Understanding Section 67 of the GST Act: Powers of Inspection, Search and Seizure

The Goods and Services Tax (GST) regime in India empowers tax authorities with specific enforcement mechanisms to ensure compliance and prevent tax evasion. Among these mechanisms, Section 67 of the Central Goods and Services Tax (CGST) Act, 2017, stands as a crucial provision that grants powers of inspection, search, and seizure to proper officers. This article provides a comprehensive examination of Section 67 and its practical implications for businesses operating under the GST framework.

Overview of Section 67

Section 67 serves as the legal foundation for GST authorities to conduct inspections, searches, and seizures when they have reasonable grounds to believe that tax evasion has occurred or is likely to occur. This provision strikes a balance between the government's need to enforce tax compliance and the rights of taxpayers, establishing clear procedures and safeguards for enforcement actions.

Key Provisions and Their Implications

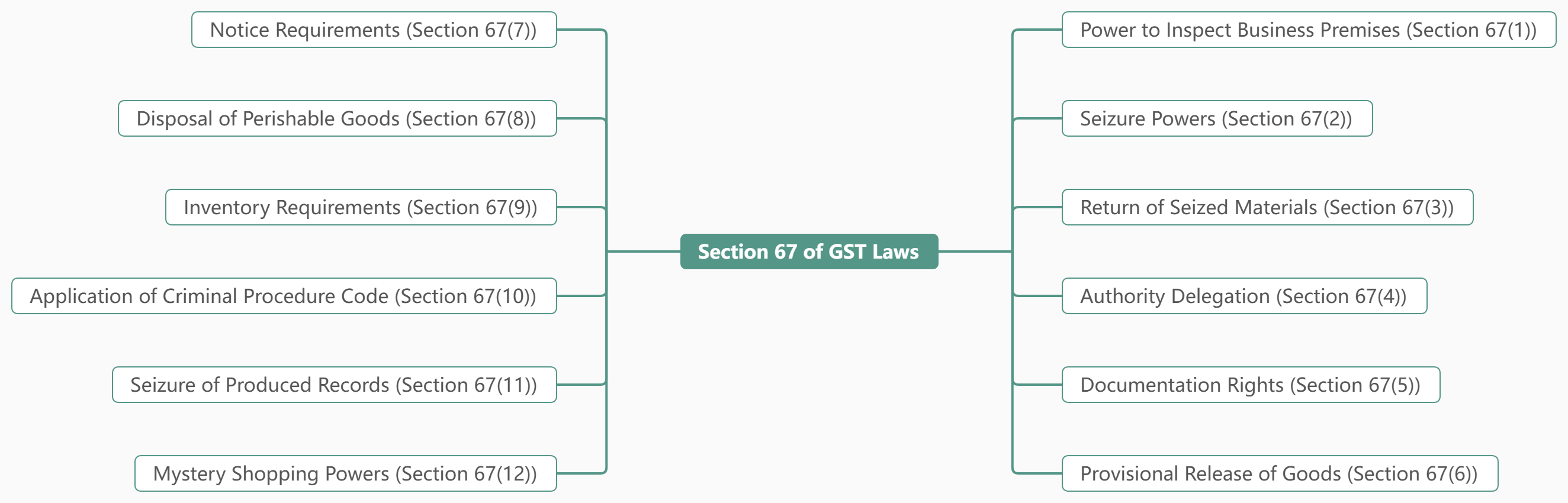

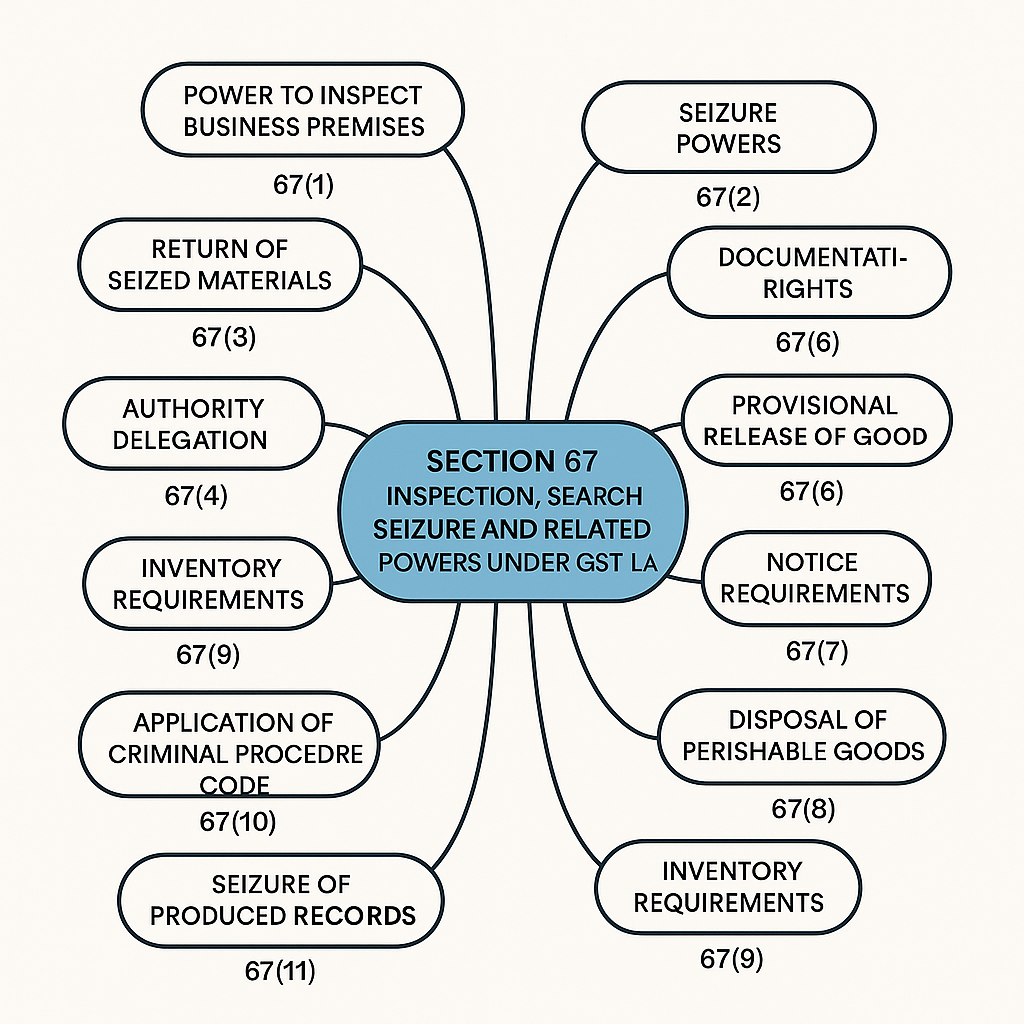

Power to Inspect Business Premises (Section 67(1))

The first subsection grants proper officers the authority to inspect any place of business. This inspection power enables officers to verify whether businesses are maintaining proper records, issuing correct invoices, and complying with GST regulations. The inspection can cover physical verification of goods, examination of documents, and assessment of business operations to ensure GST compliance.

Seizure Powers (Section 67(2))

When officers discover irregularities during inspection, Section 67(2) empowers them to seize goods, documents, or other items that may serve as evidence of tax evasion. This provision ensures that crucial evidence is preserved and prevents its destruction or tampering. The seizure must be conducted following proper procedures and documentation requirements.

Return of Seized Materials (Section 67(3))

This subsection provides relief to taxpayers by mandating the return of seized documents, books, and other materials once they are no longer required for investigation or legal proceedings. This provision prevents indefinite retention of business records and minimises disruption to normal business operations.

Authority Delegation (Section 67(4))

Section 67(4) clarifies the hierarchical structure of enforcement powers, specifying which officers can exercise these powers and under what circumstances. This ensures that inspections and seizures are conducted by duly authorized personnel, maintaining the legitimacy of enforcement actions.

Documentation Rights (Section 67(5))

Recognizing the importance of business continuity, this subsection allows taxpayers to obtain copies or extracts of seized documents. This provision ensures that businesses can continue their operations even when original documents are in custody of tax authorities.

Provisional Release of Goods (Section 67(6))

To minimize business disruption, Section 67(6) provides for the provisional release of seized goods under certain conditions. This typically involves furnishing a bond or security, allowing businesses to continue trading while investigations proceed.

Notice Requirements (Section 67(7))

This subsection addresses situations where immediate notice of seizure may not be issued, specifying the circumstances and procedures for such cases. This provision balances the need for effective enforcement with transparency requirements.

Disposal of Perishable Goods (Section 67(8))

Recognizing the special nature of perishable goods, Section 67(8) empowers proper officers to dispose of such goods in appropriate cases. This prevents economic waste while ensuring that the interests of all parties are protected.

Inventory Requirements (Section 67(9))

To ensure transparency and accountability, this subsection mandates the preparation of detailed inventory sheets for all seized items. This documentation serves as crucial evidence and protects both tax authorities and taxpayers from disputes about seized materials.

Application of Criminal Procedure Code (Section 67(10))

This provision establishes that relevant provisions of the Code of Criminal Procedure (CrPC) apply to searches and seizures under GST law. This integration ensures that established legal procedures and safeguards are followed during enforcement actions.

Seizure of Produced Records (Section 67(11))

Section 67(11) extends seizure powers to records that are voluntarily produced before officers during proceedings. This ensures that all relevant evidence can be secured, regardless of how it comes to the attention of authorities.

Mystery Shopping Powers (Section 67(12))

An innovative provision, Section 67(12) allows the department to pose as customers to verify compliance. This enables authorities to detect violations that might not be apparent through traditional inspection methods.

Procedural Framework Under Rule 139

Rule 139 of the CGST Rules, 2017, provides detailed procedures for implementing the powers under Section 67. The rule covers five key areas:

Rule 139(1) establishes procedures for conducting inspections and searches, ensuring systematic and lawful enforcement actions. Rule 139(2) specifies requirements for seizure orders, providing documentary evidence of enforcement actions. Rule 139(3) places obligations on owners or custodians of seized materials, establishing their responsibilities during the process. Rule 139(4) addresses situations where physical seizure is impracticable, providing alternative mechanisms for securing evidence. Rule 139(5) mandates detailed inventory preparation, ensuring proper documentation of all seized items.

Best Practices for Businesses

To ensure compliance and minimize risks associated with inspection and seizure actions, businesses should maintain accurate and complete records of all GST transactions, ensure proper invoice generation and maintenance, conduct regular internal audits to identify and rectify compliance gaps, train staff on GST compliance requirements and inspection procedures, and maintain good relationships with tax authorities through transparent dealings.

Conclusion

Section 67 of the CGST Act represents a critical enforcement mechanism in India's GST framework. While it grants significant powers to tax authorities, it also incorporates important safeguards to protect taxpayer rights. Understanding these provisions helps businesses maintain compliance and respond appropriately to enforcement actions. As the GST regime continues to evolve, staying informed about enforcement provisions remains essential for successful business operations in India's tax landscape.

The balanced approach of Section 67, combining enforcement powers with procedural safeguards, reflects the GST law's objective of creating a fair and efficient tax system. By understanding and respecting these provisions, businesses can contribute to a compliant tax ecosystem while protecting their legitimate interests.

GST Filing Software | Eway Bill Apis | Power of Officer Under GST | GST On Dry Fruits | GST On Society Maintenance

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified