Valuation Between Related Parties Under GST

The Problem Hidden in Plain Sight

Every month, hundreds of transactions flow quietly between branches, subsidiaries, holding companies, and affiliates. No arm-twisting. No open-market negotiation. Just an inter-company invoice, sometimes for a token amount, sometimes for nothing at all.

This is where GST auditors look first.

Related-party transactions are structurally designed to serve group interests rather than reflect commercial reality. And the GST law knows this. That is precisely why the statute strips these transactions of their 'transaction value' protection and subjects them to a separate, far more rigorous valuation architecture.

If your business has branches across states, a holding-subsidiary structure, or even an employer-employee relationship involving perquisites, you are already a party to related-party supplies. The question is not whether GST applies. The question is whether you have valued and discharged it correctly.

1. Who Qualifies as a 'Related Person' Under GST?

The starting point is a definition. The GST law has cast a wide net under the Explanation to Section 15 of the CGST Act, 2017. Persons are deemed 'related' if any of the following conditions are satisfied:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Beyond 'related persons', the law separately treats 'distinct persons' with different GST registrations of the same legal entity (e.g., a head office in Maharashtra and a branch in Tamil Nadu). Supplies between them are treated on par with related-party supplies.

Schedule I of the CGST Act mandates that supplies between related persons or distinct persons are taxable even if they are made without any consideration, provided the supply is in the course or furtherance of business.

This is the first shock for many CFOs: a free internal service or a stock transfer at cost between branches is a taxable supply under GST. Silence on the books does not mean silence in the law.

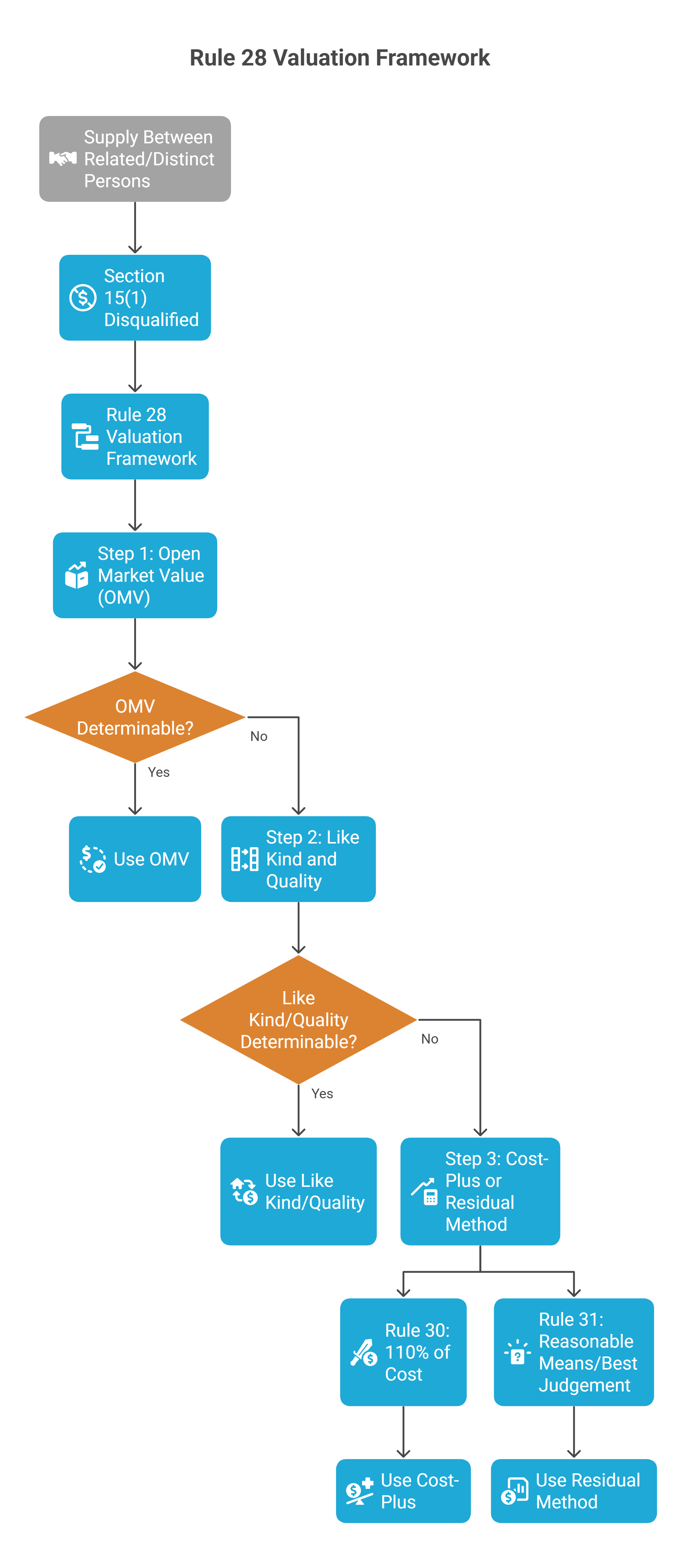

2. The Rule 28 Valuation Framework: A Sequential Test

Once a supply is identified as being between related or distinct persons, Section 15(1) of the CGST Act is knocked out. The transaction value, the price actually paid, is disqualified. The valuation must now follow Rule 28 of the CGST Rules, 2017, which prescribes a strict hierarchical method.

Step 1 Open Market Value (OMV)

The primary benchmark. OMV is defined as the full amount a buyer would pay to purchase an identical or similar supply from an unrelated supplier in similar circumstances.

This is the cleanest yardstick but also the most contested. What is the open market value of an internal IT support service? Or a centralised treasury function? This is where disputes are born.

Step 2: Like Kind and Quality

If the OMV cannot be determined, the value of goods or services of like kind and quality supplied at or about the same time to an unrelated buyer is used as the benchmark.

Step 3: Cost-Plus or Residual Method

-

Rule 30: 110% of the cost of production or provision of service.

-

Rule 31: Reasonable means / best judgement is the residual fallback.

Practical Note:

In litigation, the 'OMV' step is the most contested battleground. Taxpayers must maintain contemporaneous documentation showing how OMV was determined or demonstrate why it was not available before jumping to Rule 30 or 31. A bald assertion of 'cost plus' without exhausting prior steps has been consistently rejected in audit proceedings.

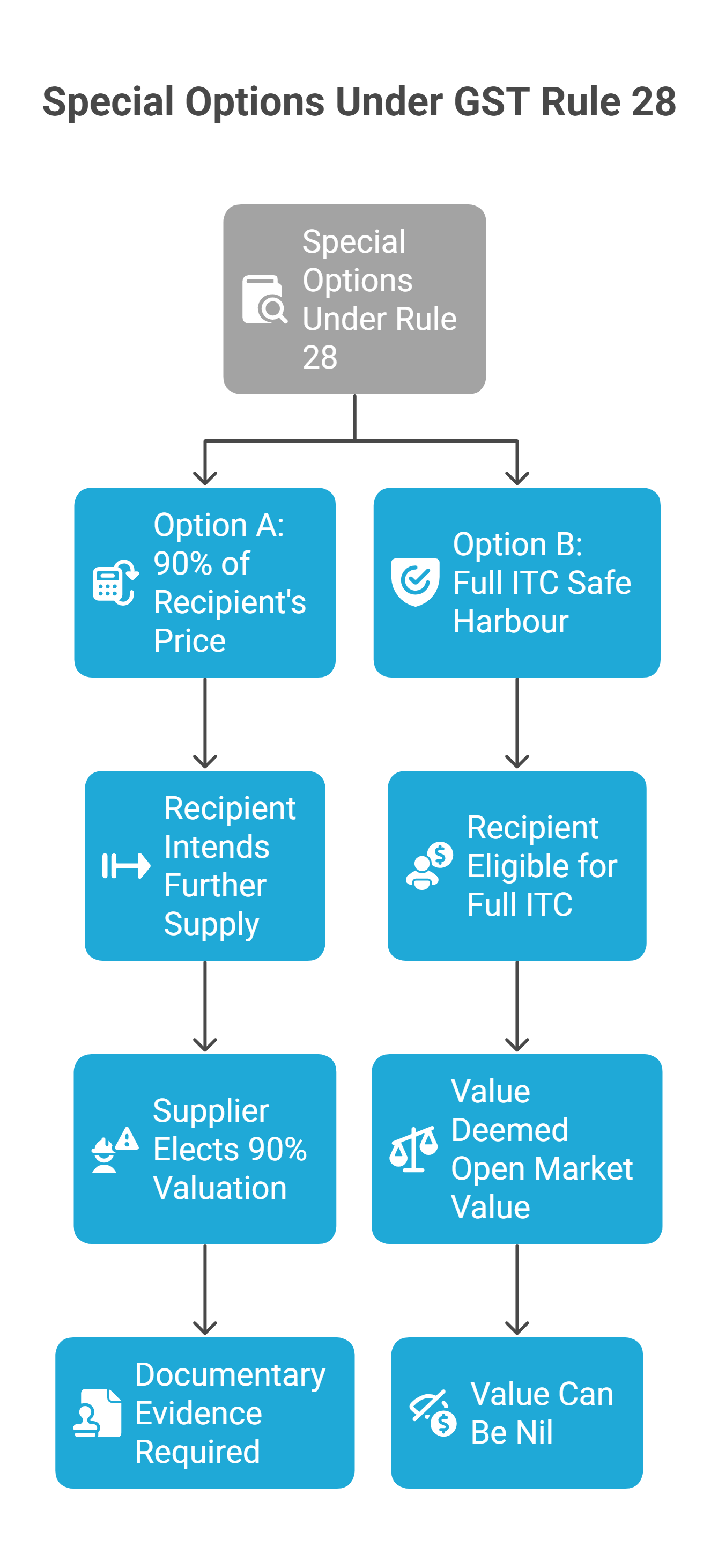

Special Options Under Rule 28

Option A: The '90% of Recipient's Price' Rule (Further Supply)

Where the related recipient intends to supply the goods further, as such, to an unrelated customer, the supplier may elect to value the goods at 90% of the price eventually charged by the recipient.

This is a useful concession for distribution chains within a group but it requires documentary evidence of the onward supply price and a specific election by the supplier.

Option B: The 'Full ITC Safe Harbour' (Second Proviso to Rule 28)

This is the most commercially significant provision in the entire related-party valuation framework.

If the recipient is eligible for full Input Tax Credit (ITC) under GST, the value declared in the invoice shall be deemed to be the open market value even if that value is nil.

CBIC Circular 199/11/2023-GST has further clarified that where a Head Office provides internally generated services to a Branch Office and full ITC is available at the Branch, the HO may issue a Nil-value invoice, and it will be legally accepted as the OMV. The tax officer cannot challenge it.

Critical caveat: 'Eligible for full ITC' is not the same as 'claims full ITC'. The recipient must be entitled to claim full ITC without any restriction under Sections 17(1), 17(2), or 17(5). If even a portion of ITC is blocked, the safe harbour collapses.

3. Corporate Guarantees: Rule 28(2) and the 1% Deeming Fiction

Corporate guarantees where a holding company furnishes a guarantee to a bank for credit availed by its subsidiary attracted enormous controversy in the GST era. The law has now been amended with the insertion of Rule 28(2).

|

|

|

|

|

|

|

|

1% of the amount of guarantee offered per annum OR actual consideration, whichever is higher |

|

|

|

|

|

|

The 1% deeming provision under Rule 28(2) operates independent of whether any consideration is actually paid. Even a 'free' guarantee is a taxable supply valued at a minimum of 1% of the guarantee amount per annum. Failure to discharge the applicable tax liability may also expose businesses to GST penalties and interest implications.

This is a significant compliance point for holding companies and group structures. Many corporate guarantees were being issued without any GST discharge, treating the transaction as either not a supply or as a financial service outside GST. Rule 28(2) has put paid to that position.

Action Point: Review all outstanding corporate guarantees. Compute the GST liability on 1% per annum. Ensure invoices have been issued and GST discharged or, where full ITC is available to the recipient, ensure the safe harbour documentation is in order.

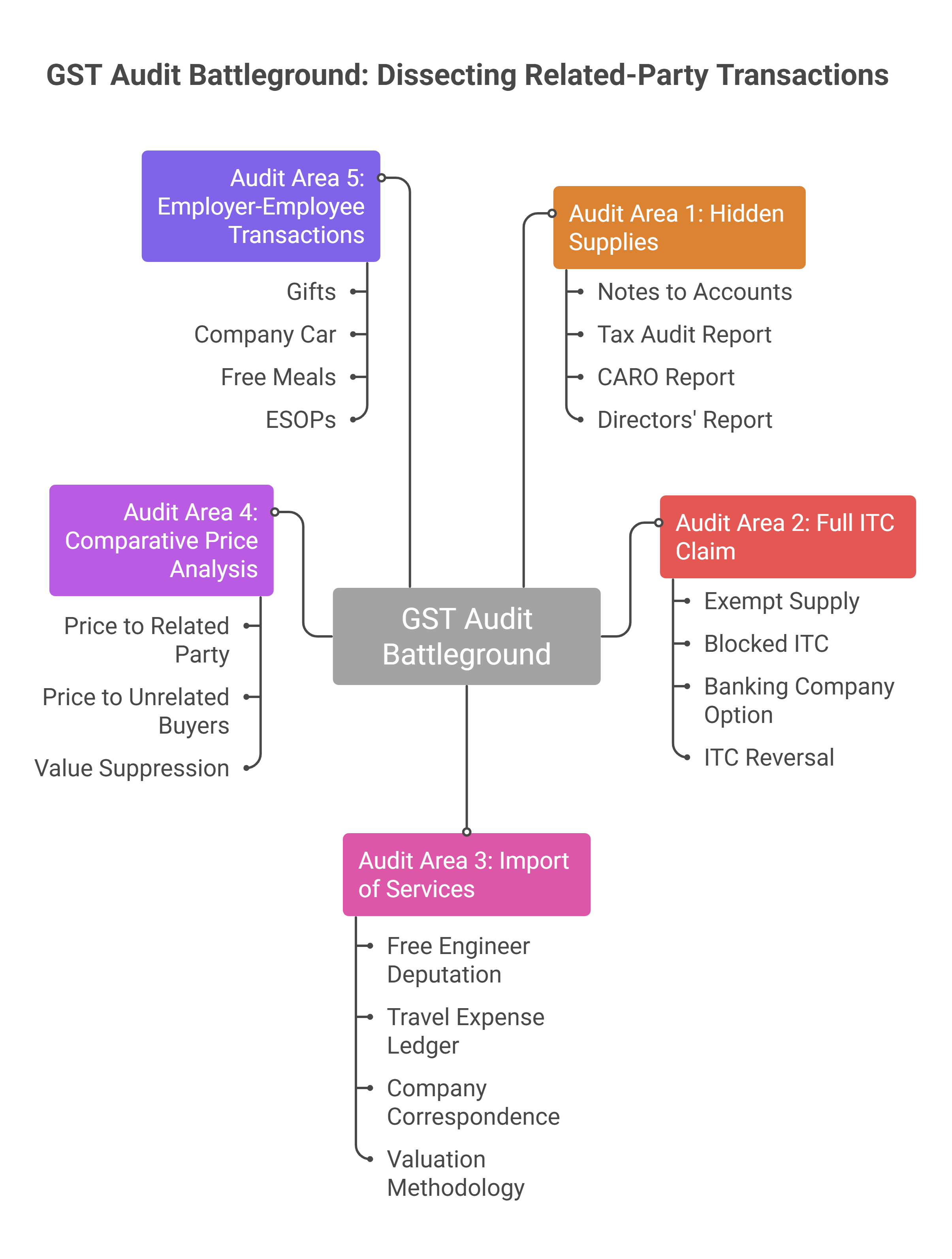

4. The GST Audit Battleground: How Officers Dissect Related-Party Transactions

The GST Audit Manual issued by the All India GST Audit Division categorises related-party transactions as 'high risk'. Businesses undergoing departmental scrutiny should understand the broader GST audit process and valuation checks applicable to related-party transactions.

Here is what the manual directs auditors to do and what you must be prepared for.

Audit Area 1: Finding Hidden Supplies That Left No Footprint

This is the auditor's first move: identifying supplies that were never recorded as supplies at all.

Unlike goods transfers (which leave an e-way bill trail), internally rendered services, legal advice from the HO legal team to a branch, shared accounting services, and centralised HR leave no entry in the P&L account. No cash changes hands. No entry is passed. But a taxable supply has occurred.

Where Auditors Look

-

Notes to Accounts in the Annual Report: Related Party Transaction Disclosures under Ind AS / AS 18

-

Tax Audit Report (Form 3CD) Clause 23 requires disclosure of related-party transactions

-

CARO report specifically flags holding-subsidiary and key managerial personnel transactions

-

Directors' Report payments to KMP, intercompany arrangements

None of these documents are part of the GST return. But a skilled auditor uses them to map the full picture of intra-group economic activity and then cross-checks against GST outward supply declarations.

Audit Area 2: Testing the 'Full ITC' Claim: The Banking Company Example

The most dangerous assumption a taxpayer can make is that the 'Full ITC Safe Harbour' protects any nominal invoice between related parties. Auditors are explicitly trained to verify whether full ITC was actually available.

The audit manual gives a sharp illustration: A banking company transfers a car between branches for Rs 10,000 and claims the protection of Rule 28's second proviso. But banking companies face ITC restrictions either due to partial exemption (Section 17(2)) or the 50% ITC reversal rule. The branch is NOT eligible for full ITC. The auditor correctly rejects the nominal value and taxes the transaction at OMV.

The lesson is unambiguous: the safe harbour is available only when the recipient's ITC eligibility is unimpeachable. Any restriction, even partial, disqualifies the safe harbour entirely.

The Auditor's Checklist for ITC Eligibility

-

Is the recipient engaged in any exempt supply? (Section 17(2) pro rata restriction applies)

-

Is any ITC blocked under Section 17(5)?

-

Has the recipient exercised the banking company's 50% option under Rule 38?

-

Has ITC actually been reversed in GSTR-3B?

Businesses generally reconcile reversals reported in GSTR-3B with GSTR-2B under GST to identify mismatches and maintain accurate compliance records.

Audit Area 3: Import of Services from Foreign Affiliates: The Invisible RCM Supply

This is a growing area of audit focus, particularly for Indian subsidiaries of multinational groups.

Under GST, the import of services from a related person or overseas establishment is taxable under the Reverse Charge Mechanism (RCM) even when no money changes hands.

Example: The Free Engineer Deputation

A foreign parent company deputes engineers to India to assist the Indian subsidiary without any billing. The Indian subsidiary pays the engineers' hotel and travel. The auditor:

-

Examines the travel expense ledger

-

Reviews company correspondence, assignment letters, and internal emails

-

Constructs the value of the imported service using Rule 30 (cost-plus) or Rule 31

-

Raises a demand for GST under RCM along with interest

The Indian entity had no invoice. No ITC to speak of. Just a demand.

Proactive Risk Management

For Indian entities with foreign parent/affiliate arrangements: Map every intra-group service received from abroad. Obtain formal inter-company agreements with defined pricing. Even if there are no cash flows, document the valuation methodology and discharge RCM liability accordingly. Do not rely on 'no invoice, no liability' reasoning; the GST law does not recognise it for related-party imports.

Audit Area 4: Comparative Price Analysis: The Smoking Gun

For related-party supplies where goods or services are also sold to unrelated customers, auditors are trained to perform a side-by-side comparison.

They extract:

-

The price charged to the related party

-

The price charged to similar unrelated buyers for similar quantities and terms

A significant, unexplained variation is treated as a red flag for artificial value suppression.

If the OMV benchmarking shows suppression and full ITC is not available at the recipient, the auditor will re-determine value under Rules 27–31 and raise a demand with interest and penalties. In such situations, proceedings may eventually culminate in a GST demand notice under Rule 142 (DRC-01).

Audit Area 5: Employer-Employee Transactions: The Perquisite Trap

Employers and employees are deemed related persons under GST law. This creates significant exposure to non-cash benefits.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Auditors examine HR policies, offer letters, and board resolutions to identify non-cash benefits. This is an area where many companies remain non-compliant simply because the HR and Finance teams are not aligned on GST implications.

5. The Cross-Charge Question: Employee Salary in HO-Branch Valuation

A perennial controversy in GST is whether the Head Office, while cross-charging services to a Branch Office, must include the salary costs of HO employees in the taxable value.

The law has now clarified this position:

Where the recipient Branch Office is eligible for full ITC, the Head Office is NOT mandatorily required to include the cost of employee salaries while computing the taxable value of internally generated services provided to the Branch.

This clarification provides significant relief to multi-locational businesses but it is conditional entirely on full ITC eligibility at the Branch. Where full ITC is not available (e.g., branches of banks, insurance companies, or entities with mixed supplies), the question of including employee costs in the cross-charge value remains open and litigated.

6. The Practical Compliance Checklist

For tax professionals advising clients on related-party transactions, here is a structured checklist:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Why proper GST valuation matters in related-party transactions

The GST framework for related-party valuation is not merely a technicality. It is the law's answer to a fundamental question: can connected persons agree among themselves on a price and present it to the tax collector as gospel? The answer is a firm no.

The architecture of Rule 28 is sequential, rigorous, and backed by detailed audit protocols, reflecting the legislature's intent to treat intra-group transactions at arm's length, whether or not the parties choose to.

The safe harbours exist. The full ITC proviso is a powerful tool. But it is available only to those who have properly verified eligibility, not assumed it.

For CFOs, Finance Directors, and tax advisors managing group structures, the compliance imperative is clear: map every related-party supply, document every valuation methodology, and do not leave the defence to chance, particularly as businesses increasingly rely on professional GST return filing services to maintain accurate compliance documentation across related-party transactions.

When related parties transact, the law presumes proximity of interest over purity of price. It falls on the taxpayer to prove otherwise, and the time to build that proof is before the audit notice arrives, not after.

Here is the question everyone must ask today: If a GST auditor walked into your client's office tomorrow and asked for the valuation workings on every intra-group supply made in the last three years, would the documentation hold?

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified