The Perils of "Second Adjudication": When Tax Authorities Trespass the Limits of Law

The Perils of "Second Adjudication": When Tax Authorities Trespass the Limits of Law

For tax professionals, CFOs, and finance leaders, few things are as frustrating as a tax dispute that refuses to die. You meticulously respond to a notice, navigate a rigorous scrutiny process, and finally secure a hard-earned refund order. You breathe a sigh of relief, believing the matter is settled. Then, months later, a fresh Show Cause Notice (SCN) lands on your desk, attempting to re-adjudicate the exact same issue.

This growing trend of proper officers bypassing established legal routes to conduct a "second adjudication" is not just administratively aggressive—it is fundamentally illegal. When authorities bypass the principles of natural justice and statutory limitations, their demands rest on a house of cards. Below, we break down the critical legal vulnerabilities of such overreaches and how businesses can robustly defend against them.

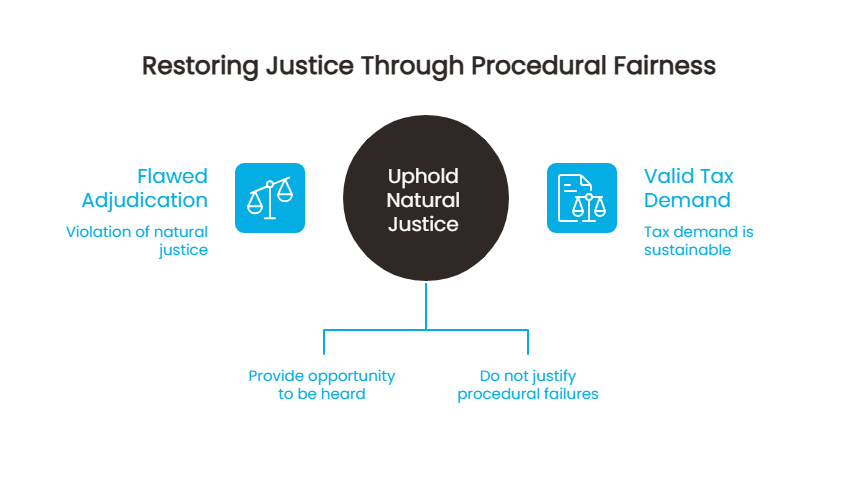

1. The Death Blow: Violation of the Principles of Natural Justice

Any adjudication concluded in violation of the principles of natural justice is fundamentally flawed from its inception. It is an established principle of civil law that procedural fairness is not a mere formality, but the very soul of justice.

The Impact of Procedural Failure

-

Total Invalidation: When an authority fails to provide a fair hearing or ignores natural justice, the error cannot be cured by subsequent justifications.

-

Fatal to the Demand: For this reason alone, the entire tax demand becomes unsustainable and is liable to be completely set aside.

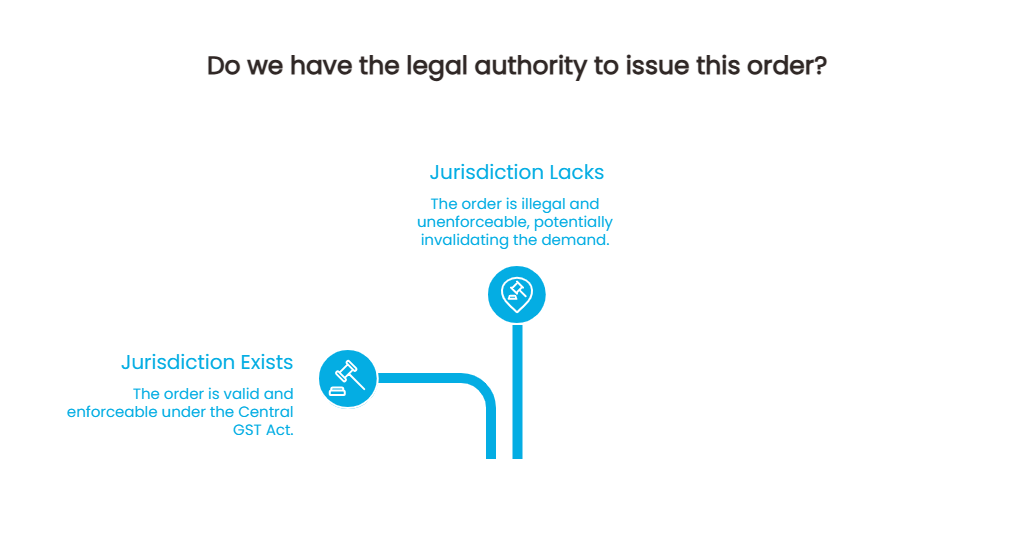

2. A Question of Jurisdiction: Acting Without Power

An order is only as valid as the statutory authority of the officer who signs it. If an underlying proceeding is initiated without the explicit jurisdiction of law, the resulting order is entirely illegal.

Why Jurisdiction Matters

-

No Inherent Powers: Tax authorities do not possess inherent powers; they only possess powers expressly granted by the Central GST Act.

-

The Consequence: If the authority exercises power outside its legal boundary, the entire demand falls apart.

3. The Myth of the "Second Adjudication"

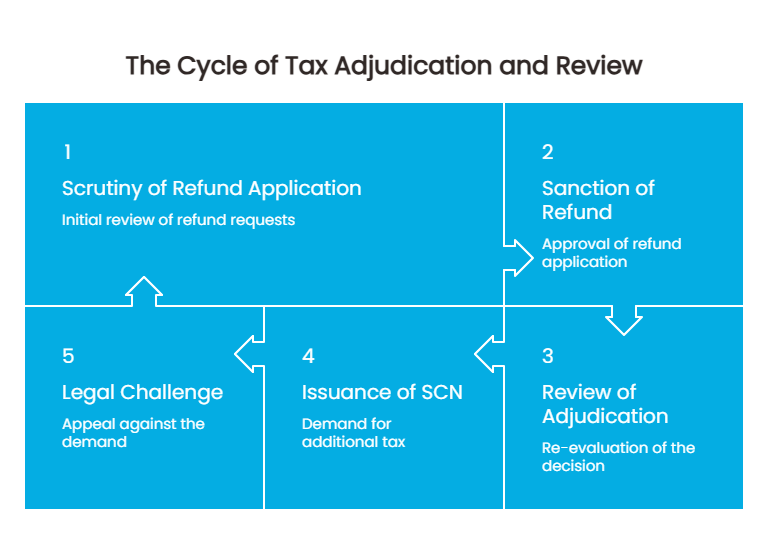

One of the most glaring errors committed by the revenue department is attempting a second round of scrutiny under the guise of a fresh notice, after a refund application has already been thoroughly examined, noticed, and adjudicated.

The Statutory Workflow vs. Review

The Central GST Act provides structured mechanisms for officers to unearth discrepancies before raising a demand. Proper Officers are explicitly empowered to undertake specific paths:

-

Scrutiny of refund applications under Section 54.

-

Scrutiny of returns under Section 61.

-

Audit under Section 65 or inquiry under Section 67.

-

Only after these stages can they issue a notice of demand under Chapter XV.

The Limitation of Review Powers

Once a Jurisdictional Proper Officer scrutinizes a refund application via Form GST RFD-08 and sanctions it via Form GST RFD-06, they cannot simply change their mind without new material facts. If no new information has come to light, re-considering a concluded adjudication is an unauthorized review.

"To issue Impugned SCN, is gross misapplication of law and the lawful course of action would have been that a departmental appeal under section 107(3) of Central GST Act be filed against the refund sanctioned..."

Bypassing Limitation Periods

When the department misses the strict limitation window to file an appeal under Section 107(2), or even the condonable period under Section 107(4), issuing a fresh SCN to recover the amount is a malicious detour. It amounts to exercising a power of review that simply does not exist in the law. Consequently, the demand is legally untenable.

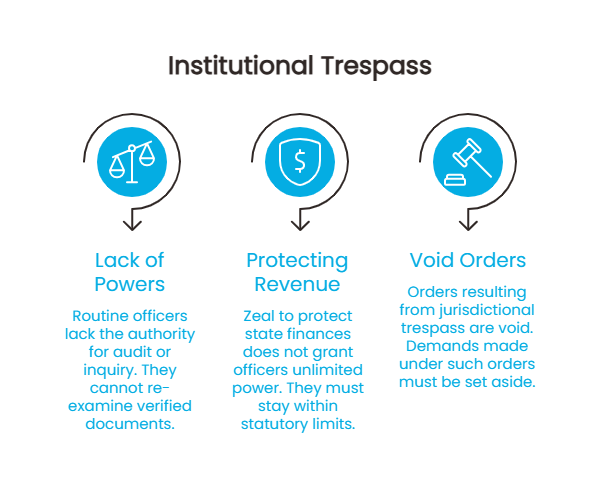

4. Institutional Trespass: Merging Distinct Officer Roles

The law deliberately separates administrative and investigative functions to ensure checks and balances. A jurisdictional officer handling routine matters cannot arbitrarily assume the specialized powers of an auditor or investigator.

Encroaching on Specialized Territory

-

Lack of Section 65/67 Powers: A routine jurisdictional Proper Officer is fundamentally not the designated Proper Officer under Section 65 (Audit) or Section 67 (Inquiry) to re-examine the correctness of documents already verified during the RFD-06 issuance.

-

Protecting Revenue Within the Law: Zeal to protect the state's financial interest does not give an officer a license to cross statutory boundaries.

"Passion to protects interests of Revenue does not permit exercise of non-existent powers or trespass into jurisdiction vested in some other Officers."

When an officer trespasses into another's statutory jurisdiction, the resulting order is void, and the demand must be set aside.

5. The Omission of Composite Notices

The department is strictly bound by its own circulars and guidelines, which are designed to prevent piecemeal litigation.

The Mandate of Circular No. 125

Under paragraph 20(b) of Circular No. 125/44/2019-GST, if the revenue has any grievance regarding the admissibility of the input tax credit (ITC) balance during a refund claim, it must issue a composite notice of demand invoking Section 73 or Section 74.

-

Vested Rights of the Taxpayer: When the officer chooses not to issue a composite notice, it creates a vested legal right for the appellant. It implies the Revenue has no grievances regarding the remaining Electronic Credit Ledger balance.

-

The Legality of Ex-Post Facto Changes: Any grievance is strictly confined to the grounds originally raised in the RFD-08. Attempting to review those grounds after passing the RFD-06 order is an impermissible, ex-post facto amendment of the original notice.

6. The Inward Supply Conflict: Confusing Commercial Realities

Tax demands often crumble when the department misinterprets the factual matrix of a business's supply chain, particularly regarding "own account" consumption versus outward business supplies.

Commercial Factual Accuracy

-

Admissible ITC: Inward supplies acquired in the ordinary course of business furtherance are completely admissible as ITC. They cannot be blocked under Section 17(5)(c) if they are directly supplied to customers.

-

The "Own Account" Distinction: The restriction on works contract services only applies if they are utilized on "own account" and are entirely disconnected from making outward supplies.

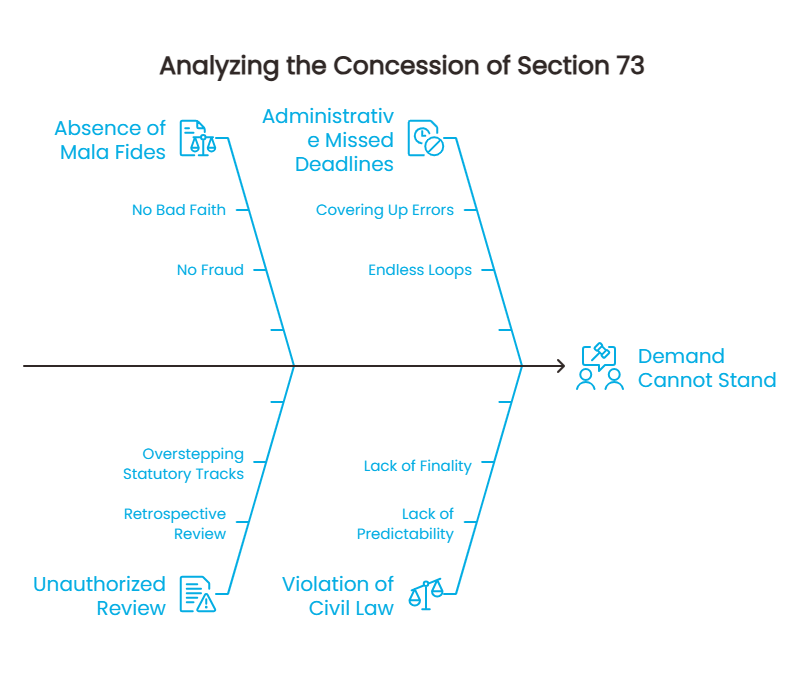

The Concession of Section 73

When the department issues an SCN under Section 73 rather than Section 74, it explicitly concedes the absence of mala fides (bad faith) or fraud on the part of the taxpayer. This proves that the new demand is not based on uncovered deception, but is merely an unauthorised, retrospective review of facts that were already fully disclosed. For this reason, the demand cannot stand.

The Takeaway

The architecture of tax law is built on predictability and finality. When proper officers attempt to convert routine procedures into endless loops of re-adjudication—often to cover up administrative missed deadlines—they violate the core tenets of civil law and natural justice.

As finance leaders and tax professionals, recognising these procedural boundaries is your strongest shield. When a tax authority oversteps its statutory tracks, it isn't just an administrative inconvenience—it is a fatal legal error.

A final thought to ponder: If the state is permitted to bypass its own limitation periods and structural boundaries through administrative re-adjudication, can a taxpayer ever truly achieve finality in their tax assessments?

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified