WHETHER MANDATORY PRE-DEPOSIT CAN BE WAIVED OR REDUCED UNDER INDIRECT TAX LAWS

INTRODUCTION

The right to file an appeal is an important statutory remedy. However, under indirect tax laws, this right is not completely unconditional.

Before an appeal is entertained, the Appellant is required to deposit a prescribed percentage of the disputed tax, duty or penalty. This is commonly known as a mandatory pre-deposit and forms an important part of the GST appeals and revision framework under the law.

In simple words, 'pre-deposit' means:

A compulsory deposit of a specified percentage of disputed demand before filing or maintaining an appeal before the Appellate Authority or Appellate Tribunal.

The object is two-fold:

-

to discourage frivolous appeals;

-

to secure partial revenue during the pendency of litigation.

At the same time, the provision can create genuine difficulty in cases where the assessee is facing financial hardship. The key question, therefore, is:

Can the mandatory pre-deposit be waived, reduced or substituted by security under indirect tax laws?

The judicial trend shows that the answer is generally No, unless the statute itself permits such waiver.

STATUTORY POSITION UNDER CUSTOMS LAW

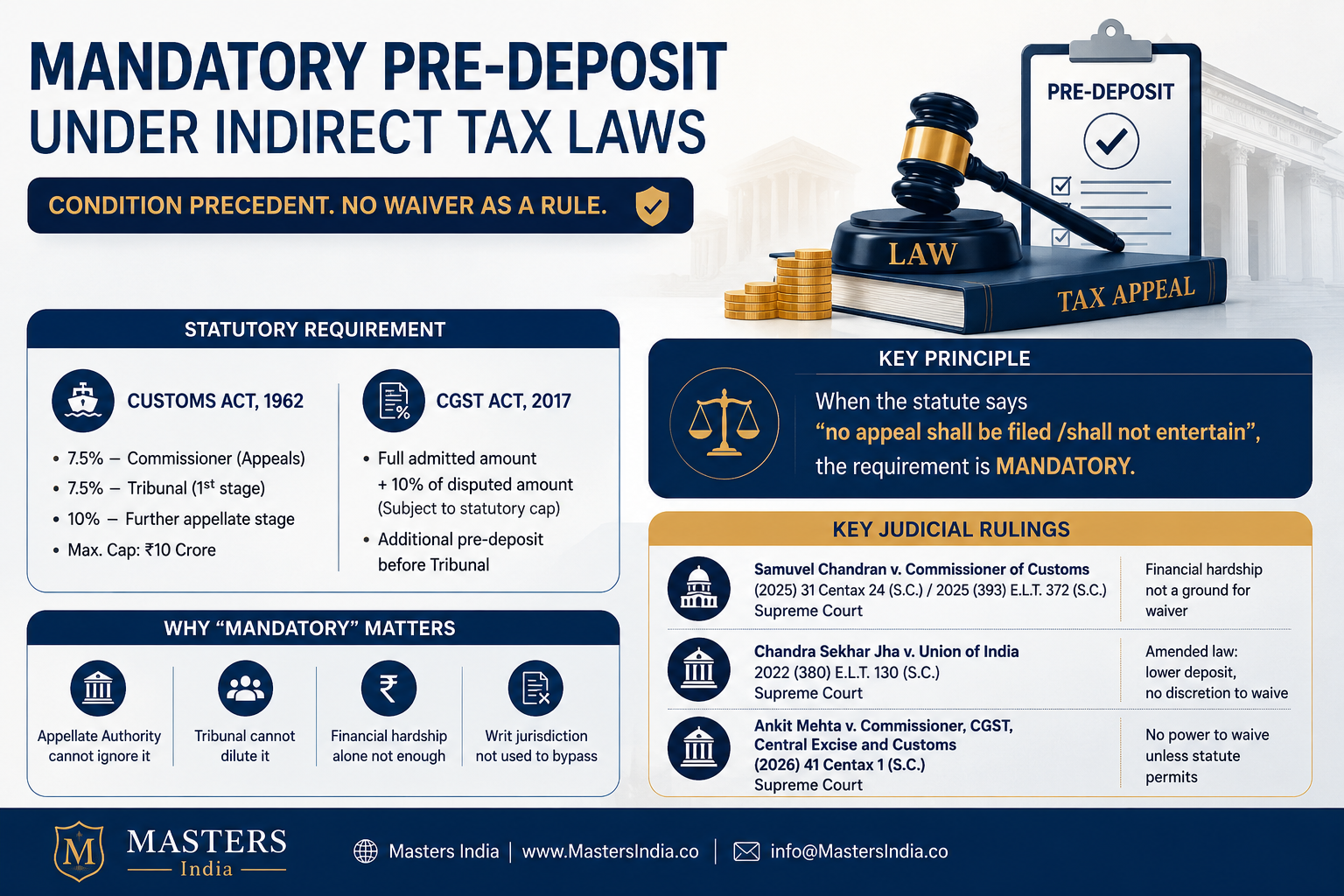

Under Section 129E of the Customs Act, 1962, the appeal cannot be entertained unless the Appellant deposits the prescribed percentage of duty or penalty.

Broadly:

-

7.5% pre-deposit is required for appeal before Commissioner (Appeals);

-

7.5% is required for appeal before Tribunal at first stage;

-

10% is required at further appellate stage;

-

the maximum pre-deposit is capped at ₹10 crore.

The amended law made a clear departure from the earlier regime. Earlier, appellate authorities had discretion to waive or dispense with pre-deposit in appropriate cases. After amendment, such discretion has been taken away.

STATUTORY POSITION UNDER GST LAW

Under Section 107(6) of the CGST Act, 2017, no appeal can be filed before the Appellate Authority unless the Appellant pays:

-

the full admitted amount of tax, interest, fine, fee and penalty; and

-

10% of the remaining disputed tax, subject to the statutory monetary cap.

Further, where the order demands only a penalty without a tax demand, the Appellant is required to deposit 10% of such penalty.

For appeal before the GST Appellate Tribunal, Section 112(8) requires an additional pre-deposit over and above the amount paid at the first appellate stage.

Thus, under GST also, a pre-deposit is treated as a condition precedent for filing and maintaining an appeal.

WHY THE WORD “MANDATORY” MATTERS

The language used in the statute is very important.

Expressions like “no appeal shall be filed” or “shall not entertain any appeal” show that the requirement is not directory. It is mandatory.

This means:

-

the Appellate Authority cannot ignore it;

-

the Tribunal cannot dilute it;

-

financial hardship alone may not be enough;

-

writ jurisdiction is also not normally used to bypass it.

The courts have repeatedly held that when the legislature has prescribed a fixed percentage, neither the Appellate Authority nor the High Court should rewrite the statute.

IMPORTANT JUDICIAL PRINCIPLES

1. Financial hardship is generally not enough

In Samuvel Chandran v. Commissioner of Customs, (2025) 31 Centax 23 (Bom.), decided by the Bombay High Court in Writ Petition (L) No. 29982 of 2024 on 24.10.2024, the assessee challenged the adjudication order and also sought a waiver of the mandatory pre-deposit. The Court held that the requirement of 7.5% pre-deposit under Section 129E of the Customs Act, 1962 could not be waived merely because the assessee pleaded inability to pay.

The Court further held that where statutory appeal was available, writ jurisdiction under Article 226 of the Constitution of India could not be used to bypass the statutory pre-deposit condition.

The matter reached the Supreme Court in Samuvel Chandran v. Commissioner of Customs, (2025) 31 Centax 24 (S.C.) / 2025 (393) E.L.T. 372 (S.C.), decided in Special Leave Petition (Civil) Diary No. 824 of 2025 on 04.04.2025. The Supreme Court dismissed the SLP and refused to interfere with the Bombay High Court’s view.

The principle is clear:

If the statute requires pre-deposit, the appeal must comply with that condition.

Mere inability to pay does not automatically create a right to waiver.

2. Earlier discretionary regime is no longer applicable

In Chandra Sekhar Jha v. Union of India, 2022 (380) E.L.T. 130 (S.C.), decided by the Supreme Court in Civil Appeal No. 1566 of 2022 on 28.02.2022, the Court examined the effect of substituted Section 129E of the Customs Act, 1962.

The assessee argued that since the case related to a period before substitution of Section 129E, the earlier discretionary regime should apply. The Supreme Court rejected this argument.

The Court explained that under the old provision, the appellant was required to deposit the full amount, but the appellate authority had discretion to waive or reduce the pre-deposit. Under the substituted provision, the pre-deposit was reduced to 7.5% or 10%, but the discretion to waive was taken away.

The Supreme Court held that the legislative intention was clear. Once the new provision applies, the Appellant cannot claim the benefit of the old waiver mechanism.

This judgement is important because it explains the policy shift:

-

earlier law: higher deposit with discretion to waive;

-

amended law: lower fixed deposit without discretion to waive.

Thus, reduced pre-deposit came with stricter statutory compliance.

3. Tribunal or Commissioner (Appeals) cannot waive pre-deposit unless statute permits

In Ankit Mehta v. Commissioner, CGST, Central Excise and Customs, (2026) 41 Centax 1 (S.C.), decided by the Supreme Court in Petition for Special Leave to Appeal No. 13375 of 2019 with connected SLPs on 24.02.2026, the assessee failed to deposit the mandatory pre-deposit and pleaded financial hardship.

The Madhya Pradesh High Court had earlier upheld the dismissal of the appeal for non-compliance with the mandatory pre-deposit. The Supreme Court refused to interfere where no provision under the Customs Act empowered the Tribunal or Commissioner (Appeals) to waive or reduce such mandatory pre-deposit.

The ratio is very practical:

Hardship may be genuine, but power must come from the statute.

If the law does not give discretion, the authority cannot create it.

4. Writ jurisdiction cannot normally override statutory pre-deposit

In Mahesh Kumar Agarwala v. Union of India, (2026) 41 Centax 282 (Gau.), decided by the Gauhati High Court in W.P. (C) No. 1359 of 2026 on 09.03.2026, the assessee challenged an order passed under Section 74 of the CGST Act, 2017 / Assam GST Act, 2017. The demand relates to alleged wrongful availment of ITC on the basis of misstatements, fake invoices, and absence of e-way bills.

The assessee sought permission to file an appeal without the mandatory pre-deposit of 10% or, alternatively, to substitute the deposit with security or a bond.

The High Court held that:

-

writ jurisdiction cannot be invoked to bypass mandatory pre-deposit under Section 107;

-

adequacy or sufficiency of reasons in the adjudication order cannot be reappraised in certiorari jurisdiction unless reasons are perverse or mala fide;

-

no extraordinary hardship or exceptional circumstance was demonstrated.

Accordingly, the prayer for waiver or substitution of pre-deposit was rejected.

This judgement reinforces one point:

Statutory pre-deposit cannot be replaced by security unless the law permits it.

LIMITED RELIEF IN SPECIAL GST TRIBUNAL SITUATIONS

There have been cases where courts gave limited protection due to non-constitution of the GST Appellate Tribunal.

In Sonali Event Pvt. Ltd. v. Union of India, (2024) 25 Centax 189 (Pat.), decided by the Patna High Court in Civil Writ Jurisdiction Case No. 16303 of 2024 on 24.10.2024, the issue arose because the GST Appellate Tribunal had not been constituted.

The amendment had reduced the tribunal-stage pre-deposit under Section 112 of the CGST Act, 2017, from 20% to 10%, but the amendment was to operate from a future date. Since the Tribunal was not functional, filing an appeal was not practically possible.

In these peculiar facts, the Court directed that on payment of 10% of the disputed tax amount, the Assessee would be entitled to stay of recovery till the Tribunal was constituted and an appeal was filed. The Court also directed the release of the bank attachment if the required amount was paid, which aligns with established legal remedies for removing GST bank account attachments after statutory compliance.

This was not a waiver of pre-deposit. It was a practical interim protection due to institutional difficulty.

This distinction is important.

A court may protect the assessee from coercive recovery in a special situation, but that does not mean the statutory requirement of pre-deposit is erased.

NO GENERAL RIGHT TO WAIVER UNDER GST

In I-Karb E-Sol Pvt. Ltd. v. Joint Commissioner of State Tax, Behala Charge, (2025) 31 Centax 418 (Cal.), decided by the Calcutta High Court in W.P.A. No. 2160 of 2025 on 11.06.2025, the assessee challenged an order passed under Section 73 of the CGST Act, 2017 / WBGST Act, 2017.

The assessee filed an appeal before the First Appellate Authority but did not make the mandatory pre-deposit under Section 107(6). The reason given was financial catastrophe, huge liabilities and financial crunch.

The Appellate Authority refused to entertain the appeal. The Assessee then approached the High Court.

The Calcutta High Court held that the Appellate Authority could not have accepted the appeal unless the assessee had paid:

-

admitted tax, interest, fine and penalty; and

-

10% of the remaining tax in dispute, subject to the statutory cap.

The Court further held that if the mandatory pre-deposit was not complied with, there was no scope for the Appellate Authority to entertain the appeal.

The legal position emerging from this judgement is:

-

financial crunch is not a substitute for statutory compliance;

-

appeal cannot be entertained without pre-deposit;

-

Appellate Authority is bound by the statute.

WHEN WRIT PETITION MAY NOT HELP

Many assessees try to approach the High Court when they are unable to make a pre-deposit. However, writ remedy has its own limits.

A writ court generally examines:

-

whether there is a violation of natural justice;

-

whether the authority lacked jurisdiction;

-

whether the order is perverse;

-

whether the statutory remedy is ineffective;

-

whether exceptional facts exist.

But where the dispute is capable of being examined on appeal and the only difficulty is pre-deposit, courts are slow to interfere.

In Digambar Road Lines v. Commissioner (Appeals), GST, Central Excise & Customs, Bhubaneswar, (2025) 36 Centax 398 (Ori.) / 2025 (104) G.S.T.L. 344 (Ori.), decided by the Orissa High Court in W.P. (C) No. 30271 of 2025 on 11.11.2025, the assessee challenged the appellate order.

The Appellate Authority had dismissed the appeal on two grounds:

-

non-fulfilment of mandatory pre-deposit under Section 107(6) of the CGST/OGST Act, 2017; and

-

findings on merits.

The Orissa High Court held that once the appellate authority had also decided the matter on merits, writ interference was not justified unless the findings were perverse, irrational, unreasonable or contrary to law.

The Court also observed that writ jurisdiction cannot be invoked merely to examine whether the decision is correct. The Court must examine the decision-making process, not sit as a regular appellate forum.

This judgement is a reminder that a writ petition is not a shortcut for a statutory appeal.

SPECIAL CASE WHERE THE QUESTION WAS LEFT OPEN

In Aarn Iron and Steel Pvt. Ltd. v. GST Officer, Ward 64, New Delhi, (2025) 26 Centax 104 (Del.) / 2025 (94) G.S.T.L. 189 (Del.), decided by the Delhi High Court in W.P. (C) No. 17631 of 2024 on 24.12.2024, the assessee sought a waiver of 10% pre-deposit for filing an appeal under Section 107 of the CGST Act, 2017 / Delhi GST Act, 2017.

The demand related to the alleged excess claim of ITC. The assessee pleaded lack of financial means.

The Delhi High Court did not finally decide the larger question of whether exemption, waiver or reduction could be granted in respect of GST demands. The Court permitted the assessee, as a unique case, to file an appeal within the time granted. The Court specifically observed that the order would not act as a precedent and the questions of law were left open.

Therefore, this judgement should be used carefully. It does not lay down a general rule that pre-deposit can be waived.

PRACTICAL TIPS FOR TAX PROFESSIONALS

Before filing an appeal, professionals should keep the following points in mind:

1. Calculate pre-deposit correctly

Check whether the dispute relates to:

-

tax;

-

penalty;

-

tax and penalty;

-

admitted amount;

-

disputed amount.

Pre-deposit is usually calculated on the disputed tax or penalty, not on the entire demand in every case.

2. Pay admitted dues separately

The admitted amount must be paid in full. Pre-deposit applies only to the remaining disputed amount.

3. Do not wait till the last date

Payment issues, portal errors and challan mismatches can create practical difficulty. Pre-deposit should be planned well before the appeal limitation expires.

4. Preserve evidence of payment

Keep the challan, payment reference, appeal acknowledgement and screenshots safely.

5. Use writ remedy carefully

A writ petition may be considered only where there is a strong jurisdictional error, violation of natural justice or exceptional circumstance. It should not be used merely as a substitute for a pre-deposit.

6. Do not advise waiver casually

Clients often ask whether pre-deposit can be waived due to financial hardship. The safer advice is:

Waiver is not ordinarily available unless the statute itself permits it or the case involves extraordinary circumstances.

CONCLUSION

In tax litigation, law rewards preparation more than sympathy.

A demand order may be wrong. The facts may be strong. The assessee may ultimately succeed. But the door of appeal opens only when the statutory key is used.

Mandatory pre-deposit is that key.

A wise taxpayer should not treat pre-deposit as a burden to be avoided. It should be treated as the first disciplined step towards serious litigation. Courts may protect rights, but they do not normally rescue a person from a condition clearly written in law.

The practical wisdom is this:

Fight the demand on merits, but respect the procedure. Challenge the order with courage, but enter the appellate forum with compliance. In tax law, the strongest case can suffer if the first statutory step is missed. Litigation is not won only by arguments; it is also won by timing, documentation, discipline and obedience to procedure.

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified