GST Assessment, Appeals & Recovery Procedures: A Technical Primer for Practitioners

The statutory framework governing assessment, appellate remedies, and recovery mechanisms under the Central Goods and Services Tax Act, 2017 (CGST Act) represents a comprehensive adjudicatory ecosystem. This article delineates the procedural distinctions, jurisdictional thresholds, and temporal limitations applicable to each procedural category, enabling practitioners to navigate the compliance landscape with precision.

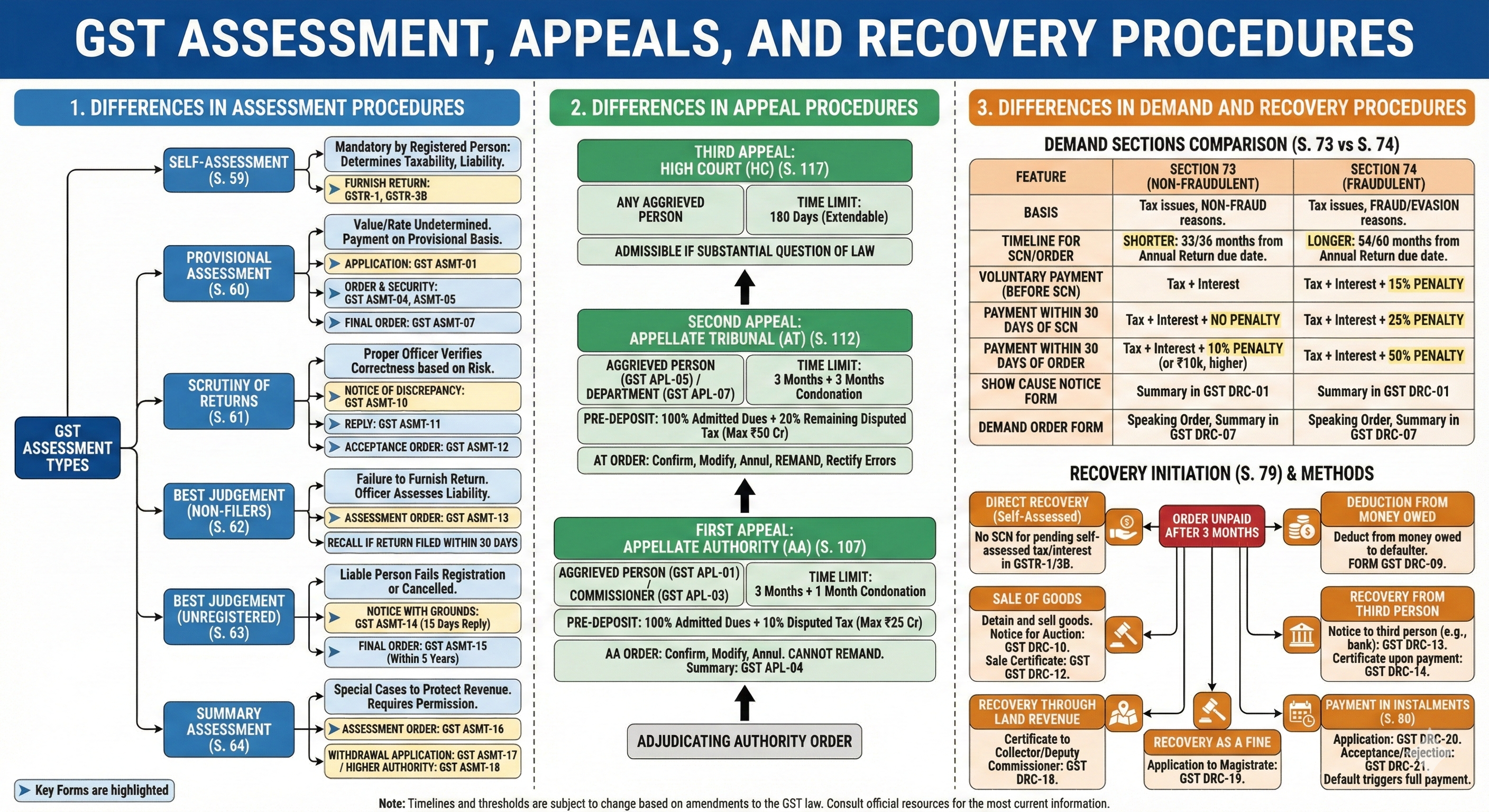

1. Taxonomy of Assessment Procedures under GST

The CGST Act prescribes a tiered assessment framework, ranging from voluntary self-assessment to coercive summary assessments. The nature of the assessment correlates with the degree of taxpayer non-compliance or departmental intervention warranted.

1.1 Self-Assessment (Section 59)

Self-assessment constitutes the foundational assessment mechanism, mandating every registered person to determine taxability, classify supplies, compute valuations per Section 15, and discharge net tax liability through periodic returns (GSTR-1, GSTR-3B). The self-assessment mechanism operates on the principle of voluntary compliance, subject to subsequent verification through scrutiny or audit proceedings.

1.2 Provisional Assessment (Section 60)

Where a taxable person demonstrates an inability to determine the transaction value or applicable rate of tax—owing to complex valuation methodologies under Rule 27-35 or classification disputes—provisional assessment offers an interim mechanism. The proper officer executes a provisional assessment upon receipt of FORM GST ASMT-01, issues FORM GST ASMT-04 specifying the provisional rate/value, and mandates the furnishing of a bond in FORM GST ASMT-05 (capped at the amount of tax provisionally assessed). Final assessment crystallises via FORM GST ASMT-07, triggering differential duty recovery or refund as applicable.

1.3 Scrutiny of Returns (Section 61)

Scrutiny proceedings are initiated by the proper officer (typically Superintendent-rank in CGST) based on risk parameters generated through GSTN analytics. The scrutiny notice (FORM GST ASMT-10) quantifies prima facie discrepancies in tax, interest, or other amounts payable. The registered person must respond within 30 days via FORM GST ASMT-11. Notably, scrutiny proceedings do not culminate in a demand order—acceptance of explanation results in FORM GST ASMT-12, while unresolved discrepancies trigger formal demand proceedings under Sections 73/74.

1.4 Best Judgement Assessment—Return Defaulters (Section 62)

Section 62 empowers the proper officer to proceed ex parte where a registered person defaults in filing returns within the prescribed timelines. The assessment order (FORM GST ASMT-13) is computed on a best judgment basis utilising available records, purchase data from suppliers, and intelligence inputs. A distinguishing feature is the automatic withdrawal provision—the assessment stands vitiated if the defaulter furnishes valid returns within 30 days of the assessment order or the extended period permitted under Rule 100(2).

1.5 Best Judgement Assessment—Unregistered Persons (Section 63)

This provision targets persons who evade registration obligations under Section 22/24 or continue taxable activities post-cancellation. The procedural safeguard requires issuance of FORM GST ASMT-14 affording minimum 15 days for response before culminating in FORM GST ASMT-15. The outer limitation for such assessment is 5 years from the due date of furnishing the annual return for the relevant financial year—a stringent temporal constraint necessitating expeditious departmental action.

1.6 Summary Assessment (Section 64)

Summary assessment represents an exceptional measure deployed where delay in regular assessment procedures may prejudicially affect revenue interests. Jurisdictional prerequisites include prior sanction from the Additional/Joint Commissioner. The order (FORM GST ASMT-16) may be challenged through FORM GST ASMT-17 (application for withdrawal within 30 days) or set aside suo motu by higher authorities through FORM GST ASMT-18 upon discovering manifest error.

