Key Provisions Governing Registration

Aggregate Turnover Thresholds

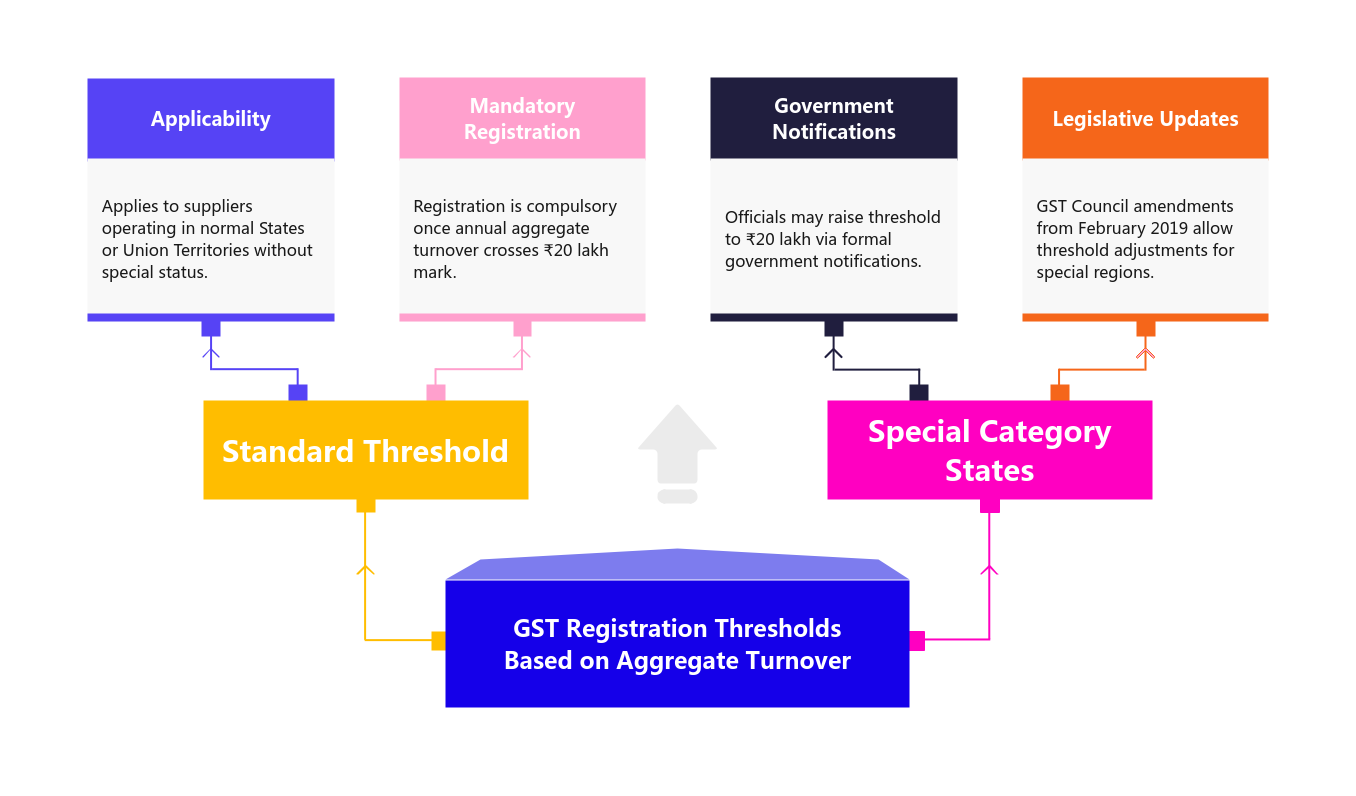

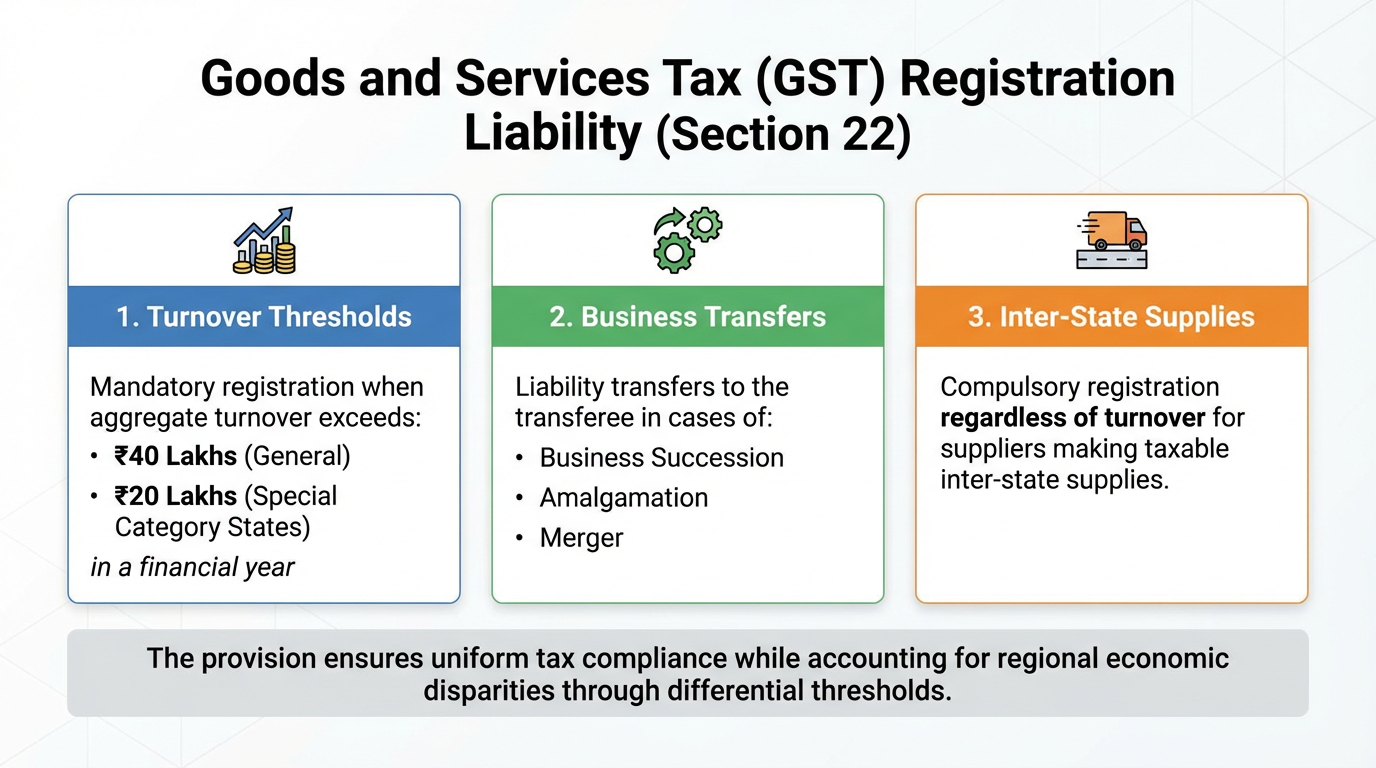

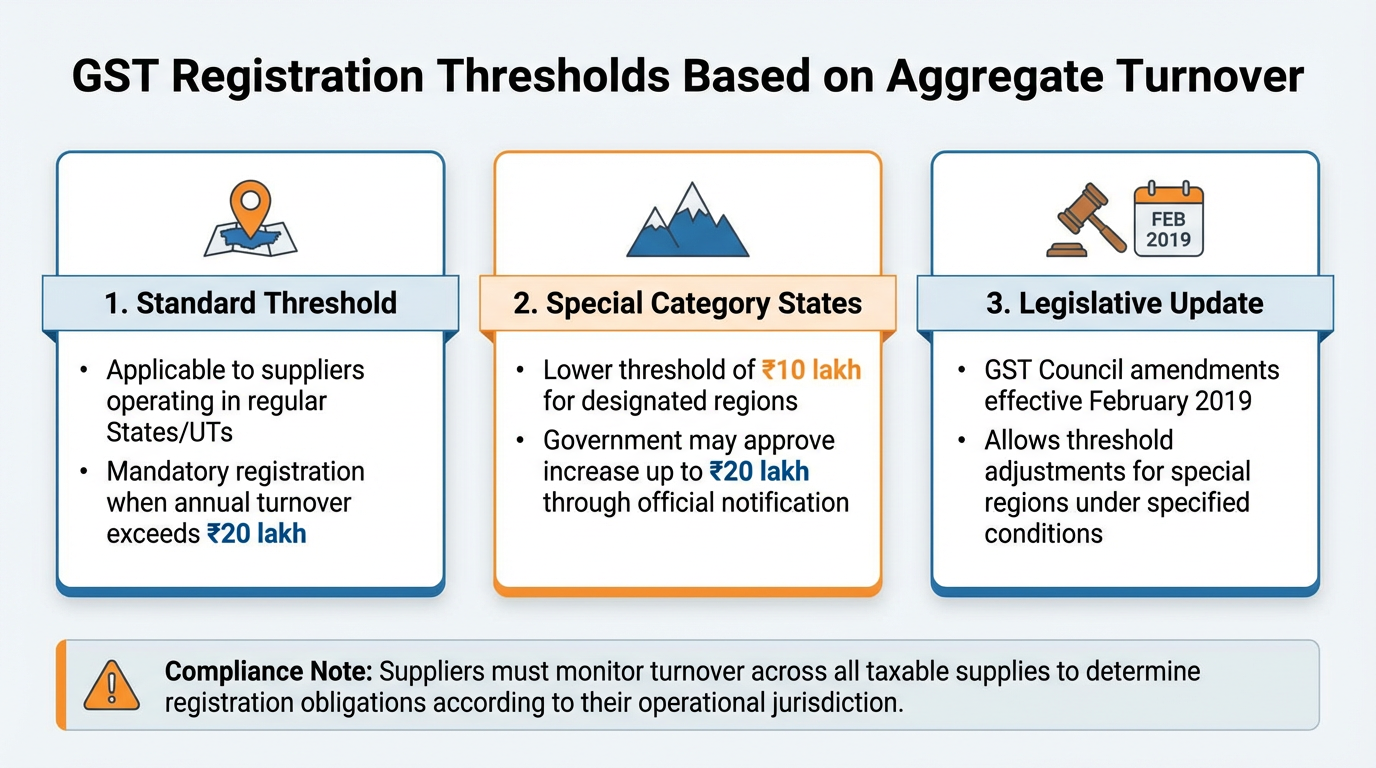

The primary determinant for GST registration liability is the aggregate turnover of a supplier in a financial year.

General Rule: Every supplier is liable to be registered in the State or Union Territory (excluding special category States) from which they make a taxable supply of goods or services, or both, if their aggregate turnover in a financial year exceeds .

Special Category States: For suppliers making taxable supplies from any designated special category State, the aggregate turnover threshold for registration is .

Government Discretion: The Government, upon the recommendation of the GST Council and at the request of a special category State, may enhance this threshold to an amount not exceeding , subject to specified conditions and limitations. This amendment was introduced by the CCST (Amendment) Act, 2018, effective from February 1, 2019.

Learning Takeaway: For non-special category States, registration is mandated if annual aggregate turnover exceeds . For special category States, the threshold is , with potential for enhancement up to via government notification.