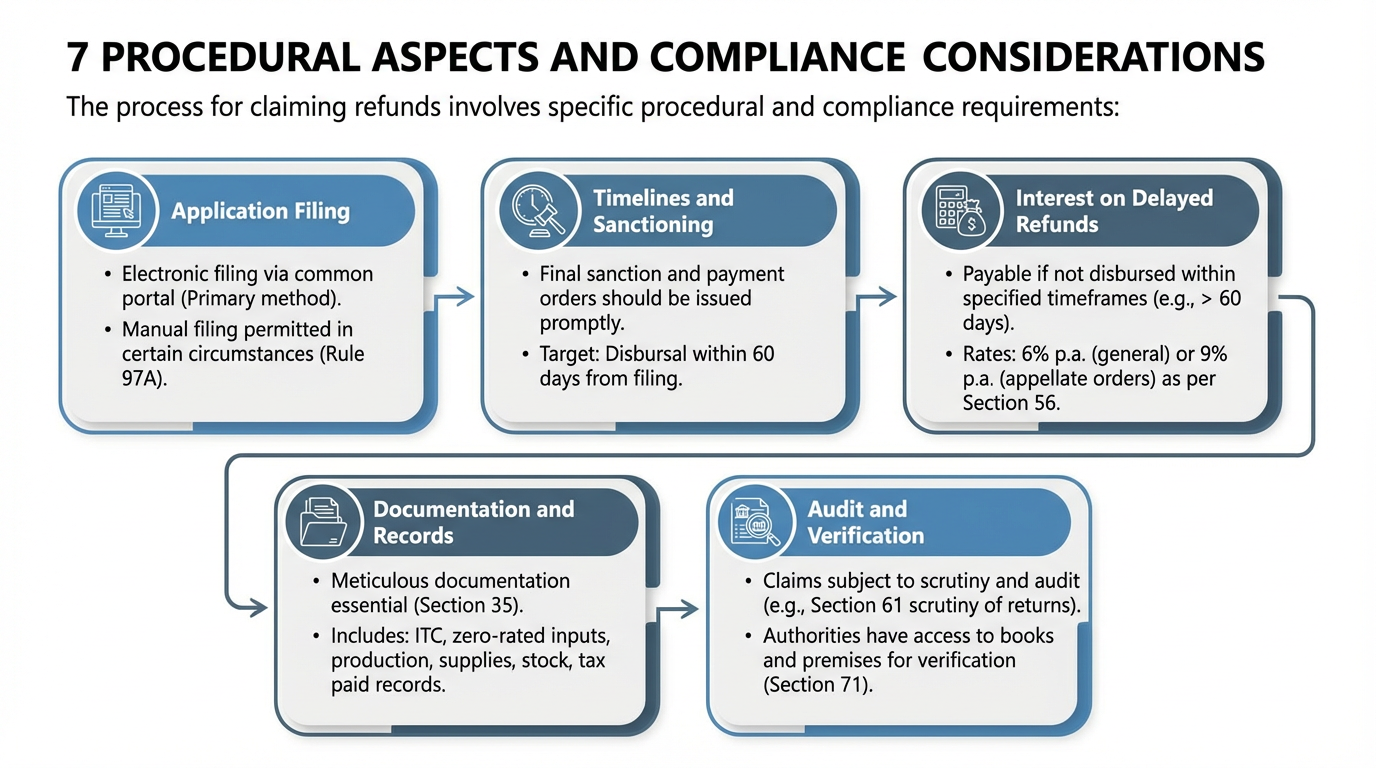

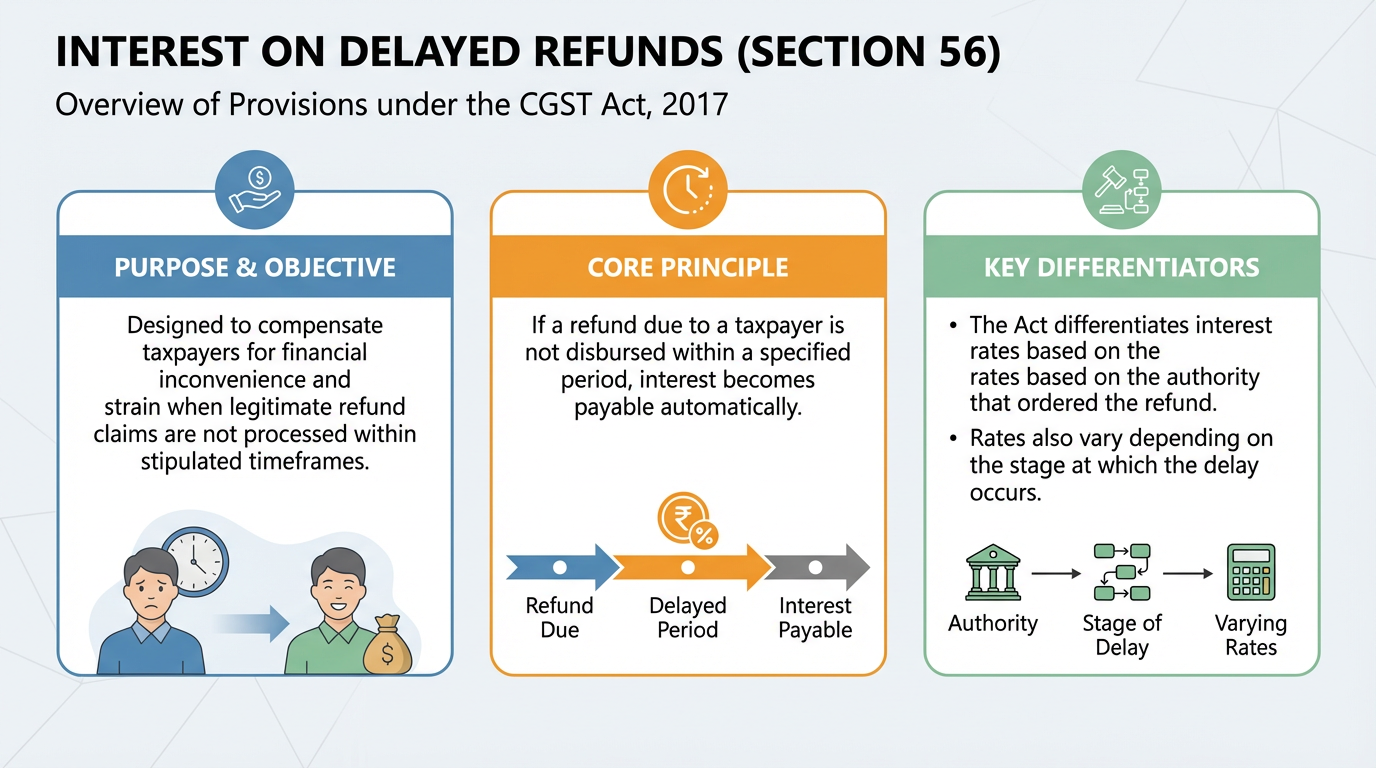

Interest on Delayed Refunds

Section 56 of the CGST Act addresses the payment of interest on delayed refunds:

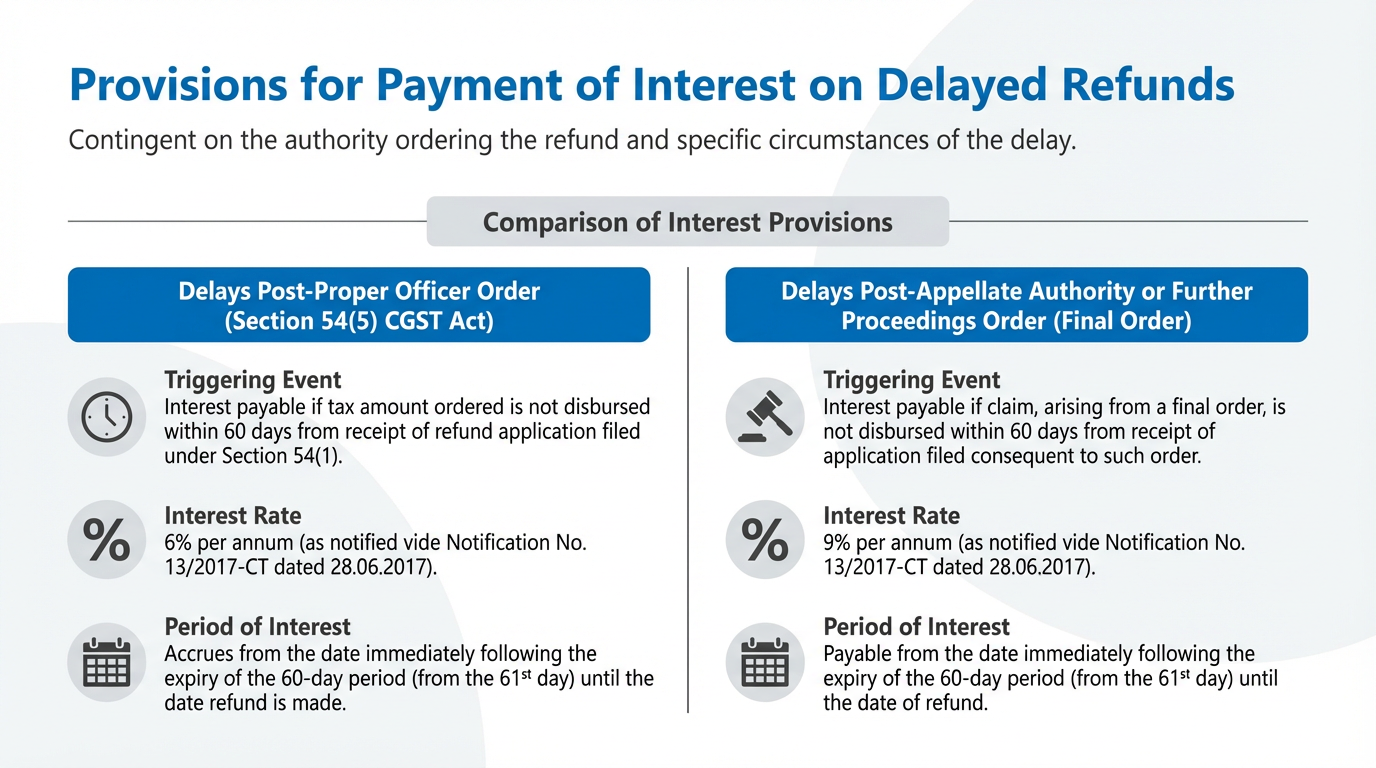

Refunds ordered by Proper Officer: If a tax refund ordered by the Proper Officer under Section 54(5) is not disbursed within 60 days from the application receipt date (under Section 54(1)), interest is payable to the applicant. The interest rate, notified by the Government (e.g., per annum), accrues from the day immediately following the -day period until the refund date.

Refunds from Appellate Orders: If a refund claim arises from a final order by an Adjudicating Authority, Appellate Authority, Appellate Tribunal, or Court, and the refund is not disbursed within days of receiving the application consequent to such order, interest is payable. The interest rate for these cases is also notified (e.g., per annum).

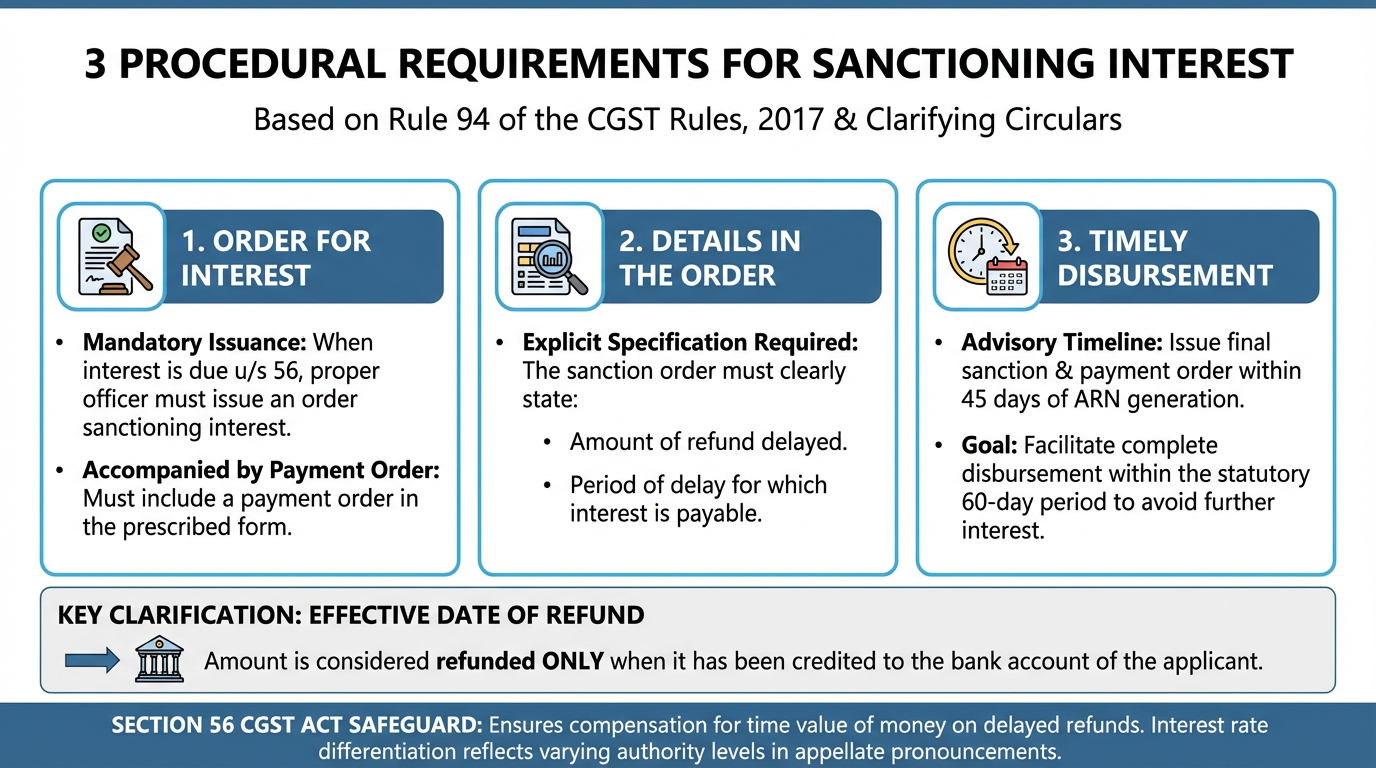

Sanctioning Interest: The Proper Officer must issue an order sanctioning the interest due under Section 56, detailing the delayed refund amount, delay period, and payable interest.

Timely Disbursement: To prevent interest accrual, tax authorities are advised to issue final sanction and payment orders within days of the Application Reference Number (ARN) generation, ensuring disbursement within the -day limit.