Interplay of Section 129 and Section 130

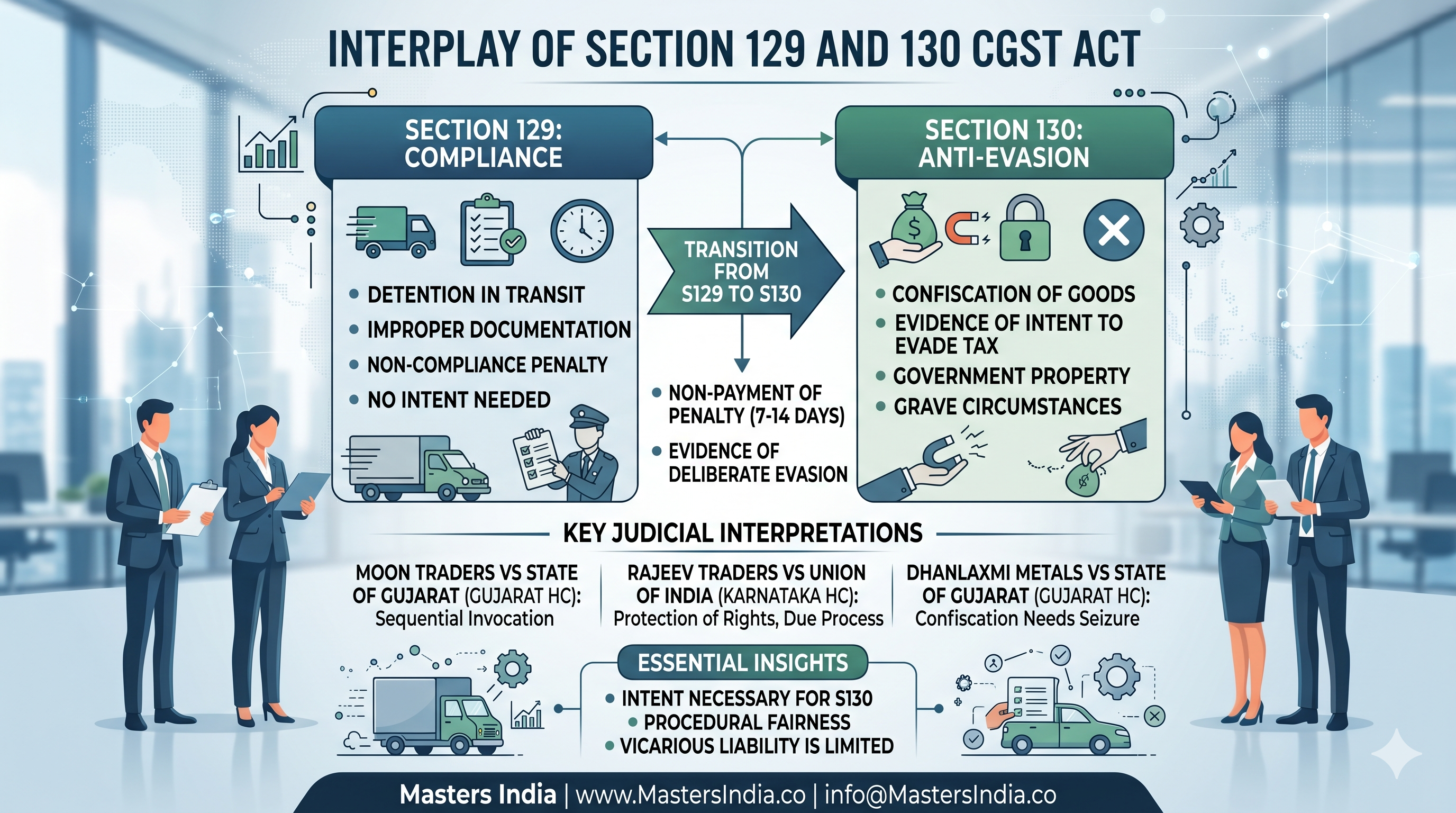

The interplay between Section 129 (detention, seizure, and release of goods in transit) and Section 130 (confiscation of goods/conveyances and levy of penalty) under the CGST Act represents one of the most litigated and intricate areas of the law.

Although both provisions address violations occurring during the transportation of goods, they differ fundamentally in their objective, the requirement of intent, and the severity of penalties imposed. Since many such disputes originate from transit-related documentation issues, businesses should also understand e-Way Bill compliance requirements under GST to minimise enforcement risks.

Distinctive Features of Sections 129 and 130

-

Section 129 (Compliance-Orientated): This section is invoked when goods are intercepted in transit due to improper documentation or discrepancies. It primarily aims to penalise non-compliance without necessitating proof of intent to evade tax.

-

Section 130 (Anti-Evasion): Applicable in grave circumstances where there is concrete evidence of an intention to evade tax. Confiscation under this section results in the goods becoming the property of the government unless a redemption fine is paid.

Transition from Section 129 to Section 130

-

Statutory Escalation: Where goods detained under Section 129 are not released owing to non-payment of tax and penalty within the prescribed period (typically 7–14 days, with shorter durations for perishable items), authorities are mandated to initiate confiscation proceedings under Section 130.

-

Evidence-Based Escalation: If, during detention under Section 129, authorities uncover evidence indicating deliberate tax evasion, they may proceed directly with Section 130 proceedings.

Judicial Interpretations of the Relationship Between Sections 129 and 130

Courts have expressed divergent views regarding whether Section 130 may be invoked independently or only subsequent to Section 129 proceedings. Such disputes frequently progress through the GST appeals and revision mechanism, where higher authorities interpret the relationship between detention and confiscation provisions.

-

Sequential Invocation (Gujarat High Court in Moon Traders): Section 130 should be resorted to only after Section 129 proceedings have been initiated and the opportunity for compliance has been afforded. Moon Traders vs State of Gujarat – Gujarat High Court [(2020) 26 TLC 139 :: (2020) 116 taxmann. com 48 (Kar.)]

-

Independent Operation (Andhra Pradesh High Court): Sections 129 and 130 function independently, permitting direct invocation of Section 130 without prior recourse to Section 129.

-

Protection of Statutory Rights (Rajeev Traders, Karnataka High Court): Detention under Section 129 confers the owner a statutory right to release goods upon compliance. Arbitrary conversion to confiscation under Section 130 without due process is impermissible. Rajeev Traders vs Union of India – Karnataka High Court – [(2022) 66 GSTL 15 (Kar.)]

-

Change in Seizure Status (Dhanlaxmi Metals, Gujarat High Court): Upon issuance of a confiscation notice under Section 130, the goods are seized under Section 67(2), superseding Section 129. Provisional release is permissible under Section 67(6) upon execution of a bond.

-

Recognition of Overlap and Need for Legislative Clarity (Synergy Fertichem, Gujarat High Court): Courts have acknowledged inconsistencies between the two sections and advocated for legislative amendments to harmonize their application. Synergy Fertichem Pvt. Ltd. vs. State of Gujarat – Gujarat High Court [2020 (33) G.S.T.L. 513 (Guj.)]

Judicial Precedents Pertaining to Section 130

1. Interplay Between Detention (Section 129) and Confiscation (Section 130)

-

Rajeev Traders vs. Union of India (Karnataka High Court): (2022) 66 GSTL 15 (Kar.) Conversion of detention under Section 129 into confiscation under Section 130 without due process infringes upon the owner’s statutory rights. Rajeev Traders vs Union of India – Karnataka High Court [(2022) 66 GSTL 15 (Kar.)]

-

M.S. Meghdoot Logistics vs. Commercial Tax Officer (Karnataka High Court): Upon discovery of mala fide intent post-detention, Section 129 proceedings may be discontinued, and Section 130 initiated. M.S. Meghdoot Logistics vs Commercial Tax Officer – Karnataka High Court (2023) 9 Centax 399 (Kar.)

-

Dhanlaxmi Metals vs. State of Gujarat (Gujarat High Court): Confiscation under Section 130 requires prior seizure; provisional release must be granted upon bond execution. Dhanlaxmi Metals vs. State of Gujarat (Gujarat High Court) (2022) 55 TLC 179 :: (2022) 114 taxmann.com 53 (Guj.)

-

Synergy Fertichem Pvt. Ltd. v. State of Gujarat (Gujarat High Court): Courts must interpret these provisions equitably, with legislative amendments recommended to resolve inconsistencies. Synergy Fertichem Pvt. Ltd. vs. State of Gujarat – Gujarat High Court [2020 (33) G.S.T.L. 513 (Guj.)]

2. Requirement of Intent to Evade Tax

-

Karnataka Traders vs. State of Gujarat (Gujarat High Court): Minor infractions such as route deviations or undervaluation alone do not justify confiscation. Karnataka Traders vs. State of Gujarat – Gujarat High Court [2022 (63) G.S.T.L. 435 (Guj.)]

-

Radha Fragrance v. Union of India (Allahabad High Court): Deliberate undervaluation to circumvent tax thresholds warrants confiscation. Radha Fragrance v. Union of India – Allahabad High Court [(2023) 4 Centax 411 (All.)]

-

Metenere Ltd. vs. Union of India (Allahabad High Court): Confiscation absent proof of intent to evade tax is arbitrary and unlawful. Metenere Ltd. vs. Union of India – Allahabad High Court [(2020) (374) E.L.T. A161 (All.)]

3. Supply Chain and Vicarious Liability

-

Shiv Enterprises vs. State of Punjab: Confiscation proceedings must bear a direct nexus to the taxpayer; vicarious liability is limited. The Supreme Court subsequently allowed adjudication to proceed prior to quashing notices. Shiv Enterprises vs. State of Punjab – Punjab & Haryana High Court [(2022) (58) G.S.T.L. 385 (P & H)]

-

Vijay Mamgain vs. State of Haryana (Punjab & Haryana High Court): Owners of conveyances cannot be compelled to pay tax and penalties on goods to obtain vehicle release; indefinite extension of vicarious liability is unconstitutional. Vijay Mamgain vs. State of Haryana – Punjab & haryana High Court [(2023) 2 Centax 39 (P&H.)]

4. Procedural Safeguards and Provisional Release

-

State Tax Officer vs. Y. Balakrishnan (Kerala High Court): Owners may pay a fine to secure provisional release during ongoing adjudication. State Tax Officer vs. Y. Balakrishnan (Kerala High Court) (2025) 86 TLC 261 :: 172 taxmann.com 800 (Ker.)

-

India Logistics And Cargo Movers vs. State of Gujarat (Gujarat High Court): Confiscation orders must be reasoned and not mechanical; arbitrary orders are subject to invalidation. India Logistics And Cargo Movers vs. State of Gujarat – Gujarat High Court [(2019) (31) G.S.T.L. 3 (Guj.)]

-

Calcutta South Transport Co. vs. State of U.P. (Allahabad High Court): Authorities may be penalised for unlawful detention and failure to release goods following quashing of confiscation orders. Calcutta South Transport Co. vs. State of U.P. – Allahabad High Court [(2022) (62) G.S.T.L. 459 (All.)]

Conclusion:

Section 129 serves as an immediate compliance checkpoint during transit, whereas Section 130 is reserved for confirmed instances of tax evasion and carries more severe penalties. Despite these distinct thresholds, the demarcation is occasionally blurred by authorities, necessitating judicial intervention to uphold taxpayers’ rights.

This analysis elucidates the distinct roles and judicial interpretations of Sections 129 and 130, underscoring the importance of procedural fairness and the need to establish intent for confiscation under Section 130.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified