Procedures for Conducting the Audit

The conduct of a GST audit involves a structured series of steps to ensure thoroughness and fairness:

Planning and Objectives: Defining clear audit objectives, scope, and criteria, while identifying key stakeholders and potential risks.

Data Collection and Understanding: Gathering all relevant data, documents, records, and information to develop a comprehensive understanding of the audited processes and operations.

Risk Assessment and Testing: Identifying and assessing potential risks to compliance, followed by testing controls, transactions, or samples to verify accuracy.

Analysis and Conclusions: Analyzing collected data to draw conclusions and pinpoint areas of concern.

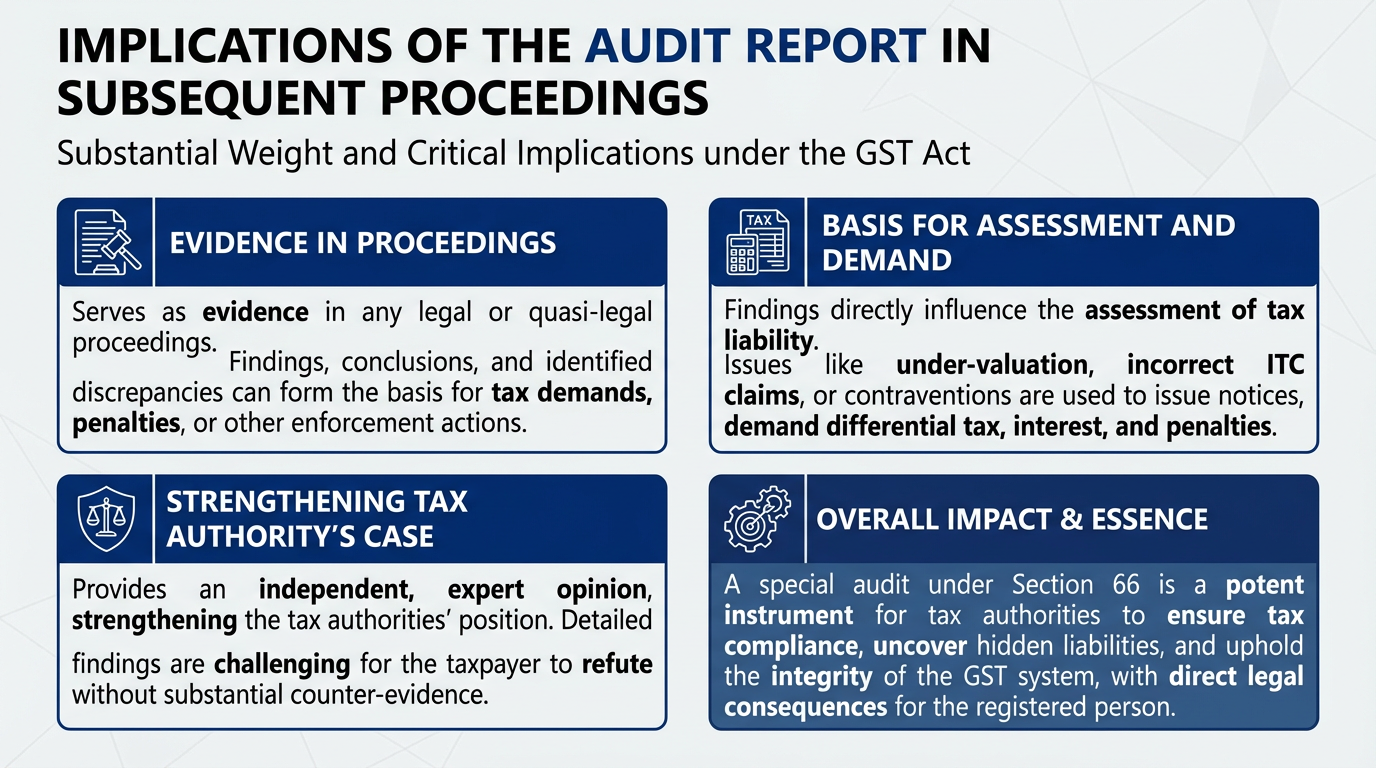

Reporting: Preparing a detailed audit report that outlines findings, supporting evidence, conclusions, and recommendations.

Communication: Discussing audit results with relevant stakeholders to ensure transparency and facilitate corrective actions.

Follow-up: Monitoring the implementation of audit recommendations and tracking progress.

Closing: Finalizing the audit process, archiving documents, and assessing overall audit effectiveness.