A CFO's Strategic Guide to GST Annual Return and Reconciliation: Preparing Your Finance Team for Success

As we approach the GST Annual Return filing season, CFOs and Finance Directors across India face a critical challenge: ensuring their teams are well-prepared to navigate the complex requirements of Form GSTR-9 and Form GSTR-9C. With the December 31st deadline looming for each financial year's returns, strategic preparation becomes essential for compliance and operational efficiency.

Understanding the Compliance Landscape

The GST framework requires annual returns and reconciliation statements for each financial year from April to March. While the government has provided relief to smaller businesses by exempting taxpayers with turnover up to Rs. 2 crore from filing Form GSTR-9 and removing the GST Reconciliation requirement (Form GSTR-9C), larger organisations must still ensure comprehensive compliance. This creates an opportunity for finance leaders to streamline processes and strengthen their compliance infrastructure.

Building Your Team's Foundation: Purchase, Sales, and ITC Documentation

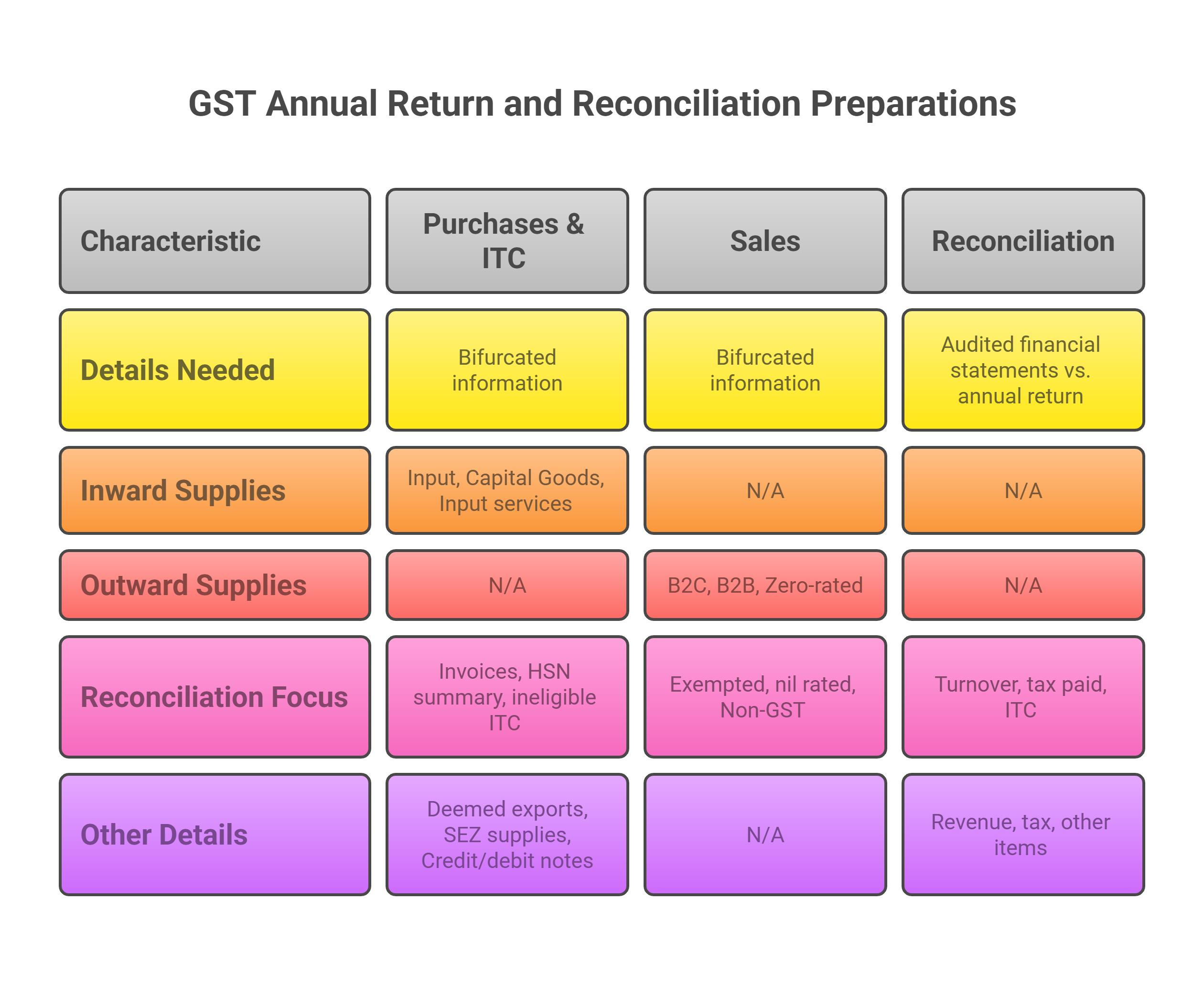

The cornerstone of successful GST annual return preparation lies in maintaining detailed breakdowns of purchases, sales, and Input Tax Credit (ITC). Your finance team needs to understand that the annual return requires granular classification that goes beyond standard accounting practices.

For purchases and ITC, the team must segregate inward supplies into distinct categories based on whether they're from registered or unregistered persons, whether they attract reverse charge, and whether they constitute inputs, capital goods, or input services. Import transactions require separate classification, and HSN-wise summaries become crucial for accurate reporting. This level of detail demands that your team maintains comprehensive records throughout the year rather than attempting year-end compilation.

On the sales side, the classification requirements distinguish between B2C transactions with unregistered persons, B2B supplies to registered entities, and zero-rated exports. Additionally, supplies that don't attract tax—including exempted, nil-rated, and non-GST supplies—require separate tracking. Special categories like deemed exports, SEZ supplies, and credit or debit notes for B2B transactions need dedicated attention in your reporting framework.

Mastering the Art of Reconciliation: From Financial Statements to GST Returns

One of the most significant challenges associated with Goods and Services Tax (GST) compliance is reconciling audited financial statements with GST returns. This complexity arises from a fundamental discrepancy: whereas financial statements are generally prepared at a pan-India level, presenting aggregated figures, GST returns necessitate a GSTIN-specific breakdown for each state in which the organisation operates.

Finance leaders should instruct their teams to maintain state-wise breakups from the beginning of the financial year. This proactive approach prevents the year-end scramble and ensures accuracy in reconciliation. The reconciliation process involves multiple layers: matching invoice values with book entries, aligning book values with GSTR-3B declarations, ensuring consistency between books and GSTR-1, and verifying that GSTR-3B and GSTR-1 align properly.

Several prevalent discrepancies emerge during turnover reconciliation that your team should foresee. Inter-state stock transfers, although not classified as sales in accounting terminology, are regarded as outward supplies under the Goods and Services Tax (GST). Employee recoveries, complimentary samples subjected to GST charges (;or reversal of sample-specific ITC), and vendor penalties all contribute to variances between accounting records and GST reporting. Comprehending these disparities enables your team to prepare more precise reconciliations and detect potential compliance gaps at an early stage.

Navigating Input Tax Credit Reconciliation

The reconciliation of Input Tax Credit (ITC) represents one of the most intricate domains of Goods and Services Tax (GST) compliance, necessitating meticulous attention to detail and a thorough understanding of GST regulations. It is imperative that your finance team ensures that ITC claims are substantiated by valid documentation, which includes tax invoices, bills of entry, debit notes, self-invoices, and Input Service Distributor (ISD) invoices.

Critical compliance points include verifying that ITC isn't claimed on restricted items, ensuring proper reversal for capital goods sales, monitoring the 180-day payment rule for job work supplies, and maintaining proper bifurcation between eligible and ineligible credits. The depreciation-ITC restriction requires particular attention, as businesses cannot claim both benefits simultaneously.

It is imperative to conduct regular reconciliation between GSTR-3B and GSTR-2A to ensure compliance with Input Tax Credit (ITC) regulations. To optimize this process, it is recommended that your team establish a systematic monthly reconciliation protocol, rather than postponing these activities until the end of the fiscal year. This proactive approach will facilitate the prompt identification and rectification of any discrepancies, thereby enhancing overall compliance and financial accuracy.

Understanding Complex Reconciliation Items

Several transactions require special attention due to differences between accounting treatment and GST requirements. Supplies without consideration, covered under Schedule 1 of the CGST Act, attract GST despite having no accounting revenue recognition under Ind AS-115. Agent-principal transactions create another complexity where the agent's books show only commission income, but GST turnover includes the full transaction value.

Post-sales discounts pose reconciliation challenges, as financial credit notes do not diminish GST turnover, despite being documented as discounts in financial statements. Government grants, although acknowledged as revenue pursuant to accounting standards, do not qualify as GST revenue when supplied by central or state governments. These intricate distinctions necessitate that your team maintains comprehensive reconciliation worksheets throughout the year.

Ensuring Robust Documentation and Record-Keeping

Effective GST compliance demands comprehensive documentation practices. Your organization must maintain books of accounts as specified under Section 35 of the GST Act, with separate records for each place of business. This includes maintaining copies of all agreements, registration-wise audited financial statements, and specialized registers for e-way bills, delivery challans, and various ITC forms.

The documentation requirements extend to maintaining separate cash and bank registers for each entity, ensuring proper recording of all transactions. Transporters and warehouse keepers within your supply chain also need appropriate record-keeping systems to support your compliance efforts.

Strategic Recommendations for Finance Leaders

As you prepare your teams for the upcoming filing season, consider implementing these strategic initiatives. First, establish monthly reconciliation protocols rather than relying on year-end exercises. This approach identifies issues early and prevents last-minute compliance rushes. Second, invest in training programs that help your team understand the nuances between accounting and GST treatments. This knowledge becomes crucial for accurate reporting and reconciliation.

Third, develop standardised templates and checklists that guide your team through the complex requirements of GSTR-9 and GSTR-9C preparation. These tools ensure consistency and completeness in your compliance efforts. Finally, consider implementing technology solutions that automate data capture and reconciliation processes, reducing manual errors and improving efficiency.

Conclusion: Transforming Compliance into Competitive Advantage

While GST annual return and reconciliation requirements present significant challenges, they also offer opportunities for finance leaders to strengthen their organizations' compliance infrastructure. By taking a proactive, strategic approach to preparation, CFOs and Finance Directors can transform what might seem like a compliance burden into a competitive advantage through improved financial visibility and control.

The key lies in commencing preparations early, diligently maintaining comprehensive records throughout the year, and ensuring that your team comprehends both the technical requirements and the strategic significance of precise GST compliance. With appropriate preparation and a conducive mindset, your organisation can effectively manoeuvre through the GST annual return season while simultaneously enhancing its financial management capabilities for the future.

Remember, the December 31st deadline approaches faster than anticipated. Begin your preparation now, empower your teams with the knowledge and tools they need, and establish GST compliance as a cornerstone of your organisation's financial excellence.

FAQs on GST Annual Return & Reconciliation

1) What is the due date for filing the GST Annual Return (GSTR-9)?

The due date is usually 31 December following the end of the financial year. Always confirm with the latest CBIC notification.

2) Who needs to file GSTR-9 and who is exempt?

Taxpayers with turnover above ₹2 crore must file GSTR-9. Exemptions apply for smaller taxpayers based on government notifications.

3) When is GSTR-9C required?

Generally, businesses with turnover over ₹5 crore must file GSTR-9C. The requirement may vary depending on the FY.

4) What documents are required for annual reconciliation?

Audited financial statements, GST returns (GSTR-1, GSTR-3B, GSTR-2A/2B), purchase/sales registers, HSN summaries, e-way bills, and ITC workings.

5) How should ITC mismatches be handled?

Run monthly 3B vs 2A/2B reconciliations, follow up with vendors, pass reversals if required, and take re-credit once eligible.

GST Audit Procedure | GST Audit Process | Notice for Conducting Audit u/s 65(3) (GST ADT-01) | Table 5 of GSTR 3B | GST Audit Checklist | GST Audit Checklist in Excel

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified