When "Sent" Is Not "Served": What Every Finance Leader Must Know About Tax Notice Laws

A tax demand cannot touch you until it reaches you lawfully. Understanding how a notice must be served is not just procedural knowledge. It is the difference between winning and losing a dispute before the fight even begins.

The Hidden Landmine in Every Tax Dispute

In the boardroom, finance leaders spend hours preparing for audits. They build response strategies, appoint consultants, and brief legal teams. Yet one of the most powerful weapons in a taxpayer's arsenal is almost always overlooked.

That weapon is the validity of the service of notice.

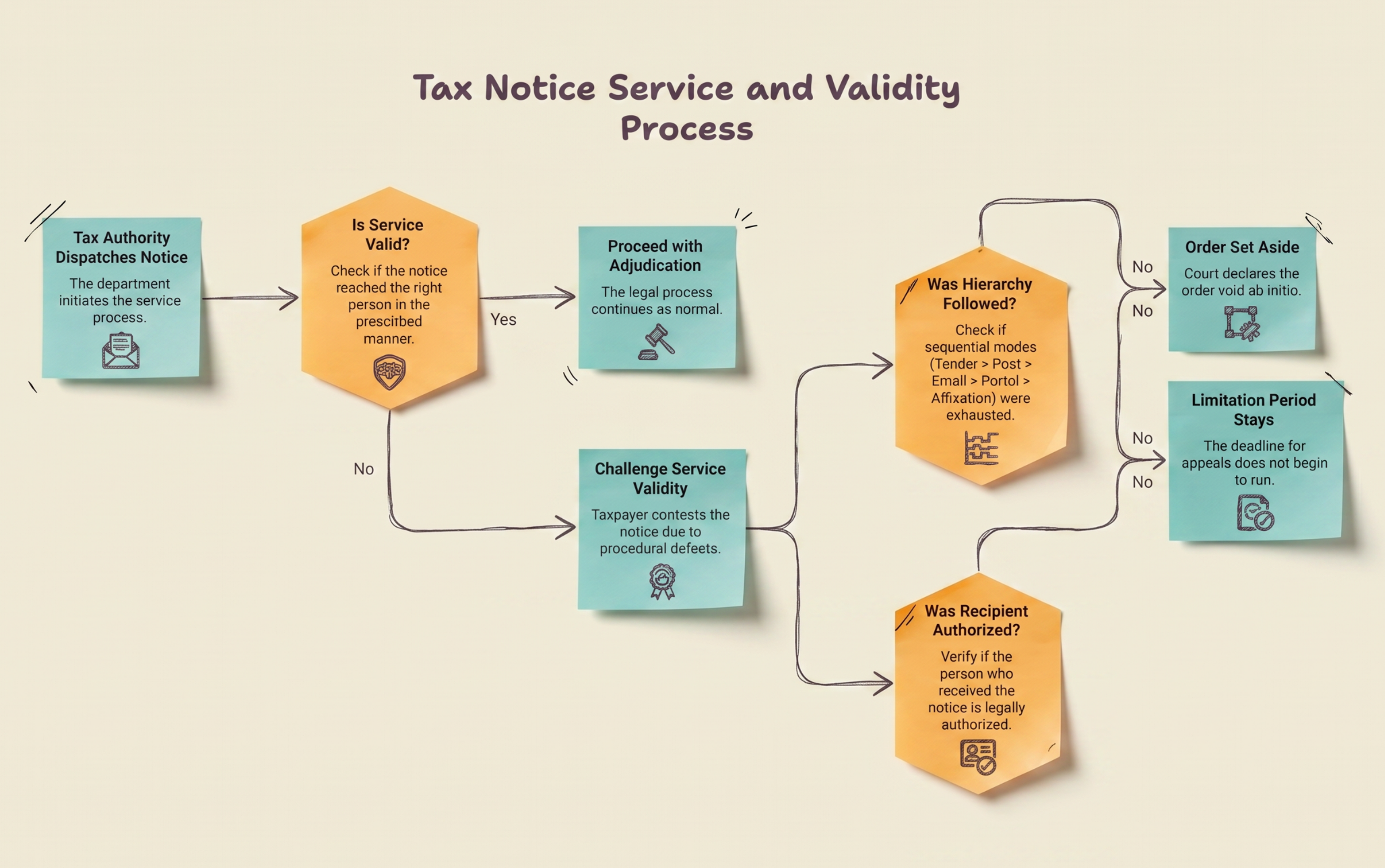

Every tax proceeding, whether under GST, Income Tax, Customs, or Central Excise , begins with a notice. But a notice that is not served correctly is, in the eyes of the law, a notice that was never served at all.

This has profound consequences:

-

Limitation periods do not begin running until valid service is made.

-

Orders passed without valid service are liable to be set aside.

-

Appeals filed long after the apparent "deadline" can still be entertained by courts , if service was defective.

This article explains the law, the case law, and what finance leaders must do to protect their organisations and their personal rights as authorised signatories.

Part I: The Foundation – What Is "Notice" and What Is "Service"?

What Is a Notice?

In legal parlance, a notice is a formal intimation. It puts a party on official awareness of a legal process that affects their rights, obligations, or duties. It can be:

-

A Show Cause Notice (SCN) proposing demand or penalty

-

A Summons requiring personal appearance

-

An Order passed in an adjudication proceeding

-

Any other communication under a tax statute

The Oxford Concise Dictionary defines notice as "formal intimation of something, or instructions to do something." Webster's Dictionary goes further: service of notice means "act of bringing to notice, either actually or constructively, in such manner as is prescribed by law."

What Is "Service of Notice"?

Service of notice means that the notice has been delivered to the right person, in the right manner, as prescribed by law. It is not enough that the department dispatches a notice. The notice must actually reach the party it is intended for.

This principle was stated with clarity by the Supreme Court:

"Giving of anything is not complete unless it has reached the hands of the person to whom it has to be given." , K. Narasimhah v. H.C. Singri Gowda (AIR 1966 SC 330)

The sending of a notice is not the completion of the giving of a notice. This is the cornerstone principle that all subsequent law is built on.

Part II: Why This Matters: The Principles of Natural Justice

Valid service of notice is not a technical formality. It is the gateway to natural justice.

The Audi Alteram Partem Principle

Audi alteram partem, Latin for "hear the other side", is a foundational principle of Indian law. No person can be condemned without a fair hearing. For a hearing to be fair:

-

The party must be informed of the allegations.

-

The party must be given a real opportunity to respond.

-

The party must know the time, place, and date of the hearing.

Service of notice is the mechanism through which all of this is ensured.

Consequences of Defective Service

| Consequence | Legal Impact |

Order passed without valid notice |

Void ab initio (null and void from inception) |

Limitation period not started |

Appeal limitation does not run |

Ex parte order passed |

Liable to be recalled and set aside |

Recovery proceedings initiated |

Can be challenged as prematur |

An order passed without a validly served notice is not merely voidable. Courts across India have consistently held that it violates the principles of natural justice and is without jurisdiction.

Part III: The Legal FRAMEWORK – How Tax Notices Must Be Served

India's major tax statutes each prescribe a specific set of modes for service. What is critical to understand is that these modes are hierarchical and sequential , not optional.

Modes of Service Under Different Laws

Mode of Service |

Customs Act, 1962 (S.153) |

Central Excise Act, 1944 (S.37C) |

CGST Act, 2017 (S.169) |

Income Tax Act, 1961 (S.282) |

Direct tender / hand delivery |

✓ |

✓ |

✓ |

✓ |

Registered Post (RPAD) |

✓ |

✓ |

✓ |

✓ |

Speed Post with proof of delivery |

✓ |

✓ |

✓ |

✓ |

Courier with acknowledgement |

✓ |

✓ |

✓ |

✓ |

Email / Electronic communication |

✓ |

, |

✓ |

✓ |

Common Portal / GST Portal |

, |

, |

✓ |

, |

Publication in newspaper |

✓ |

, |

✓ |

, |

Affixation at last known address |

✓ |

✓ |

✓ |

, |

Affixation on office notice board |

✓ |

✓ |

✓ |

, |

The Hierarchy Under GST , Section 169, CGST Act

Section 169 of the CGST Act, 2017 provides for the following modes of service, in this order:

-

Direct tender , to the taxable person, their manager, authorised representative, advocate, tax practitioner, a regular employee, or an adult family member residing with the taxpayer.

-

Registered post or speed post or courier with acknowledgement due , to the last known place of business or residence.

-

Email , to the address provided at the time of GST registration.

-

Common Portal , by making it available on the GST portal.

-

Newspaper publication , in a newspaper circulating in the locality.

-

Affixation , at the last known place of business or residence, only if all the above modes are not practicable.

-

Affixation on the officer's notice board , the last resort, when even affixation at the taxpayer's premises is not practicable.

This is not a list of equal alternatives. The law requires sequential exhaustion. Jumping directly to affixation , without attempting the earlier modes , is illegal and renders the service invalid.

Part IV: When Is Service "Deemed Complete"?

The Deeming Provisions

Section 169(2) and 169(3) of the CGST Act create deeming fictions for service:

-

169(2): A notice shall be deemed to have been served on the date it is tendered, published, or affixed in the manner provided under Section 169(1).

-

169(3): When sent by registered post or speed post, the notice shall be deemed to have been received at the expiry of the period normally taken by such post in transit, unless the contrary is proved.

When Courts Have Upheld Deemed Service

| Scenario | Court | Ruling |

Order passed in presence of advocate |

Allahabad HC (Nanumal Glass Works Vs Commissioner of Central Excise, Kanpur –2016Taxo.online 119– (ALL)) |

Service deemed complete on that date itself |

Speed post tracking shows delivery |

AP HC (RAMAKOTAIAH vs. ASSISTANT COMMR. OF C. EX. & S.T., VISAKHAPATNAM –2018(359) E.LT. 278 – (A.P.)) |

Burden shifts to assessee to disprove delivery |

Certificate from Postmaster of delivery |

P&H HC (Greenview land and buildcon Ltd. Vs. Union of India –2012 Taxo.online 14) |

Presumption of service , not rebutted by mere affidavit |

Registered post delivered to correct address |

Orissa HC (Jay Balaji Steels Ltd. Vs. CESTAT, Kolkata –2014 Taxo.online 17 (Ori.)) |

Delivery to correct address = valid service |

Speed post treated equivalent to registered post |

Orissa HC (Jay Balaji Steels Ltd. Vs. CESTAT, Kolkata –2014 Taxo.online 17 (Ori.)) |

No distinction between the two modes |

Important: The presumption is rebuttable

The presumption of service created under Section 27 of the General Clauses Act, 1897 is permissible, not inevitable. The Supreme Court in Mst..L.M.S. Ummu Saleema v. B.B. Gujral [MANU/SC/0072/1981: 1981 (3) SCC 317], it was clarified that courts may or may not draw this presumption based on facts.

The burden of rebutting the presumption lies with the party challenging service. But the initial burden to establish service lies with the authority that dispatched the notice.

Part V: When Service Is NOT Valid, The Red Zone

This is the most practically important section for finance leaders. Courts have struck down service and, consequently, set aside orders or condoned delays , in the following situations.

1. Service on an Unauthorised Person

Service must be made to a person legally authorised to accept it. Service on the following has been held invalid:

| Person Served | Court | Ruling |

Driver of vehicle |

Allahabad HC (Jindal Pipes Limited VS. State of U.P. and 3 others cited in 2020Taxo.online 49 – Allahabad High Court.) |

Service on driver = no service at all |

Friend of Director |

Delhi Tribunal (Usha Stud & Agricultural farms (P) Ltd. Vs. Comm. Of Cus., New Delhi – 2011(274) E.L.T. 365 – (Tri. – Del.)) |

Friend is not an authorised agent |

"Kitchen boy" (daily wage worker) |

Supreme Court (Saral Wire Craft Pvt. Ltd. Vs. Comr. Of Cus. C. Ex. And Service Tax cited in2015 Taxo.online 1) |

Void , order set aside, limitation ran from date of actual knowledge |

Security Guard |

CESTAT Delhi (Shri Ameya Electricals Pvt. Ltd. Vs. Commissioner of CGST, Cus. & C.Ex.,Ujjain – 2019 Taxo.online 1014) |

Invalid; effective service only from date guard delivered notice to management |

Guard/Caretaker |

CESTAT Allahabad (Harish Aneja Vs. Comm. C. Ex. & Service Tax, Hapur – 2016 Taxo.online24 (Tri. – All.)) |

Neither employee, nor family member, nor authorised person |

Dismissed employee |

Calcutta HC (Matigara Rolling Mills (P) Ltd. Vs. Commissioner of C. Ex., Siliguri – 2007(7)S.T.R. 363 – (Cal.) ) |

Person no longer in employment cannot accept service on behalf of the company |

Practical Warning: In many manufacturing units and offices, the security guard or receptionist receives all mail. Finance leaders must ensure these personnel are covered by the authorisation framework, or, better still, that senior management is personally notified of all tax communications immediately upon receipt.

2. Service on Wrong Address or Old Address, After Department Was Informed

| Scenario | Ruling |

The firm stopped business; the department was informed, notice still sent to the old business address |

Kerala HC (Reji Kurian Vs State Tax Officer, Goods & Service Tax, Mattancherry [(2018) 13 GSTL 260 (Ker.)]): Order set aside as violative of natural justice |

New address after merger known to the department, but notice sent to the old addres |

Rajasthan HC (Expo-Fyn Electricals & Electronics vs Commissioner of Central Excise [(2018) 8 GSTL 160 (RAJASTHAN)]: Matter remanded; ex parte order set aside |

Old address sent to by Tribunal registry, though new address given in recall application |

Bombay HC (Man – Made Spinners (I0 Ltd. Union of India – (2019) 368 ELT 246 (Bom.): Both orders set aside as breach of natural justice |

But note the flip side: If the taxpayer shifts office and does NOT inform the department, the service at the old address will be held valid, and the limitation will run from that date.

Key Lesson: Always update your address with every tax authority immediately upon any change. File an amendment application. Keep the acknowledgement.

3. Affixation Without Exhausting Prior Modes

This is one of the most common departmental violations. Authorities frequently skip to affixation , the last resort, without attempting registered post, email, or other prior modes.

Courts have consistently held:

-

Kashi Bartan Bhandar Vs State of U.P. – 2018 Taxo.online 651 (Allahabad HC): Affixation directly, without attempting earlier modes, is not valid service.

-

Ram Nivas Singh Contractor Vs. Of C. Ex. & S.T., Allahabad – 2018Taxo.online 649 (CESTAT Allahabad): "Colourable exercise of power" , no attempt at registered post, directly affixed.

-

Global Agencies Pvt. Ltd. Comm. Of C.Ex., Daman – 2009 Taxo.online8 – Agencies (CESTAT Ahmedabad): No finding that registered post was first attempted. Affixation of no avail.

-

Soham Realators Pole Star Vs Commissioner of C. Ex., Cus. & S.T., Nagpur – II (Bombay HC): After failed postal service, authority jumped to newspaper publication, skipping affixation. Not valid.

The rule is simple: affixation is available only when all previous modes have failed and that failure is documented.

4. No Affixation After Notice Returned Undelivered

When a notice is returned by the postal authorities with remarks such as "left", "unserved", or "unclaimed", the department must take the next step: affixation. Simply treating the returned envelope as proof of refusal , and proceeding to adjudication , has been set aside.

-

Ashesh Goradia Vs. Commissioner of Central Excise, Mumbai – III – 2012 Taxo.online 15 (Tri. – Mum.) – (CESTAT Mumbai): Notices returned with remarks "left/unserved." No affixation on the notice board. Adjudication set aside.

The postal remark "not found in delivery time" or "nobody in the factory" does NOT amount to refusal. It means the party was temporarily unavailable. Fresh steps must be taken.

5. Speed Post / Registered Post Without Proof of Delivery

Section 37C of the Central Excise Act (and, analogously, Section 169 of the CGST Act) require service by speed post or registered post with proof of delivery (acknowledgement due). Courts have firmly held:

-

Dispatch of a speed post letter is not proof of delivery.

-

Speed Post Bar Code Number alone is not proof of delivery.

-

The RPAD acknowledgement slip signed by the addressee is what constitutes valid proof.

If the department cannot produce the signed RPAD card, it has not discharged its initial burden of proof. The limitation period does not begin running until the order actually reaches the assessee.

Part VI: Who Bears the Burden of Proof?

The initial burden of proof is on the department that dispatched the notice. This is not a minor procedural point , it is a fundamental principle of law.

The Delhi High Court in Neha Cosmetics v. Commissioner of Central Excise held:

"The initial burden of proof of tender or delivery of such decision by post as required under Section 37C(2) read with Section 27 of the General Clauses Act is on the authority dispatching such notice."

The burden shifts to the assessee only after the department has established that the notice was in fact sent and delivered.

Burden of Proof , Summary

| Stage | Who Bears the Burden |

Proving that the notice was dispatched |

Department |

Proving that the notice was delivered |

Department |

Rebutting the presumption of delivery (once established) |

Assessee |

Proving non-receipt at new/changed address |

Assessee (if change not intimated to department) |

Part VII: Practical Checklist for Finance Leaders

The following checklist should be part of every company's tax compliance and litigation management protocol.

On Receipt of Any Tax Notice, Order, or Summons

-

Record the exact date of receipt in an internal register. This date triggers limitation periods.

-

Check whether the notice was served on the right person. Was it received by an authorised signatory, manager, or authorised representative? Or by a guard, driver, or delivery boy?

-

If received by an unauthorised person, immediately document when management first obtained actual knowledge of the notice.

-

Check the mode of service used. Was it by RPAD, speed post, email, or common portal?

-

Check whether all prior modes were exhausted if the notice was served by affixation.

-

Preserve the envelope, acknowledgement card, postal receipt, or any digital delivery confirmation.

Proactive Steps for the Organisation

-

Maintain an updated address on record with every tax authority , GST, Income Tax, Customs, and State tax authorities. File address amendment whenever there is a change.

-

Designate and formally authorise specific employees to receive tax communications. Maintain a board resolution or power of attorney.

-

Register the correct email addresses with all tax departments and ensure those mailboxes are actively monitored.

-

Check the GST common portal and income tax e-filing portal regularly (at least fortnightly) for notices made available electronically.

-

In case of insolvency or liquidation, ensure all tax departments are intimated and notices are directed to the Official Liquidator , not the erstwhile management.

-

In case of merger, amalgamation, or change of entity name, file intimation letters with all tax authorities immediately with the new address.

When Filing an Appeal , Service-Related Grounds

-

Always check whether there was valid service of the impugned order before computing the limitation period.

-

If service appears defective, specifically raise this ground before the Commissioner (Appeals) or Tribunal.

-

Collect evidence of non-service: postal tracking records, email inbox printouts, portal login history.

-

File a declaration on oath regarding the date of actual knowledge of the order.

-

Ask the department to produce the RPAD acknowledgement. If they cannot, press the point.

Conclusion: Words From Experience

After decades of representing taxpayers before adjudicating authorities, appellate tribunals, and High Courts, here is what I have learned about notice and service , not just as law, but as lived reality.

Procedure is substance. In tax law, those who dismiss procedural safeguards as "technical" have usually never lost a case because of them. The requirement of valid service is not a loophole. It is the law's way of saying: no one shall be condemned unheard, and no one shall be penalised in ignorance.

A notice never received is a notice never issued. The highest courts of this land have said it repeatedly, in different words, across decades: sending is not giving. Dispatching is not delivering. The act of placing an envelope in a post box does not end the state's obligation. It is only the beginning.

The burden is on the state, not on you. This is perhaps the most underappreciated protection available to taxpayers. Before you are asked to prove non-receipt, the department must first prove delivery. Demand that proof. Do not accept assumptions and surmises in place of evidence.

Your organisation's address is a legal asset. Guard it. Every time your company moves offices, every time the registered address changes, and every time key persons change , update every tax authority. An unmaintained address is a door left open for an ex parte order that could haunt you for years.

Authorise the right people. A tax demand served on a driver is no demand at all , but only if you can prove it and if you act in time. Put in place systems: authorised signatories, a dak register, and a protocol for escalating tax communications to the CFO or tax manager on the day of receipt.

Time is your most finite resource in tax disputes. Limitation periods are unforgiving. Yet courts have consistently protected those who were genuinely denied the opportunity to know of an order. The law on service is your shield, but only if you know it, invoke it promptly, and back it with evidence.

To every CFO, Director Finance, and finance leader reading this: the next time a recovery officer arrives at your premises or the portal flashes a demand you had no knowledge of , do not panic. Ask one question first: was the original notice validly served on me? That single question, backed by this law, may be worth more than all the substantive arguments combined.

The law protects the vigilant..! Be vigilant…!!

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified