Chapter 2 of the Central Goods and Services Tax Act, 2017 (CGST Act), titled "Administration," encompasses Sections 3 to 6. These sections establish the framework for the appointment, powers, and jurisdiction of tax officers, which is critical for the effective implementation and enforcement of the entire CGST Act and, by extension, the broader GST regime. This chapter lays the groundwork for subsequent operational aspects such as Levy and Collection, Input Tax Credit, and Demands and Recovery.

Section 3: Officers Under This Act

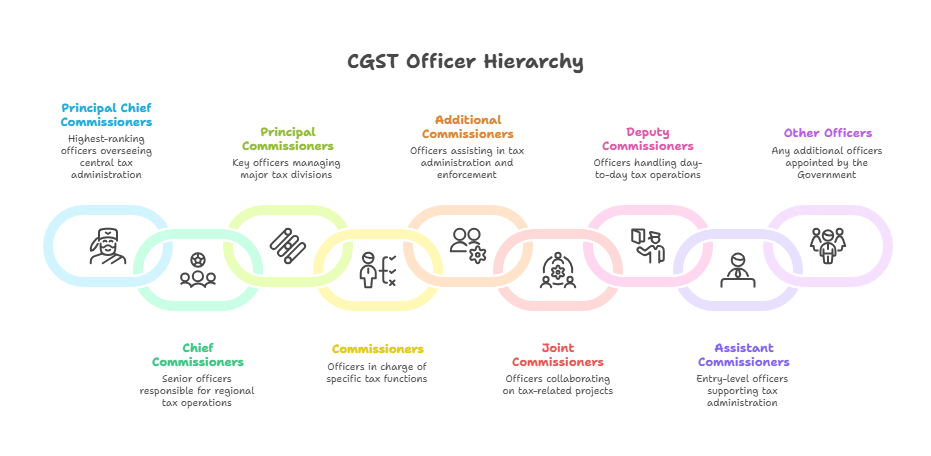

Section 3 outlines the classes of officers to be appointed by the Government via notification for the purposes of the CGST Act. These officers derive their power and authority from this section. The Government appoints the following ranks:

• Principal Chief Commissioners of Central Tax or Principal Directors General of Central Tax.

• Chief Commissioners of Central Tax or Directors General of Central Tax.

• Principal Commissioners of Central Tax or Principal Directors of Central Tax.

• Commissioners of Central Tax or Directors of Central Tax.

• Additional Commissioners of Central Tax or Additional Directors of Central Tax.

• Joint Commissioners of Central Tax or Joint Directors of Central Tax.

• Deputy Commissioners of Central Tax or Deputy Directors of Central Tax.

• Assistant Commissioners of Central Tax or Assistant Directors of Central Tax.

• Any other class of officers deemed fit by the Government.

A crucial provision is that officers appointed under the Central Excise Act, 1944, are deemed to be officers appointed under the CGST Act. Notifications are issued under this section, such as Notification No. 2/2017-Central Tax, dated 19.6.17, for the appointment of officers and their jurisdiction. Unlike exemption notifications, notifications issued under Section 3 for designating officers do not require to be laid before Parliament.