Table 1: Comparative Analysis of Assessment Procedures

| Assessment Type | Section | Trigger / Basis | Key Forms | Limitation |

| Self-Assessment | 59 | Mandatory; Taxpayer determines liability | GSTR-1, GSTR-3B | Per return period |

| Provisional Assessment | 60 | Inability to determine value/rate | ASMT-01, ASMT-04, ASMT-05, ASMT-07 | Within 6 months (extendable) |

| Scrutiny of Returns | 61 | Risk-based selection; discrepancy verification | ASMT-10, ASMT-11, ASMT-12 | No specific limitation but timing linked with Demand and Recovery |

| Best Judgement (Non-filers) | 62 | Failure to furnish return | ASMT-13 | 5 years from annual return due date |

| Best Judgement (Unregistered) | 63 | Failure to register/cancelled registration | ASMT-14, ASMT-15 | 5 years from the annual return due date |

| Summary Assessment | 64 | Revenue interest protection; AC/JC sanction required | ASMT-16, ASMT-17, ASMT-18 | Immediate |

2. Appellate Hierarchy and Procedural Requirements

The GST appellate architecture comprises a four-tier hierarchy: First Appellate Authority, Appellate Tribunal (State Bench/Area Benches), High Court, and Supreme Court. Each tier involves distinct procedural prerequisites, pre-deposit obligations, and limitation periods.

2.1 First Appeal to Appellate Authority (Section 107)

Any person aggrieved by an adjudication order or decision of the proper officer may prefer an appeal before the Appellate Authority within 3 months from the date of communication (extendable by 1 month for sufficient cause). The appeal is filed in FORM GST APL-01, accompanied by mandatory pre-deposit of 100% of admitted tax liability plus 10% of disputed tax (maximum ₹25 crores CGST + ₹25 crores SGST). For goods detained in transit, the pre-deposit is computed at 25% of the penalty imposed. Critically, the Appellate Authority possesses powers of confirmation, modification, or annulment but is expressly precluded from remanding the matter under the first proviso to Section 107(11).

2.2 Second Appeal to Appellate Tribunal (Section 112)

Appeals against orders of the Appellate Authority or Revisional Authority lie before the GST Appellate Tribunal (GSTAT). The limitation period is 3 months from receipt of order (condonable by a further 3 months). FORM GST APL-05 is prescribed for appellants. The incremental pre-deposit is 20% of remaining disputed tax (aggregate cap: ₹50 crores CGST + ₹50 crores SGST). Unlike the First Appellate Authority, the Tribunal possesses plenary powers including remand for fresh adjudication—a significant jurisdictional distinction.

2.3 Appeal to High Court (Section 117)

Appeals to the High Court from Tribunal orders are entertainable only on substantial questions of law—a jurisdictional filter excluding pure questions of fact. The limitation is 180 days, with discretionary condonation available upon satisfaction of the Court. No monetary pre-deposit is statutorily mandated at this stage.

Table 2: Appellate Forum Comparison

| Forum | Section | Limitation | Pre-Deposit | Powers |

| Appellate Authority | 107 | 3 months (+1 month) | 100% admitted + 10% disputed (max ₹25 Cr) | Confirm, modify, annul. No remand. |

| Appellate Tribunal | 112 | 3 months (+3 months) | Additional 20% disputed (max ₹50 Cr) | Confirm, modify, annul, remand, rectify. |

| High Court | 117 | 180 days (discretionary condonation) | None statutory | Substantial questions of law only. |

3. Demand Mechanisms: Section 73 versus Section 74

The dichotomy between Sections 73 and 74 represents the foundational classification in GST demand proceedings, differentiated by the presence or absence of fraud, wilful misstatement, or suppression of facts with intent to evade tax.

3.1 Section 73: Non-Fraudulent Cases

Section 73 governs demands arising from bona fide errors—tax not paid, short paid, erroneously refunded, or ITC wrongly availed/utilised for reasons other than fraud. The limitation for issuing the demand order is 3 years from the due date of the annual return of the relevant financial year (33 months for SCN, 36 months for order). Graduated penalty mitigation is available: no penalty for payment before SCN, no penalty for payment within 30 days of SCN, and 10% penalty (minimum ₹10,000) for payment within 30 days of order.

3.2 Section 74: Fraudulent Cases

Section 74 invokes an extended limitation of 5 years (54 months for SCN, 60 months for order) where tax evasion is attributable to fraud, wilful misstatement, or suppression. The penalty structure is significantly stringent: 15% penalty for payment before SCN, 25% for payment within 30 days of SCN, and 50% upon order. The burden of establishing fraudulent intent lies with the department, invoking principles from the Collector of Central Excise v. Dhiren Chemical Industries line of jurisprudence.

Table 3: Section 73 vs Section 74 — Comparative Matrix

| Parameter | Section 73 (Non-Fraudulent) | Section 74 (Fraudulent) |

| Basis | Tax issues for reasons other than fraud/suppression | Fraud, wilful misstatement, or suppression |

| Limitation Period | 3 years (SCN: 33 months; Order: 36 months) | 5 years (SCN: 54 months; Order: 60 months) |

| Payment Before SCN | Tax + Interest only | Tax + Interest + 15% Penalty |

| Payment within 30 days of SCN | Tax + Interest (No Penalty) | Tax + Interest + 25% Penalty |

| Payment within 30 days of Order | Tax + Interest + 10% Penalty (min ₹10,000) | Tax + Interest + 50% Penalty |

| Relevant Forms | DRC-01 (SCN), DRC-07 (Order) | DRC-01 (SCN), DRC-07 (Order) |

4. Recovery Mechanisms under Section 79

Recovery proceedings under Section 79 are initiated when amounts determined under any order remain unpaid for 3 months from the date of service. Notably, self-assessed liabilities under GSTR-1 or GSTR-3B may be recovered directly without issuance of a Show Cause Notice—a significant departure from the general adjudicatory framework.

4.1 Modes of Recovery

The Act prescribes multiple recovery modalities, each with distinct procedural forms:

-

Deduction from money owed: FORM GST DRC-09 directs specified officers to deduct amounts from sums payable to the defaulter.

-

Sale of goods: Detention and auction of goods under departmental control via DRC-10 (Notice for Auction), culminating in DRC-12 (Sale Certificate).

-

Garnishee proceedings: Recovery from third parties (banks, debtors) through DRC-13, with DRC-14 issued upon remittance.

-

Land revenue arrears: Certificate in DRC-18 to Collector/Deputy Commissioner for coercive recovery as land revenue arrears.

-

Magisterial proceedings: Application in DRC-19 for recovery as if it were a fine imposed by a Magistrate.

4.2 Instalment Facility (Section 80)

Section 80 provides relief to defaulters demonstrating genuine hardship. Application for payment in instalments is made via FORM GST DRC-20, with the Commissioner's acceptance/rejection communicated through DRC-21. A critical condition: default in any single instalment renders the entire outstanding balance immediately payable, accelerating recovery proceedings.

Table 4: Recovery Forms and Mechanisms

| Recovery Mode | Form(s) | Mechanism |

| Deduction from money owed | DRC-09 | Directions to the specified officer to deduct from the amounts payable to defaulter |

| Sale of goods | DRC-10, DRC-12 | Detention and auction of goods; sale certificate issued upon disposal |

| Garnishee (Third Party) | DRC-13, DRC-14 | Notice to bank/debtor to remit sums held on behalf of the defaulter |

| Land Revenue Recovery | DRC-18 | Certificate to Collector for recovery as arrear of land revenue |

| Magisterial Proceedings | DRC-19 | Application for recovery as fine imposed by Magistrate |

| Instalment Payment | DRC-20, DRC-21 | Application for instalments; default accelerates full recovery |

5. Concluding Observations

The GST procedural framework represents a sophisticated adjudicatory mechanism balancing revenue protection with taxpayer rights. Practitioners must remain cognizant of the interplay between assessment categories, limitation periods, pre-deposit thresholds, and appellate remedies. Particular attention is warranted to the automatic withdrawal provisions under Section 62, the remand prohibition at the first appellate stage, and the direct recovery provisions for self-assessed liabilities—each representing significant departures from erstwhile indirect tax jurisprudence. Strategic deployment of these procedural tools can materially impact dispute resolution outcomes and client advisory efficacy.

Disclaimer: This article is intended for informational purposes and does not constitute legal advice.

Need for GST in India | Powers of GST Officers | UQC Code in GST | Cookies New GST Rate | GST Slab for Bakery Products

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified