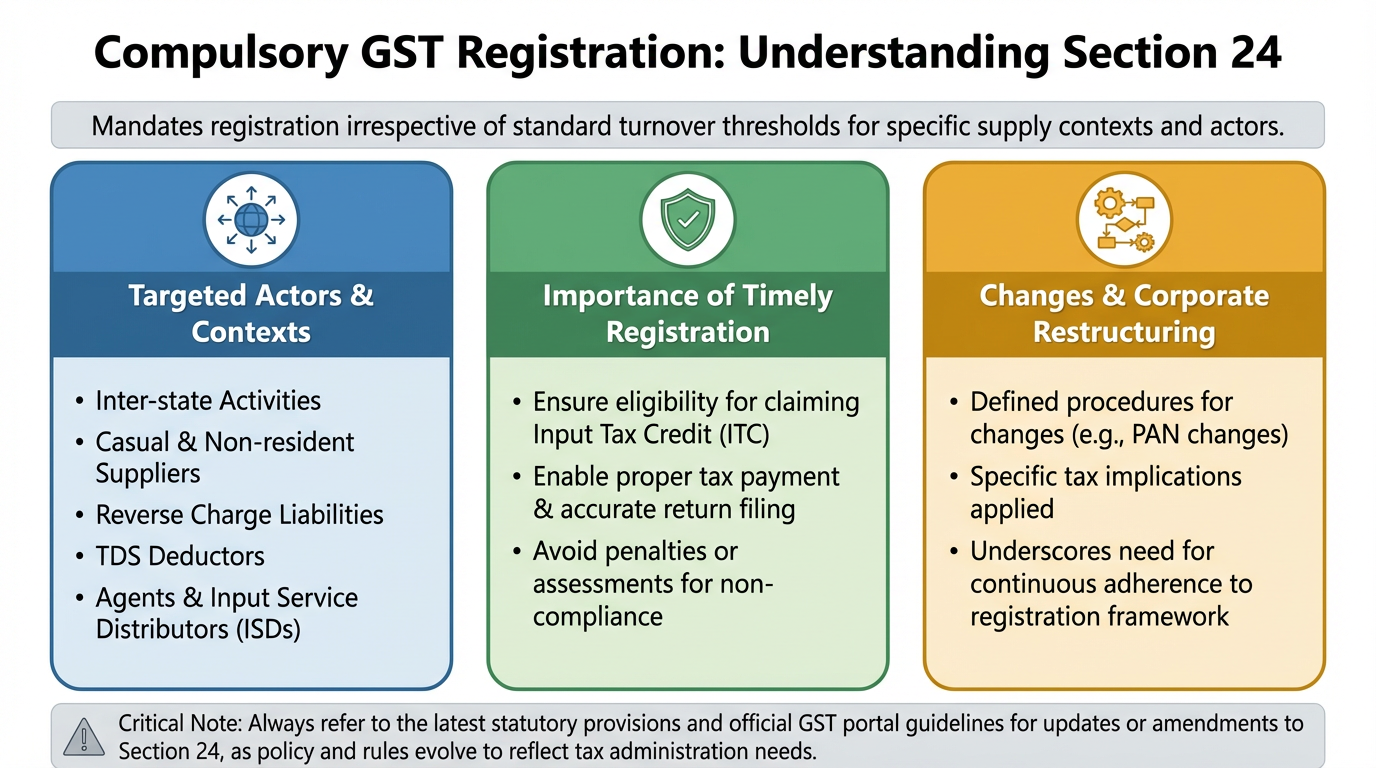

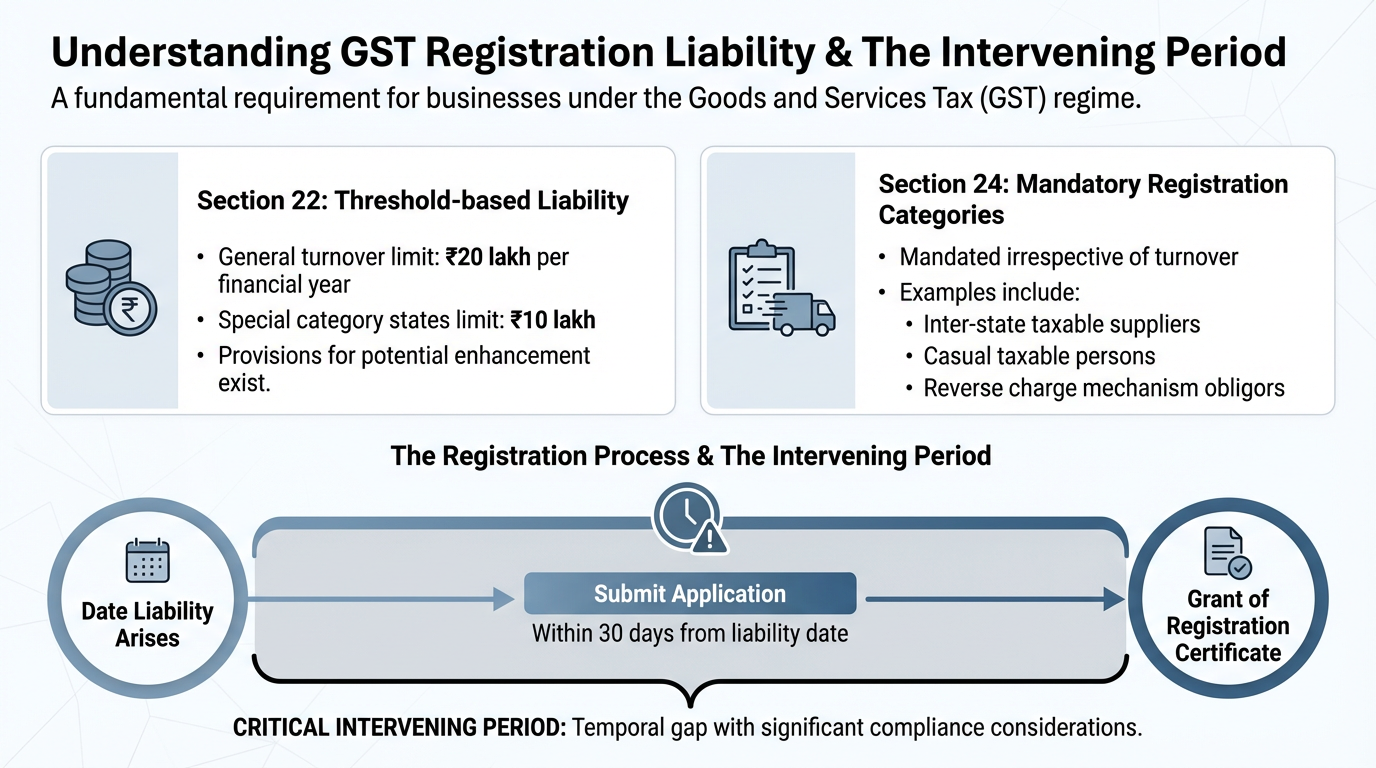

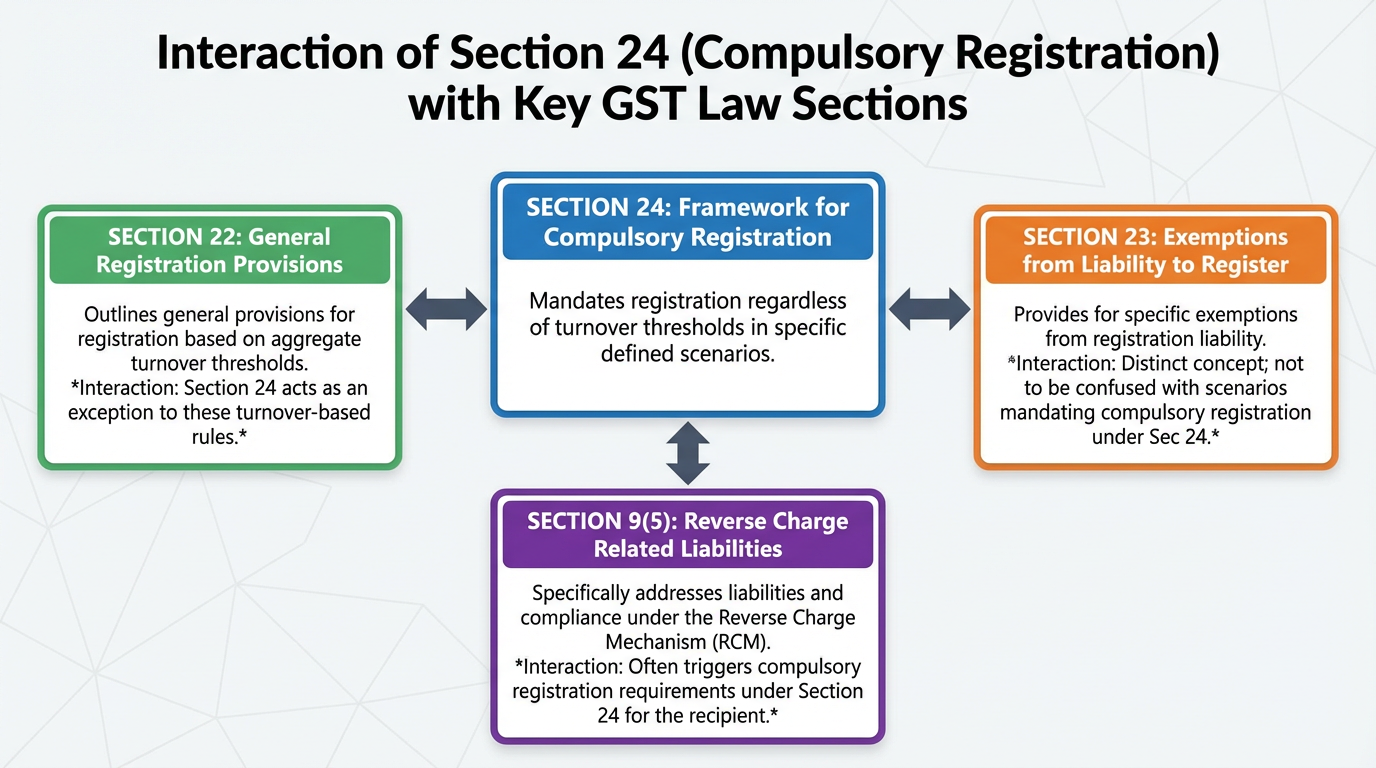

Introduction to Compulsory Registration

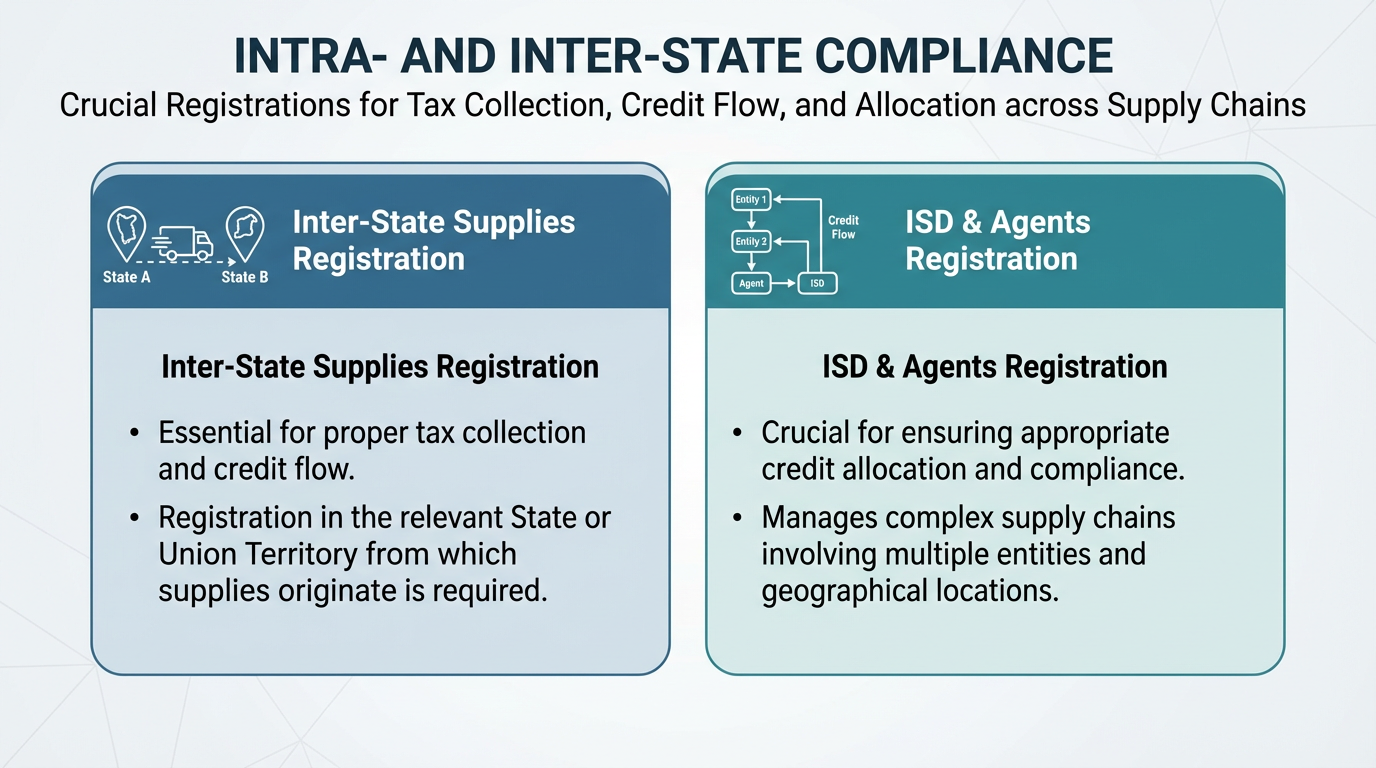

Under the Goods and Services Tax (GST) law, registration is a fundamental legal requirement for specific individuals and entities under particular circumstances. While many businesses register based on turnover thresholds as outlined in Section 22, Section 24 delineates scenarios where registration becomes compulsory, irrespective of the aggregate turnover. This provision ensures that certain activities and roles, deemed critical for effective tax administration, are brought within the GST framework from their inception. The scope of compulsory registration extends to inter-state taxable supplies, casual taxable persons, liabilities under the Reverse Charge Mechanism (RCM), non-resident taxable persons, and other related roles such as tax deductors and agents. This section consolidates these mandatory registration circumstances and explores their practical implications for taxpayers.