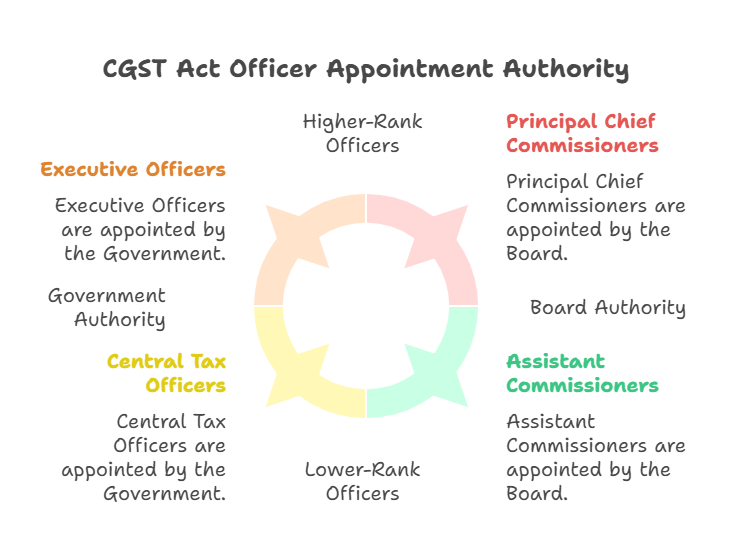

Section 4: Appointment of Officers

While the Government retains the power to appoint executive officers, Section 4 empowers the Board (Central Board of Indirect Taxes and Customs, formerly Central Board of Excise & Customs) to authorise any officer from the ranks of Principal Chief Commissioners to Assistant Commissioners to appoint officers of central tax below the rank of Assistant Commissioner for the administration of the Act. This provision ensures that administrative staff, who form the "field formations," can be appointed to assist executive officers in carrying out statutory functions.

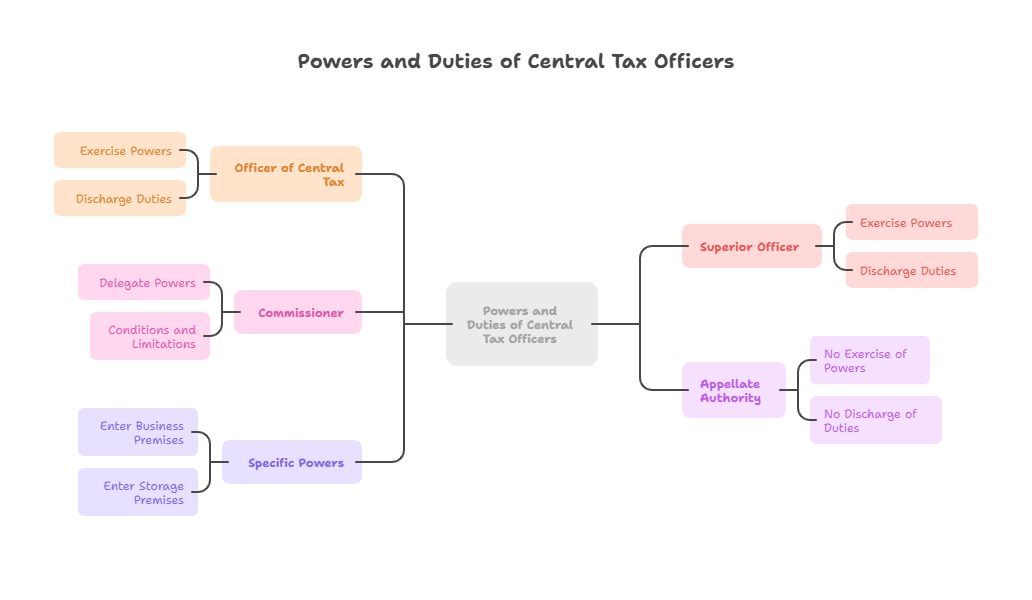

Section 5: Powers of Officers

Section 5 defines the powers and duties of central tax officers.

• An officer of central tax may exercise the powers and discharge the duties conferred or imposed on them, subject to conditions and limitations imposed by the Board.

• A superior officer of central tax may exercise the powers and discharge the duties conferred or imposed on any subordinate officer. However, this general rule does not hold good in all instances; specific notifications must be examined.

• The Commissioner can delegate his powers to any subordinate officer, subject to specified conditions and limitations.

• It is explicitly stated that an Appellate Authority shall not exercise the powers and discharge the duties conferred or imposed on any other officer of central tax.

• Officers of central tax have specific powers, such as the authority to enter any place of business or premises where goods or services are being supplied or stored.

Section 6: Authorisation of Officers of State Tax or Union Territory Tax as Proper Officer in Certain Circumstances

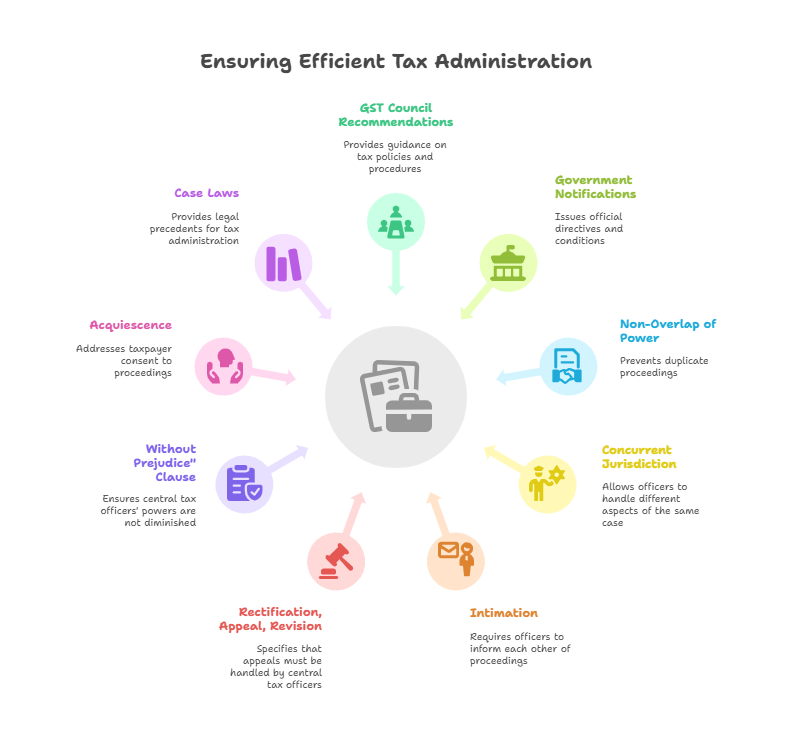

Section 6 is a key provision for avoiding duplication of tax administration in the GST regime. It allows officers appointed under the State Goods and Services Tax Act (SGST Act) or the Union Territory Goods and Services Tax Act (UTGST Act) to be authorised as proper officers for the purposes of the CGST Act. This authorisation is subject to:

• Recommendations of the GST Council.

• Conditions specified by the Government through notification.

Key aspects of this authorisation include:

• Non-overlap of Administrative Power: The intention is to enable a clear and unambiguous jurisdiction, preventing parallel proceedings over the same matter.

• Concurrent Jurisdiction: Officers of one department (e.g., State Tax) may undertake proceedings for certain aspects (e.g., audit under Section 65), while officers of the other department (e.g., Central Tax) may initiate proceedings for different aspects (e.g., inadmissible credits under Section 67) for the same taxpayer.

• Intimation: Where an officer under the CGST Act initiates proceedings, they are generally required to intimate the corresponding State/UT tax officer, and vice versa.

• Rectification, Appeal, and Revision: Any proceedings for rectification, appeal, or revision of an order passed by an officer appointed under the CGST Act shall not lie before an officer appointed under the SGST or UTGST Act.

• "Without prejudice" Clause: The provision opens with "Without prejudice to the provisions of this Act," meaning that the powers conferred on central tax officers are not derogated by this mutual allocation.

• Acquiescence: The sources caution that if a person submits to proceedings initiated by an officer, even if there was a lack of authority, and encourages Revenue to proceed, they might be treated as having "acquiesced" and could be barred from objecting later. However, High Courts, like in Juhi Industries (P) Ltd. v. State of JH & Ors., have quashed notices even after taxpayer acquiescence, emphasizing that courts can "mould relief" to avoid subversion of justice.

• Case Laws: The principle that officers appointed under State GST are also proper officers for the IGST Act (and by extension, CGST Act for mutual authorisation) has been affirmed in cases like Advantage India Logistics Pvt. Ltd. V. Union of India. Another case, G.K. Trading Company V. Union of India, clarified that Section 6(2) does not bar an officer from invoking power under Section 70 unless a proceeding on the same subject matter has already been initiated by a proper officer.

This administrative structure is designed to ensure efficient and coordinated tax collection across India's federal system, with clear lines of authority and mechanisms for inter-departmental cooperation.

Need for GST in India | Powers of GST Officers | UQC Code in GST | Cookies New GST Rate | GST Slab for Bakery Products

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified