Can ITC Be Claimed for Consulting Services Used for Business Expansion?

ITC on Consulting Services | Can ITC Be Claimed for Coinsultancy?

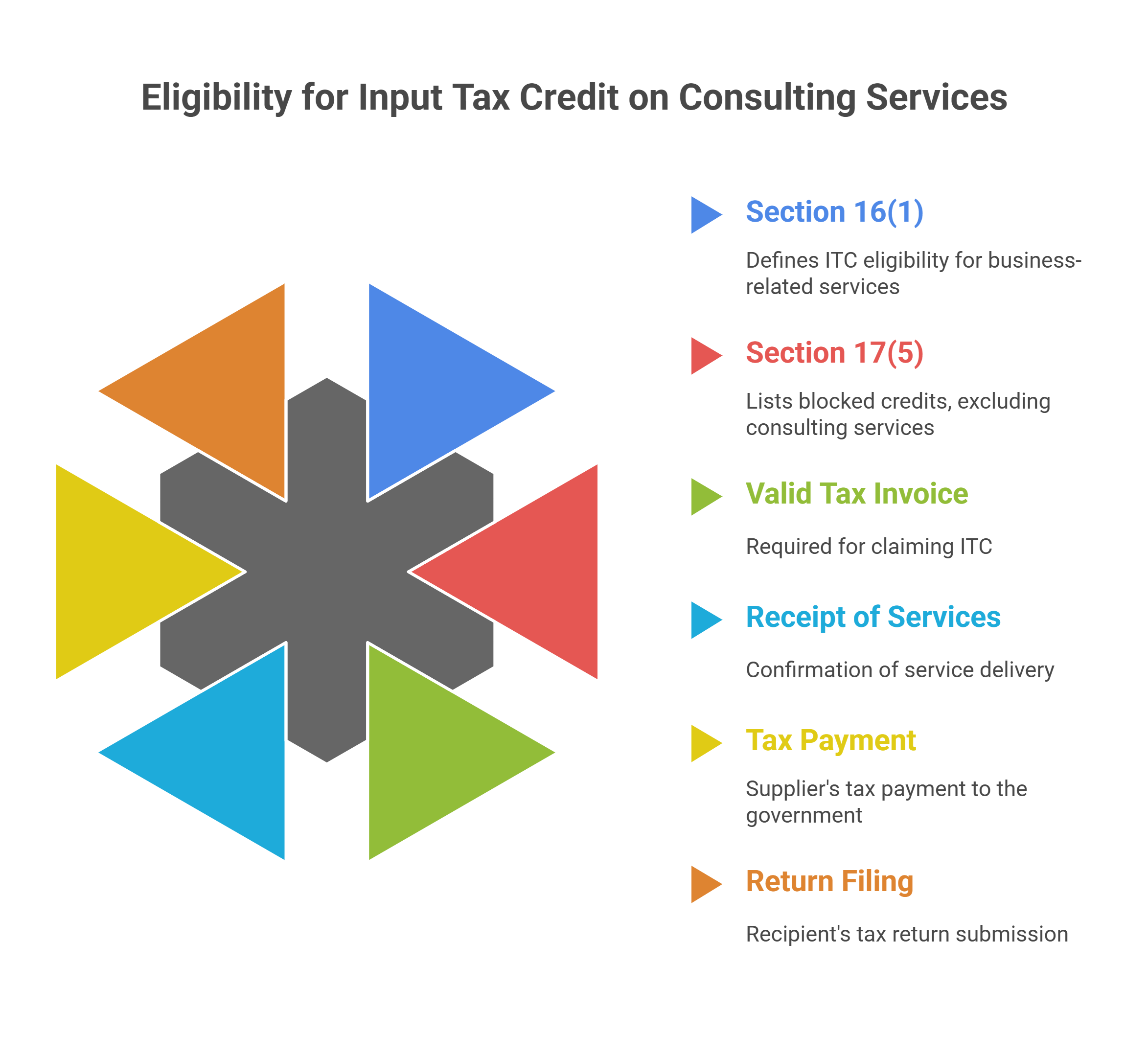

Yes, Input Tax Credit (ITC) can generally be claimed on consulting services used for business expansion. Such services qualify as inputs used in the course or furtherance of business under Section 16(1) of the CGST Act, 2017. Section 17(5) of the Act, which lists specific categories of "blocked credits," does not include general business consulting services. Therefore, provided the other conditions under Section 16 are fulfilled, ITC on such services is admissible.

Detailed Explanation

The admissibility of Input Tax Credit on consulting services for business expansion can be analysed by examining two key provisions of the CGST Act, 2017: Section 16 (Eligibility and conditions for taking ITC) and Section 17(5) (Blocked Credits).

1. Eligibility under Section 16 of the CGST Act

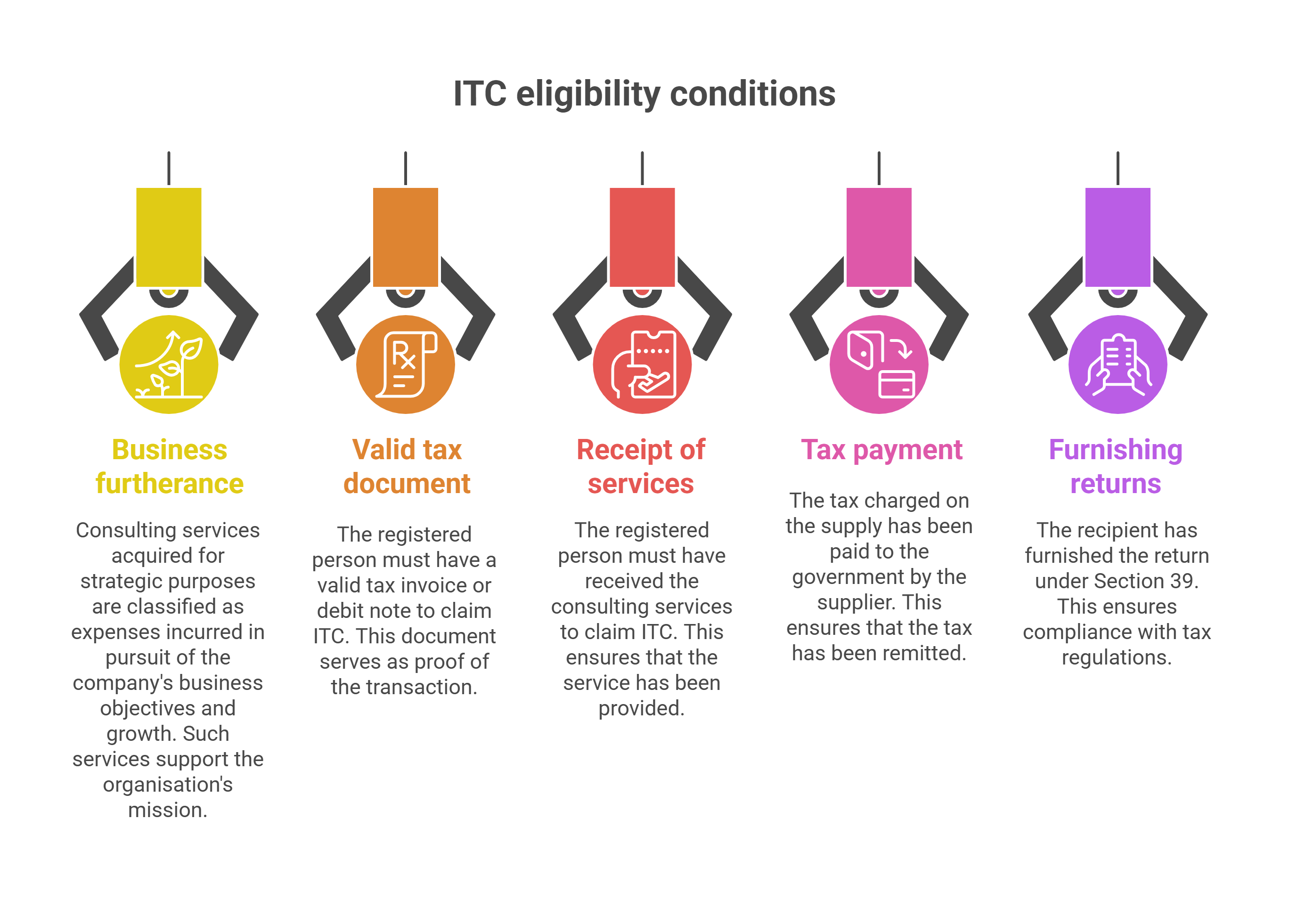

Section 16(1) of the CGST Act lays down the fundamental principle for availing ITC. It states that a registered person is entitled to take credit of input tax charged on any supply of goods or services or both which are used or intended to be used in the course or furtherance of his business.

-

"In the course or furtherance of business": This expression is broad in scope. Consulting services that are acquired for strategic purposes—including, but not limited to, conducting thorough market analysis, enhancing operational efficiency, engaging in meticulous financial planning, or facilitating expansion into new markets—are definitively classified as expenses incurred in pursuit of the company's business objectives and growth. Such services are essential components in supporting and furthering the overall mission and strategic interests of the organisation.

-

Other Conditions: To claim this ITC, the registered person must also satisfy the other conditions stipulated in Section 16, namely:

-

Possession of a valid tax invoice or debit note.

-

Receipt of the consulting services.

-

The tax charged on the supply has been paid to the government by the supplier.

-

The recipient has furnished the return under Section 39.

-

Since consulting services for business expansion meet the primary condition of being used for business purposes, the ITC is prima facie eligible, subject to the restrictions placed under Section 17.

2. Analysis of Section 17(5) - Blocked Credits

Section 17(5) begins with a non-obstante clause, overriding the provisions of Section 16(1). It provides a specific list of goods and services on which ITC is not available, even if they are used in the course or furtherance of business.

.png)

A review of the items listed under Section 17(5) confirms that general business consulting services are not included. The major categories of blocked credits specified in this section are:

-

[Sec 17(5)(a), (aa) & (ab)] Motor vehicles, vessels, and aircraft: ITC is blocked on motor vehicles for transporting persons with a seating capacity of up to thirteen, and on vessels and aircraft.

-

Exception: Credit is available if they are used for further supply, transportation of passengers/goods, or imparting training.

-

-

ITC on related services like general insurance, servicing, and repair is also blocked unless the vehicles/vessels/aircraft are used for the excepted purposes.

+Motor+Vehicle.png)

-

[Sec 17(5)(b)] Specific Supplies:

-

Food and beverages, outdoor catering, beauty treatment, health services, etc.

-

Membership of a club, health, and fitness centre.

-

Travel benefits extended to employees on vacation (e.g., LTC).

-

Exception: ITC is available if an inward supply of a particular category is used for making an outward taxable supply of the same category or as part of a composite/mixed supply.

+specific+supply.png)

-

-

[Sec 17(5)(c) & (d)] Immovable Property:

-

Works contract services for the construction of an immovable property (other than plant and machinery).

-

Goods or services received for the construction of an immovable property (other than plant and machinery) on one's own account.

-

Exception: Credit is available for works contract services if it is an input service for the further supply of works contract services.

+immovable+property.png)

-

-

[Sec 17(5)(fa)] Corporate Social Responsibility (CSR): ITC on goods or services used for activities relating to CSR obligations under Section 135 of the Companies Act, 2013.

+CSR.png)

-

[Sec 17(5)(g) & (h)] Personal Consumption & Disposals:

-

Goods or services used for personal consumption.

-

Goods lost, stolen, destroyed, written off, or disposed of by way of gift or free samples.

+Personal+Consumption+and+disposal.png)

-

-

[Sec 17(5)(i)] Tax Paid under Specific Sections: Tax paid in accordance with the provisions of Section 74 (tax not paid or short paid due to fraud, etc.).

Conclusion

As consulting services for business expansion do not fall into any of the blocked categories under Section 17(5), the credit is not restricted by this provision. Therefore, a registered person is entitled to claim ITC on such services, provided the general conditions of Section 16 are met.

Penalty for Late Gst Registration | Need of GST In India | 16 Digit Invoice Number in GST | GST Inspector Salary | Dry Fruits Hsn Code | GST Maintenance Charges

About the Author

- ★★

- ★★

- ★★

- ★★

- ★★

Check out other Similar Posts

CFO Weekly Digest

A weekly newsletter delivering sharp insights, strategic analysis, and critical updates on business, finance, and compliance — designed exclusively for CFOs and Finance Leaders

Masters India is a GST Suvidha Provider (GSP) appointed by Goods and Services Tax Network (GSTN), a Government of India enterprise.

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301

Procapitus Business Park, 4th Floor, D 247/4A, Sector 63 Rd, Noida, Uttar Pradesh 201301 info@mastersindia.co

info@mastersindia.co

Certified