There are various types of refunds available under the GST regime, referencing ONLY the directly relevant statutory provisions, rules, circulars, and latest amendments.

1. Statutory Provisions: CGST Act, 2017

Section 54: Refund of Tax

-

Governs the primary framework for refund claims.

-

Allows refund of tax, interest, or any other amount paid (Section 54(1)), subject to an application made within two years from the relevant date.

-

Explains and restricts the refund of unutilized input tax credit (ITC) under certain circumstances (Section 54(3)), such as zero-rated supplies, inverted duty structure, and with key exceptions.

Special Provisions:

-

Section 54(6): Provision for grant of provisional refund (90%) in cases of zero-rated supply (export without payment of tax), subject to further scrutiny and final order.

Section 55: Refund to Certain Persons

-

Allows notified specialised agencies (like UN organisations, embassies) to claim a refund on inward supplies, as notified.

2. Relevant Rules: CGST Rules, 2017

Rule 89 - Application for Refund

-

Lays down the electronic application procedure (Form GST RFD-01).

-

Refund can be claimed for various categories such as excess cash ledger balance, unutilized ITC, IGST paid on export, etc.

-

Mandatory Aadhaar authentication for registered persons (Rule 10B, effective 01.01.2022).

Rule 96 - Refund of Integrated Tax Paid on Goods/Services Exported

-

Automates IGST refund processing for export of goods, deeming shipping bills as refund applications (subject to conditions).

Rule 95B (Inserted Vide Notification No. 12/2024-CT dt. 10.07.2024)

-

Refund process specific to Canteen Stores Department (CSD).

Rule 97A

-

Permits manual filing in specified circumstances.

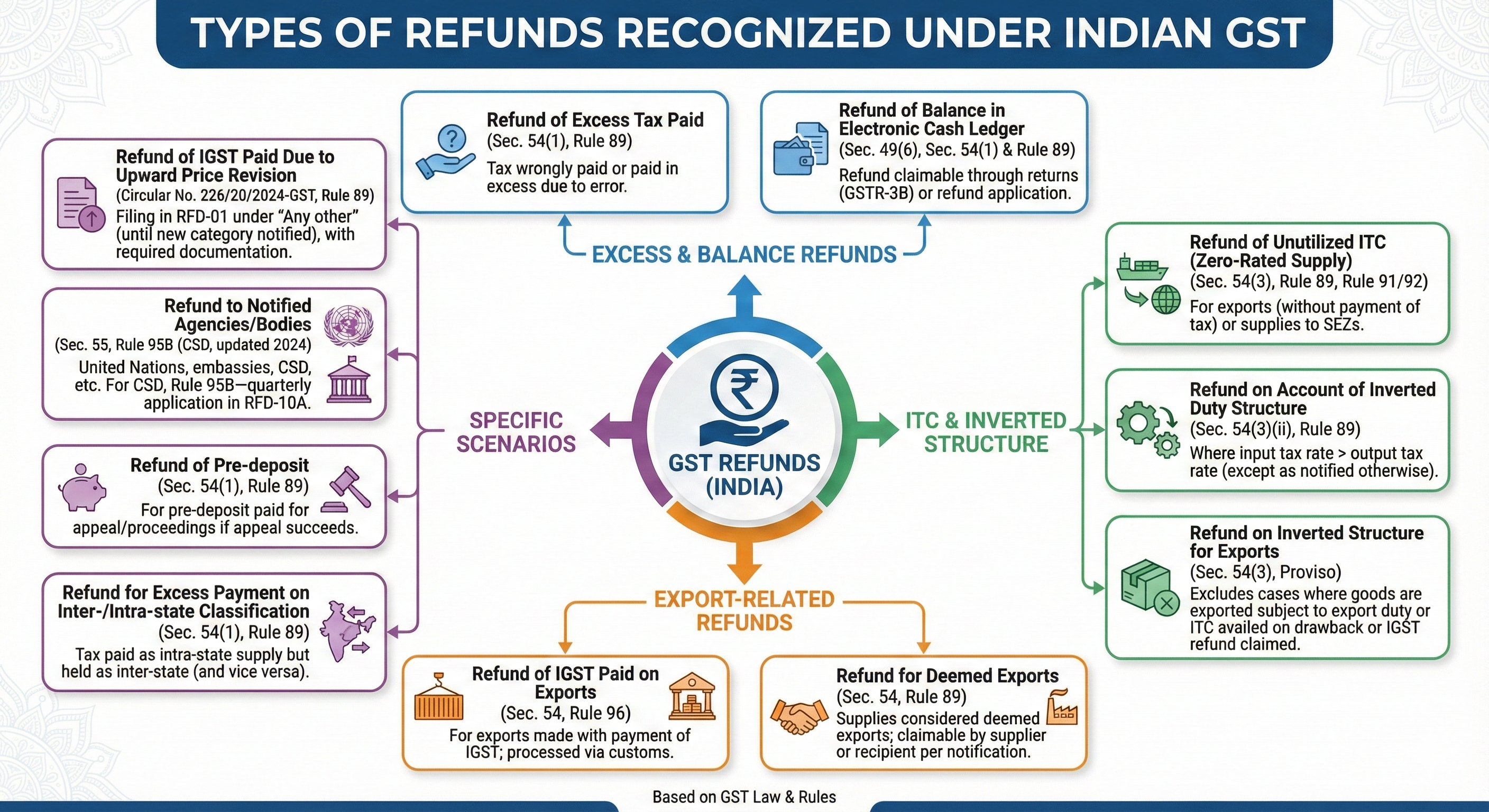

3. Types of Refunds Recognised under GST

| Type of Refund | Statutory Basis | Key Details |

| Refund of excess tax paid | Sec. 54(1), Rule 89 | Tax wrongly paid or paid in excess due to an error. |

| Refund of balance in the electronic cash ledger | Sec. 49(6), Sec. 54(1) & Rule 89 | Refund claimable through returns (GSTR-3B) or a refund application. |

| Refund of unutilized ITC (zero-rated supply) | Sec. 54(3), Rule 89, Rule 91/92 | For exports (without payment of tax) or supplies to SEZs. |

| Refund on account of inverted duty structure | Sec. 54(3)(ii), Rule 89 | Where input tax rate > output tax rate (except as notified otherwise). |

| Refund of IGST paid on exports | Sec. 54, Rule 96 | For exports made with payment of IGST; processed via customs. |

| Refund for deemed exports | Sec. 54, Rule 89 | Supplies considered deemed exports; claimable by supplier or recipient per notification. |

| Refund of IGST paid due to upward price revision | Circular No. 226/20/2024-GST, Rule 89 | Filing in RFD-01 under “Any other” (until new category notified), with required documentation. |

| Refund to notified agencies/bodies | Sec. 55, Rule 95B (CSD, updated 2024) | United Nations, embassies, CSD, etc. For CSD, Rule 95B—quarterly application in RFD-10A. |

| Refund of pre-deposit | Sec. 54(1), Rule 89 | For pre-deposit paid for appeal/proceedings if appeal succeeds. |

| Refund on inverted structure for exports | Sec. 54(3), Proviso | Excludes cases where goods are exported subject to export duty or ITC availed on drawback or IGST refund claimed. |

| Refund for excess payment on inter-/intra-state classification | Sec. 54(1), Rule 89 | Tax paid as intra-state supply but held as inter-state (and vice versa). |

4. Additional/Recent Developments (2024–2025)

| Amendment/Notification | Key Change |

| Circular No. 226/20/2024-GST (11.07.2024) | Mechanism for claiming refund of additional IGST paid on upward price revision post-export, via RFD-01. |

| Circular No. 227/21/2024-GST (11.07.2024) | Electronic refund process for CSD under new Rule 95B; quarterly RFD-10A. |

| Notification No. 12/2024-CT (10.07.2024) | Amended CGST Rules to insert Rule 95B (CSD refunds) and support upward price revision refunds. |

| 2025 Council Recommendations/Proposed Amendments | Risk-based provisional refund for inverted duty structure and exports; proposal to remove ₹1,000 limit for export refunds. |

5. Procedural Clarifications and Circulars

-

Refund Claims Filing: Must be chronological and not for periods prior to already claimed periods (Circular No. 135/05/2020-GST).

-

Export Refunds: Filing by month/quarter, but not spanning different financial years unless specifically allowed (Circular No. 37/2018).

-

Unregistered Persons: Refund only in specific scenarios like contract cancellation (Circular No. 188/20/2022-GST).

-

Undertaking for Refunds: Applicants must undertake to repay the amount with interest if later found ineligible (Circular No. 125/44/2019-GST).

-

Provisional Refunds: 90% refund may be granted provisionally for zero-rated and, prospectively, IDS; balance after final scrutiny (Rule 91, forthcoming amendment).

Practical Implications

-

Form to Use: Typically, FORM GST RFD-01 (electronic) for most categories; RFD-10A for CSD; and GSTR-3B return for cash ledger refunds.

-

Time Limits: Generally within 2 years of the relevant date (Section 54(1)), with special limits for certain classes (e.g., 6 months for UN agencies).

-

Documentation: Ensure all documents are as per Rule 89(2), and additional documents for special categories (as per latest circulars and notifications).

-

New Categories & Process: Watch for operationalisation of risk-based provisional refunds (from 1 Nov 2025 for IDS/Export) and portal developments for new refund types.

Summary Table: Refund Types

| # | Refund Type | Main Provision(s) | Key Form/Process | Recent Update (2024–25) |

| 1 | Excess tax paid | Sec. 54(1), Rule 89 | RFD-01 | |

| 2 | Cash ledger balance | Sec. 49(6), Sec. 54(1), Rule 89 | GSTR-3B or RFD-01 | |

| 3 | Unutilized ITC (zero-rated supply) | Sec. 54(3), Rules 89, 91/92 | RFD-01 | Risk-based provisional refund (from Nov 2025) proposed |

| 4 | Inverted duty structure (IDS) | Sec. 54(3), Rule 89 | RFD-01 | Risk-based provisional refund (from Nov 2025) proposed |

| 5 | IGST on export (with payment) | Sec. 54, Rule 96 | Deemed via Shipping Bill | Portal/Customs processing |

| 6 | Refund to agencies (UN, CSD, etc.) | Sec. 55, Rule 95B (CSD) | RFD-10A (CSD), RFD-01 | Rule 95B (CSD), Qtrly, new e-filing process (2024) |

| 7 | Upward IGST on export price revision | Cir. 226/20/2024-GST, Rule 89 | RFD-01 "Any Other" | New mechanism & portal updation underway |

| 8 | Pre-deposit for appeals | Sec. 54(1), Rule 89 | RFD-01 | |

| 9 | Excess inter-/intra-state reclassification | Sec. 54(1), Rule 89 | RFD-01 |

Key Points

-

Only directly relevant types and procedures are covered above as per statutory and regulatory framework.

-

For new types (e.g. upward price revision, CSD refunds), follow the latest circulars/notifications for the process and eligible documentation.

-

Always verify the latest notifications and circulars for operational details as procedures may rapidly evolve.

-

If your scenario does not fit the above, please specify for further guidance.

References:

-

CGST Act, 2017: Sections 54, 55

-

CGST Rules: 89, 91, 92, 95B, 96, 97A

-

Circular No. 226/20/2024-GST (IGST on upward price revision)

-

Circular No. 227/21/2024-GST (CSD refunds)

-

Notification No. 12/2024-CT

-

Circular No. 125/44/2019-GST (refund undertakings and provisional refund process)

-

Latest Council Recommendations & Amendments (2025)

DRC-01 format | Need for GST in India | Powers of GST Officers | GST Audit Procedure | GST ADT-01 | Penalty for Non GST Registration

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified