One Company, Many Identities: 5 Vital Lessons for Navigating GST Audits with Multiple GSTINs

One Company, Many Identities: 5 Vital Lessons for Navigating GST Audits with Multiple GSTINs

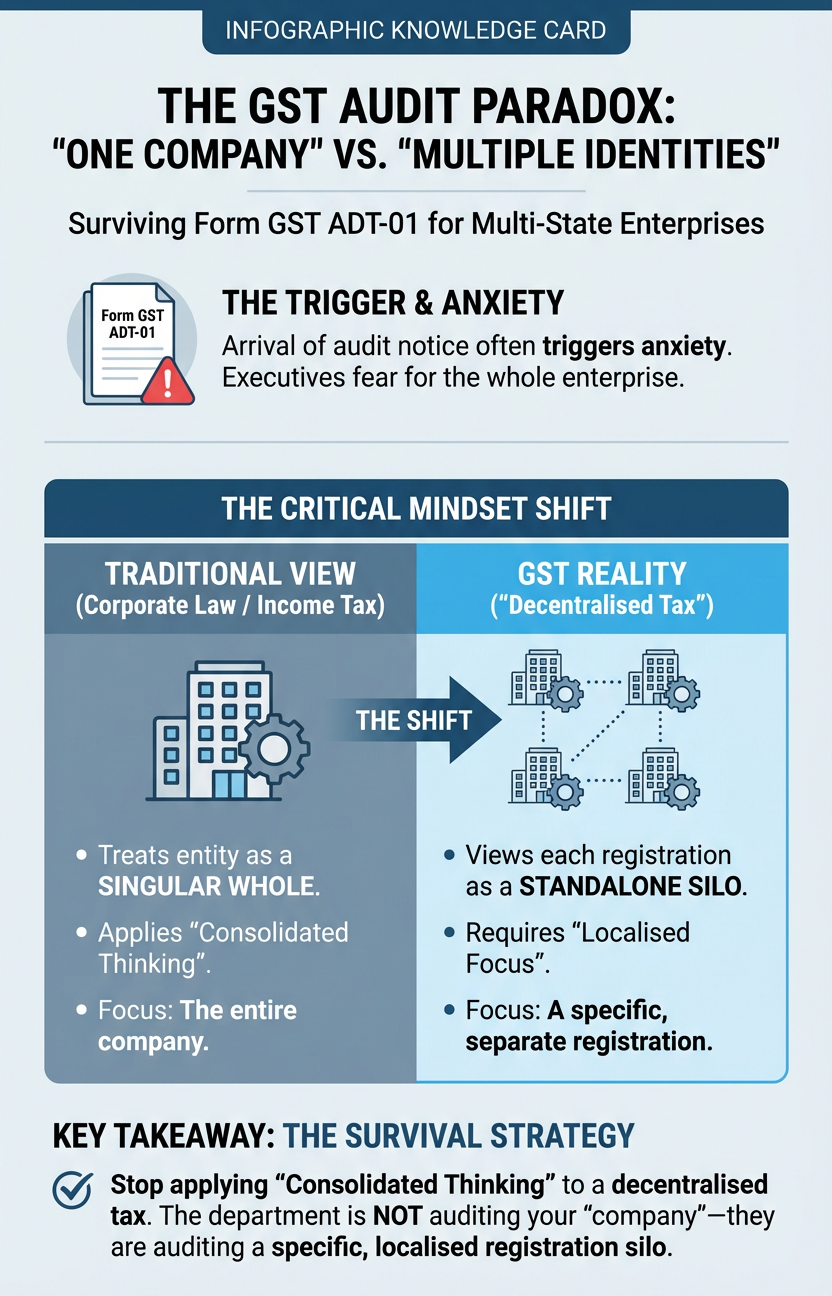

The Audit Letter Anxiety

For the leadership of a multi-state enterprise, few documents carry as much weight as Form GST ADT-01. The arrival of an audit notice often triggers a predictable wave of anxiety, yet many executives fail to realise that for a multi-location business, the department is not auditing a "company" but a specific, localised registration. Understanding the GST audit process becomes especially important for businesses operating across multiple GST registrations and jurisdictions.

As a strategic auditor, I have seen even the most robust corporations stumble because they applied "consolidated thinking" to a "decentralised tax". While corporate law and income tax treat your entity as a singular whole, GST views each of your registrations as a standalone silo. This article is the definitive source of wisdom for surviving the shift from the "one company" mindset to the "multiple identity" reality.

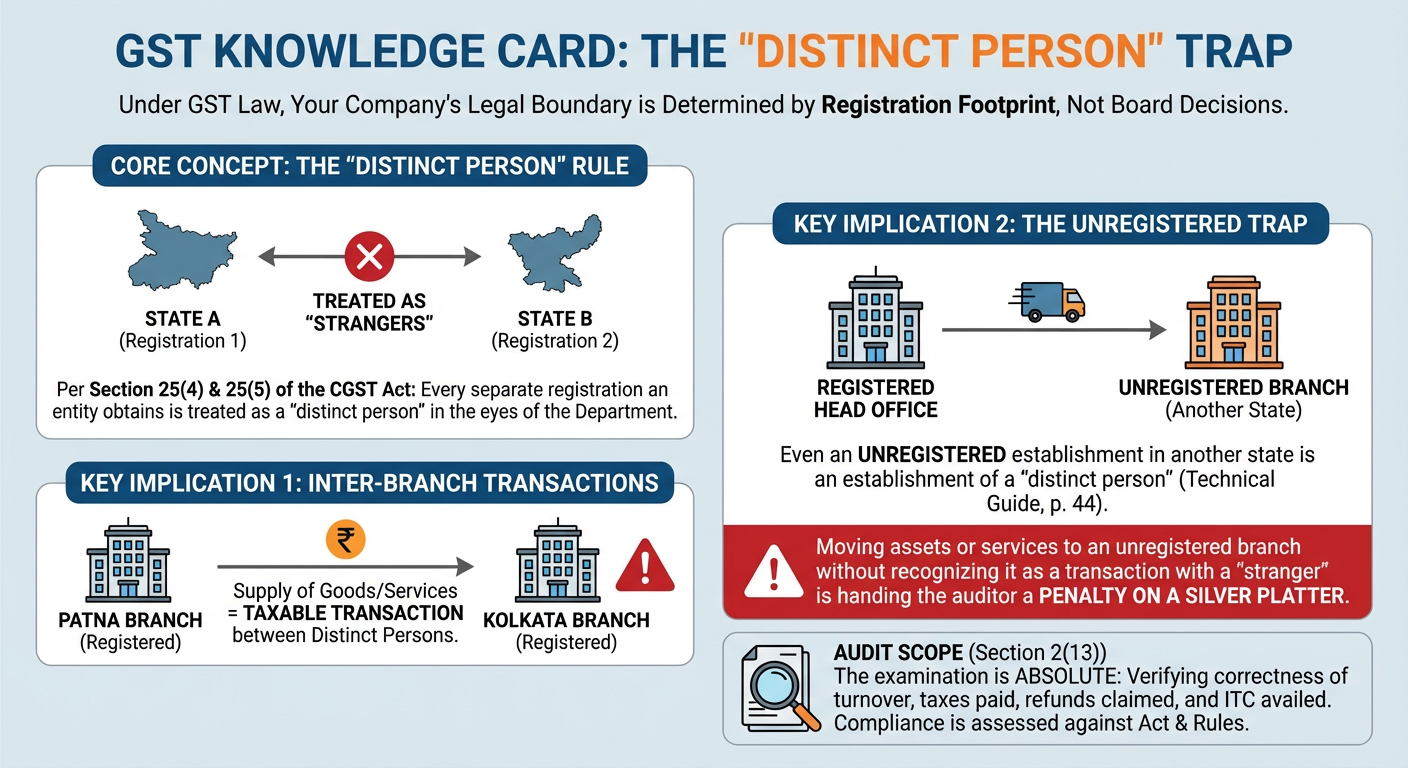

Takeaway 1: You are a "Distinct Person" (Even to Yourself)

Under GST law, your company’s legal boundary is not determined by your board of directors but by the geographical footprint of your registrations. Per Sections 25(4) and 25(5) of the CGST Act, every registration an entity obtains is treated as a "distinct person".

This is the ultimate trap for business owners accustomed to consolidated reporting. In the eyes of the Department, a branch in Patna is a complete stranger to a branch in Kolkata. Even an unregistered establishment in another state is considered an establishment of a distinct person. If you move assets or services to an unregistered branch without recognising it as a transaction with a "stranger", you are effectively handing the auditor a penalty on a silver platter. The scope of their examination is absolute:

"Audit" means the examination of records, returns and other documents maintained or furnished by the registered person under this Act or the rules made thereunder or under any other law for the time being in force to verify the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed and to assess his compliance with the provisions of this Act or the rules made thereunder. (Section 2(13))

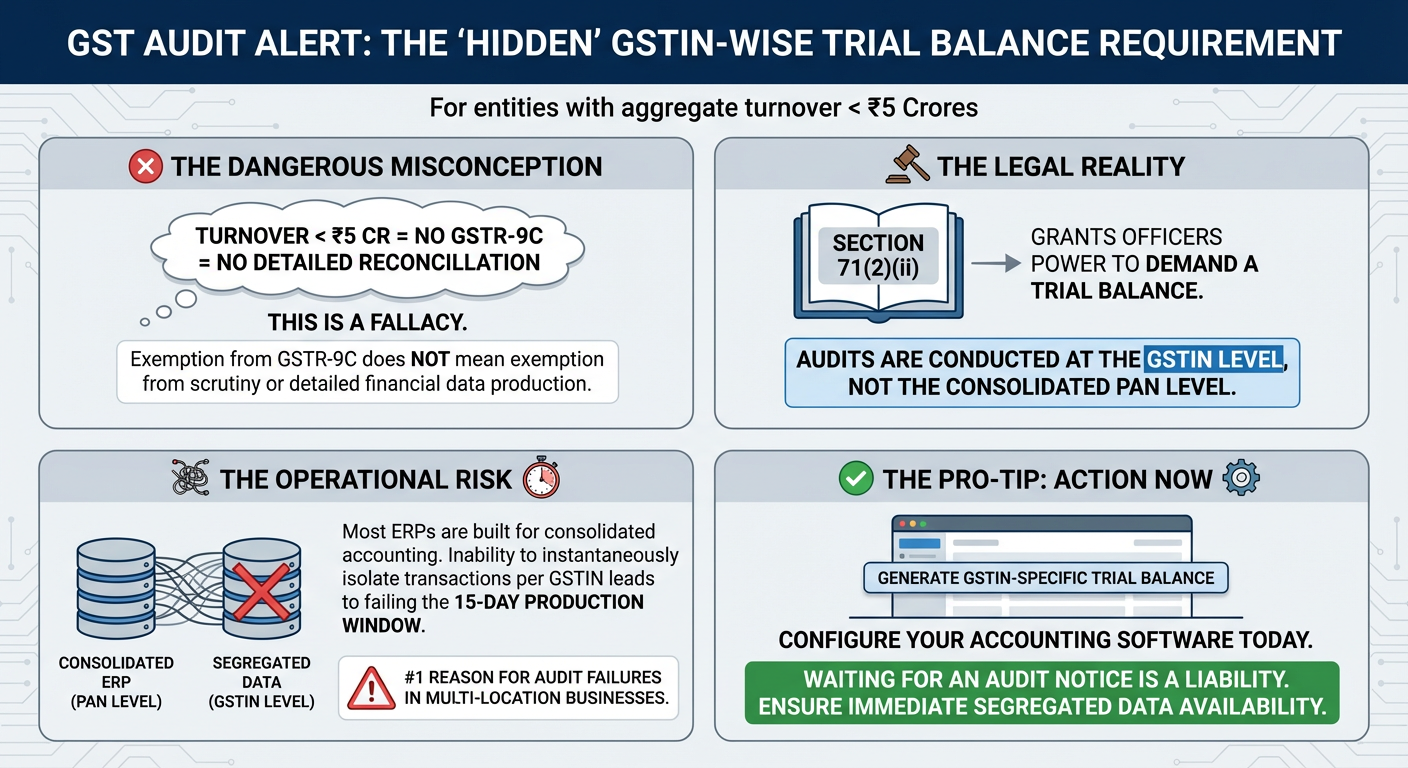

Takeaway 2: The "Hidden" Requirement of GSTIN-wise Trial Balances

A dangerous misconception persists among entities with an aggregate turnover below ₹5 crore: that because they are exempt from filing GSTR-9C, they are exempt from detailed financial reconciliation. This is a fallacy. While Section 35 (Accounts and Records) does not explicitly name a "trial balance", Section 71(2)(ii) grants officers the power to demand it.

Most ERP systems are built for consolidated accounting. However, an audit is conducted at the GSTIN level, not the PAN level. If your software cannot instantaneously isolate every transaction, expense, and revenue stream for a specific registration, you will fail the 15-day production window. This is the #1 reason for audit failures in multi-location businesses—the inability to produce a localised financial snapshot from a consolidated database.

Pro-Tip: Configure your accounting software to generate a GSTIN-specific Trial Balance today. Waiting for an audit notice to begin segregating your financial data is not a strategy; it is a liability. Audit officers will use Section 71(2)(ii) to expose this compliance gap in your IT infrastructure.

Takeaway 3: The Danger of "Invisible" Stock Transfers

In a single-unit entity, moving inventory from a warehouse to a showroom is an internal transfer. In the multi-GSTIN world, per Schedule I, this is a "taxable supply" even without consideration.

Auditors are trained to hunt for "revenue netting with expenses". This occurs when internal transfers are treated as mere cost centres rather than revenue-generating supplies. A common example involves samples. Many companies believe samples are "free", but when sent between distinct persons, they are taxable supplies requiring a formal tax invoice. Failing to issue an invoice for a laptop or a batch of samples moving between offices is an "invisible" supply that auditors will make visible and expensive. Such inter-state stock movements must also comply with e-way bill requirements under GST to avoid disputes during audits and inspections.

"A tax invoice shall be raised when the goods move permanently, along with an employee, from one state to another... Sending samples from one state to another between distinct persons would be a supply without consideration and will be covered under Schedule I and requires raising a tax invoice."

![]()

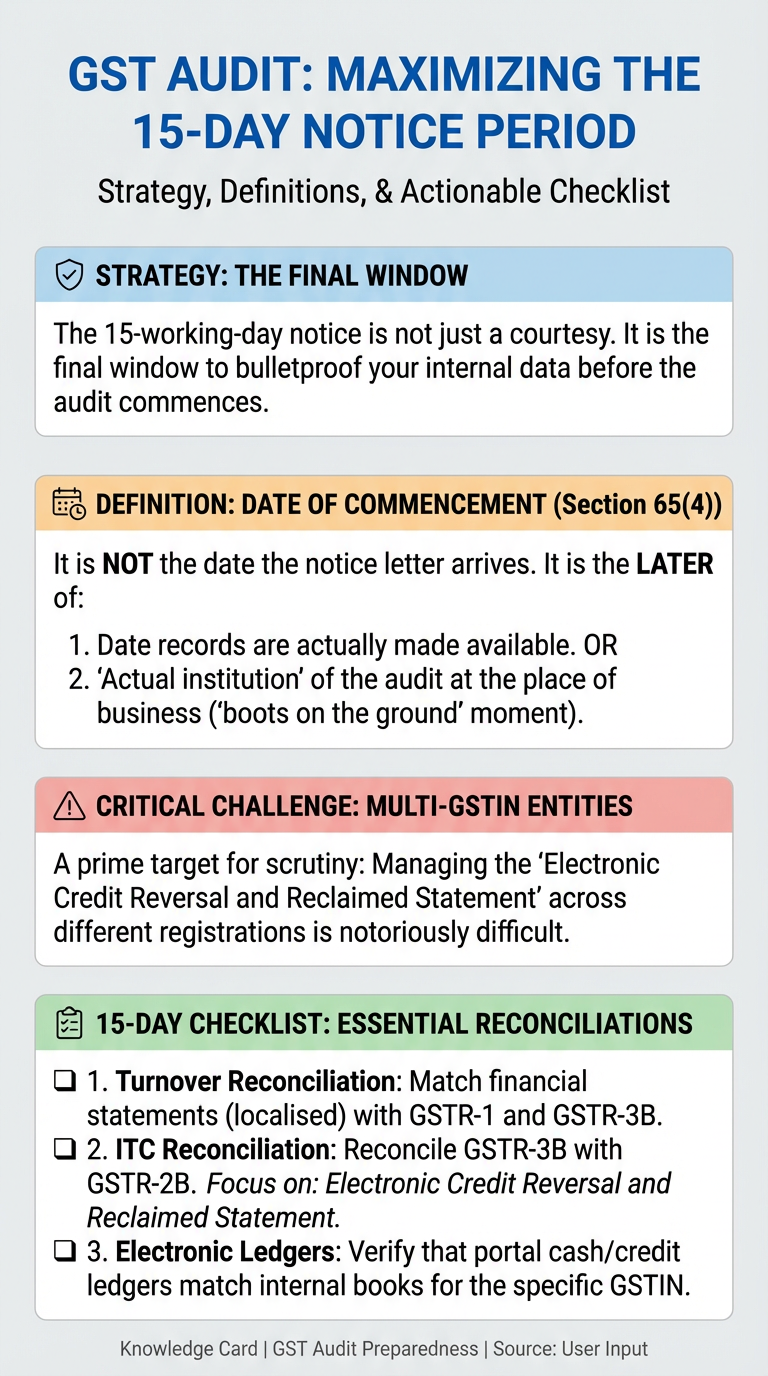

Takeaway 4: The 15-Day Countdown and the Power of Prior Intimation

The law grants you a 15-working-day notice period before an audit commences. Strategic auditors view this not as a courtesy, but as the final window to ensure your internal data is bulletproof.

You must understand the definition of the "Date of Commencement" under Section 65(4). It is not the date the letter arrives. It is the date on which the records are actually made available or the "actual institution" of the audit at the place of business—the "boots on the ground" moment, whichever is later.

During this window, multi-GSTIN entities must manage a specific nightmare mentioned on page 109 of the Source: the Electronic Credit Reversal and Reclaimed Statement. Managing these reversals and reclaims across different registrations is notoriously difficult and a prime target for scrutiny. For this, businesses generally rely on proper reconciliation and management of Input Tax Credit (ITC) under GST to minimise mismatches during departmental audits. So make sure that your 15-day checklist includes:

-

Turnover Reconciliation: Matching financial statements (localised) with GSTR-1 and GSTR-3B.

-

ITC Reconciliation: Reconciling GSTR-3B with GSTR-2B, specifically focusing on the "Electronic Credit Reversal and Reclaimed Statement". Accurate reconciliation with GSTR-2B under GST helps businesses identify mismatches and maintain audit-ready compliance records.

-

Electronic Ledgers: Verifying that portal cash/credit ledgers match your internal books for that specific GSTIN.

Takeaway 5: Digital Transparency (The Audit of the Algorithm)

Modern GST audits have evolved from paper-shuffling to a deep dive into your IT ecosystem. Under Section 71, officers have the authority to inspect not just documents but also "computers, computer programs, and computer software".

Under Rule 57(3), taxpayers must provide "passwords for such files and explanation for codes used". This means the auditor is no longer just looking at the invoice; they are auditing the algorithm that generated it. Furthermore, Rule 57(1) requires you to maintain electronic backups so that records can be restored within a "reasonable period". If your IT and tax teams are not in sync before the auditor arrives, your inability to explain proprietary software logic or restore data can be treated as non-compliance.

![]()

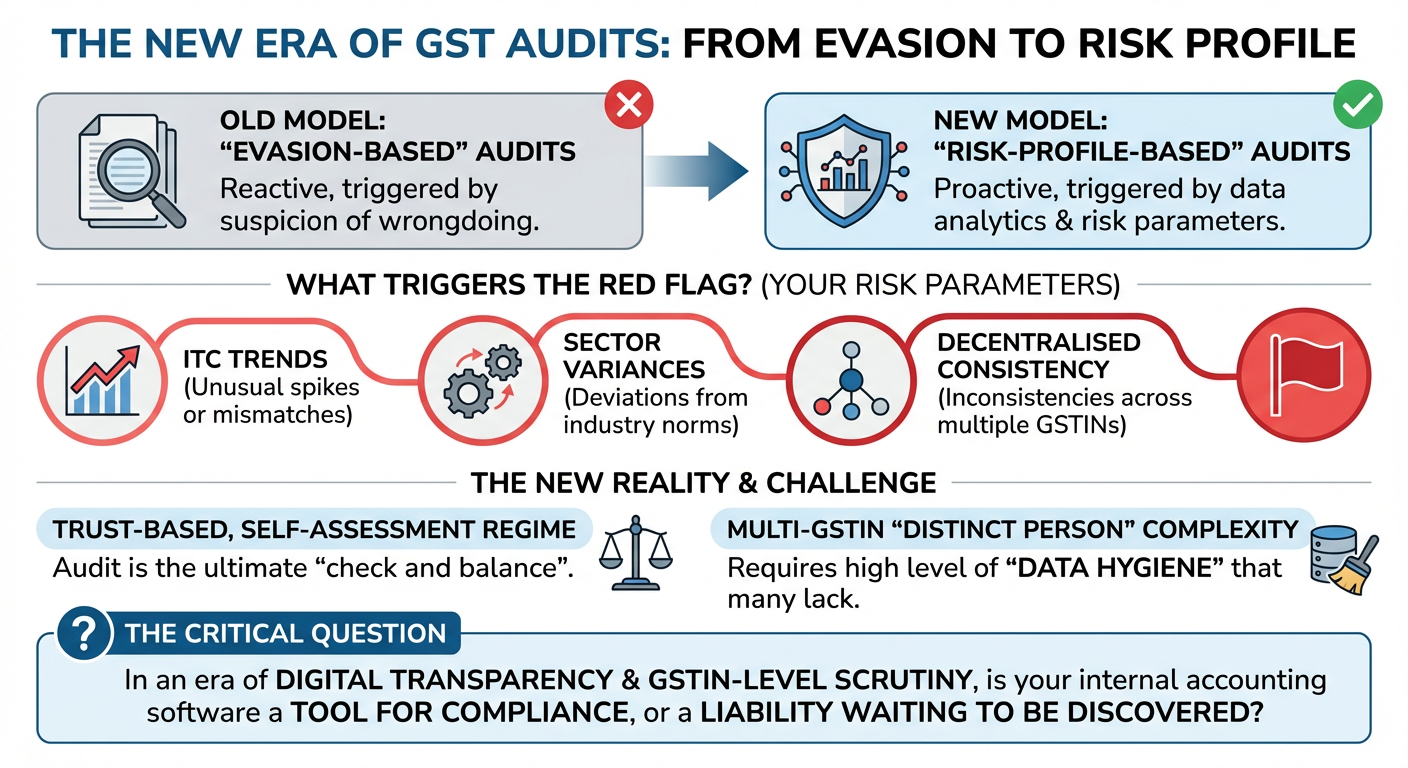

Understanding GST audit risks for businesses with multiple GSTINs

The GST department has moved away from "evasion-based" audits toward a "risk-profile-based" model. Your company's risk parameters—ITC trends, sector variances, and decentralised consistency—are what trigger the red flag.

GST is a trust-based, self-assessment regime, and the departmental audit is the ultimate "check and balance". For the multi-GSTIN entity, the complexity of being a "distinct person" requires a level of data hygiene that many businesses have yet to achieve. That’s why businesses increasingly rely on professional GST return filing services to maintain accurate compliance records across multiple GSTINs.

The Final Question: In an era of digital transparency and GSTIN-level scrutiny, is your internal accounting software a tool for compliance or a liability waiting to be discovered?

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified