GST Refunds under Section 54: Complete Legal Framework, Eligibility & Process Explained

Section 54: Refund of Tax, is the foundational provision within Chapter 12: Refunds (Sections 54-58) of the Central Goods and Services Tax (CGST) Act, establishing the legal framework and procedures for a person to claim various types of refunds. This ensures that excess tax paid, unutilised input tax credit (ITC), and other amounts erroneously paid are returned to eligible claimants.

Eligibility and Application for Refund (Section 54(1))

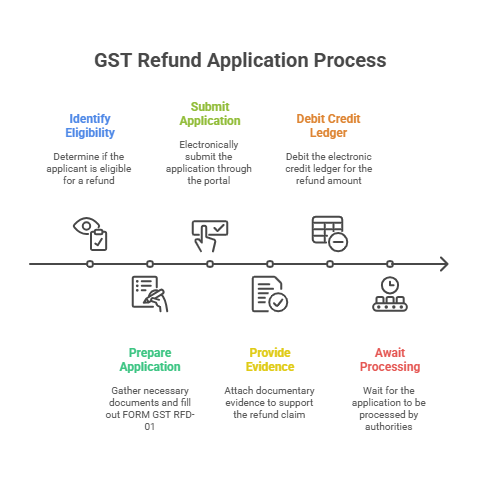

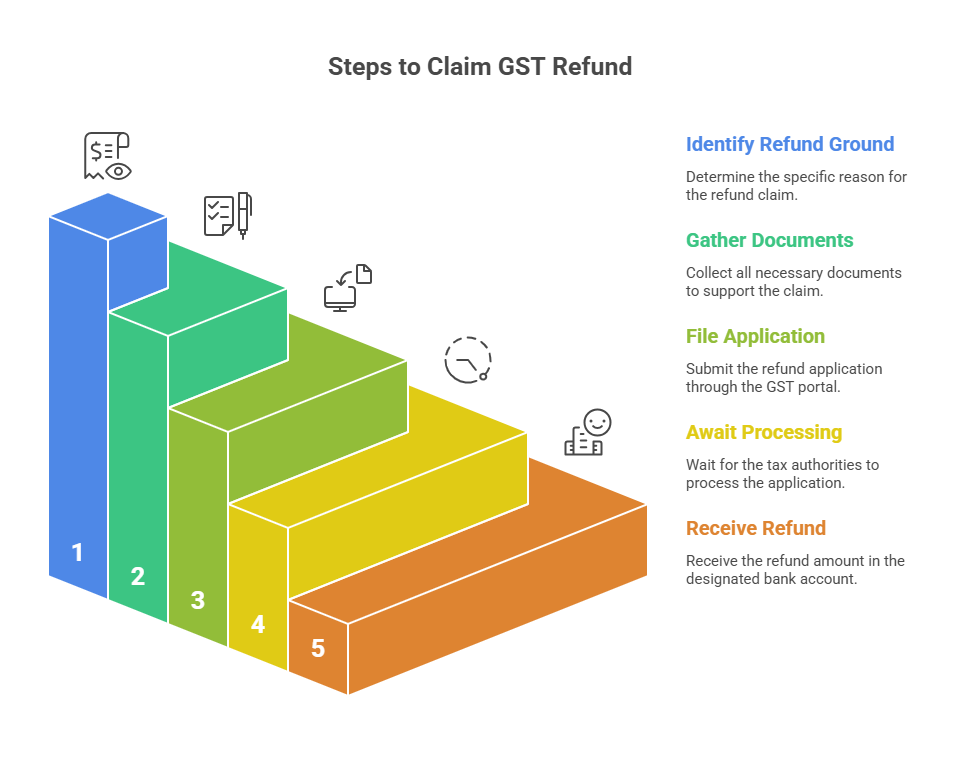

Any person claiming a refund of any tax and interest, if any, paid on such tax or any other amount paid by them, may make an application. This application is typically filed electronically in FORM GST RFD-01 through the common portal, either directly or through a Facilitation Centre.

A crucial condition for claiming a refund is that the application must be made before the expiry of two years from the relevant date. The "relevant date" varies depending on the nature of the refund claim. For instance, for tax wrongfully collected and paid as per Section 77, the relevant date is the date of payment of tax under the correct head. The period from 1st March 2020 to 28th February 2022 was excluded for computing this limitation period, offering relief to taxpayers.

The application must be accompanied by documentary evidence to establish that a refund is due and, generally, that the incidence of the tax had not been passed on to any other person. However, if the amount claimed as refund is less than two lakh rupees, a self-declaration based on available evidence, certifying that the incidence of tax was not passed on, may suffice. The electronic credit ledger is debited by the applicant for the claimed refund amount.

Specific Grounds for Refund under Section 54

1. Refund of Unutilised Input Tax Credit (ITC) (Section 54(3)):

◦ Zero-rated supplies: This includes exports of goods or services or both, and supplies made to Special Economic Zone (SEZ) units or developers.

▪ Exports of goods: Requires a statement with shipping bills or bills of export and relevant export invoices. For export of electricity, specific details including energy exported and tariff are required. The value of goods exported is typically the Free on Board (FOB) value in the Shipping Bill or Bill of Export. Insistence on proof of realization of export proceeds for goods is generally not envisaged in the law.

▪ Exports of services: Requires a statement with invoices and relevant Bank Realisation Certificates (BRC) or Foreign Inward Remittance Certificates (FIRC).

▪ Supplies to SEZ units or developers: Requires a statement of invoices, evidence of endorsement, and details of payment. A declaration that tax has not been collected from the SEZ unit or developer is also necessary.

▪ Restrictions on zero-rated supplies: No refund of unutilised ITC or integrated tax paid on zero-rated supply of goods is allowed if such goods are subjected to export duty. The definition of "Turnover of zero-rated supply of goods" is specified for calculation purposes. Persons claiming refund of IGST paid on exports should not have received supplies on which the benefit of certain notifications (e.g., 48/2017-CT, 40/2017-CT (Rate), 41/2017-IT (Rate)) has been availed, with exceptions for capital goods under EPCG Scheme.

◦ Inverted duty structure: When the rate of tax on inputs is higher than the rate of tax on output supplies, other than nil-rated or fully exempt supplies. The refund of ITC is granted as per a specific formula: Maximum Refund Amount = {(Turnover of inverted rated supply of goods and services) x Net ITC ÷ Adjusted Total Turnover} - [{tax payable on such inverted rated supply of goods and services x (Net ITC ÷ ITC availed on inputs and input services)}]. "Net ITC" means ITC availed on inputs during the relevant period, excluding ITC claimed under certain sub-rules. The formula includes turnover of both goods and services from July 2022 onwards. There are notifications specifying goods and services for which refund of unutilised ITC under inverted duty structure is not allowed, such as certain fabrics and construction services.

◦ Deemed exports: A statement containing invoice details and other evidence as notified is required. The application can be filed by the recipient or the supplier, subject to conditions like the recipient not availing ITC. The relevant date for refund in deemed exports is the date of filing the return relating to such supplies by the supplier.

2. Other Refund Categories (Section 54(5) & (8)):

◦ Finalisation of provisional assessment: Refund arises from the final assessment order.

◦ Tax wrongly collected and paid (Section 77): Refund for transactions considered intra-State but subsequently held inter-State, or vice versa.

◦ Excess payment of tax: A statement showing details of the excess payment claim is required.

◦ Refund for unregistered persons: When a service agreement is cancelled or terminated, and the unregistered person has borne the tax incidence, they can claim a refund with specific documents, including a certificate from the supplier that tax has been paid and not adjusted via credit note.

◦ Refund for additional IGST due to upward price revision post-exports: A new sub-rule (1B) in rule 89 allows filing an application in FORM GST RFD-01 for this specific refund. Specific documentary evidence, including BRC/FIRC for additional foreign exchange remittance and a CA/Cost Accountant certificate, is required.

◦ Refund of pre-deposit: Amounts paid as pre-deposit for filing appeals under Section 107(6) or 112(8) are refundable if the appeal results in such a refund.

◦ Excess balance in electronic cash ledger (ECL): Any balance in the ECL can be claimed for refund. The two-year limitation period does not apply to this specific type of refund.

◦ Refund of integrated tax to the Government of Bhutan: The Central Government may pay refund of IGST to the Government of Bhutan for notified goods, in which case the exporter shall not receive any refund.

◦ Refunds stemming from orders: Refunds resulting from an order passed by a proper officer, appellate authority, Appellate Tribunal, or court.

Refund Processing and Orders

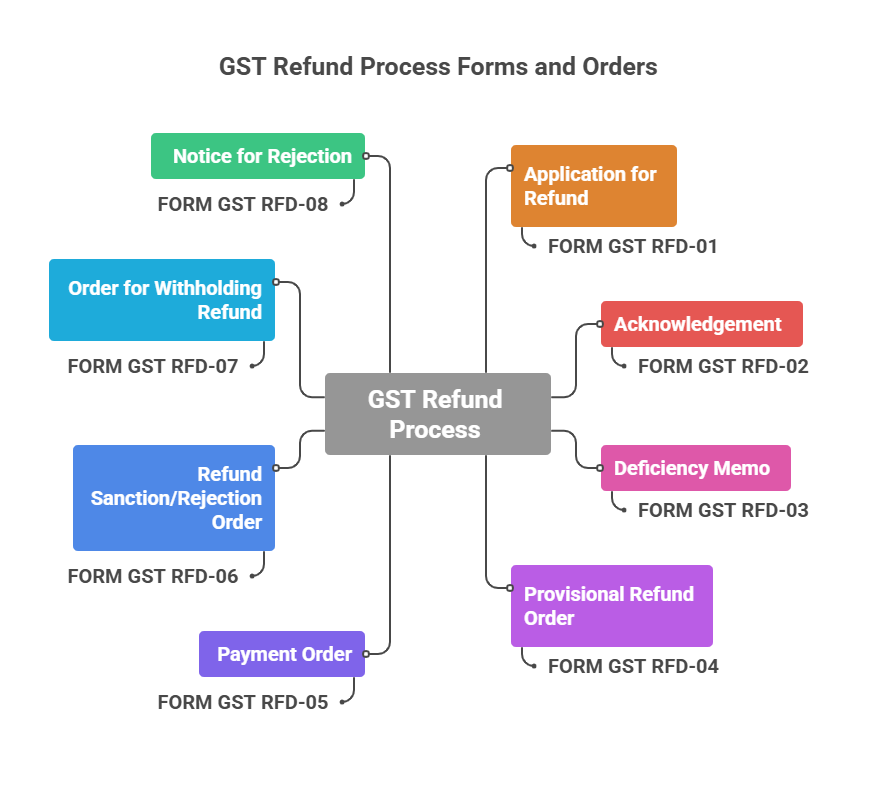

The process for refund applications involves various forms:

• FORM GST RFD-01: Application for Refund. For IGST paid on services exported out of India, the application is filed in FORM GST RFD-01.

• FORM GST RFD-02: Acknowledgement of the refund application.

• FORM GST RFD-03: Deficiency memo, communicated if deficiencies are noticed. The period from filing to deficiency communication is excluded from the two-year limitation period for a fresh refund claim.

• FORM GST RFD-04: Provisional Refund Order, for provisional refunds under Section 54(6).

• FORM GST RFD-05: Payment Order, issued for sanctioned amounts.

• FORM GST RFD-06: Refund Sanction/Rejection Order.

• FORM GST RFD-07: Order for withholding refund, stating reasons.

• FORM GST RFD-08: Notice for rejection of refund application, requiring a show cause.

If the proper officer is satisfied that the refund is due, they make an order, and the amount determined is generally credited to the Consumer Welfare Fund (CWF) under Section 57. However, Section 54(8) specifies conditions where the refundable amount is paid directly to the applicant instead of being credited to the CWF. These include refunds of tax paid on exports, unutilised ITC under Section 54(3), tax paid on supplies not provided, tax refunded under Section 77, and amounts where the applicant has not passed on the tax incidence to another person. Refunds are generally not paid if the amount is less than ₹1,000, applied per tax head separately. If a refund claim for unutilised ITC is rejected, the debited amount is re-credited to the electronic credit ledger through FORM GST PMT-03 upon appeal rejection or a written undertaking not to appeal.

Withholding of Refunds (Section 54(10) & (11))

Refunds can be withheld in specific circumstances:

• Upon a request from the jurisdictional Commissioner of central tax, State tax, or Union territory tax, if the applicant is required to pay any tax, interest, or penalty that has not been stayed by an appellate authority or court.

• If the proper officer of Customs determines that goods were exported in violation of the Customs Act, 1962.

• If any appeal or further proceeding is pending and the Commissioner believes that granting the refund would adversely affect revenue due to malfeasance or fraud, after giving an opportunity of being heard. When a refund is withheld and subsequently granted, the taxable person is entitled to interest at a notified rate.

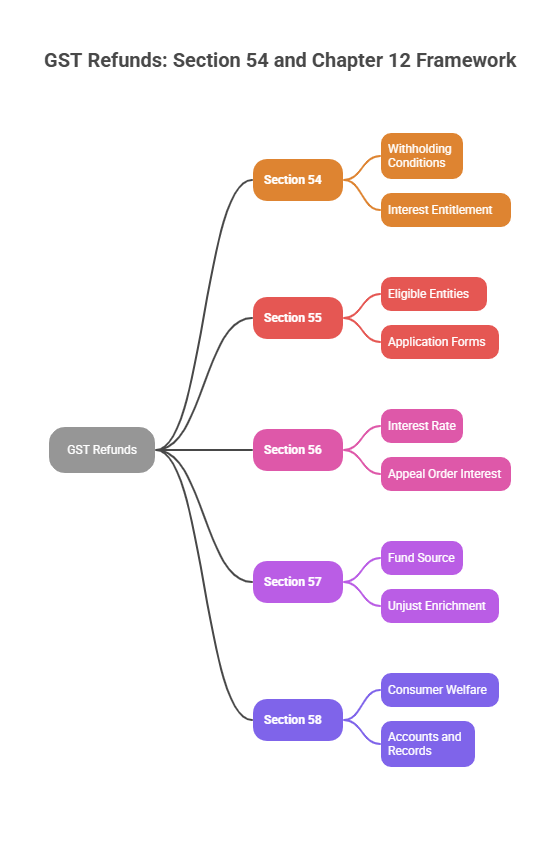

Section 54 in the Larger Context of Refunds (Sections 54-58)

Section 54 is the most extensive part of Chapter 12 and forms the operational backbone for all refund-related activities.

• Section 55: Refund in Certain Cases: This section empowers the Government to notify specific entities, such as specialised agencies of the United Nations, multilateral financial institutions, consulates, or embassies, to claim refunds on notified inward supplies. These entities apply for refunds quarterly in FORM GST RFD-10, accompanied by a statement of inward supplies in FORM GSTR-11. The Canteen Stores Department (CSD) is also eligible for a 50% refund of CGST/IGST paid on inward supplies for subsequent supply to Unit Run Canteens, with a specific application process in FORM GST RFD-10A.

• Section 56: Interest on Delayed Refunds: This section directly refers to Section 54(5). If a refund sanctioned under Section 54(5) is not paid within sixty days from the date of application, interest is payable to the applicant from the date immediately after the expiry of the sixty-day period until the date of refund. If the refund arises from an appeal order, a higher interest rate, not exceeding 9% per annum, may be applicable.

• Section 57: Consumer Welfare Fund: Section 57 mandates the constitution of the Consumer Welfare Fund (CWF), to which amounts referred to in Section 54(5) (i.e., amounts where unjust enrichment is established) are credited. Section 54 thus dictates the primary source of funds for the CWF.

• Section 58: Utilisation of Fund: This section governs the utilisation of the CWF for consumer welfare, with accounts and records maintained in consultation with the Comptroller and Auditor-General of India.

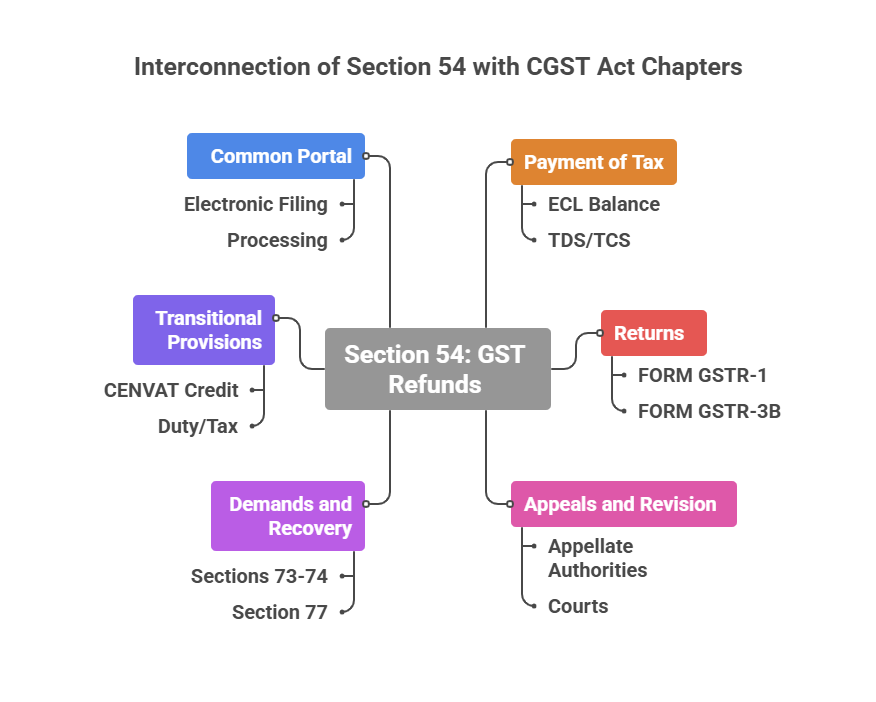

Interconnection with other CGST Act Chapters:

• Payment of Tax (Sections 49-53A): Section 54 governs the refund of any balance in the electronic cash ledger (ECL) as per Section 49(6). Refunds arising from excess or erroneous Tax Deduction at Source (TDS) (Section 51) or Tax Collection at Source (TCS) (Section 52) are also dealt with in accordance with Section 54, with the amounts credited to the deductee's/supplier's ECL.

• Returns (Sections 37-48): Accurate and timely filing of returns (like FORM GSTR-1, FORM GSTR-3B) by suppliers is essential for recipients to claim ITC and subsequently refunds.

• Appeals and Revision (Sections 107-121): Refunds often arise from orders passed by appellate authorities or courts. Pre-deposit amounts for appeals are also refundable under Section 54.

• Demands and Recovery (Sections 73-84): Erroneously granted refunds can be recovered under Sections 73 or 74. Refund claims for tax wrongfully collected (Section 77) are processed under Section 54.

• Transitional Provisions (Section 142): Claims for refunds under erstwhile laws (e.g., CENVAT credit, duty, tax) are disposed of in accordance with the provisions of those existing laws, with the refund accruing in cash. No refund of CENVAT credit is allowed if carried forward under the CGST Act.

• Common Portal: The electronic filing and processing of refunds are done through the common portal.

In essence, Section 54 provides the comprehensive legal and procedural blueprint for obtaining various refunds under GST, tightly integrated with other critical chapters and sections of the CGST Act to ensure accuracy, transparency, and timely disbursement of funds.

Matching Reversal and Reclaim of ITC | GSTR 3B Table 5 | How to Reset GSTR 3B After Submitted | Supreme court ITC to be given to the purchaser even if tax is not deposited by seller | GST Audit Procedure

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified