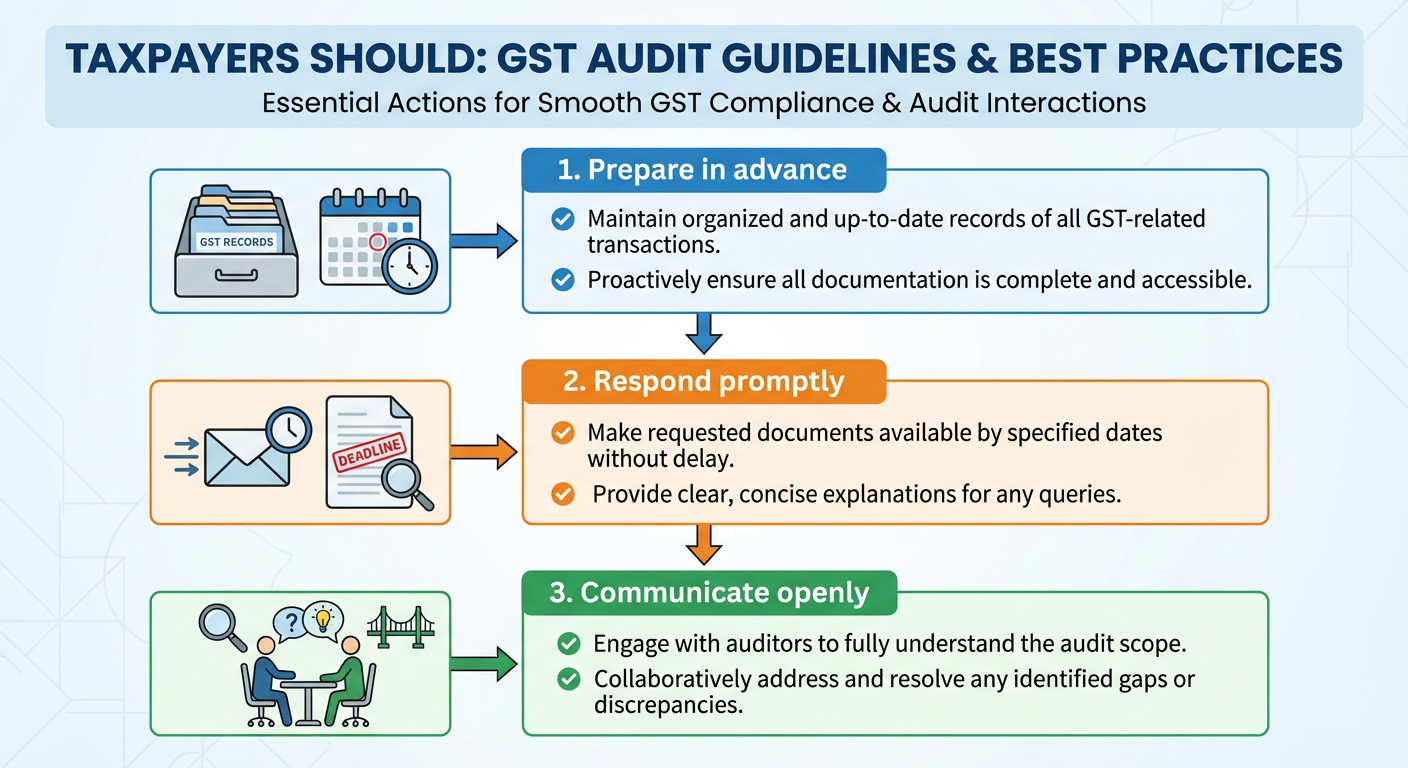

Process for Addressing Discrepancies

When a return is selected for scrutiny, the proper officer conducts a detailed examination to verify the accuracy and completeness of the taxpayer’s information. If discrepancies are identified, a specific procedure is followed:

Issuance of Notice: The proper officer issues a notice to the registered person, detailing the identified discrepancies and requesting an explanation or clarification.

Taxpayer’s Response: The registered person is given an opportunity to respond to the notice, providing a satisfactory explanation or necessary documentation to resolve the discrepancies within a specified timeframe.

Verification and Decision: The proper officer reviews the taxpayer’s response and supporting documents. If the explanation is satisfactory and discrepancies are resolved, the scrutiny for that issue may conclude. If the explanation is unsatisfactory, or if no response is received within the prescribed time, further action may be taken.

Further Action: Unresolved discrepancies can lead to additional proceedings under the GST Act. This may include:

Requesting additional information or documents.

Conducting further verification or inspection, as permitted by Section 71 for access to business premises.

Initiating assessment proceedings under Section 62 (for non-filers) or Section 63 (for unregistered but liable persons).

Ordering a special audit under Section 66 if there is reason to believe that declared values are incorrect or availed credit is outside normal limits.

The overarching goal of Section 61 is to foster voluntary compliance by allowing taxpayers to correct errors identified during scrutiny, thereby maintaining the integrity of the tax system.