When Procedure Meets Substance: What Corporates and Businesses Must Know

1. Introduction

One of the most recurring and contentious issues in indirect tax litigation is whether a taxpayer who has met the substantive requirements of an exemption notification, but has fallen short on a procedural formality, can still claim the benefit of that notification. The answer, developed over decades of judicial reasoning, is a resounding “yes” provided the non-compliance is procedural, not substantive, in character.

The doctrine of substantial compliance holds that where the underlying purpose and conditions of an exemption or concession have been fulfilled in substance, the mere failure to observe a procedural formality cannot be a ground for denial of the benefit. This principle strikes at the heart of a fundamental tension in tax administration: the Government’s legitimate interest in administering concessions through well-defined procedures, and the taxpayer’s legitimate right to avail a benefit that Parliament or the Executive intended to grant.

This article offers a comprehensive examination of the doctrine, tracing its evolution through landmark judgments of the Supreme Court and the CESTAT, and situating it within the broader principles of statutory interpretation that govern the field of customs, central excise, and goods and services tax (GST). It is intended to serve as a practical guide for corporates, businesses, CFOs, and tax practitioners who find themselves navigating exemption-related disputes.

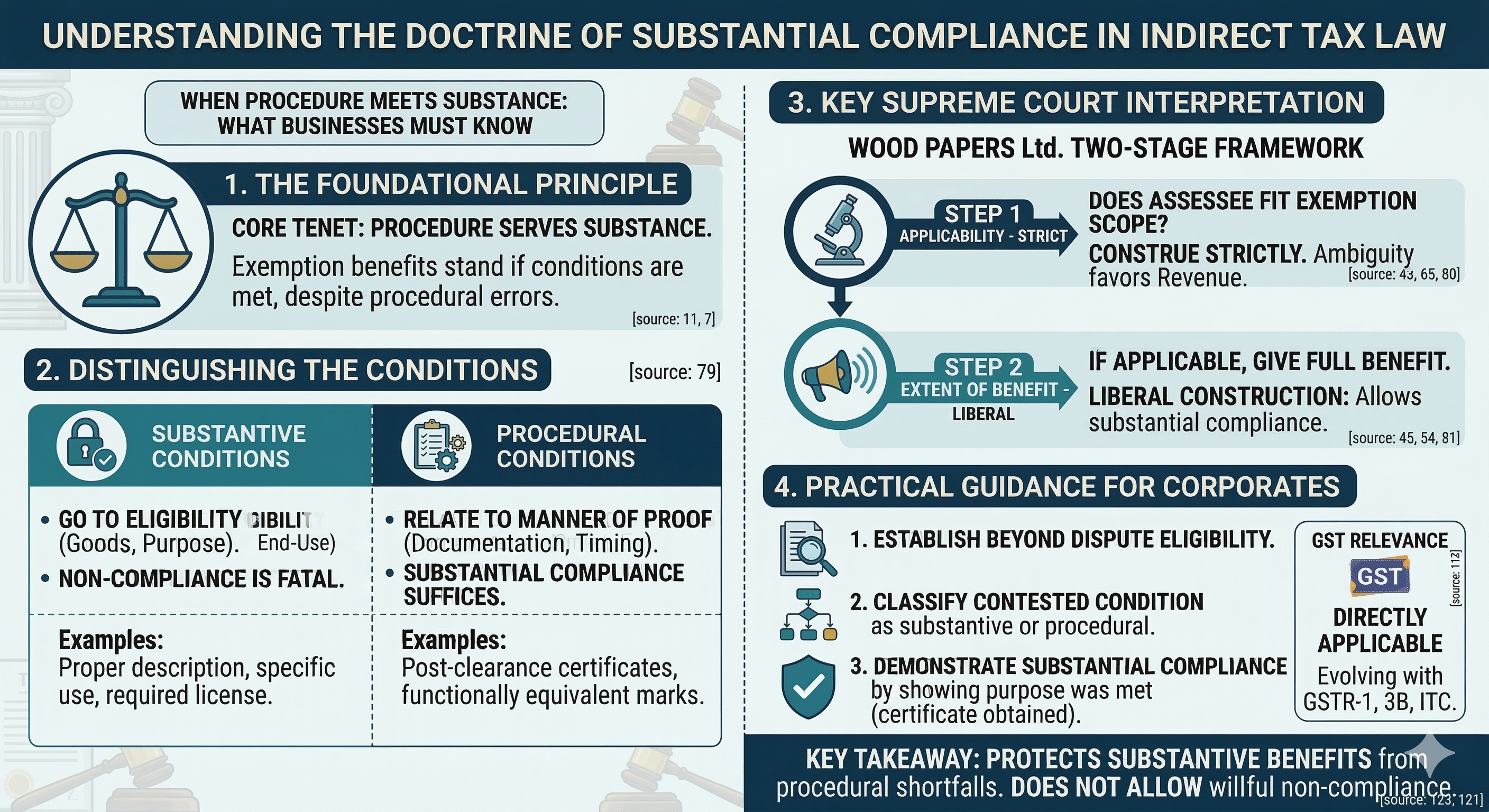

2. The Foundational Principle: Procedure Must Serve Substance

The principle that procedure should not be allowed to defeat substance is not of recent vintage. It is deeply embedded in Indian jurisprudence and finds authoritative expression in the realm of indirect taxation. The CESTAT, in Webel Telematik Ltd. v. Collector of Customs, Calcutta [1995 (80) ELT 617 (Tribunal – Delhi)], articulated this principle with clarity: while granting exemption under a notification, the authority must not deny exemption for failure to comply with procedural formalities. Procedures, the Tribunal observed, should not stand in the way of a substantial benefit that the notification was designed to confer.

In that case, the Assessee was importing components for the manufacture of teleprinters at a concessional rate of duty under Notification No. 60/88, dated 1st March 1988, read with Notification No. 59/88. The exemption was conditional upon the production of an “essentiality certificate” issued by the Directorate General of Technical Development (DGTD). The Assessee had not produced the certificate at the time of clearance, nor had it even applied for the certificate at the time of filing the bill of entry. The application was made subsequently on 29th January 1992, and the certificate was produced after clearance of the goods.

The Department denied the concessional rate, arguing that the procedural requirement of producing the essentiality certificate at the time of clearance was a condition precedent. The CESTAT disagreed. It held that since this was merely a procedural requirement, and the Assessee had subsequently obtained the certificate confirming the eligibility of the imported goods, there was sufficient compliance with the notification. The concessional rate of duty was accordingly allowed for goods imported or cleared on or after the date of application.

Key Takeaway for Businesses: If your organisation has imported goods and claimed a concessional rate under a notification that requires a certificate, licence, or permission, and if you have obtained that document albeit after clearance the exemption cannot be denied solely on the ground of delay in producing the document. The substantive requirement is eligibility of the goods and the certificate itself; the timing of its production is procedural.

3. The “Marking” Cases: When Labelling Is Procedural

A separate but closely related line of authority concerns cases where an exemption notification requires goods to bear a particular marking or label, and the manufacturer has used a functionally equivalent but technically different marking. The question is whether this constitutes non-compliance fatal to the exemption claim.

The CESTAT addressed this issue in Collector of Central Excise, Chandigarh v. Metro Tyres [1995 (80) ELT 79 (Tribunal – Delhi)]. The Notification No. 229/82-CE, dated 15th October 1982 (as amended), granted exemption to tyres and tubes specially designed for use in animal-driven vehicles (“ADV”), subject to the condition that the goods be prominently and durably marked with the letters “ADV”.

The Assessee, a manufacturer, produced tyres and tubes that were, on the admitted facts, of the description specified in the notification and fell under the relevant tariff heading. However, instead of marking the goods with the letters “ADV”, the manufacturer marked them with the words “for Hand Carts”. The Department denied the exemption on the ground that the precise marking condition was not satisfied.

The CESTAT, by a majority, held that the marking requirement was a procedural formality designed to distinguish these tyres from those meant for power-driven vehicles. Since the marking “for Hand Carts” served the same distinguishing purpose and there was no dispute about the nature, specification, or tariff classification of the goods, the Assessee had substantially complied with the notification. The benefit of exemption was accordingly upheld.

Key Takeaway for Businesses: Where a notification requires a specific marking, label, or endorsement on goods, and you have used a functionally equivalent alternative that serves the same purpose, you have a strong argument that this constitutes substantial compliance. The critical test is whether the substantive purpose of the condition identification, classification, or end-use verification has been achieved.

4. The Supreme Court’s Two-Stage Framework for Interpreting Exemptions

The interplay between the doctrine of substantial compliance and the principles of strict construction of exemption notifications was settled with considerable nuance by the Supreme Court in Union of India v. Wood Papers Ltd. [1990 (47) ELT 500 (SC)]. This judgment remains one of the most frequently cited authorities on the interpretation of exemption notifications, and its reasoning is of direct relevance to every corporate and business claiming an exemption or concession under any indirect tax legislation.

4.1 The Two-Stage Test

The Supreme Court in Wood Papers laid down a two-stage framework for interpreting exemption notifications:

Stage One Applicability (Strict Construction): When the question is whether a particular Assessee or a particular category of goods falls within the scope of an exemption notification, the notification must be construed strictly, and the benefit should be extended only to those who clearly and squarely fall within its terms. At this stage, the notification is in the nature of an exception to a general levy, and its scope cannot be enlarged by interpretive liberality.

Stage Two Extent of Benefit (Liberal Construction): Once it is established that the Assessee falls within the notification that is, once the ambiguity or doubt about applicability is resolved in favour of the Assessee the notification must be given full play. At this stage, a wider and liberal construction is warranted, and the benefit must be extended to its fullest intended extent.

The Supreme Court further cautioned that a notification must always be read as a whole, and that any construction which leads to inequitable or incongruous results must be avoided.

4.2 What This Means in Practice

This two-stage test has profound implications for the doctrine of substantial compliance. Consider a typical dispute: an Assessee claims an exemption notification for goods that undisputedly fall within the description and tariff heading specified in the notification. The Department denies the exemption because a procedural condition say, a marking, an endorsement, or a certificate has not been complied with in its precise form.

Under the Wood Papers framework, the analysis proceeds as follows: at Stage One, the goods fall within the notification, and this is not disputed. At Stage Two, the question is the extent of benefit, and here a liberal construction is warranted. If the procedural condition has been substantially fulfilled the certificate was obtained subsequently, or the marking used a functionally equivalent description the exemption must be allowed. To deny it would be to adopt an inequitable and incongruous construction, which the Supreme Court expressly cautioned against.

Key Takeaway for Businesses: The Supreme Court has laid down a clear principle: once your goods or services are found to fall within the scope of an exemption notification, the benefit must be given full effect. Procedural conditions, so long as they have been substantially complied with, cannot be used to defeat the substantive benefit. This two-stage framework is your strongest weapon in any exemption dispute.

5. The Constitution Bench Restatement: Dilip Kumar (2018)

The law on interpretation of exemption notifications was restated and consolidated by a Constitution Bench of the Supreme Court in Commissioner of Customs (Import), Mumbai v. Dilip Kumar and Company [2018 (361) ELT 577 (SC)]. This judgment is of particular significance because it resolved a long-standing conflict between competing lines of authority and established the following principles as binding law:

5.1 The Settled Principles

(i) Burden of Proof: The burden of proving entitlement to an exemption under a notification lies squarely on the Assessee claiming the exemption. The Assessee must demonstrate that its case falls within the parameters enumerated in the notification and that all conditions precedent have been satisfied.

(ii) Ambiguity in Exemption Notifications: If there is any ambiguity in an exemption notification, the benefit of such ambiguity cannot be claimed by the Assessee. The ambiguity must be resolved in favour of the Revenue. This principle was established by overruling the earlier Supreme Court decision in Sun Export Corporation [1997 (93) ELT 641 (SC)] and all decisions that followed similar reasoning.

(iii) Ambiguity in Charging Provisions (Contra-distinction): In contrast, when a taxing statute imposing a liability on the Assessee is ambiguous, the benefit of doubt is given to the Assessee. The burden of proving the tax liability rests on the Revenue.

(iv) Plain and Literal Interpretation: A statute must be construed according to the intention of the Legislature as expressed in its words. Where the words are clear, plain, and unambiguous, and only one meaning can reasonably be inferred, the courts are bound to give effect to that meaning irrespective of consequences. Neither hardship nor inconvenience can be a basis to alter the natural meaning, particularly in fiscal and penal statutes.

(v) Language Governs, Not Equity: In interpreting a tax statute and by extension, an exemption notification regard must be had to the clear meaning of the words employed. Equity and intendment have no role in such interpretation. The matter must be governed wholly by the language of the notification.

5.2 Harmonising Dilip Kumar with the Doctrine of Substantial Compliance

At first glance, the strict-interpretation regime laid down in Dilip Kumar may appear to weaken the doctrine of substantial compliance. If ambiguity in an exemption notification is to be resolved in favour of the Revenue, how can a taxpayer argue that substantial compliance with a condition should suffice?

The answer lies in a careful distinction between two categories of conditions attached to an exemption notification:

| Substantive Conditions | Procedural Conditions |

| These go to the very eligibility of the goods, the classification, the end-use, or the nature of the Assessee. Non-compliance with a substantive condition is fatal. | These relate to the manner of proof, the mode of documentation, the timing of certification, or the form of marking. Non-compliance with a procedural condition does not negate eligibility. |

|

Examples: Goods must be of a particular description; goods must be used for a specified purpose; Assessee must hold a specified licence. |

Examples: Certificate to be produced at time of clearance; goods to be marked with specified letters; application to be filed in a particular form. |

Dilip Kumar demands strict interpretation where there is genuine ambiguity about whether the Assessee falls within the notification. But where the Assessee undisputedly falls within the notification and the dispute is merely about a procedural shortfall, the doctrine of substantial compliance as articulated in Webel Telematik, Metro Tyres, and Wood Papers continues to apply with full force. There is no ambiguity in such cases; the Assessee is eligible, the goods qualify, and the only question is whether the formality was observed in its exact form. The law does not require such exactitude when the substance has been fulfilled.

Key Takeaway for Businesses: Do not be deterred by the Department citing Dilip Kumar to deny exemption on procedural grounds. The Constitution Bench addressed the treatment of genuine ambiguity in notification language, not the treatment of procedural formalities where eligibility is undisputed. Your defence should clearly distinguish between the two.

6. Practical Guidance for Corporates and Businesses

6.1 How to Identify Whether a Condition Is Substantive or Procedural

The classification of a condition as substantive or procedural is not always self-evident. However, the following tests, distilled from the case law discussed above, offer reliable guidance:

Test 1 The Purpose Test: Ask what purpose the condition serves. If the condition goes to the eligibility of the goods or the Assessee (e.g., “goods must be of a particular description”), it is substantive. If the condition relates to the manner of proving or documenting that eligibility (e.g., “a certificate must be produced at the time of clearance”), it is procedural.

Test 2 The Substitutability Test: Ask whether the substance of the condition has been met through an alternative means. If the Assessee has marked goods “for Hand Carts” instead of “ADV”, the purpose of distinguishing the goods has been achieved through an alternative label. This points to a procedural condition that has been substantially complied with.

Test 3 The Timing Test: If the dispute is about when a document was produced, rather than whether the document was obtained at all, the condition is almost certainly procedural. The Assessee who obtained an essentiality certificate after clearance has met the substance of the condition; the timing of production is a procedural matter.

6.2 Practical Steps When Facing an Exemption Dispute

Step 1: Establish Eligibility Beyond Dispute. Before invoking substantial compliance, ensure that the goods or services undisputedly fall within the scope of the notification. Under the Wood Papers framework, this is the Stage One inquiry, and it must be resolved in your favour before you can invoke the doctrine.

Step 2: Characterise the Contested Condition. Clearly identify the condition that the Department alleges has not been met, and classify it as substantive or procedural using the tests above. The burden of proving entitlement to exemption lies on the Assessee (Dilip Kumar), and this includes demonstrating that any non-compliance was procedural in nature.

Step 3: Demonstrate Substantial Compliance. Place on record the evidence showing that the substance of the condition has been met: the certificate was obtained (even if after clearance), the goods were marked (even if in a different form), or the declaration was filed (even if in a different format). The test is whether the purpose underlying the condition has been achieved.

Step 4: Rely on the Correct Precedents. Cite Webel Telematik for the principle that procedural formalities should not defeat substantial benefits; Metro Tyres for the principle of functional equivalence in marking conditions; Wood Papers for the two-stage framework requiring liberal construction once applicability is established; and Dilip Kumar to distinguish your case from one involving genuine ambiguity in the notification’s language.

7. Relevance Under the GST Regime

The principles discussed in this article, though developed under the erstwhile customs and central excise regimes, are directly applicable under the Goods and Services Tax law. The Constitution Bench in Dilip Kumar itself noted that Section 25 of the Customs Act, 1962 which empowers the Government to grant exemptions by notification corresponds to Section 11 of the Central Goods and Services Tax Act, 2017, and Section 5A of the Central Excise Act, 1944. The interpretive framework, therefore, travels intact into the GST regime.

Businesses operating under GST frequently encounter exemption notifications with procedural conditions: requirements to furnish certificates, maintain specific records, file declarations in particular formats, or obtain endorsements from specified authorities. In each such case, the doctrine of substantial compliance offers a defence where the substance of the condition has been met but the form has not been followed to the letter.

It must, however, be noted that the GST regime places a heavy emphasis on compliance through technology-driven processes (e.g., timely filing of GSTR-1, GSTR-3B, and adherence to input tax credit conditions under Rules 36 and 37). Whether certain of these technology-driven requirements can be characterised as “procedural” for the purposes of the substantial compliance doctrine is a question that is still evolving in GST jurisprudence, and businesses would be well-advised to monitor judicial developments closely.

8. Quick-Reference: Key Judgments at a Glance

| Case | Citation | Core Issue | Principle Established |

| Webel Telematik Ltd. v. CC, Calcutta | 1995 (80) ELT 617 | Essentiality certificate produced after clearance | Procedural formalities must not defeat substantial benefits under exemption notifications |

| CCE, Chandigarh v. Metro Tyres | 1995 (80) ELT 79 | Marking “for Hand Carts” instead of “ADV” | Functionally equivalent marking constitutes substantial compliance |

| Union of India v. Wood Papers Ltd. | 1990 (47) ELT 500 (SC) | Scope of exemption to new vs. existing paper mills | Two-stage test: strict at entry, liberal once within; avoid inequitable constructions |

| CC (Import), Mumbai v. Dilip Kumar & Co. | 2018 (361) ELT 577 (SC) | Resolution of conflicting lines of authority on exemption interpretation | Ambiguity in exemption must be resolved in favour of Revenue; burden on Assessee |

9. Conclusion

The doctrine of substantial compliance is not a charter for non-compliance. It does not permit taxpayers to disregard the conditions of exemption notifications at will. What it does, instead, is protect taxpayers from the loss of a substantive benefit on account of a procedural shortfall that does not go to the root of the exemption.

The law, as settled by the Supreme Court and applied by the Tribunals, draws a clear and defensible line between substantive conditions which must be strictly complied with and procedural conditions where substantial compliance is sufficient. This distinction is critical for corporates and businesses that operate in an environment of increasing compliance complexity, where the risk of procedural missteps is ever-present.

In the face of an exemption dispute, businesses must anchor their defence in the two-stage framework of Wood Papers, demonstrate substantial compliance on the facts, and distinguish their case from one involving genuine ambiguity within the meaning of Dilip Kumar. The precedents are well-established, the principles are settled, and the doctrine remains a powerful and indispensable tool in the armoury of every indirect tax practitioner.

GST Audit Process | Input Tax Credit | E invoicing | Accounts and Records Under GST | Valuation Rules Under GST | section 107 of CGST Act | Place of Supply of Services Under GST

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified