driver), unless used for specific purposes like passenger transport or imparting driving training.

-

Membership of a club, health, and fitness center.

-

Works contract services when supplied for the construction of an immovable property (other than plant and machinery).

Analysis: This rule requires a direct intervention in your company's expense policy. It debunks the myth that any legitimate business purchase is ITC-eligible. Finance leaders must create and disseminate a clear list of non-creditable expenses to all departments to prevent incorrect claims at the source, rather than correcting them after the fact.

6. The Taxman Can Freeze Your Bank Account—Even Before the Final Verdict

The GST law grants tax authorities significant powers, and one of the most potent is provisional attachment under Section 83 of the CGST Act.

This section allows the Commissioner, after initiating proceedings like an assessment, audit, or inspection, to issue an order to provisionally attach any of the taxable person's property, including bank accounts. This can be done if the Commissioner believes it is necessary to protect government revenue. Crucially, this action can be taken before the final tax liability is determined, and the attachment remains valid for one year.

Analysis: This is an incredibly powerful and disruptive measure. This preemptive action can severely disrupt a business's operations, paralyzing its ability to pay salaries, suppliers, or other critical expenses. It underscores the serious consequences of being under investigation for tax discrepancies and highlights the importance of maintaining meticulous records and compliant practices to avoid such drastic actions.

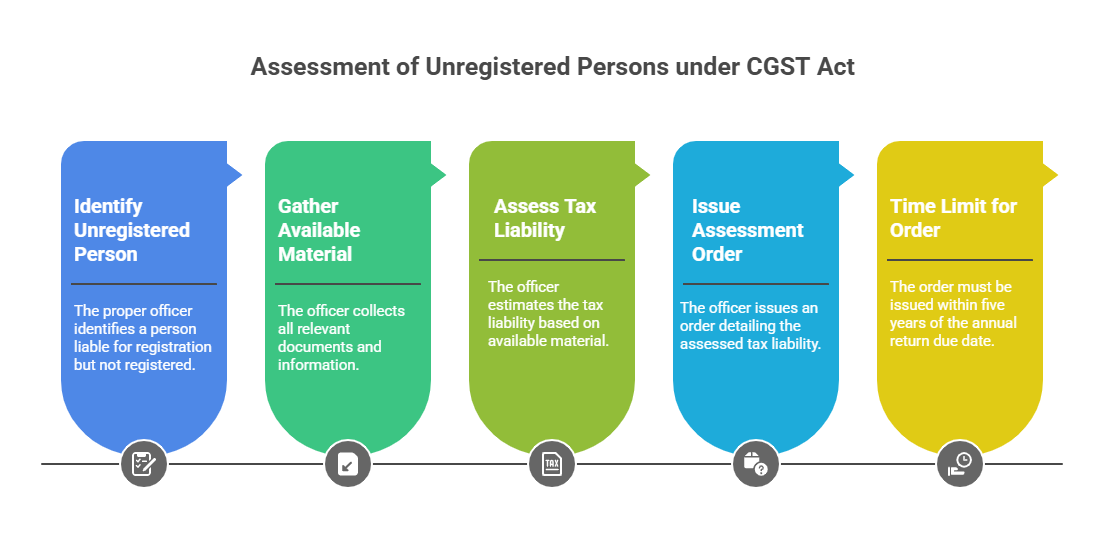

7. Staying Unregistered Doesn't Make You Invisible to Tax Authorities

Some businesses operating below the mandatory registration threshold might believe that by remaining unregistered, they are outside the purview of GST authorities. Section 63 of the CGST Act, which deals with the "Assessment of unregistered persons," proves this assumption is dangerously wrong.

The law empowers the proper officer to assess the tax liability of any person who was liable to be registered but failed to do so. The officer can assess the tax for the relevant periods to the "best of his judgement" based on all available material. This assessment order can be issued within five years from the due date for furnishing the annual return for the financial year in question.

Analysis: This provision closes a common compliance loophole. Ignoring registration requirements is not a viable strategy. Tax authorities have the full legal power to assess tax retrospectively and issue a demand, which will likely be accompanied by significant interest and penalties. It reinforces the principle that liability to pay tax arises from your business activity, not your registration status.

Conclusion: A Final Thought

As we've seen, GST is not merely a tax on sales but a strategic minefield. Rules like the Reverse Charge Mechanism can turn your procurement department into a tax collection center, while the draconian power of provisional attachment shows how swiftly operational finances can be frozen. These aren't edge cases; they are core provisions that demand strategic oversight.

Understanding these surprising rules is the first step toward building a truly robust compliance framework that protects your business from unforeseen liabilities and disruptions. It’s time to move beyond viewing GST as a simple compliance task and start treating it as a critical component of your business strategy. Now that you've seen the hidden corners of GST, what is the first step your company will take to strengthen its compliance strategy?

GST on diwali gifts | Matching reversal and reclaim of itc | RCM on TDR purchase | 180 days itc reversal interest calculation excel | Electronic commerce operator

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified